A. Stotz All Weather Strategies – April 2026

The All Weather Strategy is available in Thailand through FINNOMENA. If you’re interested in our allocation strategy, you can also join the Become a Better Investor Community. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

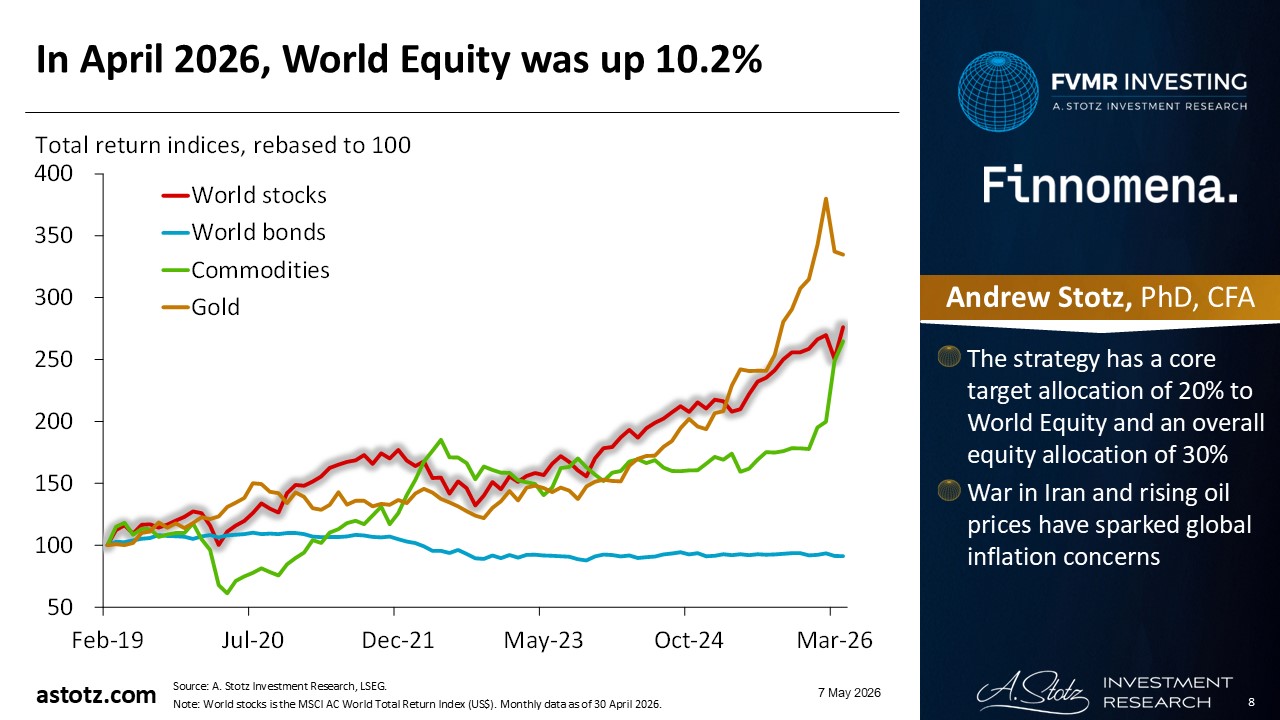

In April 2026, World Equity was up 10.2%

- The strategy has a core target allocation of 20% to World Equity and an overall equity allocation of 30%

- War in Iran and rising oil prices have sparked global inflation concerns

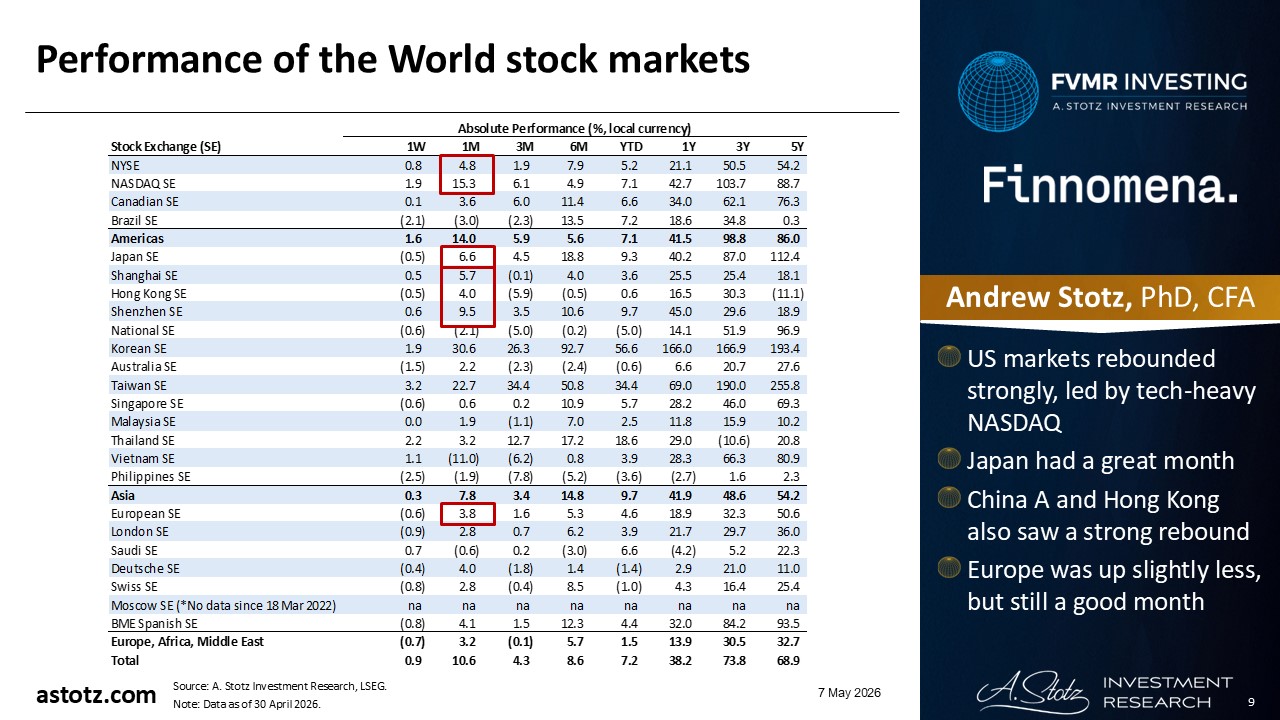

Performance of the World stock markets

- US markets rebounded strongly, led by tech-heavy NASDAQ

- Japan had a great month

- China A and Hong Kong also saw a strong rebound

- Europe was up slightly less, but still a good month

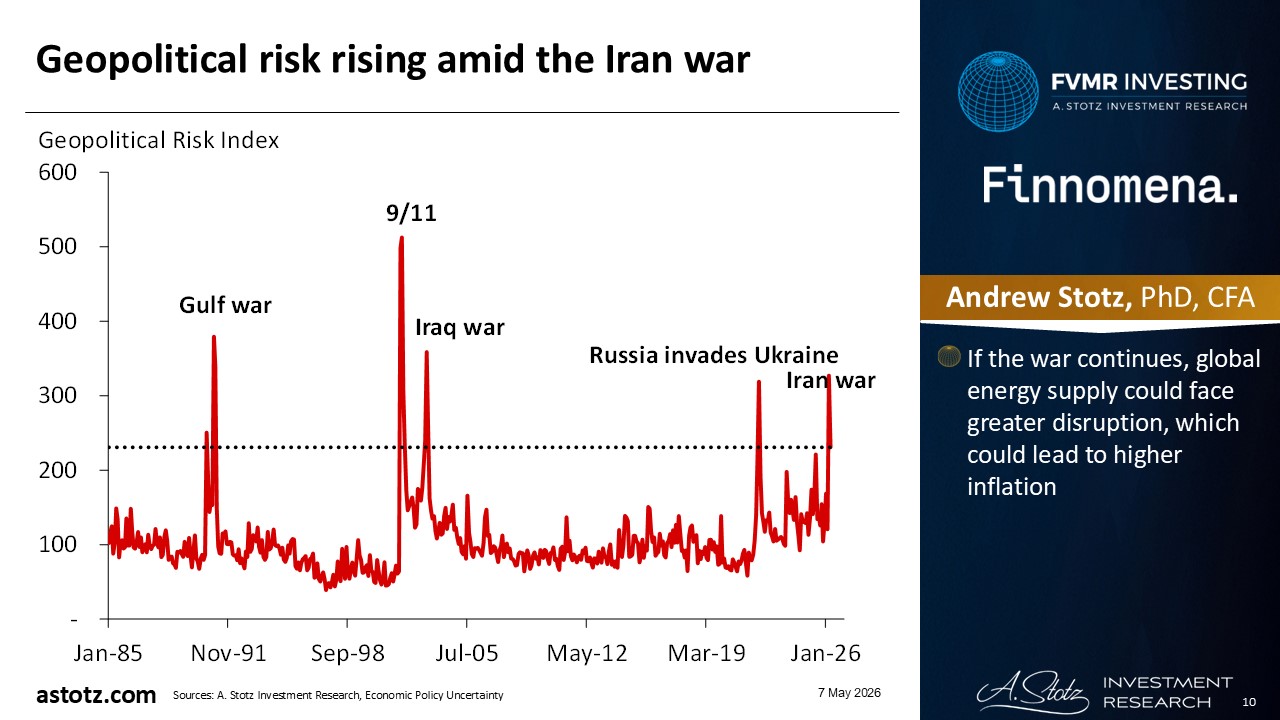

Geopolitical risk rising amid the Iran war

- If the war continues, global energy supply could face greater disruption, which could lead to higher inflation

