ISMS 33: Fed Success! High LT Rates & Recession Coming

The post was originally published here.

Listen on

Apple | Google | Spotify | YouTube | Other

Click here to get the PDF with all charts and graphs

Fed Success! High LT Rates & Recession Coming

- World yield curve inversion is falling because of rising LT rates

- Rising LT rates are reducing yield curve inversion fastest in DM Americas and DM Europe

- Rates are high across EMs, crushing in FMs, and low in EM Asia

- France and Germany ST rates rising; DM countries have past peak yield curve inversion due to rising LT rates

- Rates are low in China, which, together with India, never inverted

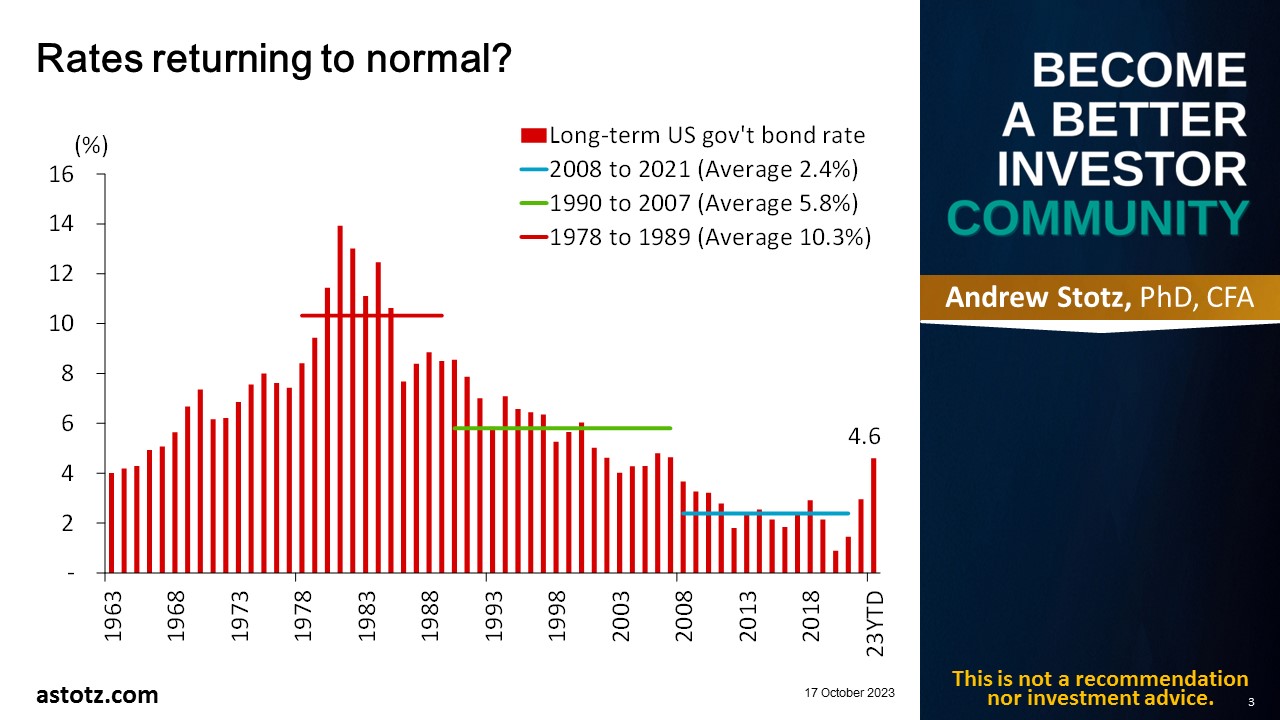

Rates returning to normal?

