A. Stotz All Weather Strategies – July 2022

Executive summary

- Global upheaval as ESG policies backfire

- Fed hiked 0.75% and the definition of a recession was changed

- The ECB hiked 0.50% and EU fights internally. German energy crisis appears inevitable

- China reported weak numbers, worsening global slowdown concerns

- Central bankers appear to be raising rates into a recession to stifle inflation

- We see opportunities to allocate to sectors and countries within equity, e.g., World Energy and India

- Demand for necessities (food and energy), inflation, and supply-chain disruptions are going to drive the asset class higher

- Bonds and Gold to protect capital

The All Weather Strategy is available in Thailand through FINNOMENA. If you’re interested in our allocation strategy, you can also join the Become a Better Investor Community. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

What happened in world markets in July 2022

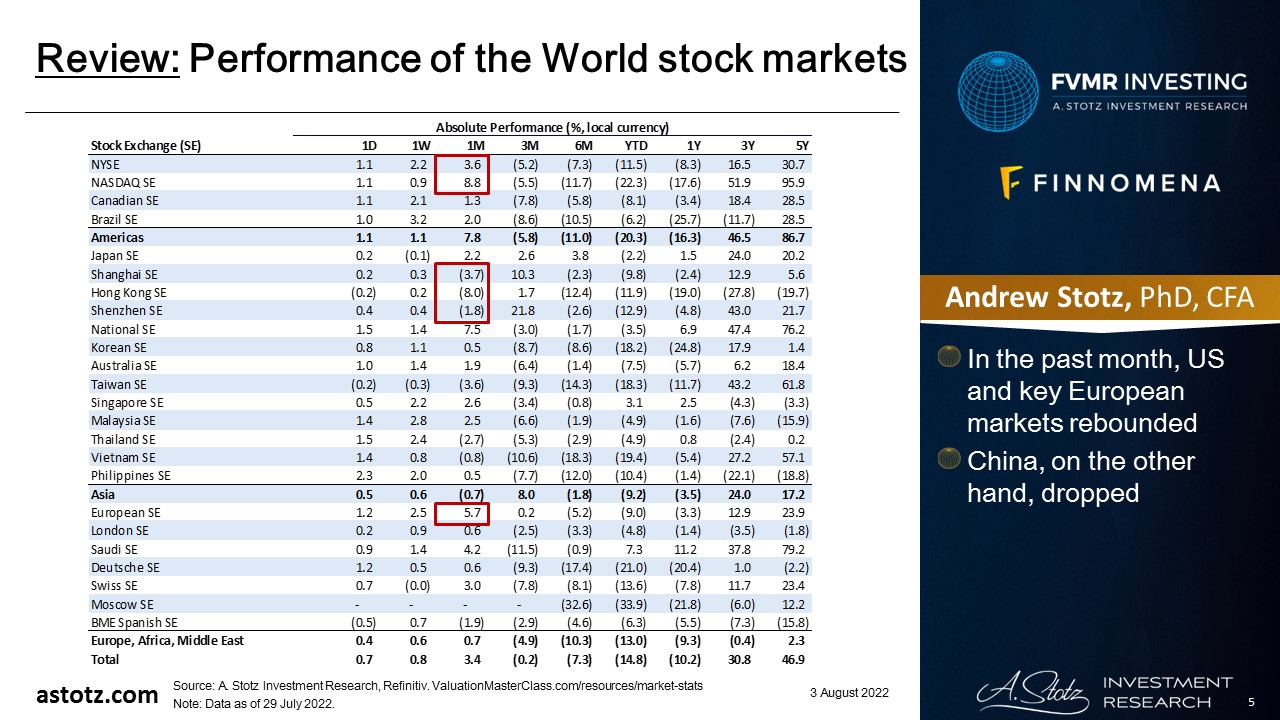

Performance of the World stock markets

- In the past month, US and key European markets rebounded

- China, on the other hand, dropped

Find the updated Performance of the World stock markets here.

ESG policies backfire

There are currently three countries in the world with an ESG score over 90:

Sri Lanka, where government just collapsed.

Ghana, where the national power supply has shut down.

Netherlands, where farmers have revolted against the state

Green energy is a deadlier virus than covid

— Michael Seifert (@realmichaelseif) July 15, 2022

Sri Lanka has seen massive protests

NOW – Protesters storm the presidential palace in Sri Lanka’s capital.pic.twitter.com/Wv6oQ10kBQ

— Disclose.tv (@disclosetv) July 9, 2022

Protests in Ghana due to soaring prices

Protests against high cost of living in Accra, Ghana turn violent. Some “Arise Ghana” protestors threw rocks, stones + burnt tyres. police firing tear gas and using water canon. Chaos.

— will ross (@willintune) June 28, 2022

Dutch farmers protest the government’s policy to reduce nitrogen emissions

Dutch farmers are still protesting over being made to cut down on their production in the name of climate mandates, according to Sky News host James Morrow.https://t.co/lmLM8esa2O

— Sky News Australia (@SkyNewsAust) July 31, 2022

- Sri Lanka, Ghana, and Netherlands are just a few examples of countries that have seen protests and upheaval

- Numerous, especially emerging, countries have seen protests due to massive price increases

The uproars highlight the divides between the politicians and the people

— Rothmus 🏴 (@Rothmus) July 29, 2022

Fed hiked another 0.75%

BREAKING: The Federal Reserve raised its benchmark interest rate by a hefty three-quarters of a point for a second straight time in its most aggressive drive in three decades to tame high inflation. https://t.co/sIsRWx1z3l

— The Associated Press (@AP) July 27, 2022

2Q22 US GDP contracted and US has entered recession

BREAKING: The US is now officially in a recession after two consecutive quarters of negative GDP growth.#Bitcoin is the escape hatch

— Bitcoin Magazine (@BitcoinMagazine) July 28, 2022

Or has US entered a recession?

Old definition of recession. pic.twitter.com/cfIxp7R5qB

— Wall Street Silver (@WallStreetSilv) July 28, 2022

The White House decided to change the definition of a recession

The Biden Administration is redefining “recession” in an effort to avoid political backlash.

It’s not a recession if you change the definition of recession.

Soviet-level propaganda from a soviet-level regime. pic.twitter.com/bXtvPpOeD8

— BowTiedRanger (@BowTiedRanger) July 24, 2022

Yellen sounds optimistic about the US economy

US TREASURY SECRETARY YELLEN: THE US ECONOMY HAS ENTERED A NEW PHASE CHARACTERISED BY STEADY, SUSTAINED GROWTH.

— Breaking Market News ⚡️ (@financialjuice) July 28, 2022

- She follows suit and disagrees, saying the US is not in a recession

- According to the new definition of course

One thing we know, is that you seldom resolve problems by denying them

Fed Chair Powell admits that he was wrong again

Powell: ”I don’t think I would do that again. I don’t think I would keep policy so accommodative again as inflation was already picking up as we did in 2021”

This mistake will leave long-lasting scars on Central Bankers – and it matters a lot for macro & markets looking ahead

— Alf (@MacroAlf) July 27, 2022

Are they being wrong on purpose?

It’s true. 🤣 pic.twitter.com/3evWVmZP8Y

— Markets & Mayhem (@Mayhem4Markets) July 16, 2022

- The Fed was wrong about inflation

- Is the Fed just trying to manage market expectations with its communications?

- Will the “soft landing” succeed or will Fed crash the market?

ECB hiked 0.50%, which was more surprising than the Fed’s hike

When it comes to Europe, the ECB hiked 50 bps and the chart below shows what happened to Bund yields

A timid attempt at pricing higher yields followed by a rapid decline

Also in EU, bond markets are screaming: the more you tighten now, the more you’ll have to ease later

13/ pic.twitter.com/PJPdYahhDm

— Alf (@MacroAlf) July 22, 2022

ECB’s new tool has been a failure so far

Despite the ECB’s rolling out of a new tool last week to prevent fragmentation, Italian bonds are still yielding considerably more than German notes. The spread on 2-year maturities is still near the widest levels since the height of the pandemic, in 2020. pic.twitter.com/fUqrG0UFL4

— Lisa Abramowicz (@lisaabramowicz1) July 26, 2022

- The purpose of the anti-fragmentation tool is to avoid large spreads between EU members’ bonds

- Which has clearly not been accomplished yet

The anti-fragmentation tool has led to internal fighting

Germans are already preparing to sue the ECB on the new anti-fragmentation tool

Its open-ended nature & skew towards weaker countries makes it prone to be labeled as direct debt financing (illegal under EU laws)

A prime example of how poor is the current Eurozone’s architecture

— Alf (@MacroAlf) July 29, 2022

The EU fights about energy too

NORTH vs SOUTH 2.0:

Spain, Greece and Portugal reject the EU call for 15% cuts in natural gas consumption to help Germany

Spanish Energy Minister (clearly aiming at Berlin): “Contrary to other countries, Spain hasn’t been living beyond its means in energy terms”#EnergyCrisis

— Javier Blas (@JavierBlas) July 21, 2022

Germany says to stop coal and oil imports from Russia

#Germany will completely stop buying Russian #coal on Aug. 1 and Russian #oil on Dec. 31

Russian currently supplies 40% of Germany’s coal and 40% of its oilhttps://t.co/0rYZg0JgOL

— Tracy (𝒞𝒽𝒾 ) (@chigrl) July 13, 2022

Russia cuts gas supplies to Europe

Here we go: Force Majeure 👇 pic.twitter.com/30Ivq7KojP

— Gianluca (@MenthorQpro) July 18, 2022

- Russia has countered EU sanctions by saying its unable to deliver gas through Nord Stream

Will the oil just be rerouted through Saudi Arabia?

Saudia Arabia now buys cheap Russian oil, so it can sell its own oil to the West.

Russia wins, Saudia Arabia wins, and the west loses.https://t.co/cjfuLW8hlN

— Fabian Wintersberger (@f_wintersberger) July 15, 2022

It’s clear that Germany is headed for an energy crisis

This horror chart suggests that #Germany is heading for a huge energy crisis. Not only are gas prices near record highs, but electricity prices in particular are signaling stress. pic.twitter.com/8zxueSGhxh

— Holger Zschaepitz (@Schuldensuehner) July 27, 2022

Politicians ask citizens to brace themselves

⚠️ In Germany, politicians warn citizens to be prepared for blackouts, gas shortages and energy bills of 1500€ – 3000€. A disaster waiting to happen.

— Marc-André Fongern (@Fongern_FX) July 19, 2022

Basics may become luxury

German parties this winter pic.twitter.com/58kyURbLKD

— Tourist (@AssetTraveller) July 7, 2022

China GDP came in weaker than expected

*CHINA 2Q GDP GROWS 0.4% Y/Y; EST. 1.2%

*CHINA JUNE RETAIL SALES RISE 3.1% Y/Y; EST. 0.3%

*CHINA JAN.-JUNE FIXED INVESTMENT RISES 6.1% Y/Y; EST. 6%

*CHINA JUNE INDUSTRIAL OUTPUT RISES 3.9% Y/Y; EST. 4%— zerohedge (@zerohedge) July 15, 2022

Reports about bank runs in China

BANK OF CHINA IN ZHENGZHOU

pic.twitter.com/Vccs1K1Jsb— INVESTMENT HULK (@INVESTMENTSHULK) July 10, 2022

Though, the printer goes brrr!

Chinese M2 growth printing at 11.4% in June!

This is GOOD news for the global economy in 12 months from now pic.twitter.com/mzolFad3fk

— AndreasStenoLarsen (@AndreasSteno) July 11, 2022

Keep in mind China’s size

To put things in perspective, the Chinese real estate market is the biggest single asset class in the world with an estimated market value of roughly $55 trillion (as per Dec 2021).

Larger than the US stock market.

Chinese real estate output just shrank by 7% YoY in Q2.