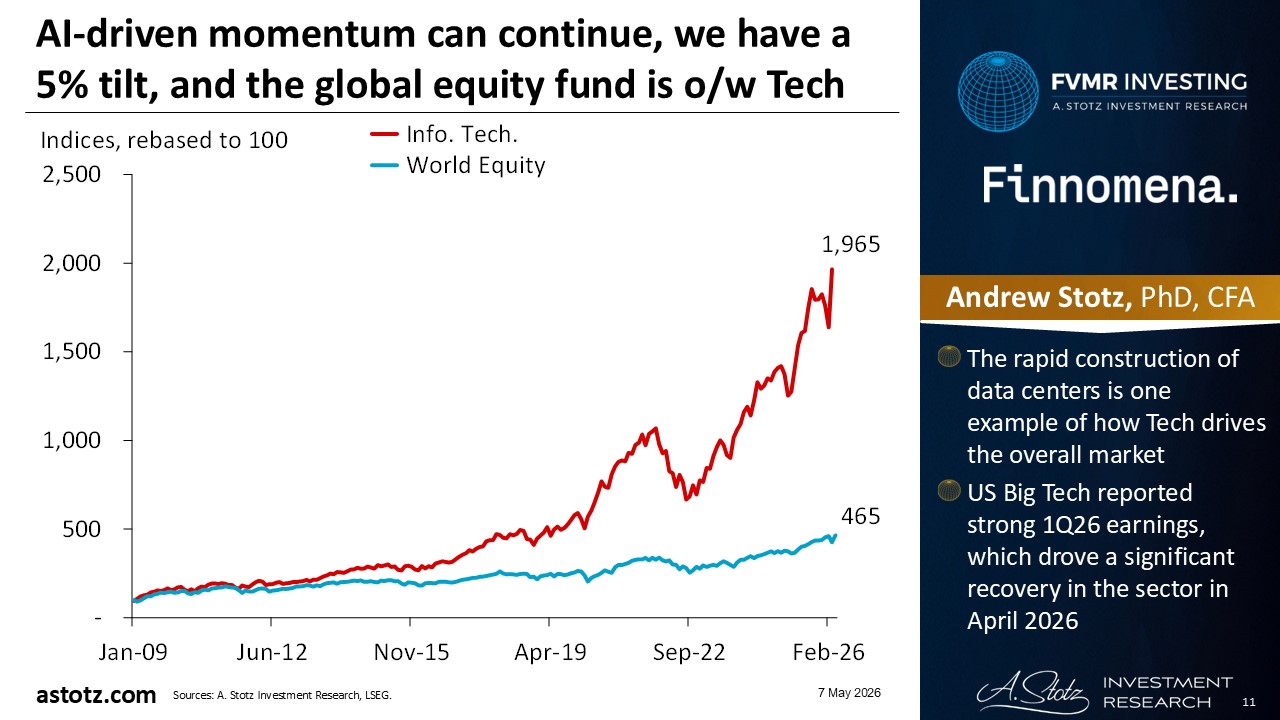

AI-driven momentum can continue, we have a 5% tilt, and the global equity fund is o/w Tech

- The rapid construction of data centers is one example of how Tech drives the overall market

- US Big Tech reported strong 1Q26 earnings, which drove a significant recovery in the sector in April 2026

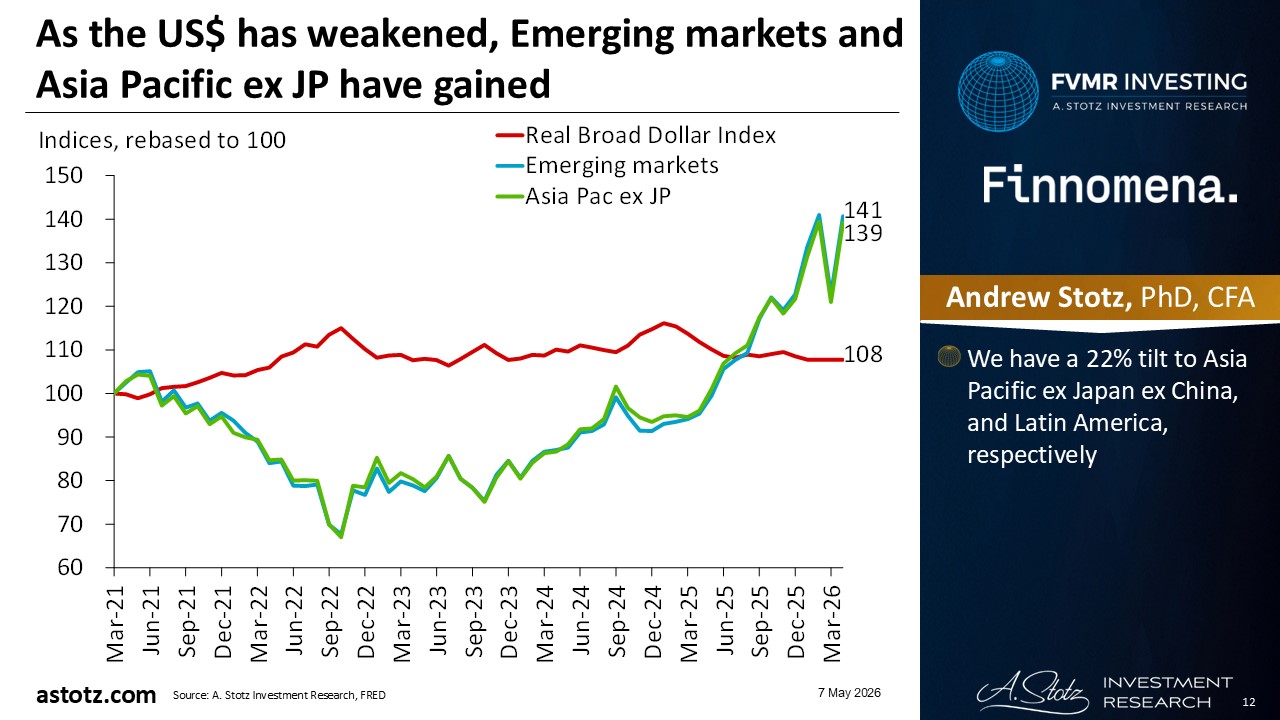

As the US$ has weakened, Emerging markets and Asia Pacific ex JP have gained

- We have a 22% tilt to Asia Pacific ex Japan ex China, and Latin America, respectively