Irving Fisher (1867 –1947) – One of the earliest American neoclassical economists

- Described as “the greatest economist the United States has ever produced”

- His reputation during his lifetime was irreparably harmed by his public statement, just nine days before the Wall Street Crash of 1929, that the stock market had reached “a permanently high plateau”

- His 1930 treatise, The Theory of Interest, summed up a lifetime’s research into capital, capital budgeting, credit markets, and the factors (including inflation) that determine interest rates

- Some core concepts

- Time Preference – The idea that people generally prefer to have goods and services sooner rather than later

- Real Interest Rate – The real interest rate adjusts for the effects of inflation, allowing for a more accurate evaluation of the purchasing power of money over time

- Fisher Equation – Relates nominal interest rates to real interest rates and inflation

- Expressed as: Nominal Interest Rate = Real Interest Rate + Inflation Rate

- The Fisher Effect – Suggests that nominal interest rates adjust in response to expected changes in inflation

- In other words, if people anticipate higher inflation, nominal interest rates will rise to compensate

Jeremy Siegel (born 1945) Professor of finance at the Wharton School of the University of Penn.

- Comments extensively on the economy and financial markets

- Wrote two books, but most prominent is

- Stocks for the Long Run: The Definitive Guide to Financial Market Returns and Long-Term Investment Strategies

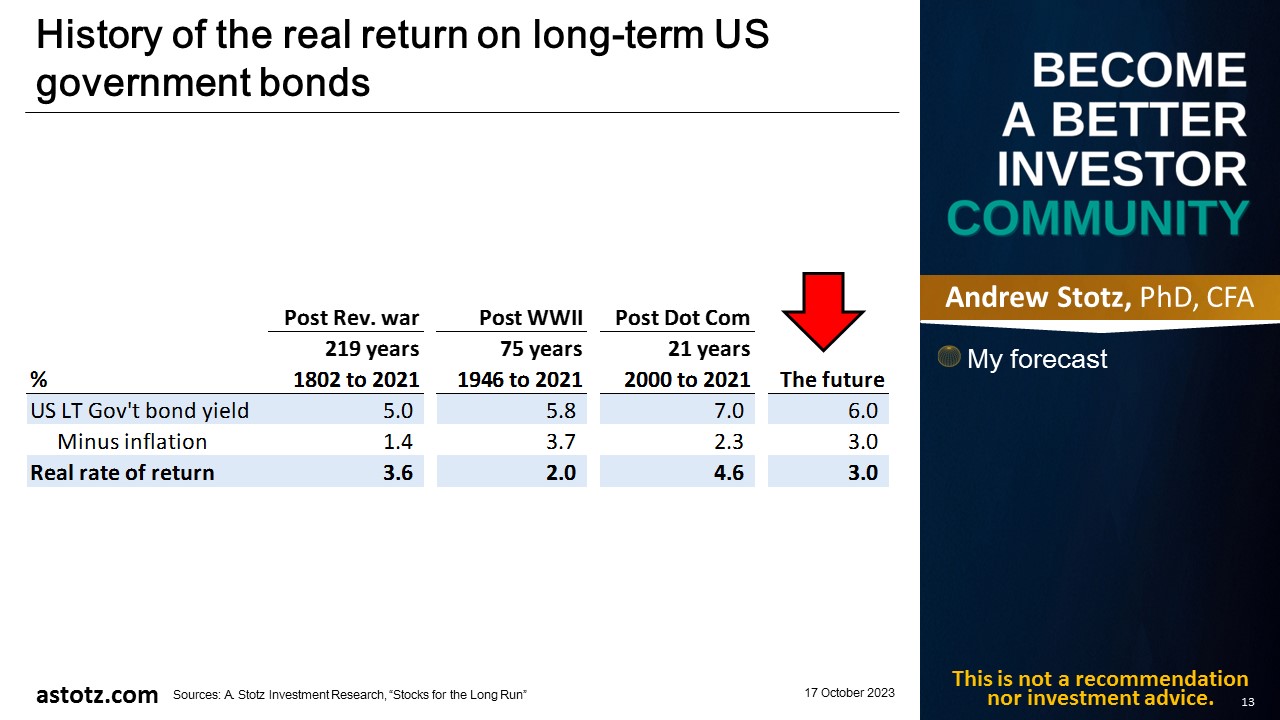

History of the real return on long-term US government bonds

Global Markets

World yield curve inversion is falling because of rising LT rates

Interest rate level – 5.4% world 3m yield, 10yr 4.4%; LT rates much higher in EM

- World 3m rates were 5.4% in Sept., DM rates were 4.4%, and EM rates were 6.9%, a 2.6ppt premium