— Alf (@MacroAlf) July 18, 2022

Key takeaways

- Global upheaval as ESG policies backfire

- Fed hiked 0.75% and the definition of a recession was changed

- The ECB hiked 0.50% and EU fights internally

- German energy crisis appears inevitable

- China reported weak numbers, worsening global slowdown concerns

Performance review: All Weather Inflation Guard

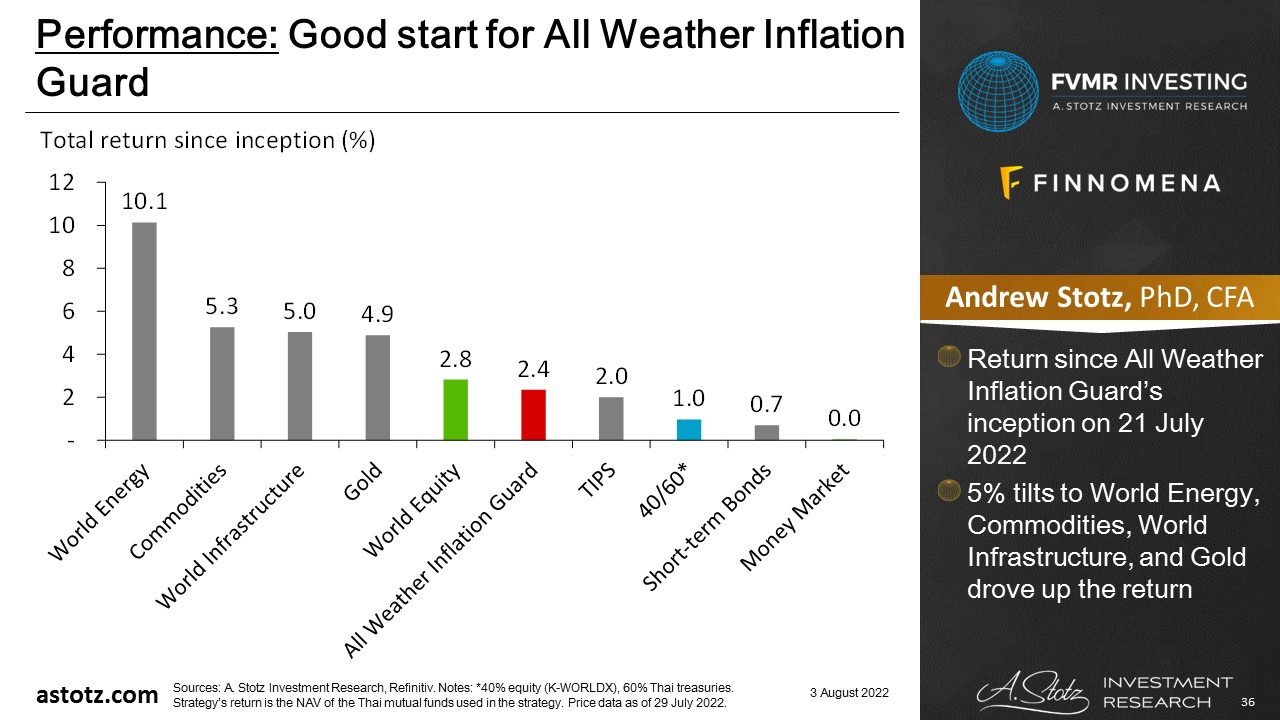

Good start for All Weather Inflation Guard

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- Return since All Weather Inflation Guard’s inception on 21 July 2022

- 5% tilts to World Energy, Commodities, World Infrastructure, and Gold drove up the return

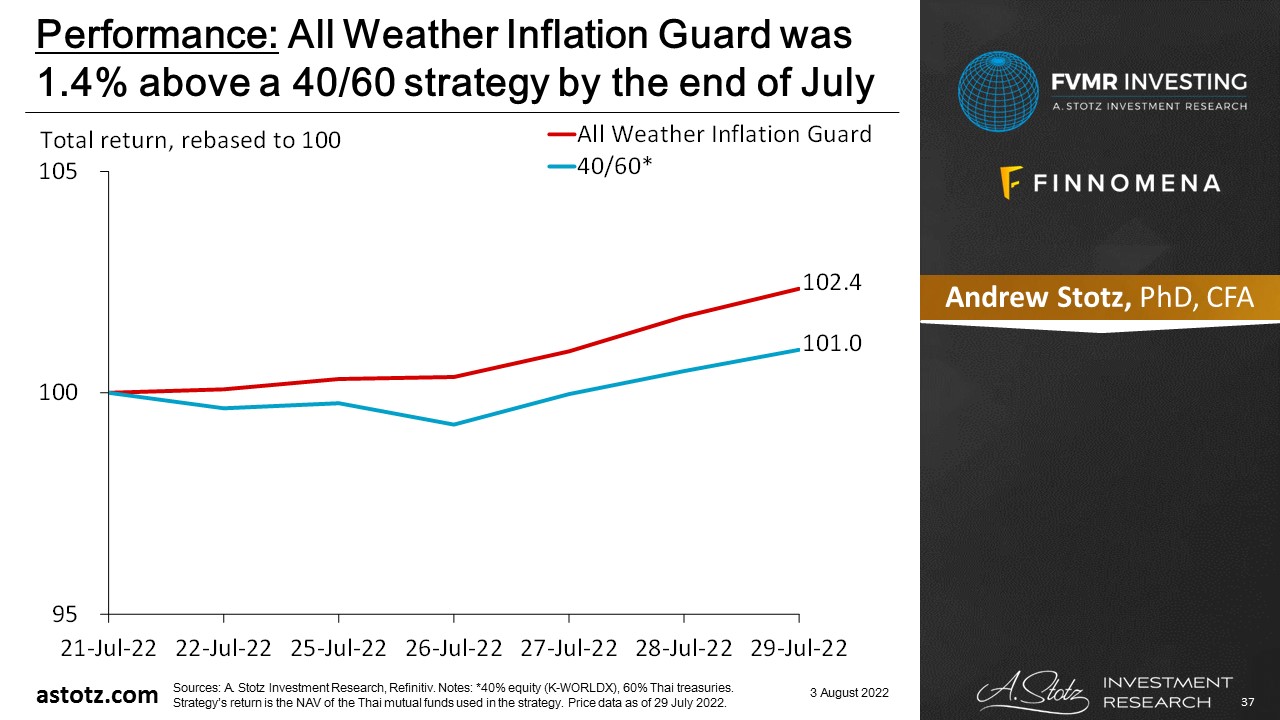

All Weather Inflation Guard was 1.4% above a 40/60 strategy by the end of July

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- All Weather Inflation Guard had only been up and running for a bit more than a week

- The strategy was 1.4% above a 40/60 portfolio by the end of July 2022

Performance review: All Weather Strategy

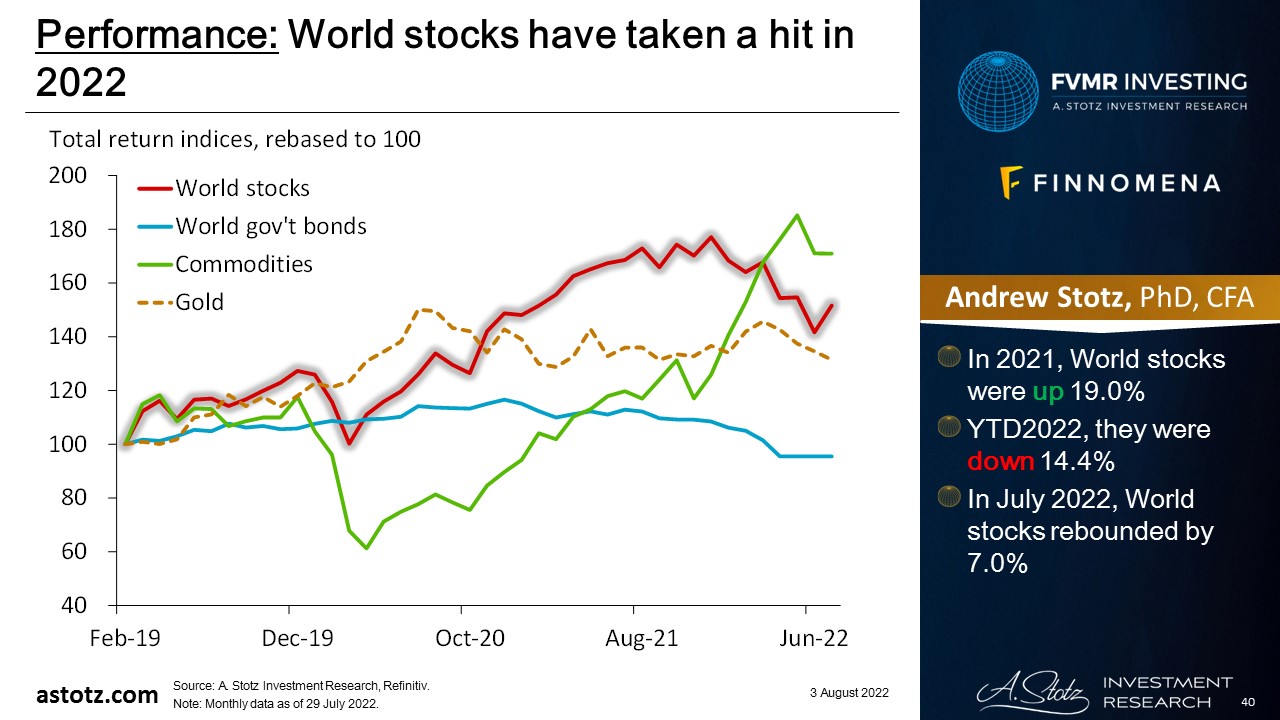

World stocks have taken a hit in 2022

- In 2021, World stocks were up 19.0%

- YTD2022, they were down 14.4%

- In July 2022, World stocks rebounded by 7.0%

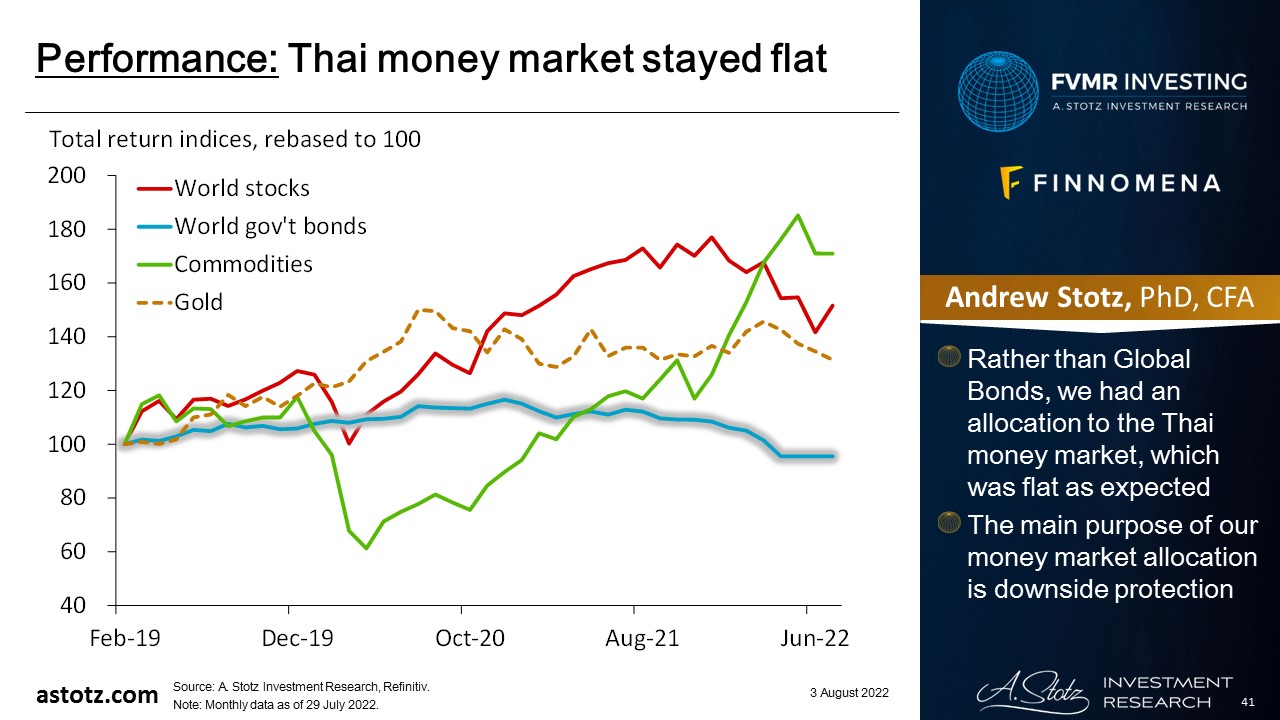

Thai money market stayed flat

- Rather than Global Bonds, we had an allocation to the Thai money market, which was flat as expected