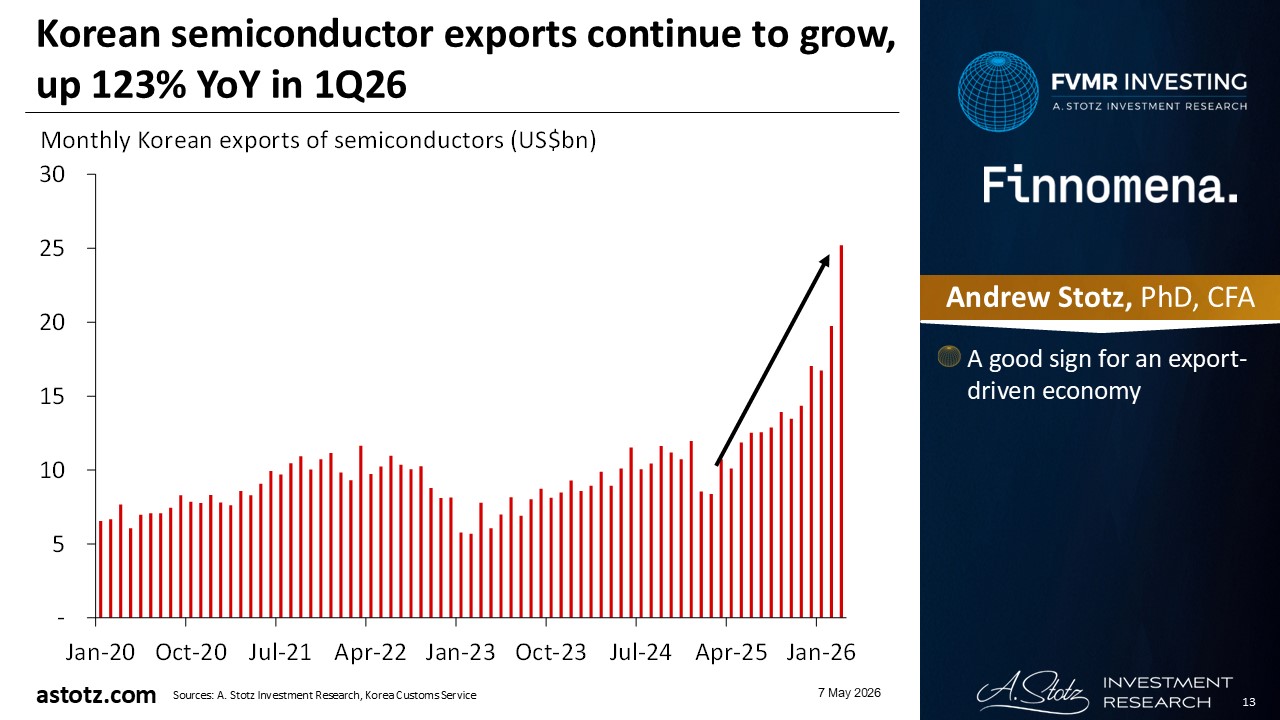

Korean semiconductor exports continue to grow, up 123% YoY in 1Q26

- A good sign for an export-driven economy

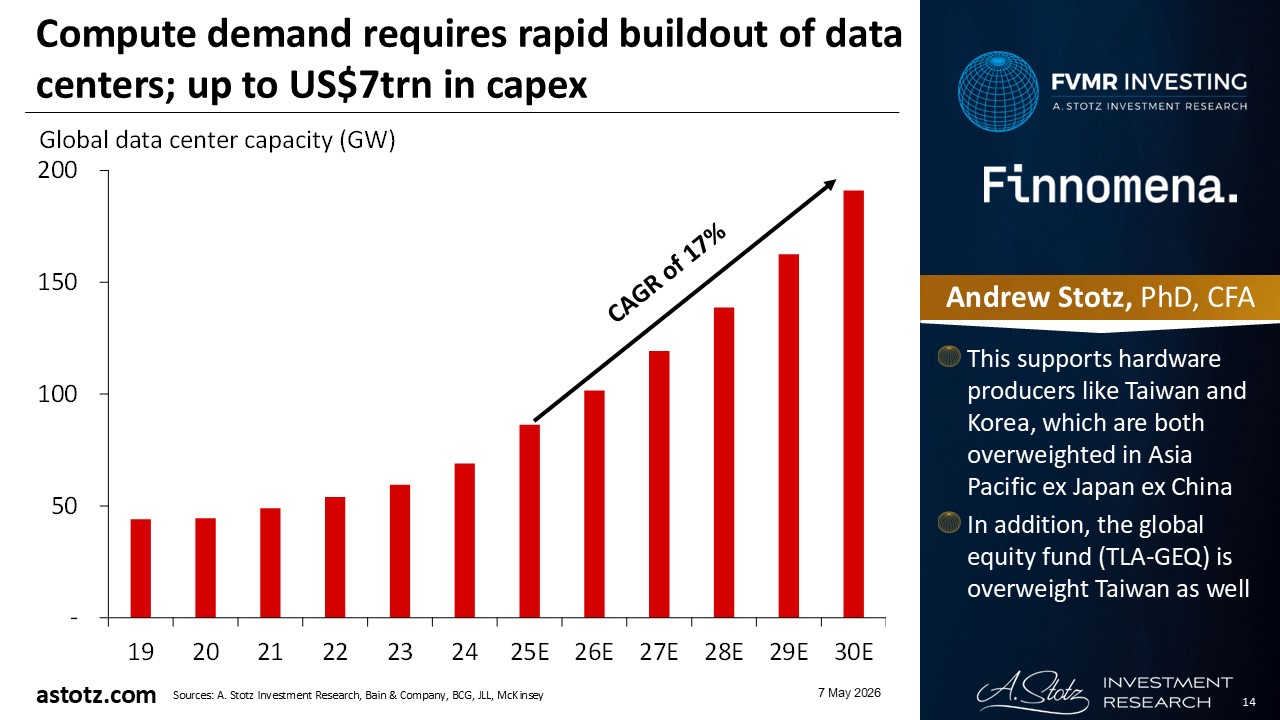

Compute demand requires rapid buildout of data centers; up to US$7trn in capex

- This supports hardware producers like Taiwan and Korea, which are both overweighted in Asia Pacific ex Japan ex China

- In addition, the global equity fund (TLA-GEQ) is overweight Taiwan as well

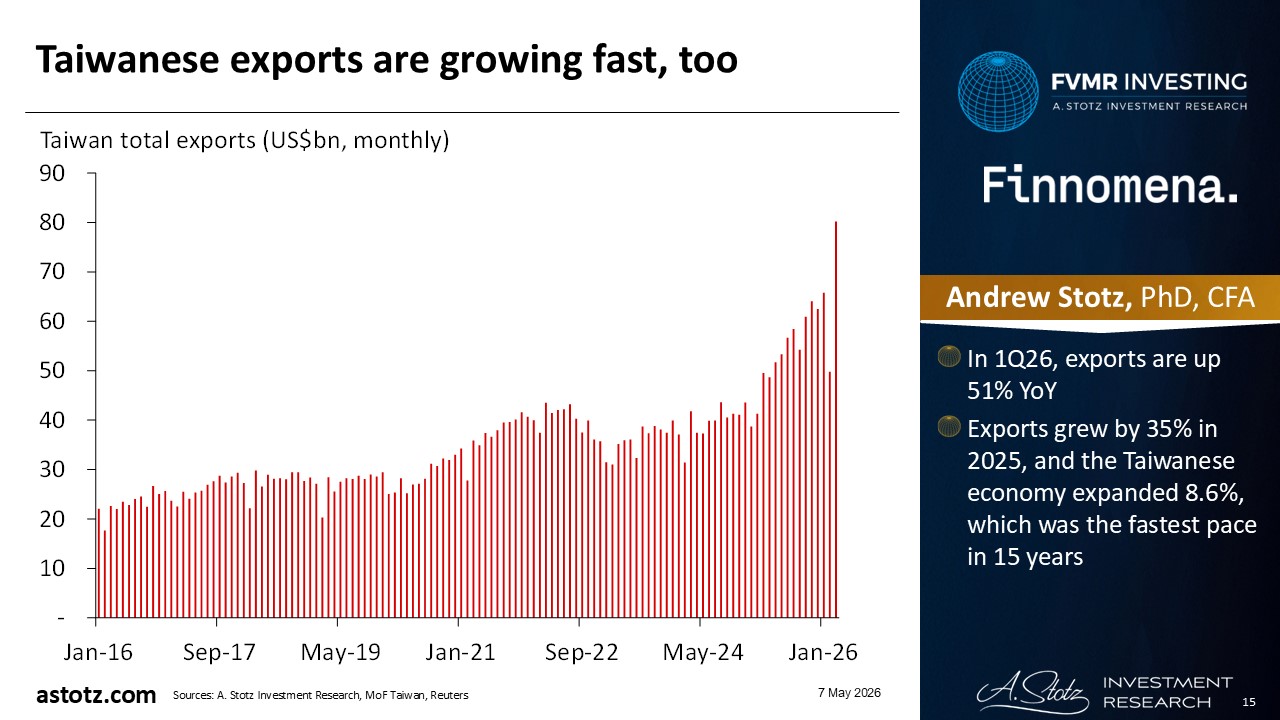

Taiwanese exports are growing fast, too

- In 1Q26, exports are up 51% YoY

- Exports grew by 35% in 2025, and the Taiwanese economy expanded 8.6%, which was the fastest pace in 15 years