- World 1yr rates were 5.1% in Sept., DM rates were 4.3%, and EM rates were 6.2%, a 1.9ppt premium

- World 10yr rates were 4.7% in Sept., DM rates were 3.8%, and EM rates were 5.9%, a 2ppt premium

Year-on-year changes – DM 3m yield rose from lower base; fast DM LT rate rise

- 3m yield had a large 2.2ppt YoY rise to 4.4% in DM; there was a smaller 1.4ppt rise in EM

- 1yr rates only increased 0.7ppts YoY in EM; but were up a large 1.4ppt YoY in DM

- 10yr EM rates up only 0.2ppts YoY, DM rates rose by a much higher 0.7ppts

Rate progression – DM tightening has stopped but continues in EM

- 3m rates were flat MoM in DM and are on the rise in EM

- A 0.5ppt MoM rise in EM 1yr yield is raising World yields; DM yield was flat

- Sept 10yr yield rose in both DM and EM, up about 0.4ppts MoM

Yield curve – Rising LT rates pushed world past August peak inversion

- August looks to have been World peak inversion as LT yields have been rising

- World 3m rates rose fast, but now LT rates have started to rise

- May looks to have been DM peak inversion as LT yields start to rise

- 3m DM rates have flattened, but LT rates have been rising, reducing yield curve inversion

- August looks to have been EM peak inversion as LT yields have been rising

- After a year of significant rises in EM ST rates, LT rates have started rising, reducing inversion

Key points and the bottom line

- 5.4% world 3m yield, 10yr 4.4%; LT rates much higher in EM

- DM 3m yield rose from lower base; fast DM LT rate rise

- DM tightening has stopped but continues in EM

- Rising LT rates pushed world past August peak inversion

- World yield curve inversion is falling because of rising LT rates

Developed Market Regions

Rising LT rates are reducing yield curve inversion fastest in DM Americas and DM Europe

Interest rate level – High DM Americas rates, EM Europe lower, and DM Pacific much lower

- DM Americas 3m rates were 5.4% in Sept, DM Europe rates were 4.0%, DM Pacific rates were 1.4%

- DM Americas 1yr rates were 5.5% in Sept, DM Europe rates were 3.7%, DM Pacific rates were 1.6%

- DM Americas 10yr rates were 4.5% in Sept, DM Europe rates were 3.6%, DM Pacific rates were 2.1%

Year-on-year changes – ST rates rising in DM Europe, LT rates rising in DM Americas

- 2.8ppts YoY 3m rate rise in DM Europe, to 4%; up only 0.5ppt to a low 1.4% in DM Pacific

- DM Americas and Europe had a high 1.5ppt rise in 1yr rate; 0.5ppt in DM Pacific to a low 1.6%

- DM Americas had the highest rise in 10yr yields, up 0.8ppts, but other regions are rising as well

Rate progression – Rates hardly moved MoM across all DM regions

- DM Europe central bank tightening drove fast 3m rate YoY rise; rates flat MoM in all DM regions

- 1yr rate barely moved MoM in all DM regions

- 10yr yield rising fastest MoM in DM Americas and Europe, slow MoM rise in DM Pacific

Yield curve – Rising LT rates in DM Americas and Europe flattening yield curve; normal in DM Pacific

- DM Americas inversion peaked in May 2023; LT rate rise reduced inversion by 0.5ppts MoM