- The main purpose of our money market allocation is downside protection

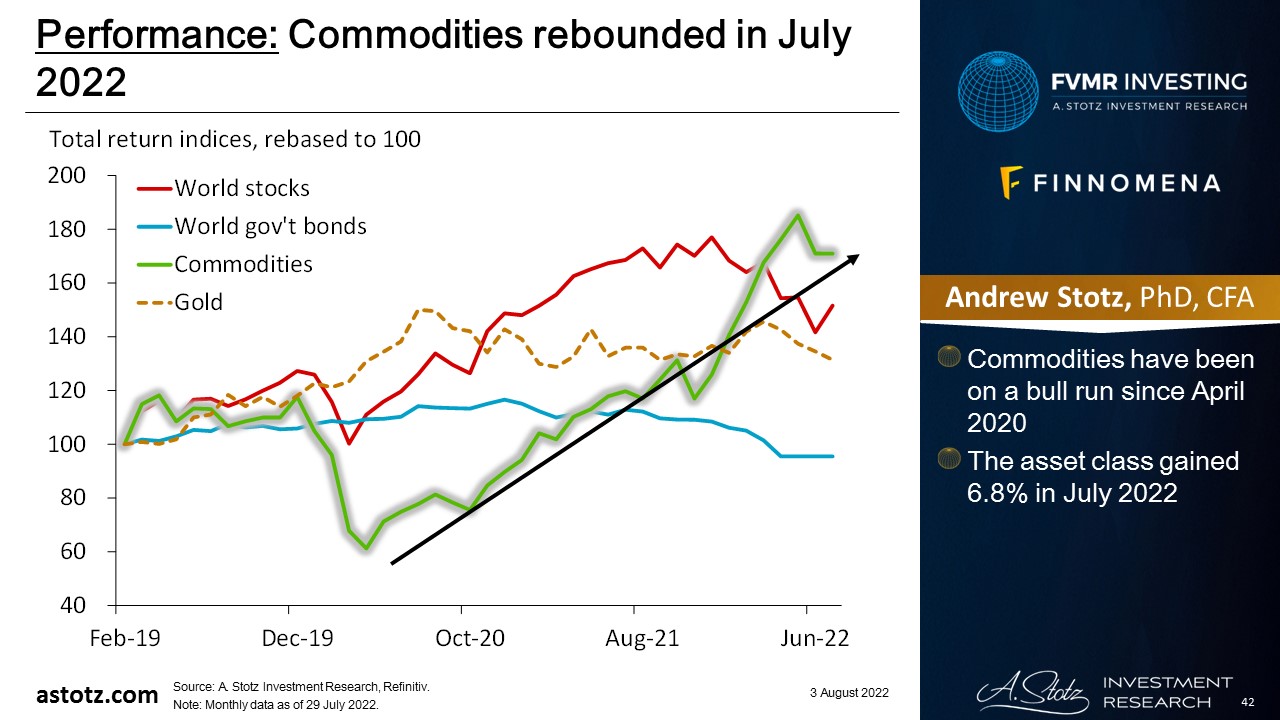

Commodities rebounded in July 2022

- Commodities have been on a bull run since April 2020

- The asset class gained 6.8% in July 2022

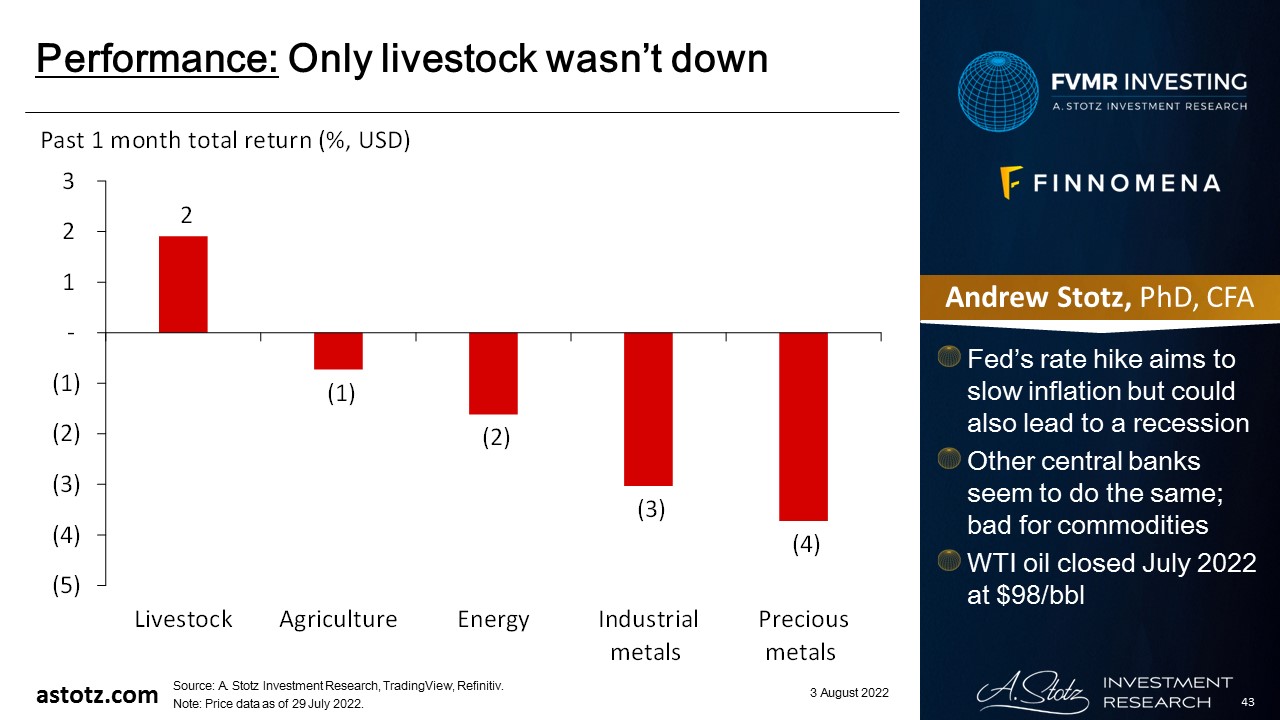

Only livestock wasn’t down

- Fed’s rate hike aims to slow inflation but could also lead to a recession

- Other central banks seem to do the same; bad for commodities

- WTI oil closed July 2022 at $98/bbl

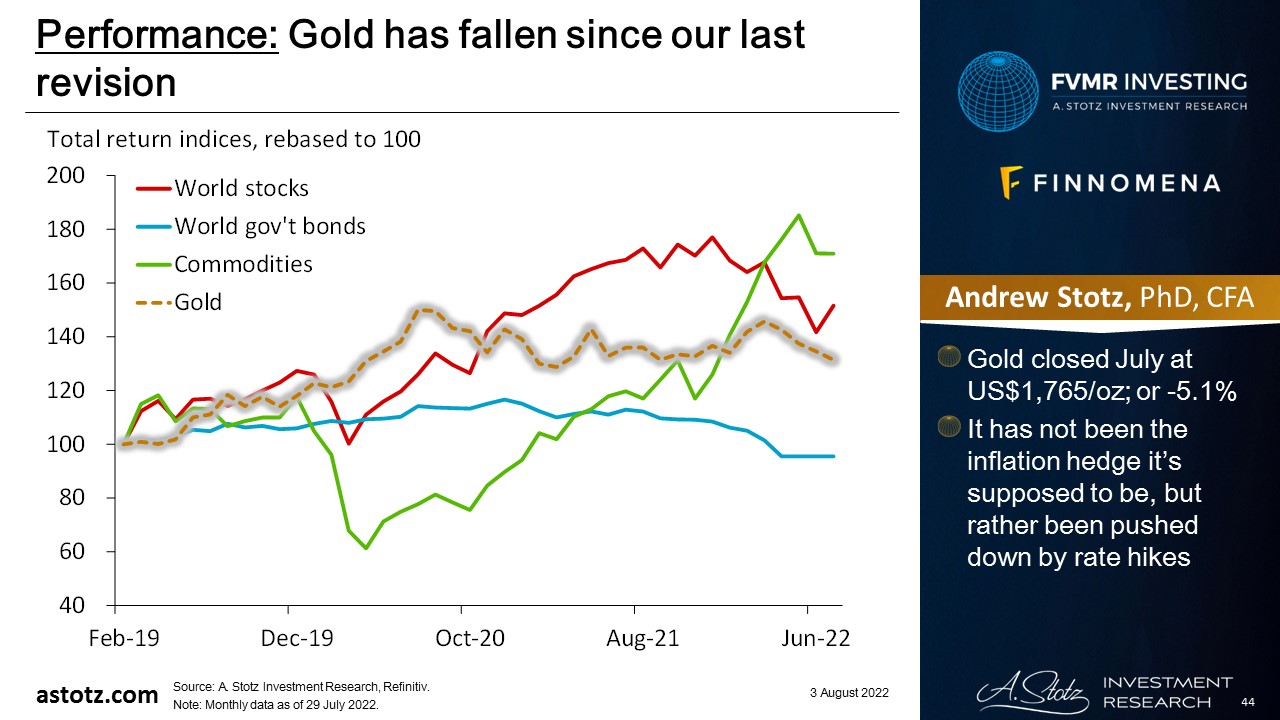

Gold has fallen since our last revision

- Gold closed July at US$1,765/oz; or -5.1%

- It has not been the inflation hedge it’s supposed to be, but rather been pushed down by rate hikes

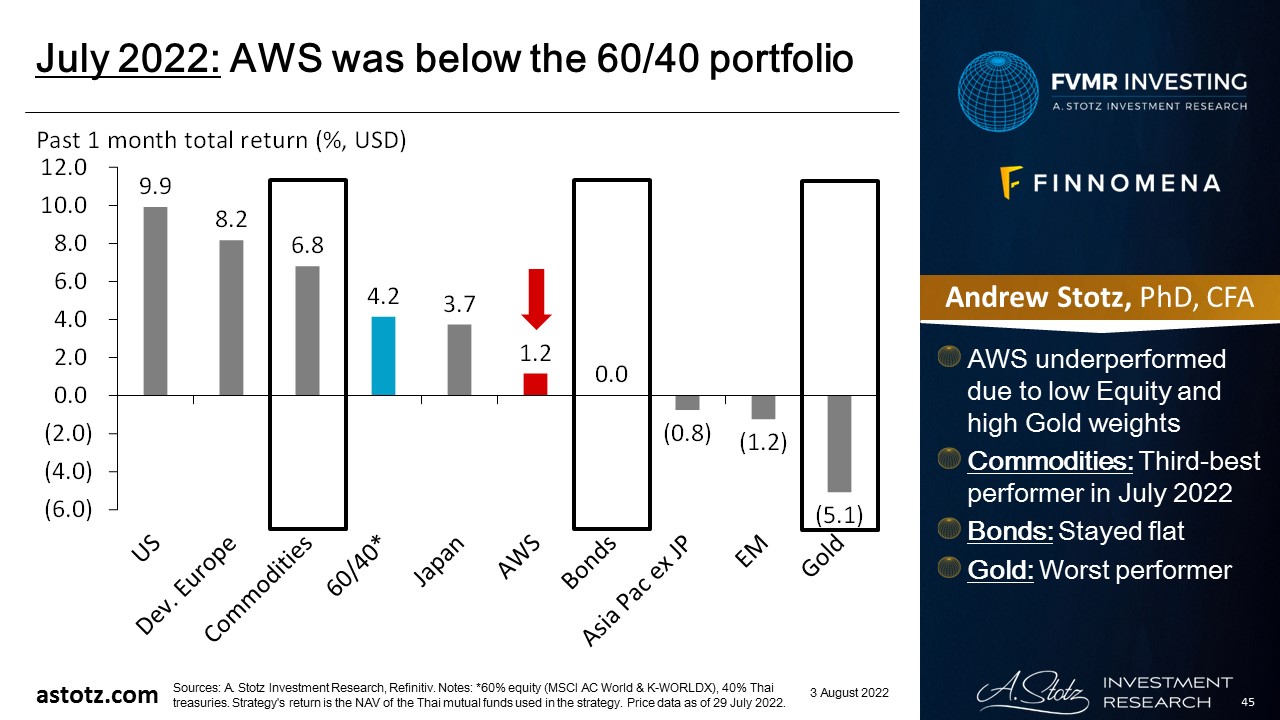

AWS was below the 60/40 portfolio

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- AWS underperformed due to low Equity and high Gold weights

- Commodities: Third-best performer in July 2022

- Bonds: Stayed flat

- Gold: Worst performer

Since inception: Above a traditional 60/40 portfolio

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- Since inception, the strategy was 7.4% above a 60/40 portfolio by the end of July 2022

AWS has performed well

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

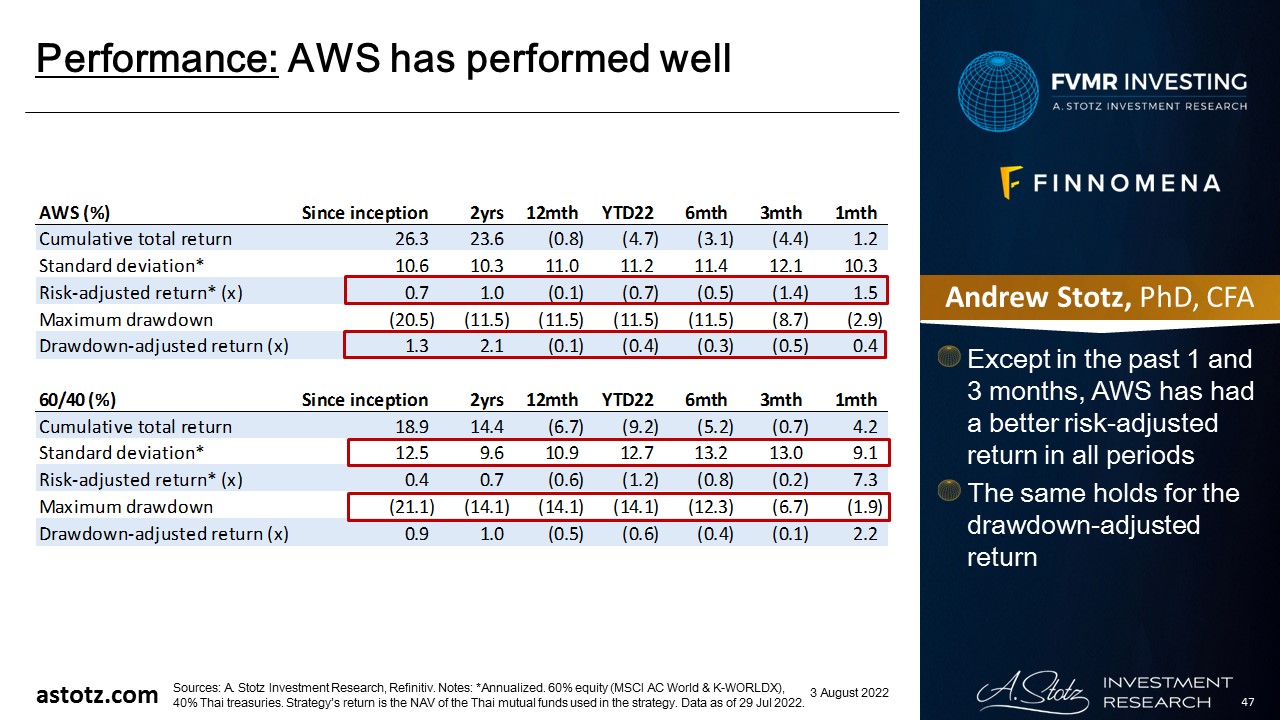

- Except in the past 1 and 3 months, AWS has had a better risk-adjusted return in all periods