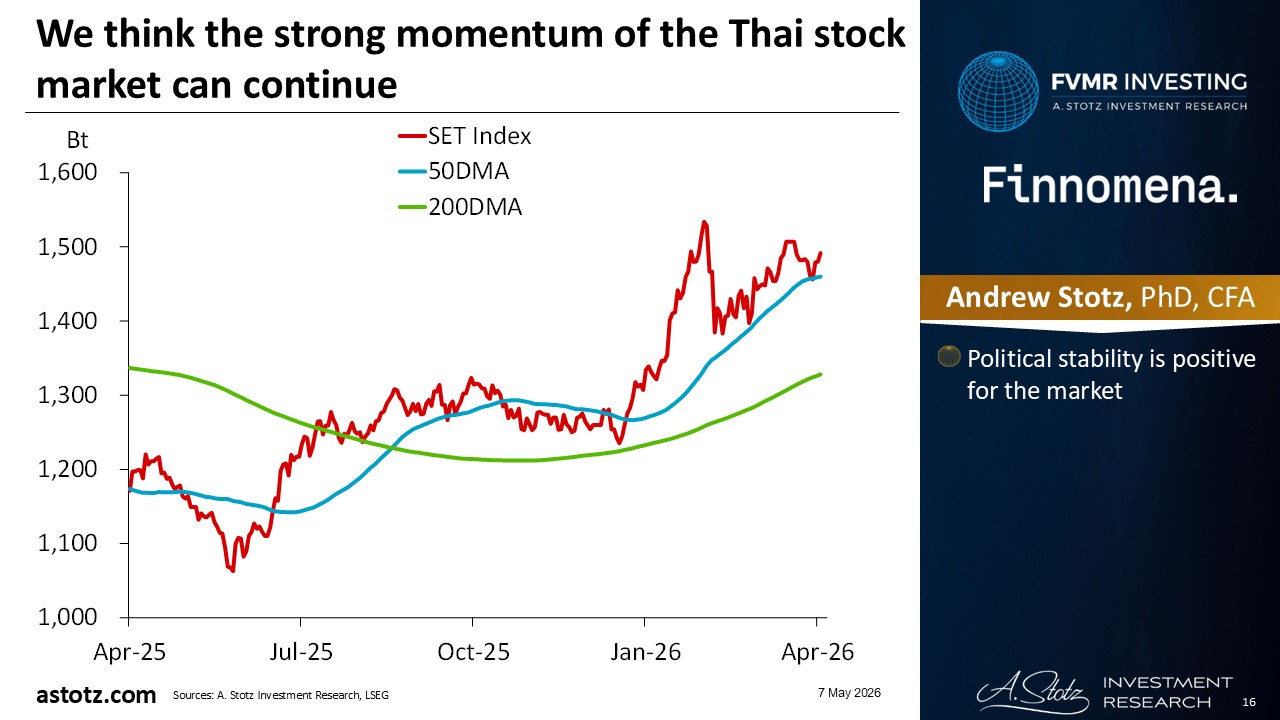

We think the strong momentum of the Thai stock market can continue

- Political stability is positive for the market

We have a 20% tilt to Latin America

- In Latin America, Brazil has about 60% weight, Mexico has over 25%, and Chile and Peru account for the rest in the Latin America fund we use in the strategy

- Both Brazil and Mexico are rich in natural resources and are significant exporters

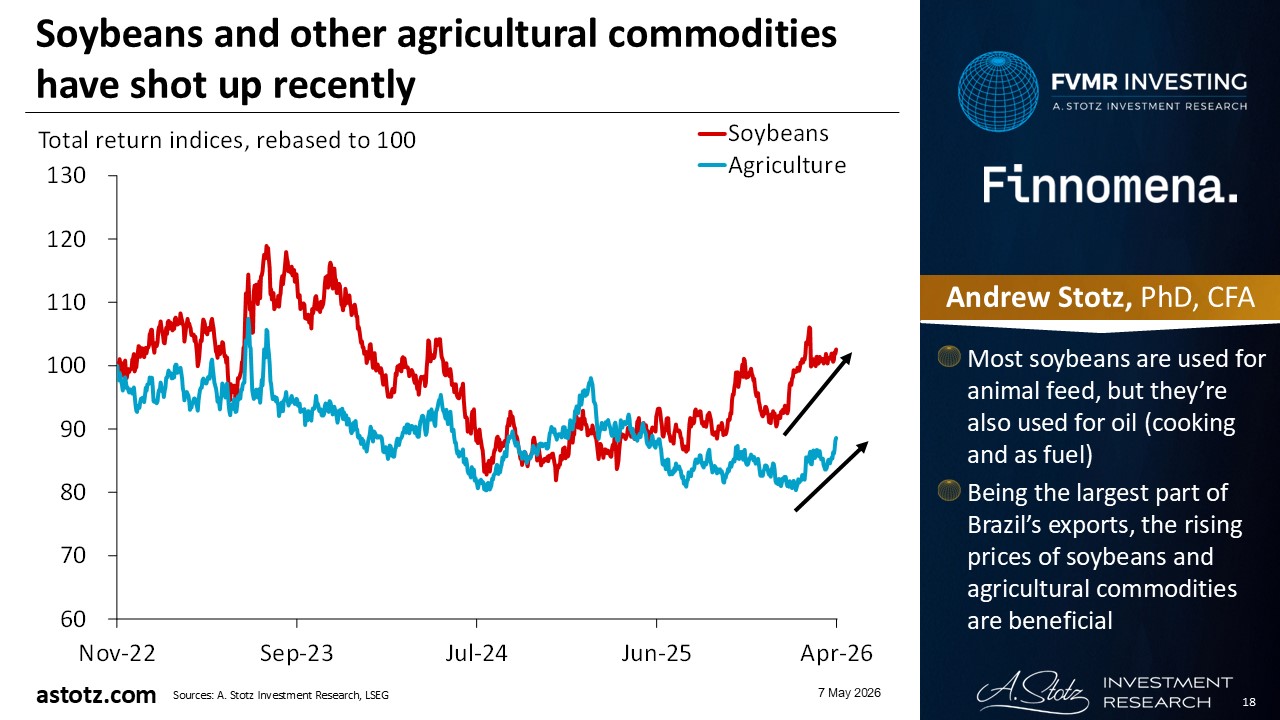

Soybeans and other agricultural commodities have shot up recently

- Most soybeans are used for animal feed, but they’re also used for oil (cooking and as fuel)

- Being the largest part of Brazil’s exports, the rising prices of soybeans and agricultural commodities are beneficial