- DM Europe yield curve inversion peaked a bit later, in August, and fell MoM due to LT rate rise

- DM Pacific yield curve never inverted as it never went through a US Fed-style hiking cycle

Key points and the bottom line

- High DM Americas rates, EM Europe lower, and DM Pacific much lower

- ST rates rising in DM Europe, LT rates rising in DM Americas

- Rates hardly moved MoM across all DM regions

- Rising LT rates in DM Americas and Europe flattening yield curve; normal in DM Pacific

- Rising LT rates are reducing yield curve inversion fastest in DM Americas and DM Europe

Emerging Market Regions

Rates are high across EMs, crushing in FMs, and low in EM Asia

Interest rate level – ST EM rates high, ranging from 12% to 35%, but a low 3.2% in EM Asia

- EM Americas 3m rates were 11.9% in Sept, EM Asia rates were 3.2%, EM Europe rates were 11.6%, EM ME&A rates were 15.7%, Frontier rates were 33.5%

- EM Americas 1yr rates were 11.3% in Sept, EM Asia rates were 3.1%, EM Europe rates were 15.2%, EM ME&A rates were 25.2%, Frontier rates were 16%

- EM Americas 10yr rates were 11% in Sept, EM Asia rates were 3.6%, EM Europe rates were 12.5%, EM ME&A rates were 17.5%, Frontier rates were 11%

Year-on-year changes – ST rates in FM and EM ME&A are up, LT rates are rising fast in EM Europe

- Biggest YoY rise of 3m yields in Frontier markets, up 10.6ppt, and EM ME&A up 4.6ppt

- 1yr yield rose most YoY in EM ME&A, up 7.4ppt and EM Europe up 5.2ppt

- 10yr yields flat YoY in EM Americas; 3.2ppt rise in EM Europe and 2.9ppt rise in EM ME&A

Rate progression – FM ST rates up massively, but flat MoM, LT rates rising in EM Europe

- 3m rates up MoM in EM Europe; down in super high FMs and high EM Americas; flat in EM Asia

- 1yr yields show significant rise in EM Europe; High in EM ME&A; Low in EM Asia

- LT rates are up across EMs, rising particularly fast MoM in EM Europe, low and flat in EM Asia

Yield curve – Inversion massive in FM, falling in EM Americas; normal in EM Asia, Europe, and EM ME&A

- EM Americas yield curve inverted slightly more than World; but peaked in June 2023

- EM ME&A yield curve never inverted as ST rates have always been high

- Frontier yield curve inversion peaked in August 2023, but crushing ST rates remain

Key points and the bottom line

- ST EM rates high, ranging from 12% to 35%, but a low 3.2% in EM Asia

- ST rates in FM and EM ME&A are up, LT rates are rising fast in EM Europe

- FM ST rates up massively, but flat MoM, LT rates rising in EM Europe

- Inversion massive in FM, falling in EM Americas; normal in EM Asia, Europe, and EM ME&A

- Rates are high across EMs, crushing in FMs, and low in EM Asia

Developed Countries

France and Germany ST rates rising; DM countries have past peak yield curve inversion due to rising LT rates

Interest rate level – US/UK have 5.5% ST and 4.6% LT rates, Germany and France lower at 3.6%

- US 3m rates were 5.5% in Sept, Japanese rates were 0.2%, German rates were 3.6%, UK rates were 5.4%, French rates were 3.8%

- US 1yr rates were 5.5% in Sept, Japanese rates were zero, German rates were 3.7%, UK rates were 5.1%, French rates were 3.8%

- US 10yr rates were 4.6% in Sept, Japanese rates were 0.8%, German rates were 2.8%, UK rates were 4.4%, French rates were 3.4%

Year-on-year changes – ST rates are rising fast in France and Germany, LT rates rising most in the US

- Fastest YoY 3m yield rise in France and Germany, up about 3ppt; no change in Japan