- The same holds for the drawdown-adjusted return

AWS has experienced less volatility than a 60/40

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- Mostly 25-65% target weight for equity has reduced volatility

- Since gold is generally uncorrelated to equity, it has reduced the overall AWS volatility

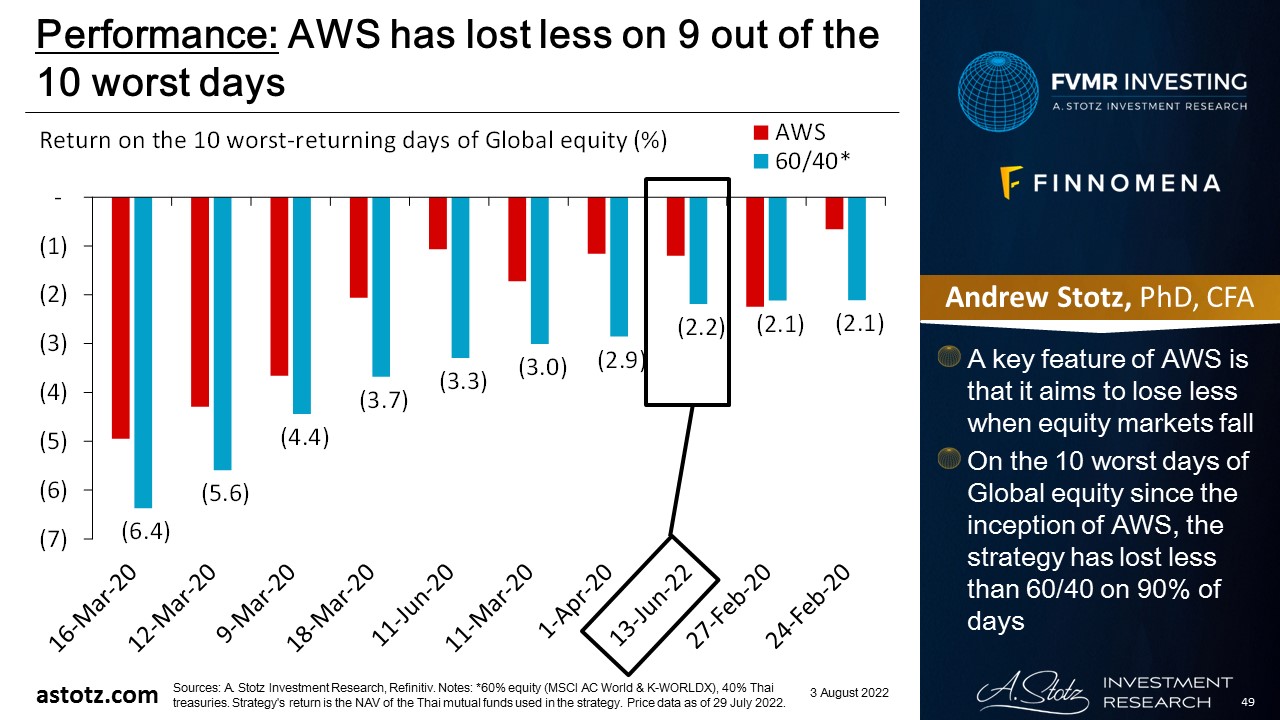

AWS has lost less on 9 out of the 10 worst days

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- A key feature of AWS is that it aims to lose less when equity markets fall

- On the 10 worst days of Global equity since the inception of AWS, the strategy has lost less than 60/40 on 90% of days

AWS outperformed a 60/40 in 61% of months

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- In 25 out of 41 months, the All Weather Strategy has beaten a traditional 60/40 portfolio

Key takeaways

- The All Weather Strategy underperformed a 60/40 strategy by 3% in July 2022

- The underperformance was due to low Equity and high Gold weights

- Since inception, the strategy was 7.4% above a 60/40 portfolio by the end of July 2022

Performance review: All Weather Alpha Focus

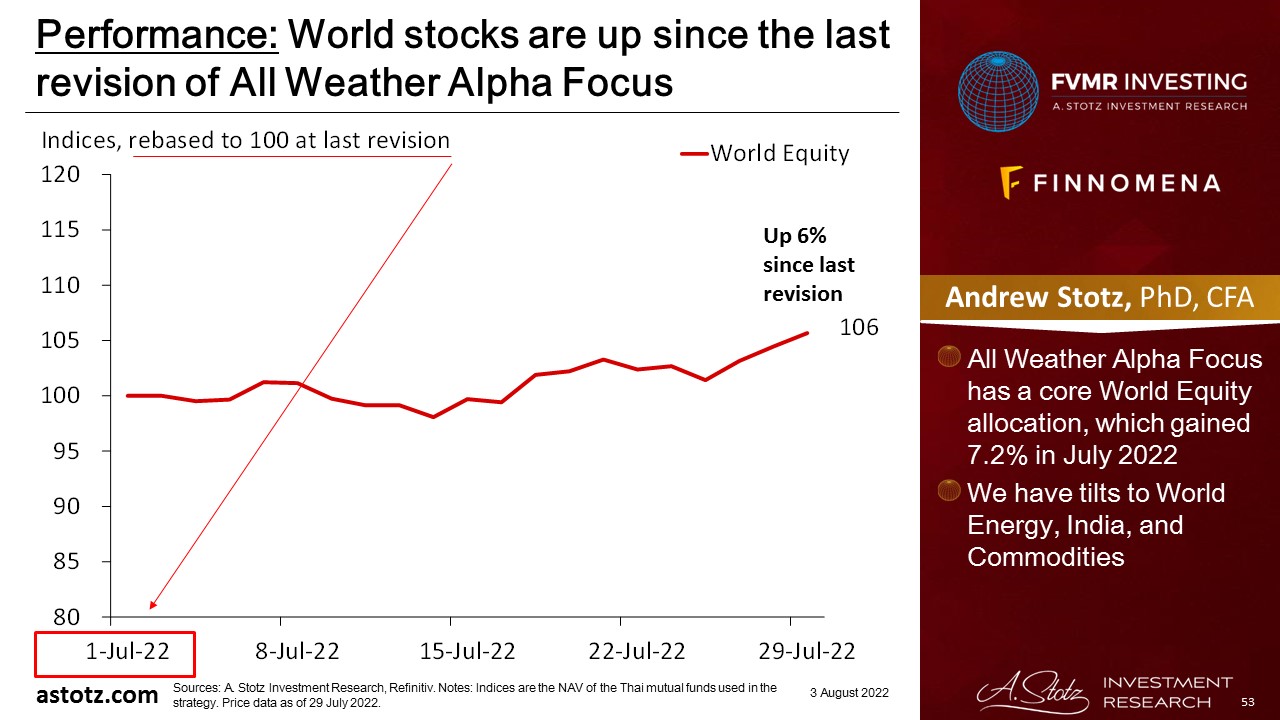

World stocks are up since the last revision of All Weather Alpha Focus

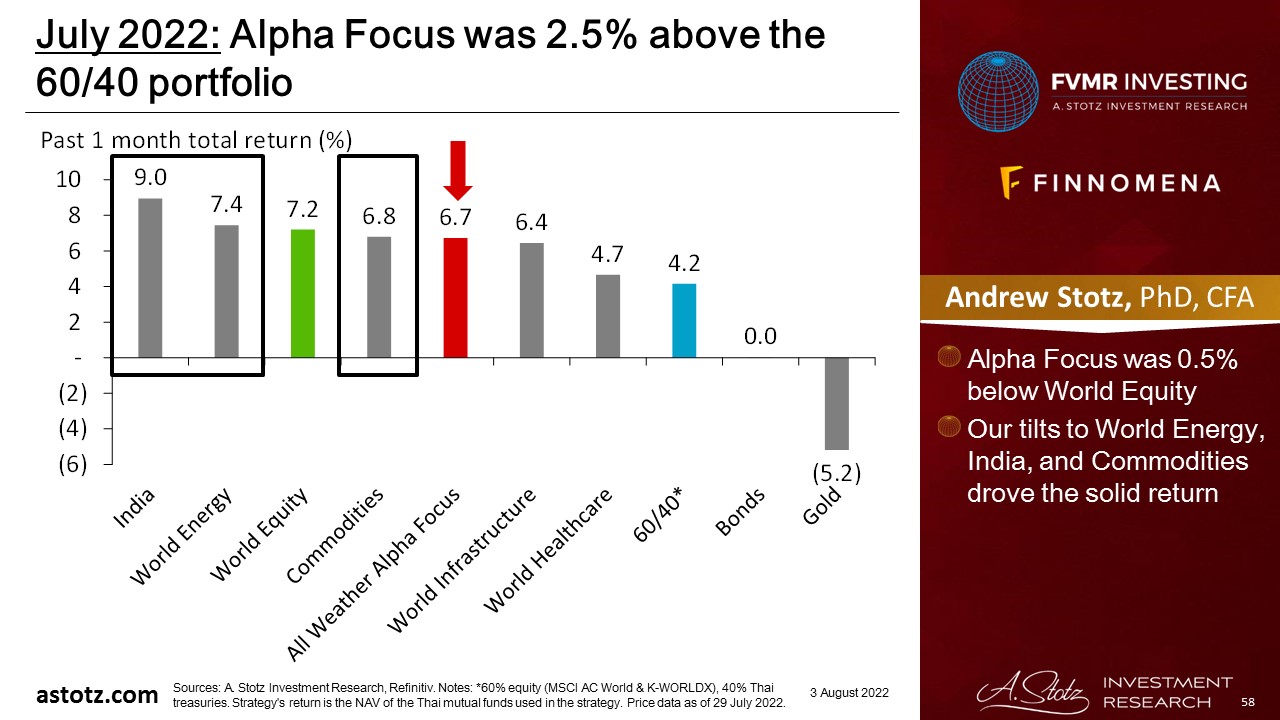

- All Weather Alpha Focus has a core World Equity allocation, which gained 7.2% in July 2022

- We have tilts to World Energy, India, and Commodities

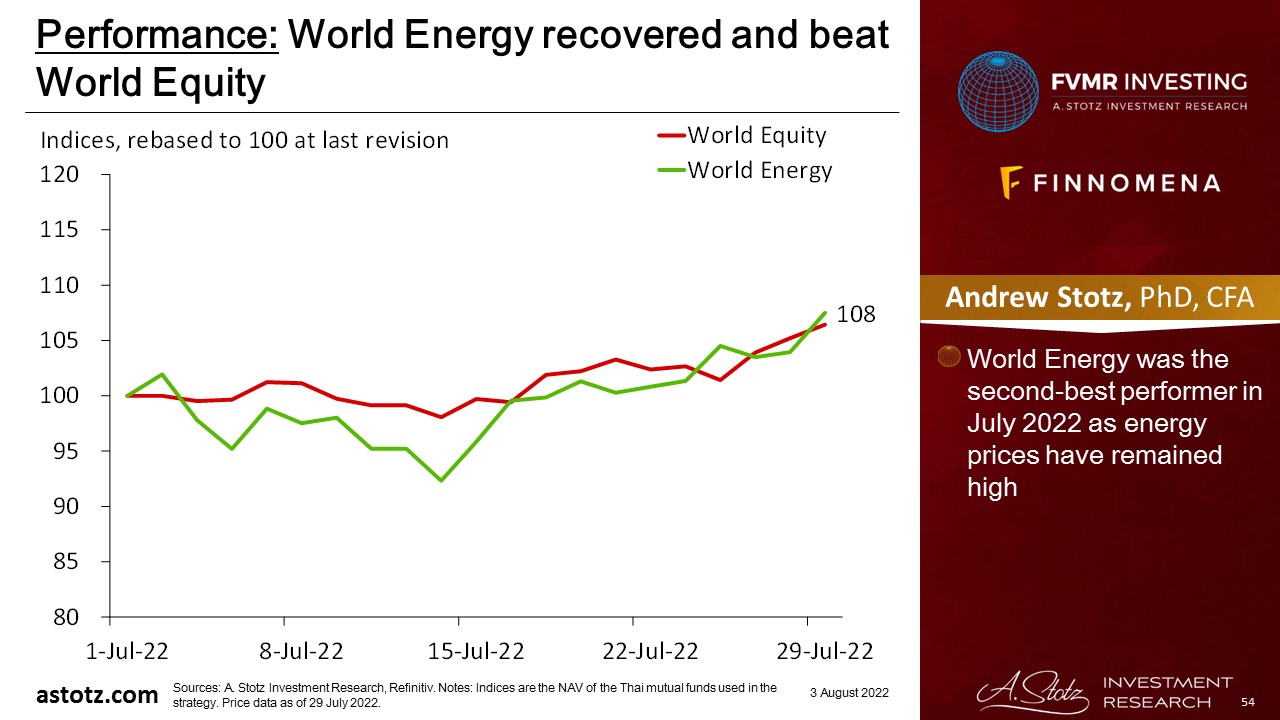

World Energy recovered and beat World Equity

- World Energy was the second-best performer in July 2022 as energy prices have remained high