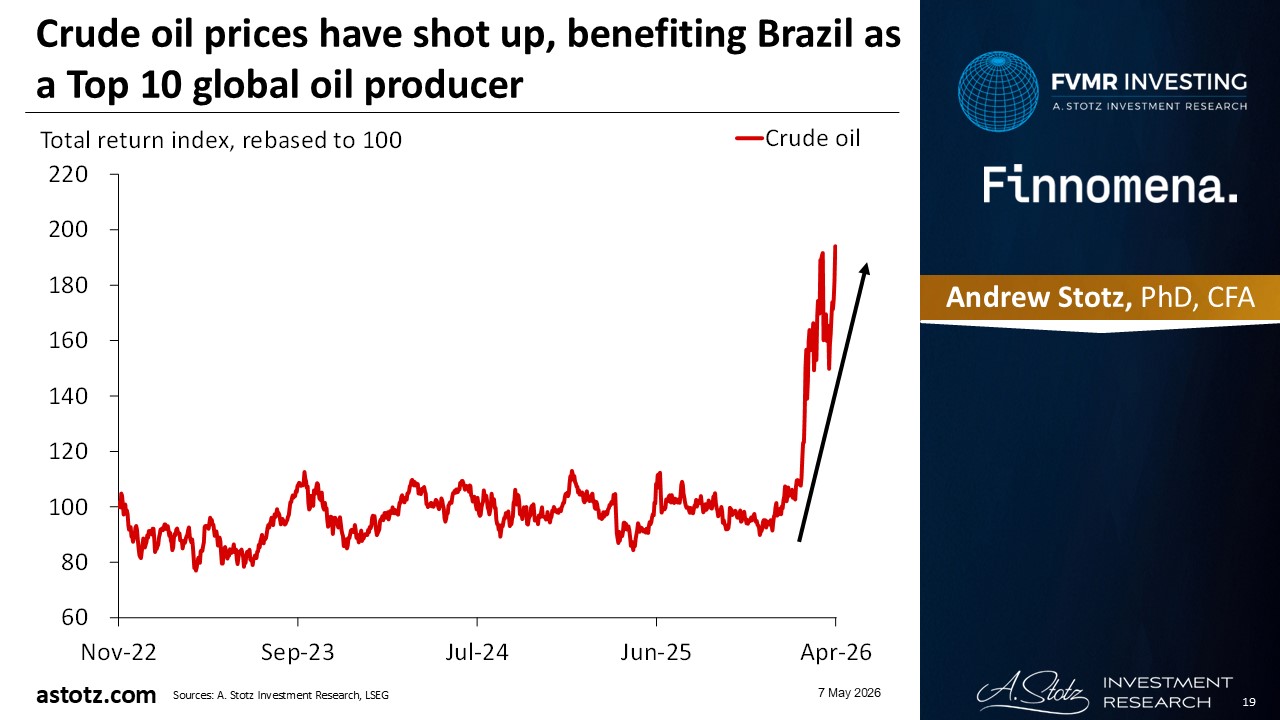

Crude oil prices have shot up, benefiting Brazil as a Top 10 global oil producer

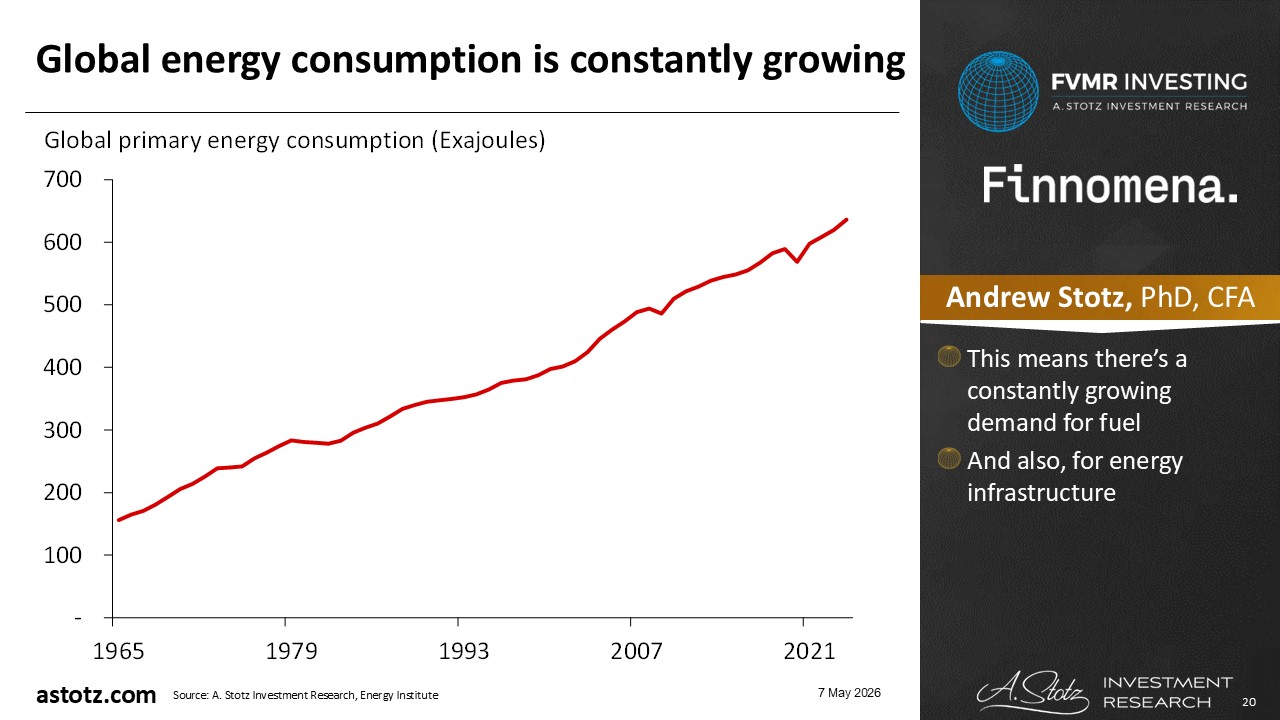

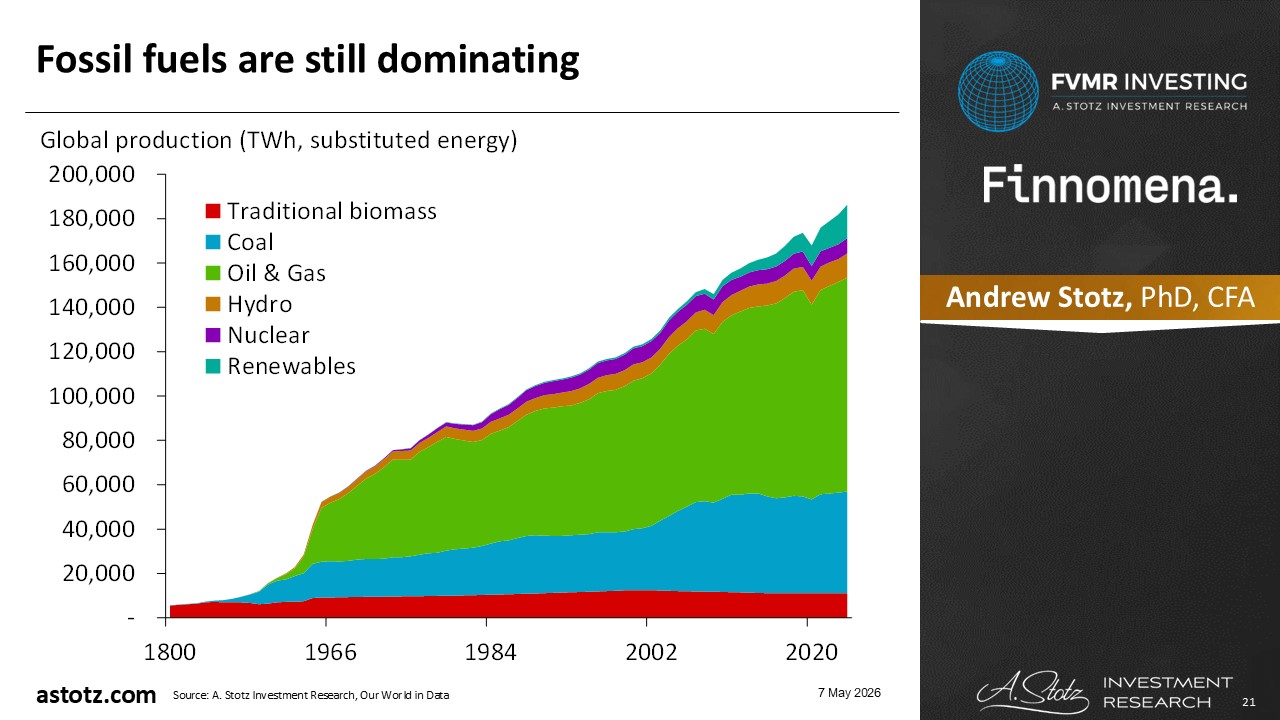

Global energy consumption is constantly growing

- This means there’s a constantly growing demand for fuel

- And also, for energy infrastructure

Fossil fuels are still dominating

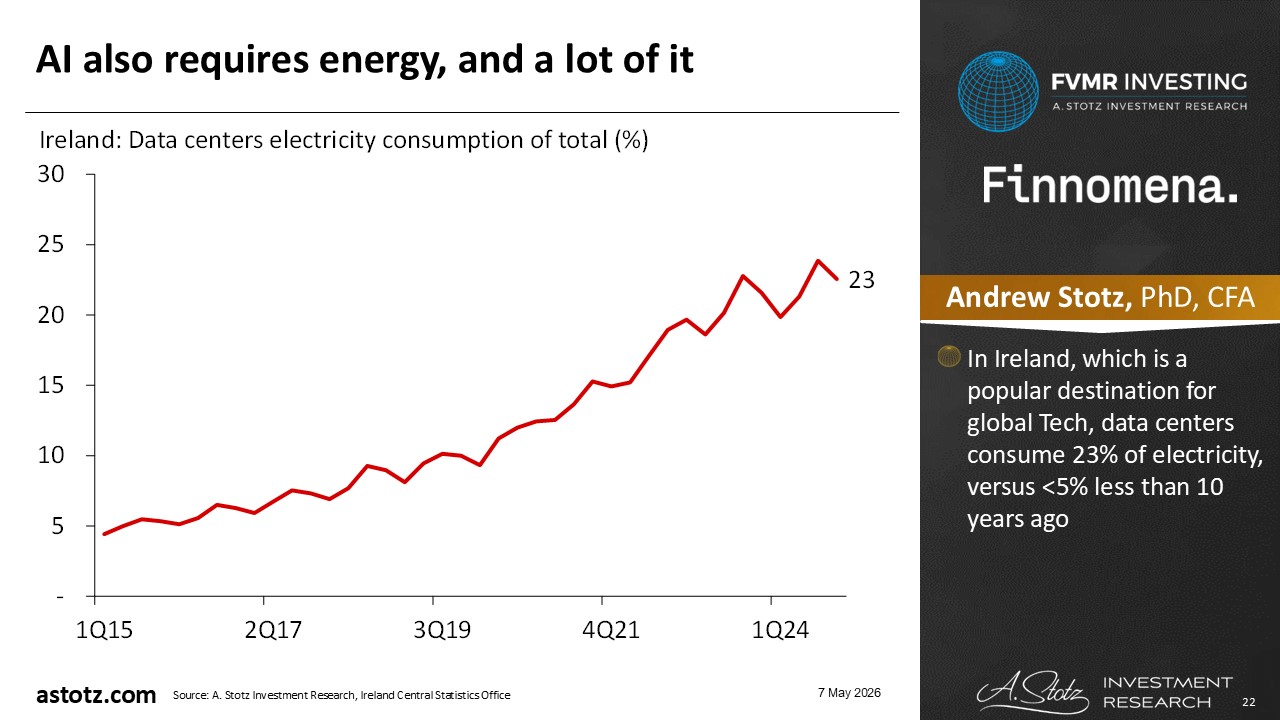

AI also requires energy, and a lot of it

- In Ireland, which is a popular destination for global Tech, data centers consume 23% of electricity, versus <5% less than 10 years ago