- 1yr yield up about 2ppts in France and Germany; Japan flat

- Biggest 10yr yield rise in the US, followed by France and Germany

Rate progression – MoM LT rates rising in the US, Germany, France, UK and Japan are flat MoM

- 3m rates rose most in France and Germany; US and UK have steadied; Japan remains flat

- 1yr rates rose most in France and Germany; US is rising MoM; Japan remains flat

- LT rates are up half ppt in the US, Germany, and France; even Japan has been rising

Yield curve – Germany, UK, and France passed peak inversion in Aug; US passed in May

- US yield curve inversion peaked in May 2023; 10yr rates rose by 50bp MoM in Sep 2023

- Japan had a tiny MoM 0.1ppt increase in both short and long-term rates, never inverted

- The deepest inversion in Germany was Aug 2023; rising LT rates have reduced inversion

- The deepest inversion in the UK was Aug 2023; tiny LT rate rise, and tiny ST rate fall MoM

- The deepest inversion in France was Aug 2023; LT rates up 4bp MoM

Key points and the bottom line

- US/UK have 5.5% ST and 4.6% LT rates, Germany and France lower at 3.6%

- ST rates are rising fast YoY in France and Germany, LT rates rising most in the US

- LT rates rising MoM in the US, Germany, France; UK and Japan are flat MoM

- Germany, UK, and France just passed peak inversion in Aug; US passed in May

- France and Germany ST rates rising; DM countries have past peak yield curve inversion due to rising LT rates

Emerging Countries

Rates are low in China, which, together with India, never inverted

Interest rate level – Low 2-4% rates in China and Korea, 7% in India, and 12% in Russia and Brazil

- Chinese 3m rates were 2.3% in Sept, Indian rates were 6.9%, Korean rates were 3.6%, Russian rates were 12.4%, Brazilian rates were 12.3%

- Chinese 1yr rates were 2.2% in Sept, Indian rates were 7%, Korean rates were 3.6%, Russian rates were 16.5%, Brazilian rates were 11%

- Chinese 10yr rates were 2.7% in Sept, Indian rates were 7.2%, Korean rates were 4%, Russian rates were 12.9%, Brazilian rates were 11.7%

Year-on-year changes – ST rates in China, India, and Korea up less than 1ppt, LT rates flat; rates rising in Russia

- 3m yield up most YoY in India and Korea, followed by China; down in Brazil

- 1yr yield was up most YoY in Russia, down in Brazil

- 10yr yield was down a bit YoY in China, India, Korea, and Brazil; up only in Russia

Rate progression – Yields are flat in China, India, and Korea, rising in Russia and falling in Brazil

- 3m yield flat MoM in India, Korea, and Russia; rising a bit MoM in China, falling in Brazil

- 1yr yield rising fast in Russia; down MoM in India and Brazil

- 10yr yield was up YoY only in Russia but up MoM slightly in China, India, Korea, & Brazil

Yield curve – Yield curves never inverted in China and India; Russia’s inversion stopped; Brazil passed inversion peak

- China never inverted; ST rates were up 30bps MoM, LT rates were up only 10bps

- India never inverted; nearly flat yield curve has remained unchanged MoM

- Korea saw a brief and mild inversion in Jan 2023; slight MoM steepening w/ LT rates up

- Peak Russian inversion Oct 2022; LT rates up nearly 1ppt MoM

- Peak Brazil yield curve inversion in Jun 2023; nearly equal MoM fall in ST rates and rise in LT

Key points and the bottom line

- Low 2-4% rates in China and Korea, 7% in India, and 12% in Russia and Brazil

- ST rates in China, India, and Korea are up less than 1ppt, LT rates flat; rates rising in Russia

- Yields are flat in China, India, and Korea, rising in Russia and falling in Brazil

- Yield curves never inverted in China and India; Russia’s inversion stopped; Brazil passed peak

- Rates are low in China, which, together with India, never inverted