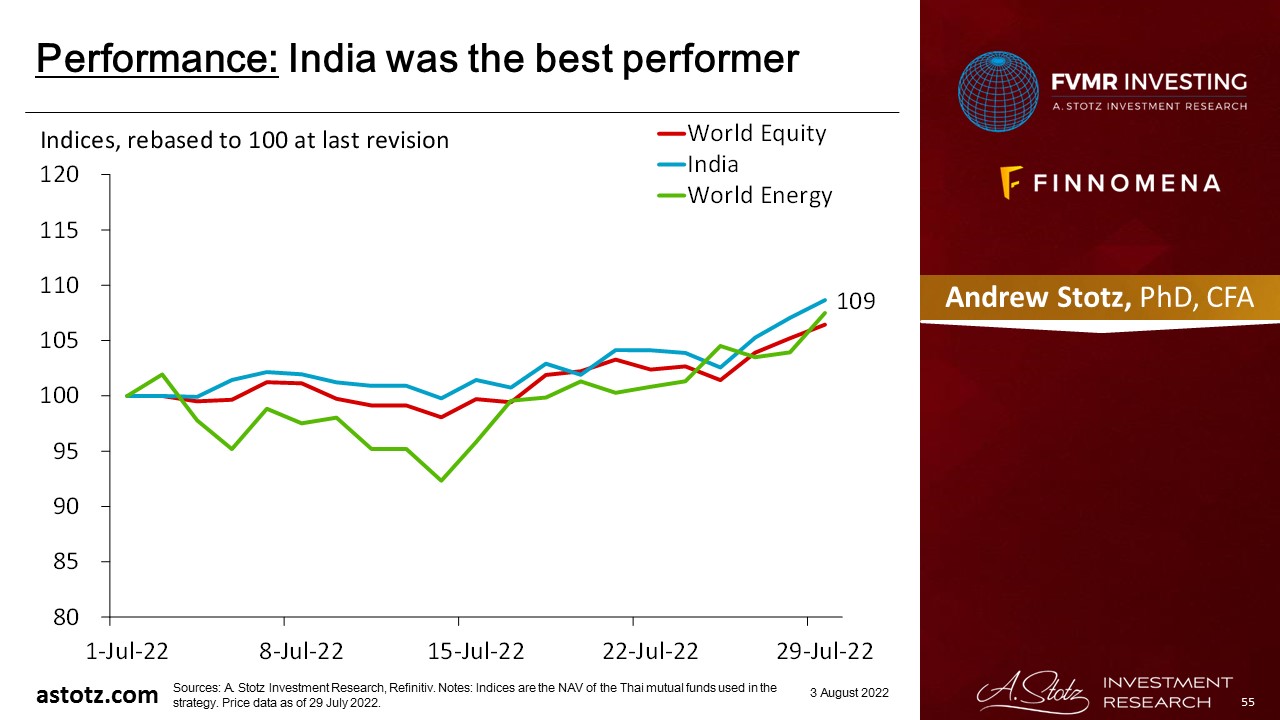

India was the best performer

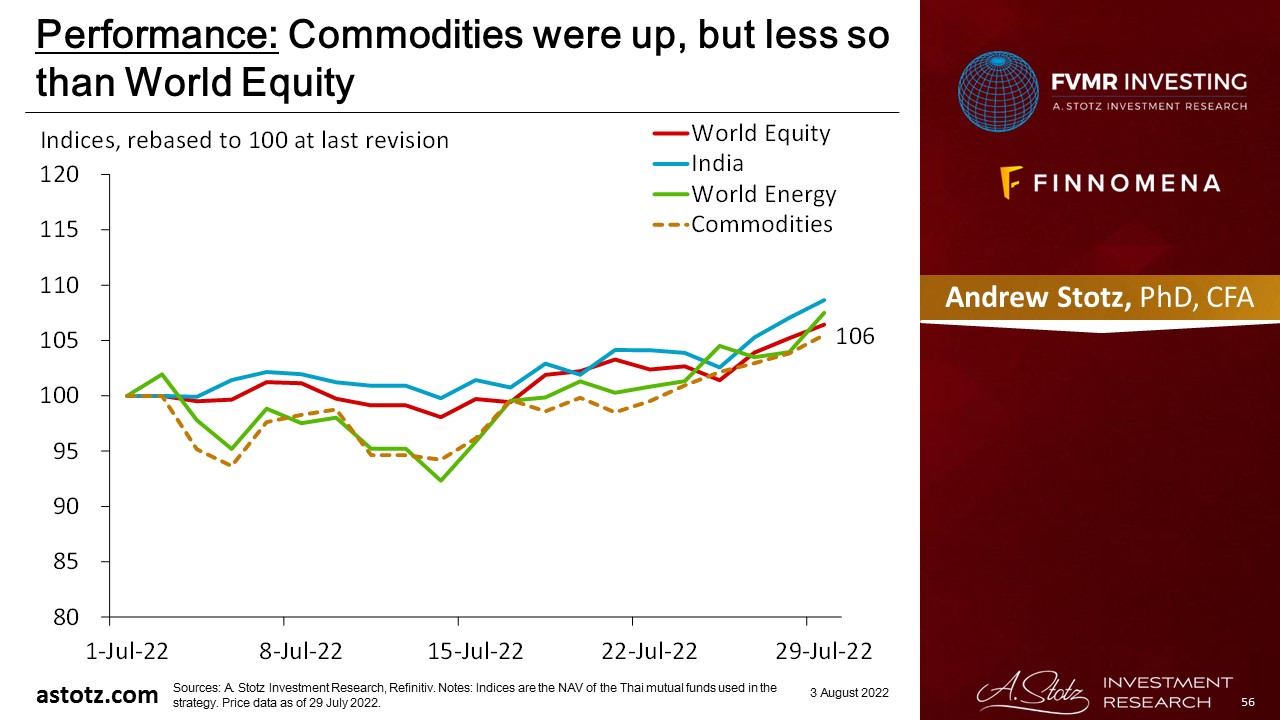

Commodities were up, but less so than World Equity

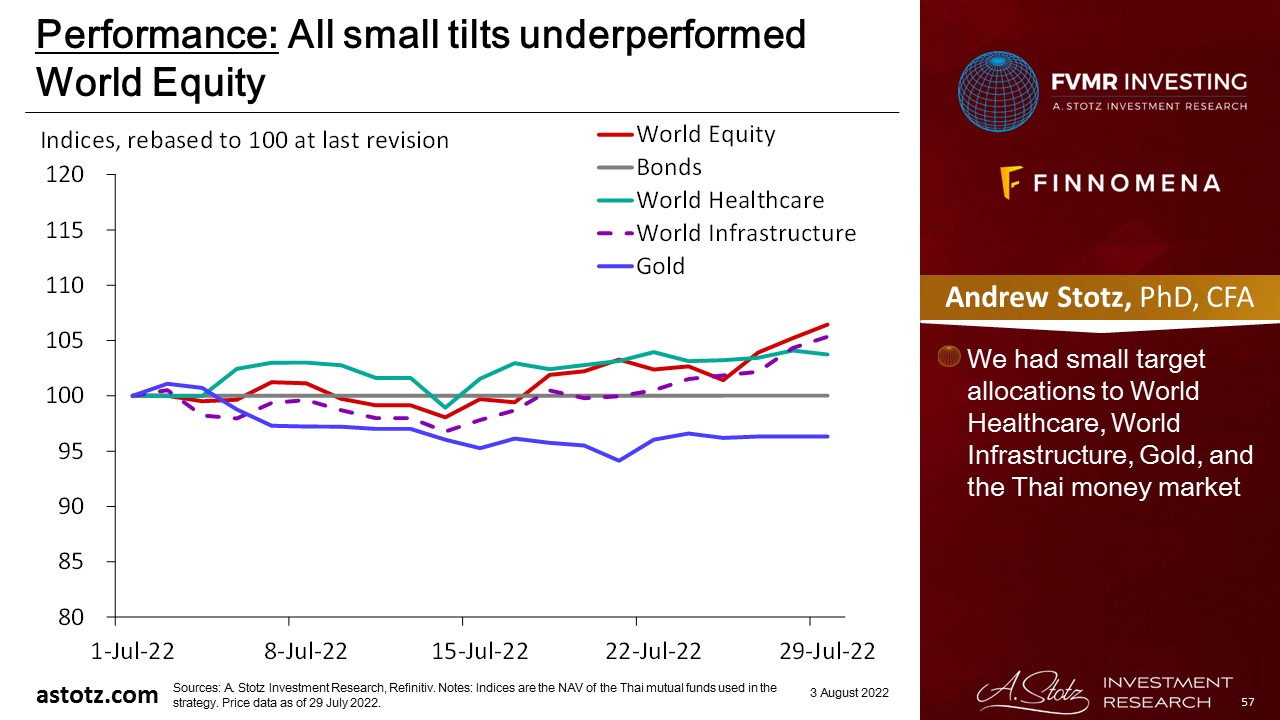

All small tilts underperformed World Equity

- We had small target allocations to World Healthcare, World Infrastructure, Gold, and the Thai money market

Alpha Focus was 2.5% above the 60/40 portfolio

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- Alpha Focus was 0.5% below World Equity

- Our tilts to World Energy, India, and Commodities drove the solid return

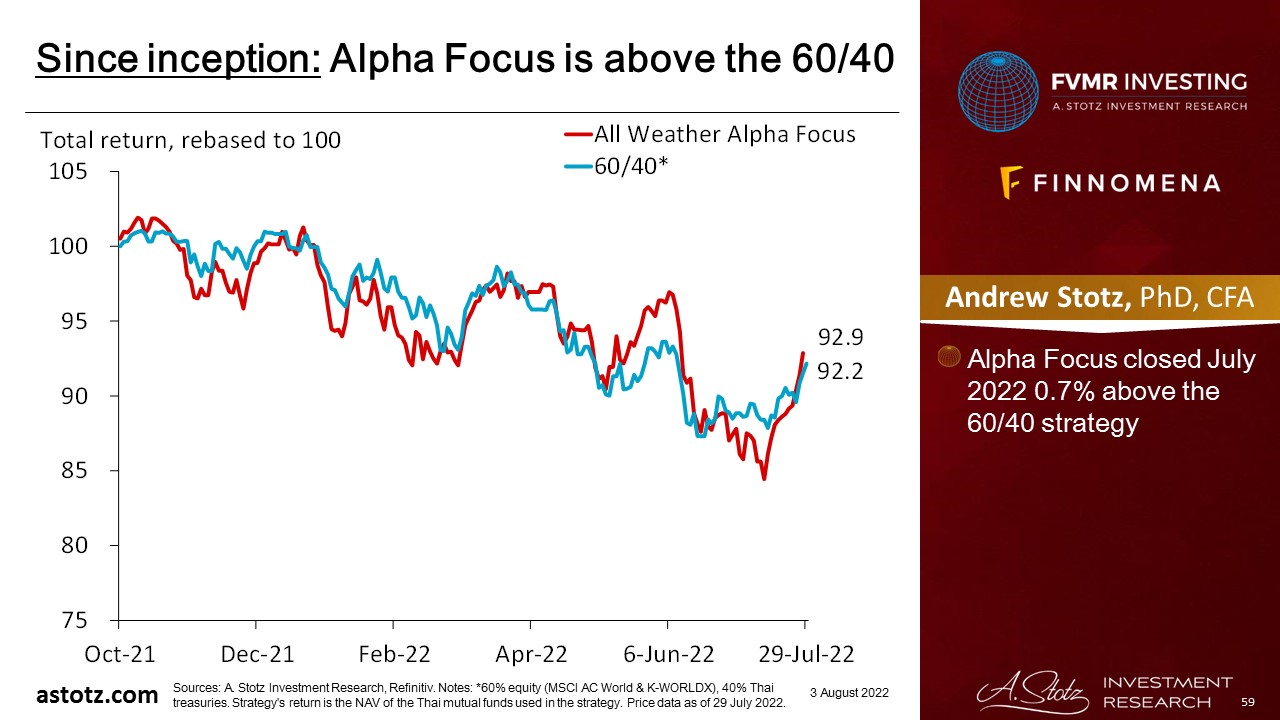

Since inception: Alpha Focus is above the 60/40

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- Alpha Focus closed July 2022 0.7% above the 60/40 strategy