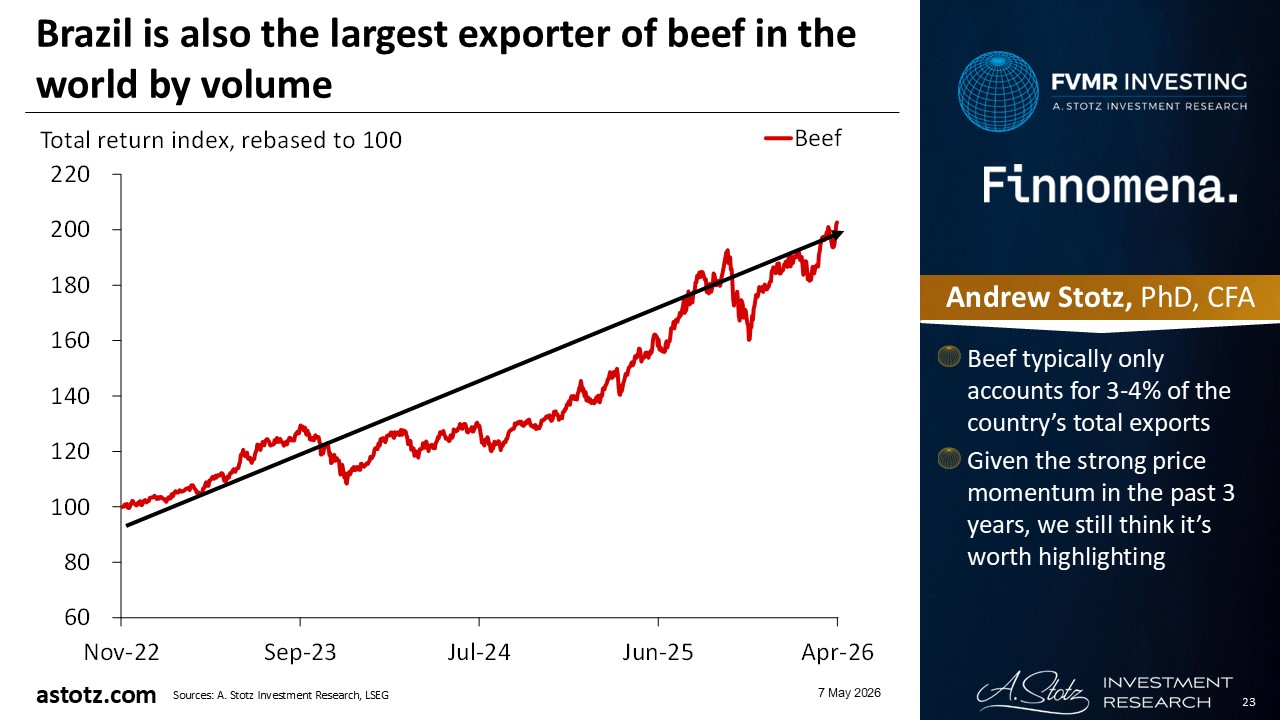

Brazil is also the largest exporter of beef in the world by volume

- Beef typically only accounts for 3-4% of the country’s total exports

- Given the strong price momentum in the past 3 years, we still think it’s worth highlighting

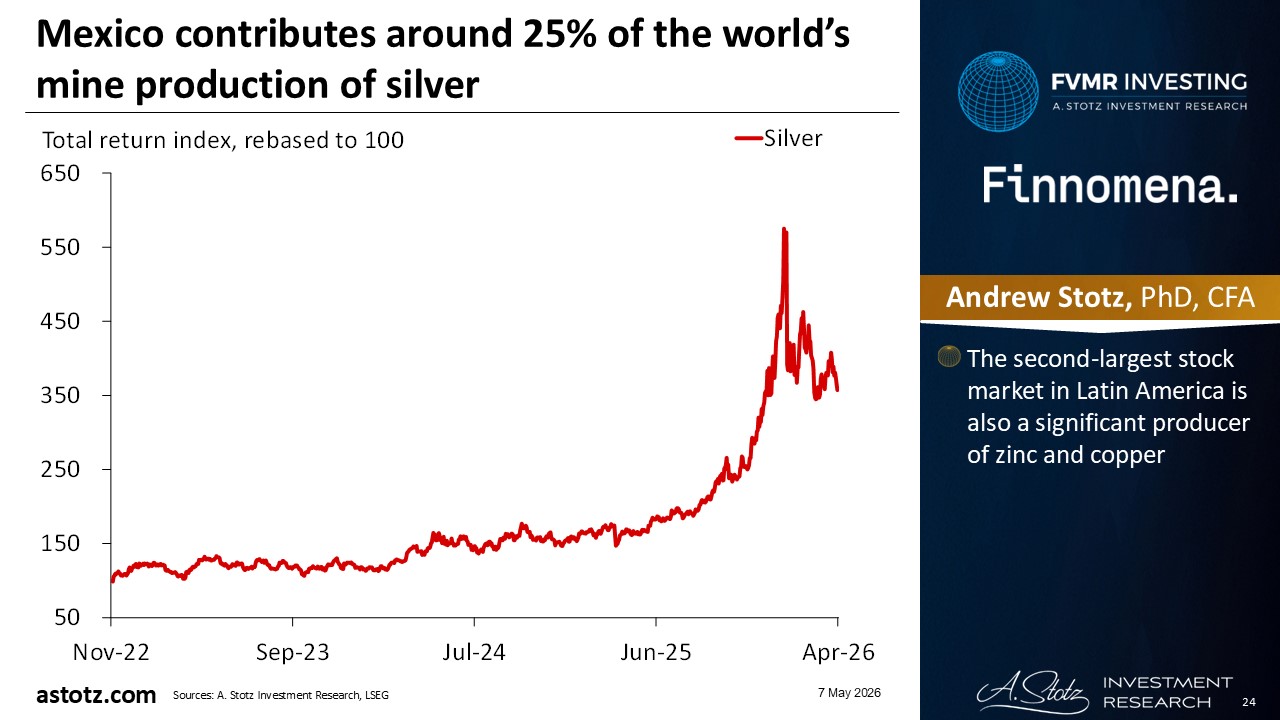

Mexico contributes around 25% of the world’s mine production of silver

- The second-largest stock market in Latin America is also a significant producer of zinc and copper

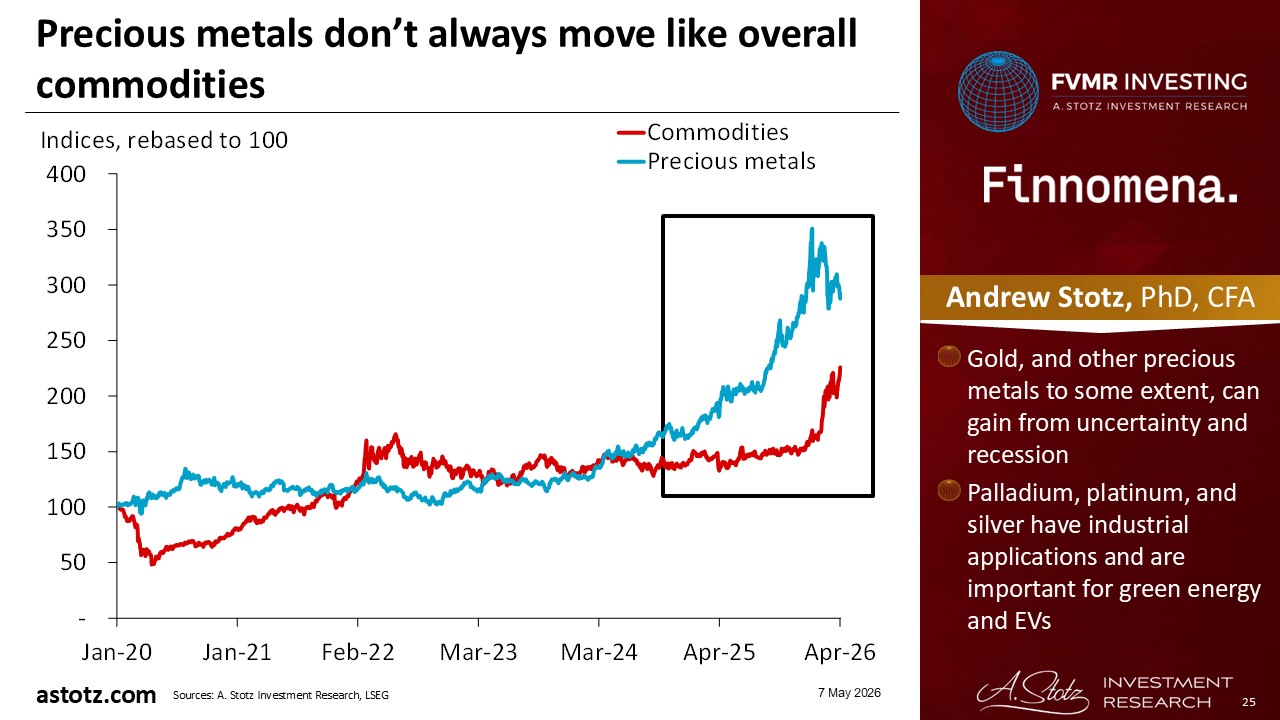

Precious metals don’t always move like overall commodities

- Gold, and other precious metals to some extent, can gain from uncertainty and recession

- Palladium, platinum, and silver have industrial applications and are important for green energy and EVs

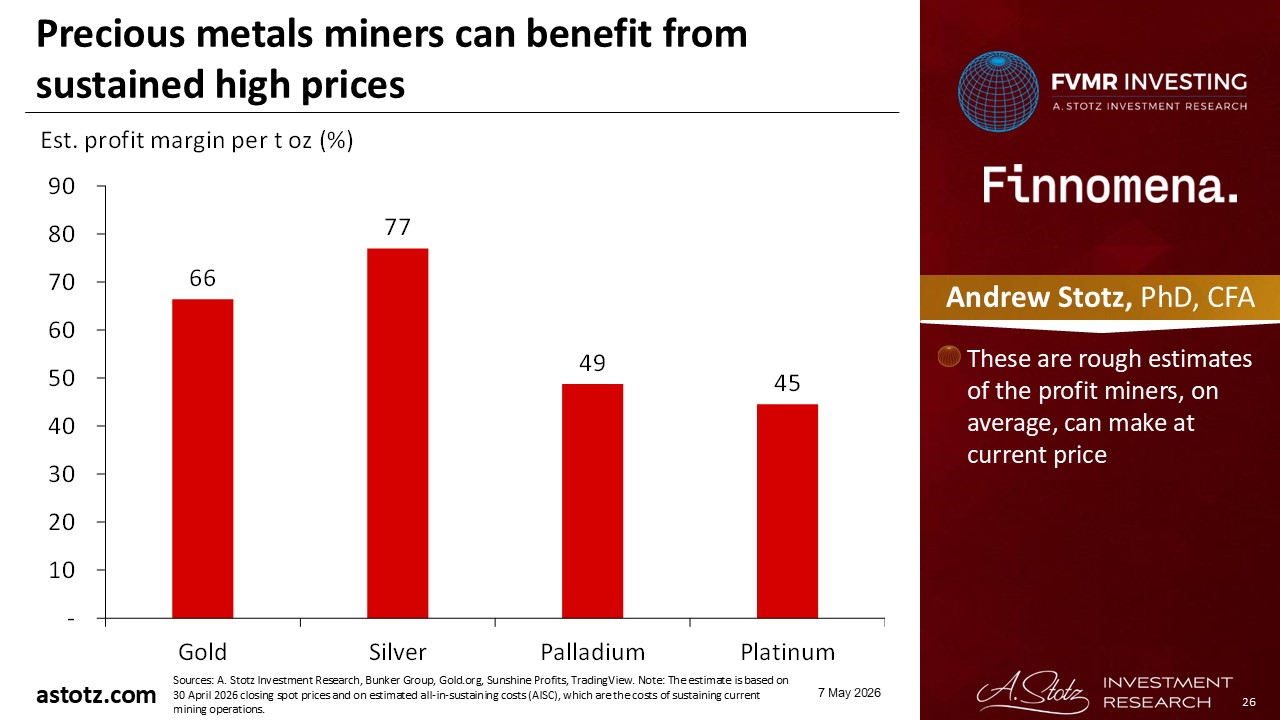

Precious metals miners can benefit from sustained high prices

- These are rough estimates of the profit miners, on average, can make at current price

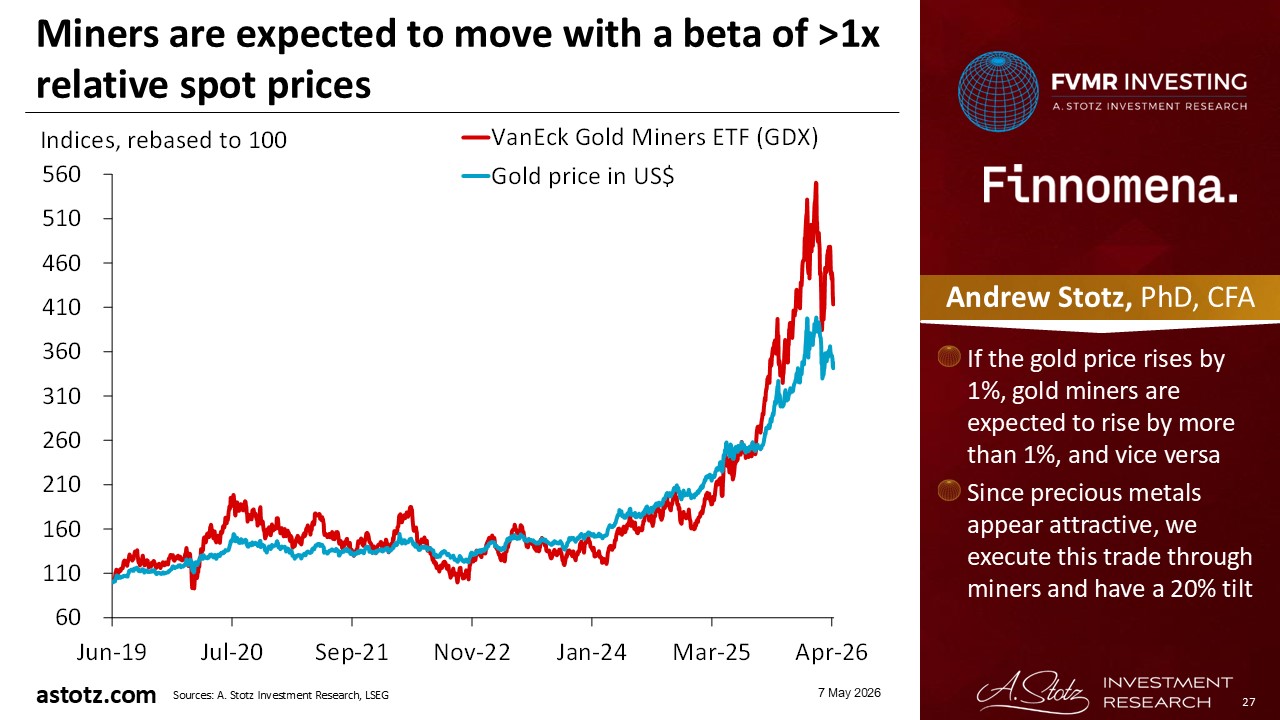

Miners are expected to move with a beta of >1x relative spot prices

- If the gold price rises by 1%, gold miners are expected to rise by more than 1%, and vice versa

- Since precious metals appear attractive, we execute this trade through miners and have a 20% tilt

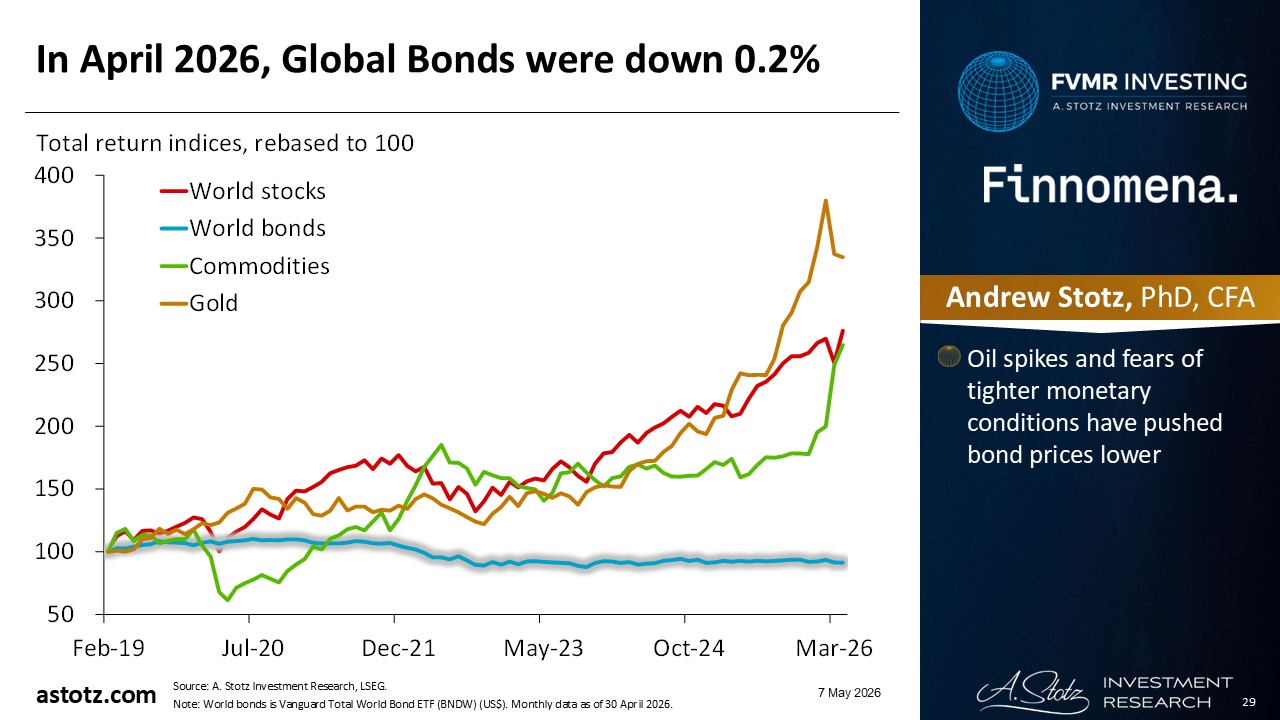

In April 2026, Global Bonds were down 0.2%

- Oil spikes and fears of tighter monetary conditions have pushed bond prices lower