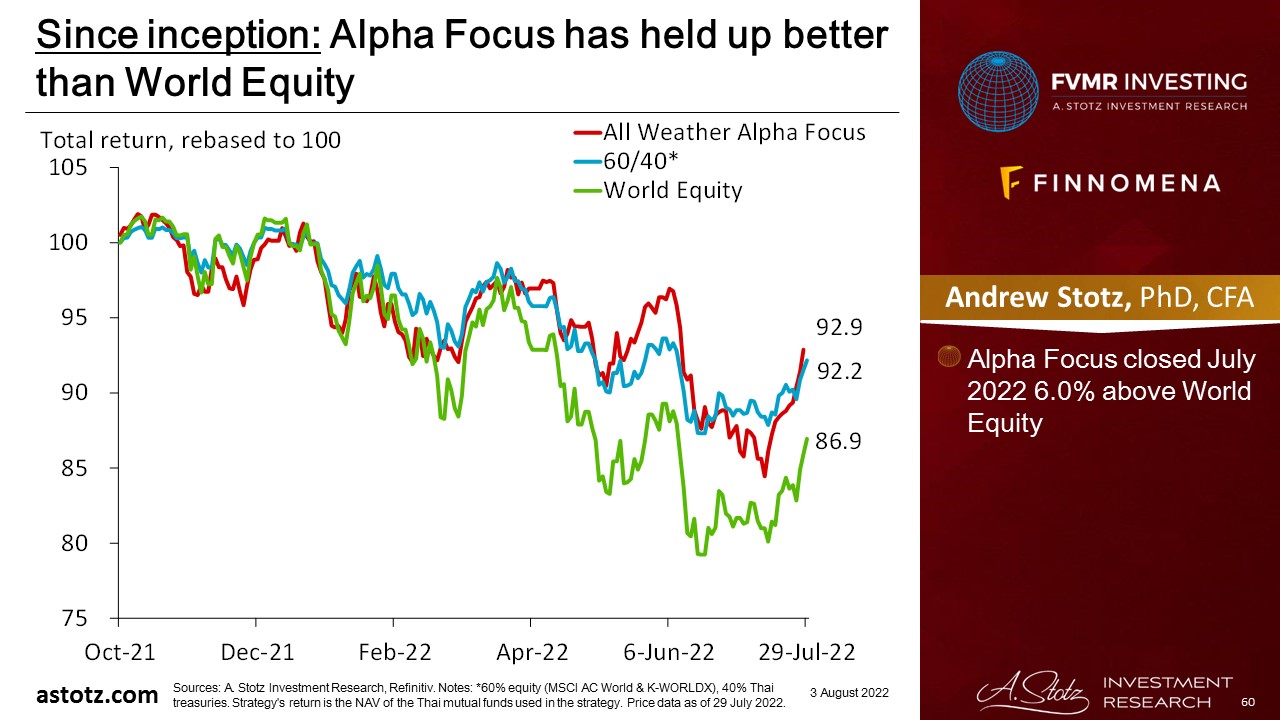

Since inception: Alpha Focus has held up better than World Equity

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- Alpha Focus closed July 2022 6.0% above World Equity

Key takeaways

- All Weather Alpha Focus outperformed a 60/40 strategy by 2.5% in July 2022, though it was 0.5% below World Equity

- Our tilts to World Energy, India, and Commodities drove the solid return

- Since inception, the strategy was 0.7% above a 60/40 portfolio and 6.0% above World Equity by the end of July 2022

Global outlook that guides our asset allocation

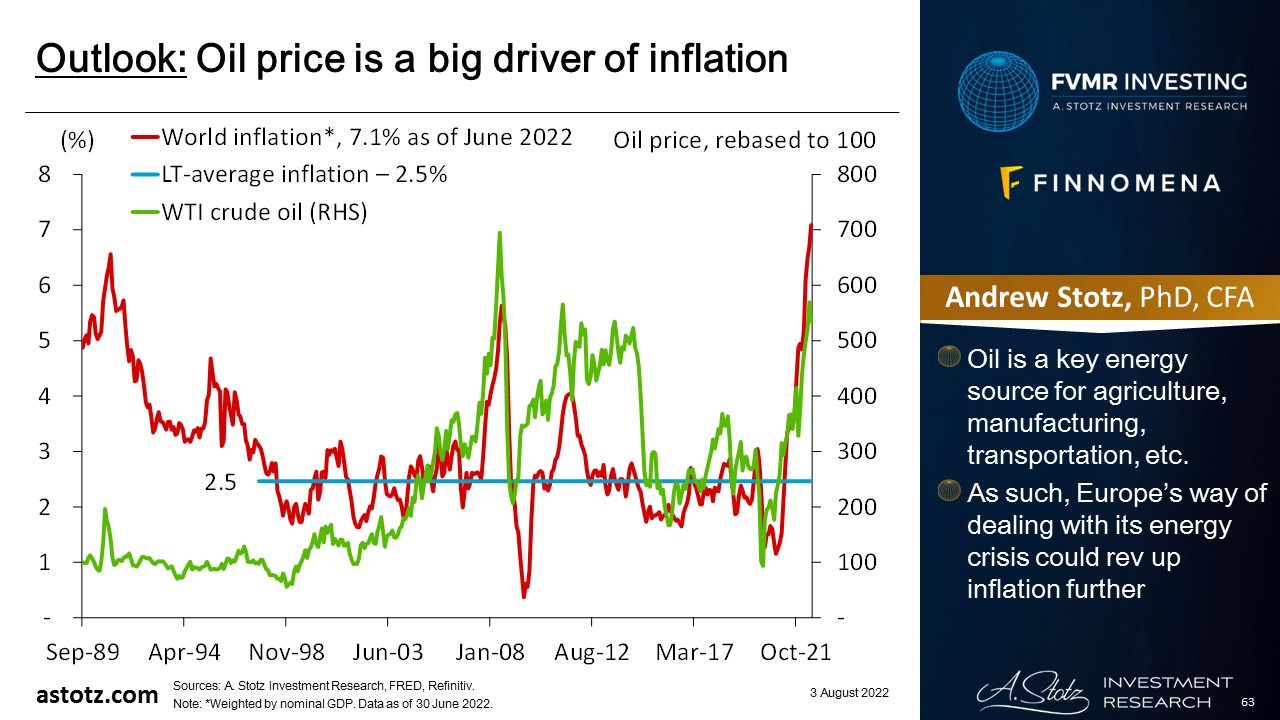

Oil price is a big driver of inflation

- Oil is a key energy source for agriculture, manufacturing, transportation, etc.

- As such, Europe’s way of dealing with its energy crisis could rev up inflation further

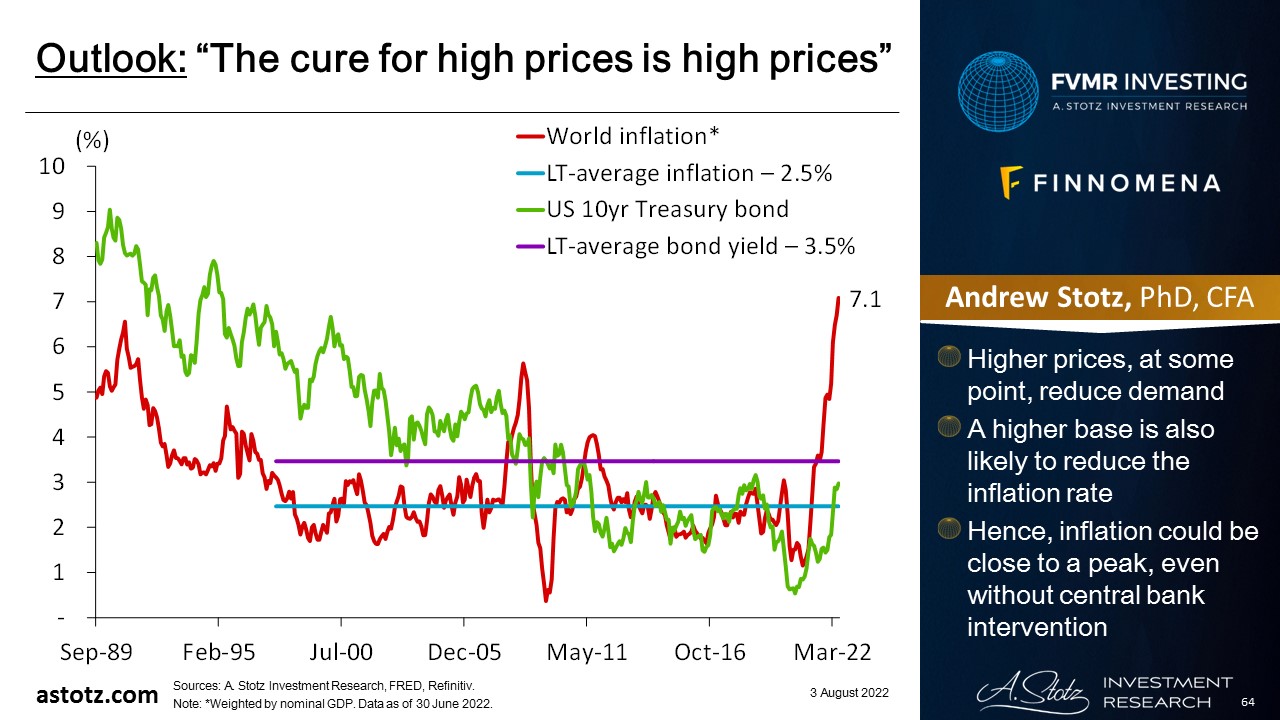

“The cure for high prices is high prices”

- Higher prices, at some point, reduce demand

- A higher base is also likely to reduce the inflation rate

- Hence, inflation could be close to a peak, even without central bank intervention

The Fed raises rates, but Biden talks about stimulating the economy

It’s almost as if reducing inflation is not the real purpose of the Inflation Reduction Act. https://t.co/xSAKdI2OvQ

— Byron York (@ByronYork) July 30, 2022

Soft landing is the goal of the Fed

- “I do not think the U.S. is currently in a recession. It doesn’t make sense that the U.S. would be in recession.”

- “We do want to see demand running below potential for a sustained period to create slack. We’re trying to do just the right amount. We’re not trying to have a recession.”

Fed seems to have changed its communication strategy

- “We think it’s time to just go to a meeting-by- meeting basis and not provide the kind of clear guidance that we had provided on the way to neutral.”

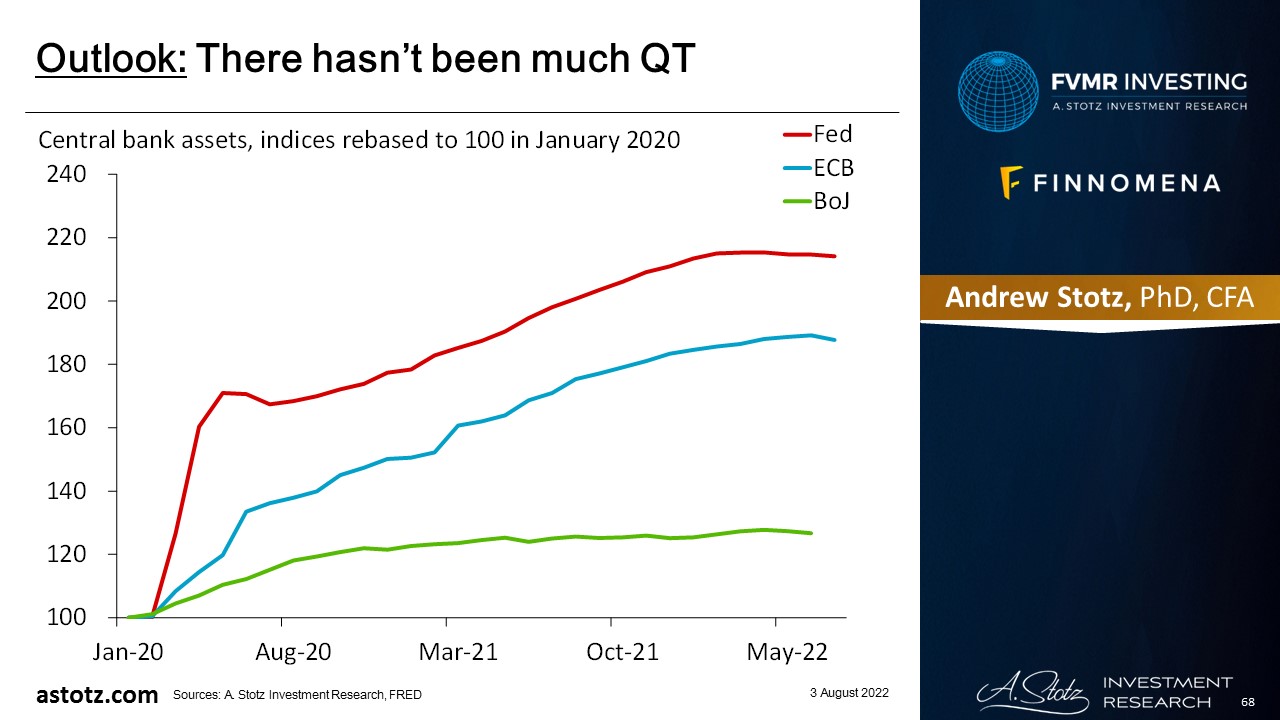

There hasn’t been much QT

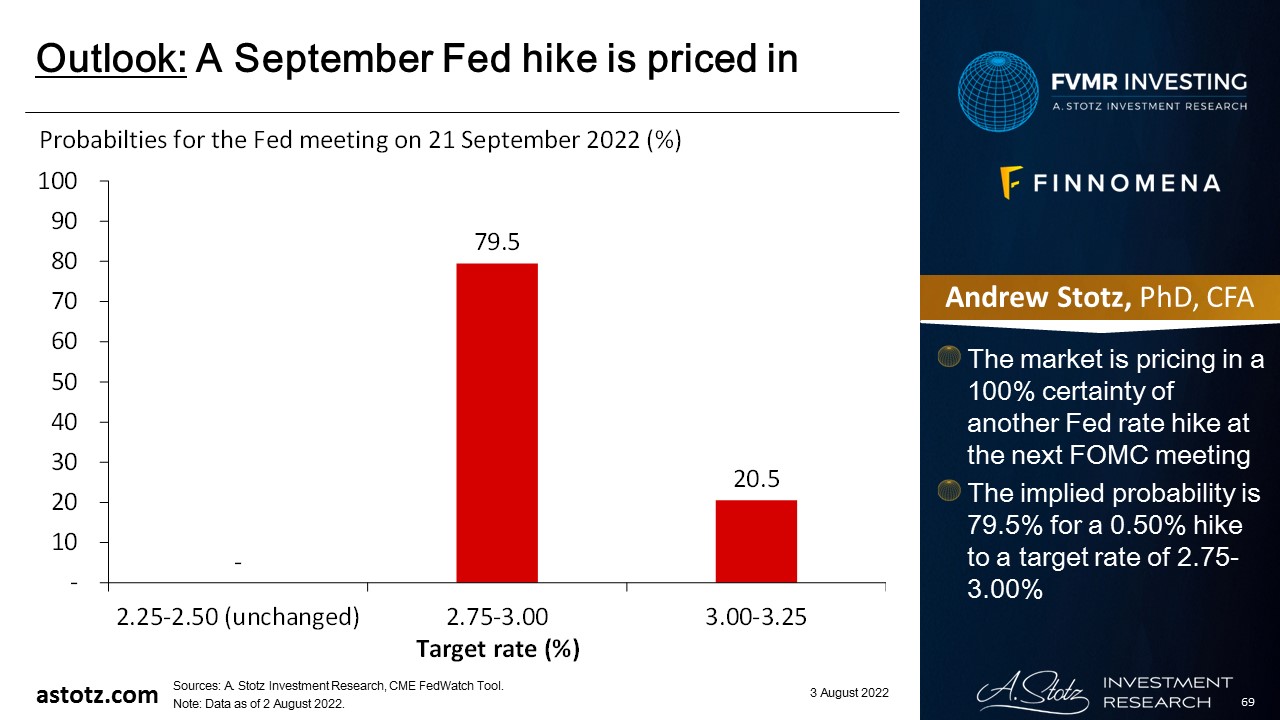

A September Fed hike is priced in

- The market is pricing in a 100% certainty of another Fed rate hike at the next FOMC meeting

- The implied probability is 79.5% for a 0.50% hike to a target rate of 2.75-3.00%

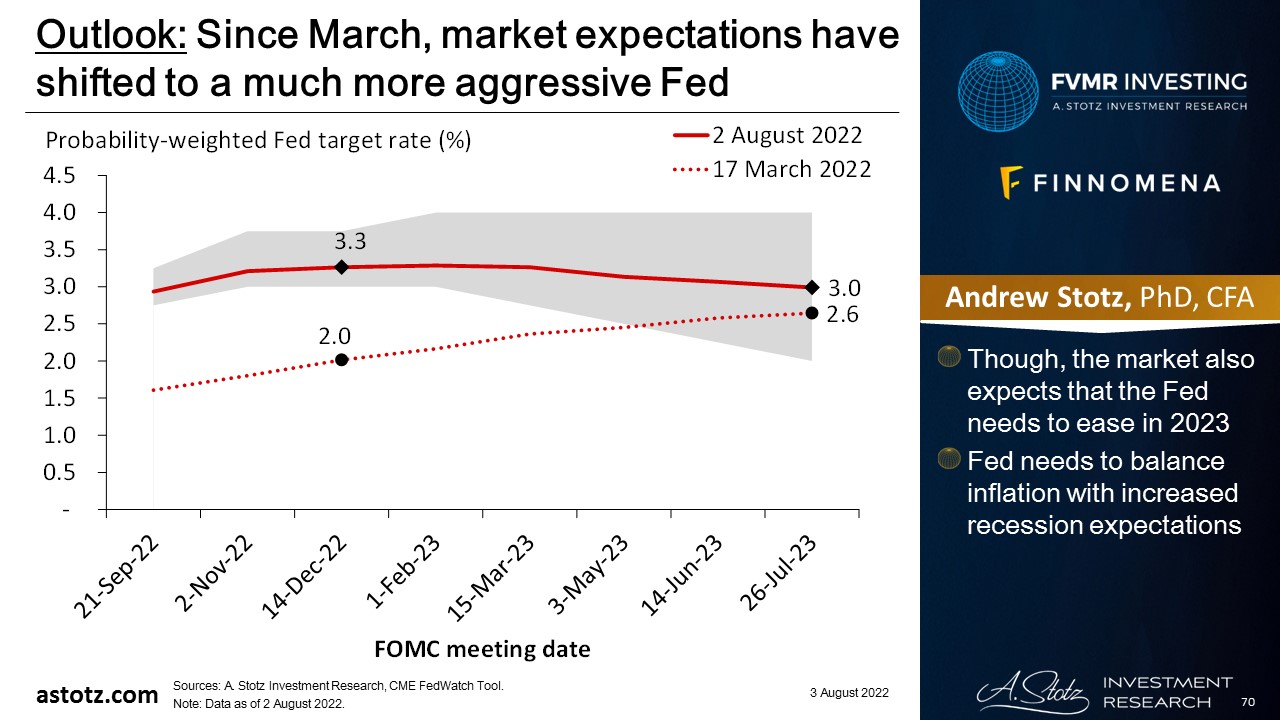

Since March, market expectations have shifted to a much more aggressive Fed

- Though, the market also expects that the Fed needs to ease in 2023

- Fed needs to balance inflation with increased recession expectations

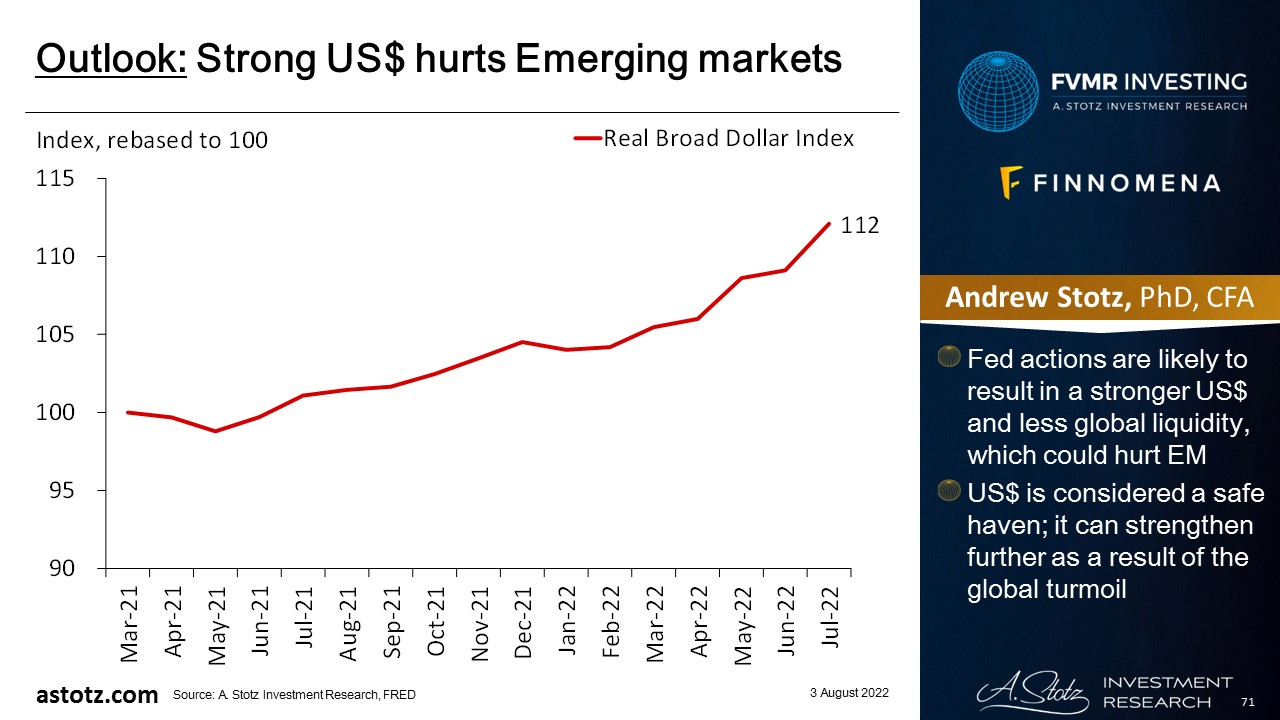

Strong US$ hurts Emerging markets

- Fed actions are likely to result in a stronger US$ and less global liquidity, which could hurt EM

- US$ is considered a safe haven; it can strengthen further as a result of the global turmoil

We could see further hikes in the EU as well

- The hike in July brought the key rate to zero in the EU instead of negative, which has been the case since 2014

- Like the Fed, ECB has decided to stop forward guidance and use a meeting-by-meeting approach

- Though, ECB President Lagarde re-affirmed the commitment to the 2% inflation target

We think the course will be reversed

- As you can see, central banks are communicating that they’re going to get inflation down, and investors seem to buy the rhetoric

- We still think central bankers and politicians will change course and return to accommodative policies as soon as something “breaks”

US inventories are up, which could signal a slowdown in consumption

Here’s a chart you don’t see every day: pic.twitter.com/VLOo4kZCX6

— Tren Griffin (@trengriffin) July 25, 2022

Yield-curve inversion has been an accurate predictor of recessions

A benchmark U.S. yield curve is the most inverted since 2000. U.S. 2-year Treasuries are yielding the most versus 10-year notes since that year, typically a signal of recession in the following 12-18 months. pic.twitter.com/WDeCs386Jn

— Lisa Abramowicz (@lisaabramowicz1) July 26, 2022

- Though many indicators look negative for equity, we see opportunities to allocate to specific sectors like World Energy and markets like India within the asset class

Indian stocks can remain strong

- Indian IT companies have reported rising backlogs and struggle to keep up with demand

- The new Indian Gov’t budget is focused on infrastructure, renewables, and healthcare spending to continue fast GDP growth

- Continued budget deficit should instill confidence about Indian Gov’t support

- We think India can outperform the World stock index, so we keep our 20% target weight

Bonds are typically a safe place to be

- In recessions, safer assets like gov’t bonds are typically performing well

- Though with high inflation, low yields could still lead to negative real returns

- We typically don’t allocate to Bonds to speculate in the upside, but rather use it as a way to protect capital over time

Commodities still look attractive

Goldman on recent commodity rout:

“Commodities r disassociated from micro fundamentals…latest comm. sell-off de-linked from phys. fundamentals & driven by financial liquidation. Inventories…continue to fall from already uncomfortably low lvls… #oil #OOTT #EFT pic.twitter.com/XzmOgNrmwN— OpenSquareCapital (@OpenSquareCap) July 9, 2022

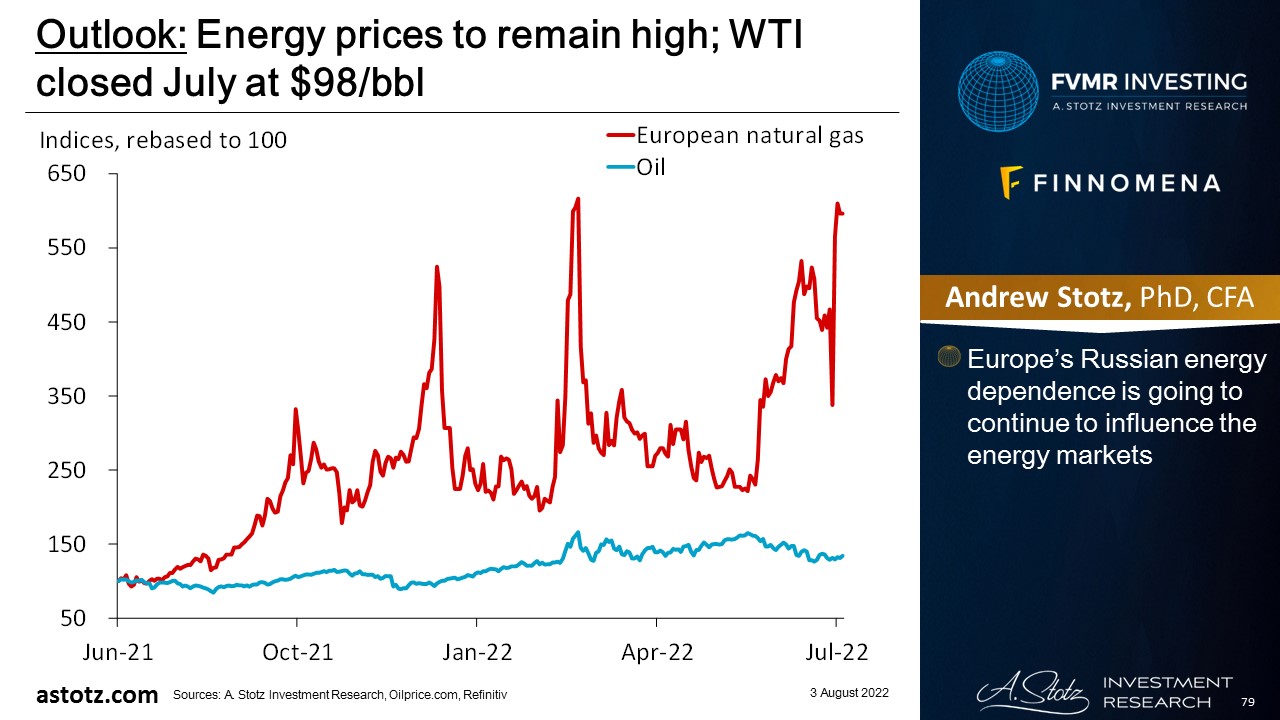

Energy prices to remain high; WTI closed July at $98/bbl

- Europe’s Russian energy dependence is going to continue to influence the energy markets

Fundamental support for energy prices

- Ukraine war could lead to further supply shocks

- Energy prices can also remain high due to past underinvestment in new projects

- Besides energy, Russia is an exporter of many industrial metals, and Russia and Ukraine are both important exporters of soft commodities

- A re-opening of China could lead to increased demand for commodities

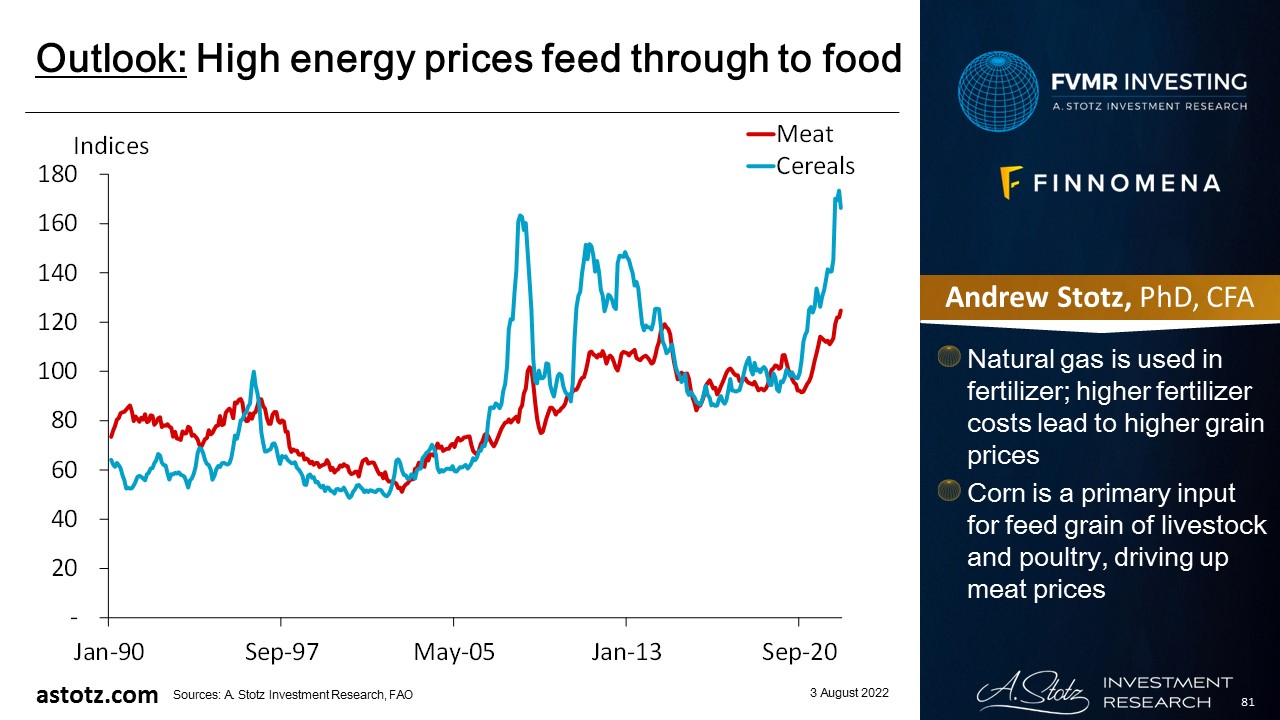

High energy prices feed through to food

- Natural gas is used in fertilizer; higher fertilizer costs lead to higher grain prices

- Corn is a primary input for feed grain of livestock and poultry, driving up meat prices

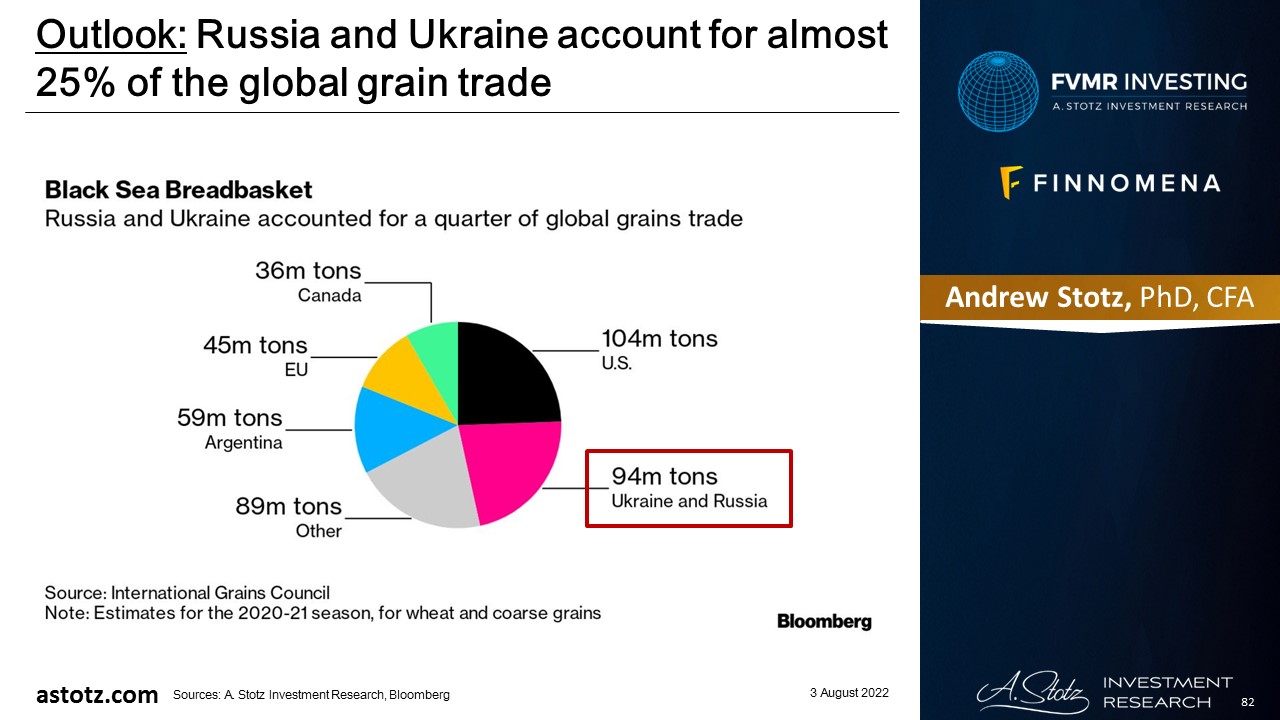

Russia and Ukraine account for almost 25% of the global grain trade

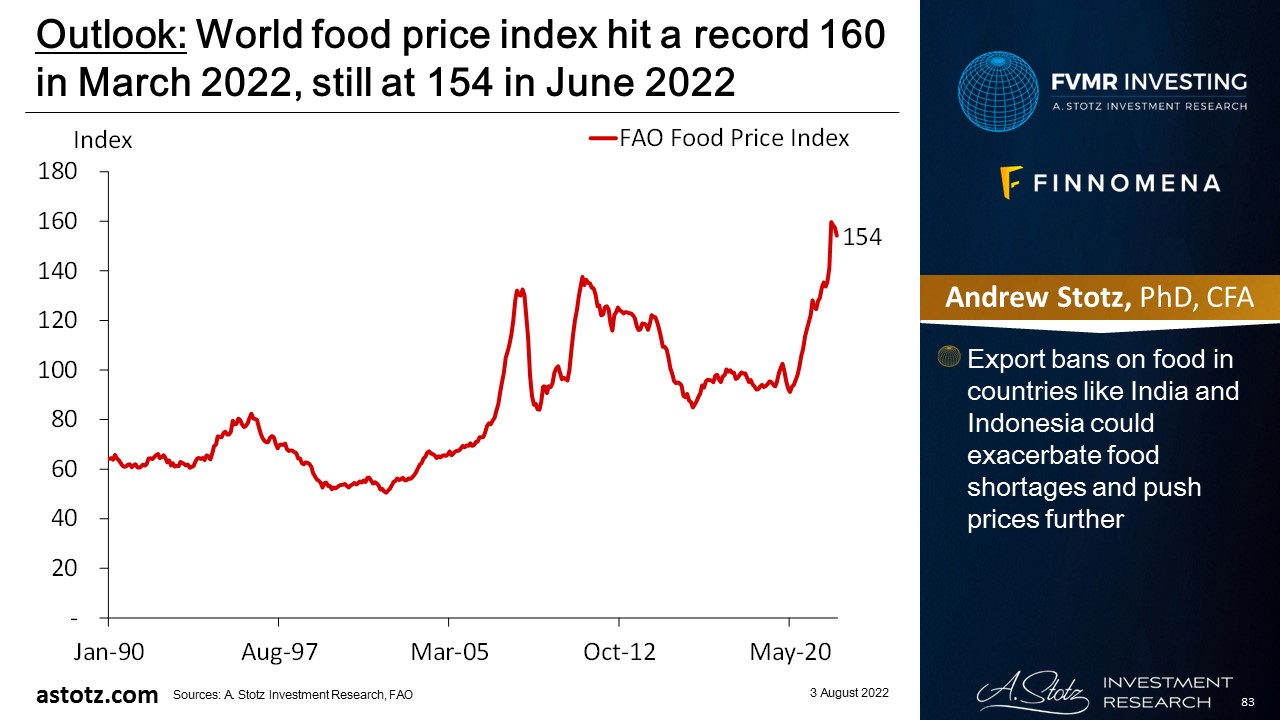

World food price index hit a record 160 in March 2022, still at 154 in June 2022

- Export bans on food in countries like India and Indonesia could exacerbate food shortages and push prices further

Commodities set to go higher

- Demand for necessities (food and energy), inflation, and supply-chain disruptions related and unrelated to the war in Ukraine are going to drive the asset class higher

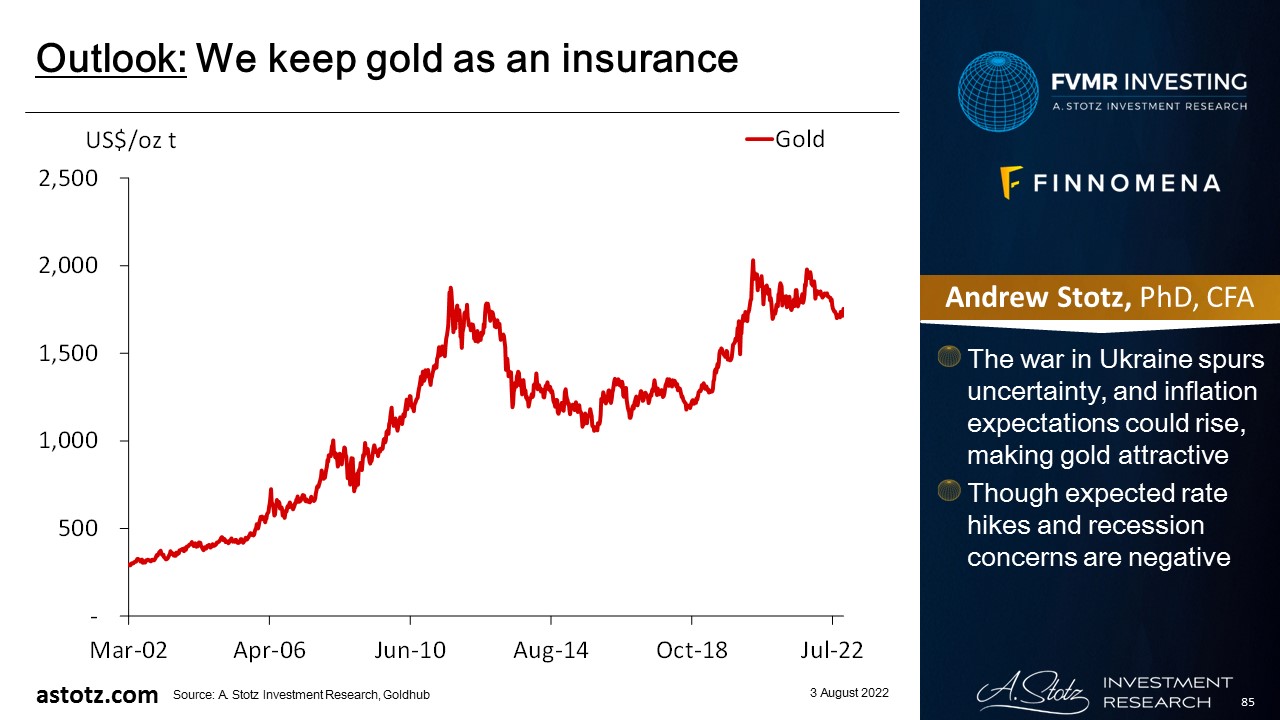

We keep gold as an insurance

- The war in Ukraine spurs uncertainty, and inflation expectations could rise, making gold attractive

- Though expected rate hikes and recession concerns are negative

Key takeaways

- Central bankers appear to be raising rates into a recession to stifle inflation

- We see opportunities to allocate to sectors and countries within equity, e.g., World Energy and India

- Demand for necessities (food and energy), inflation, and supply-chain disruptions are going to drive the asset class higher

- Bonds and Gold to protect capital

Risks

Inflation quickly gets under control

- We are positioned to benefit from rising inflation through our Commodities allocation

- Weak Chinese economy could reduce commodities demand; leads to lower prices

- Collapsing energy prices would be damaging since we have high exposure through our allocations to World Energy and Commodities

- Other commodities could fall with energy prices too, as it’s part of the production cost

Global recession pushing down stocks

- If major central banks would surprise and be too aggressive with rate hikes and QT, it could crash the stock markets

- Alpha Focus has a tilt to Indian equity, so the strategy would be negatively impacted if the Indian market were to crash

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.