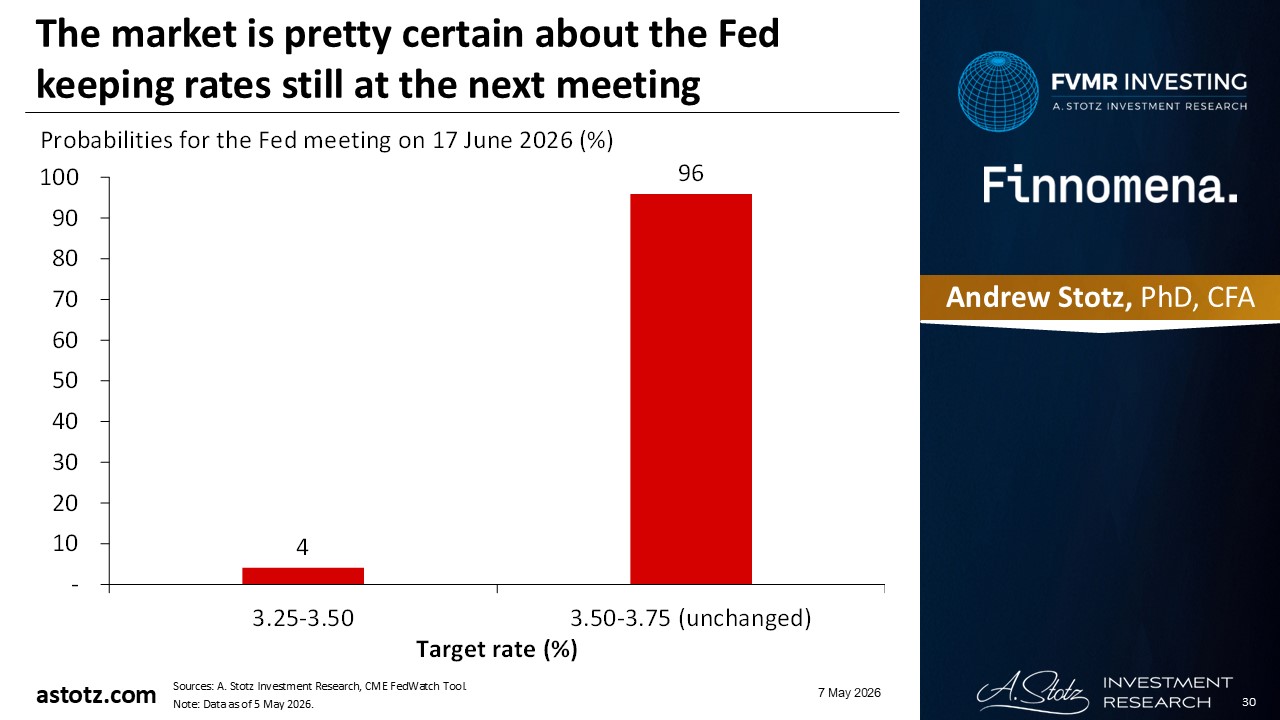

The market is pretty certain about the Fed keeping rates still at the next meeting

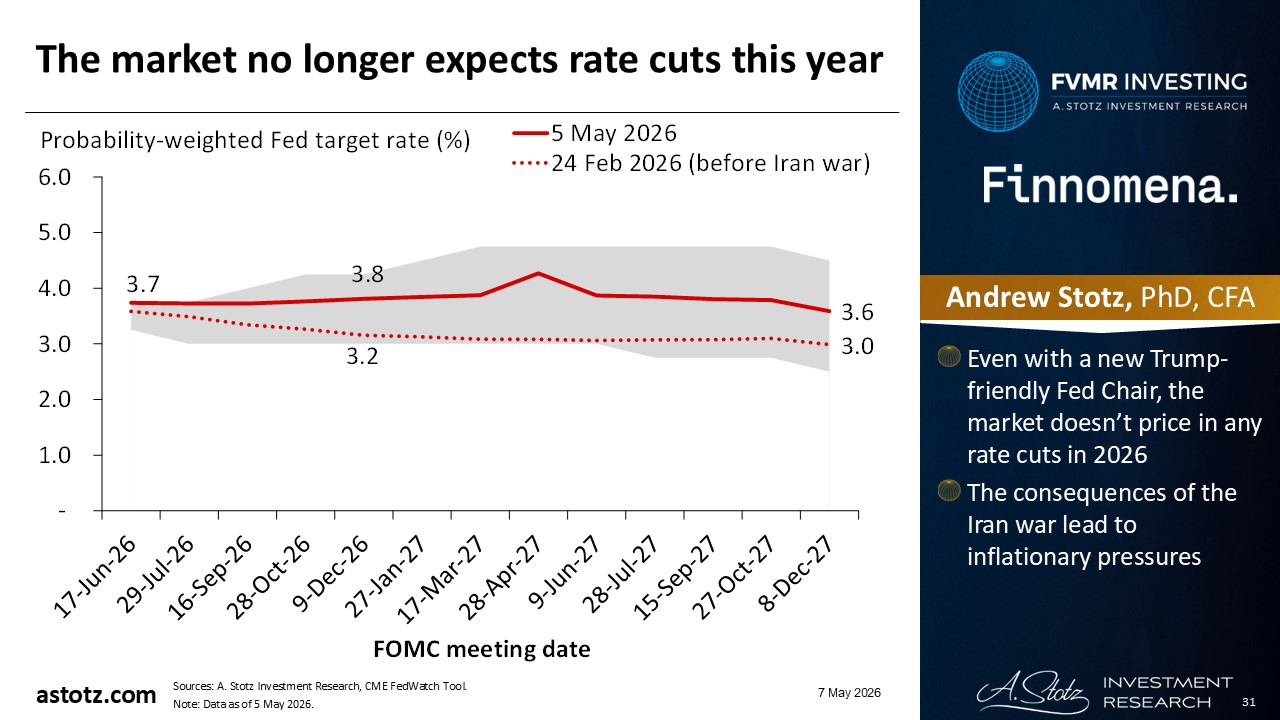

The market no longer expects rate cuts this year

- Even with a new Trump-friendly Fed Chair, the market doesn’t price in any rate cuts in 2026

- The consequences of the Iran war lead to inflationary pressures

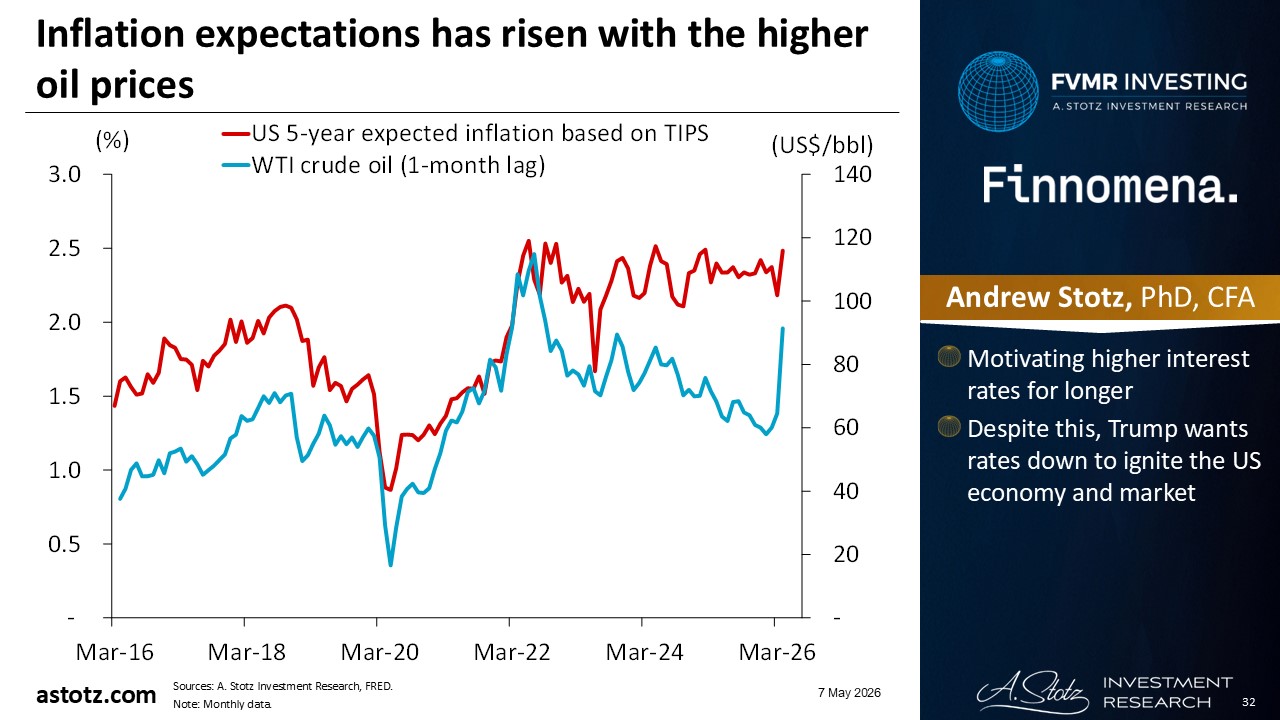

Inflation expectations has risen with the higher oil prices

- Motivating higher interest rates for longer

- Despite this, Trump wants rates down to ignite the US economy and market

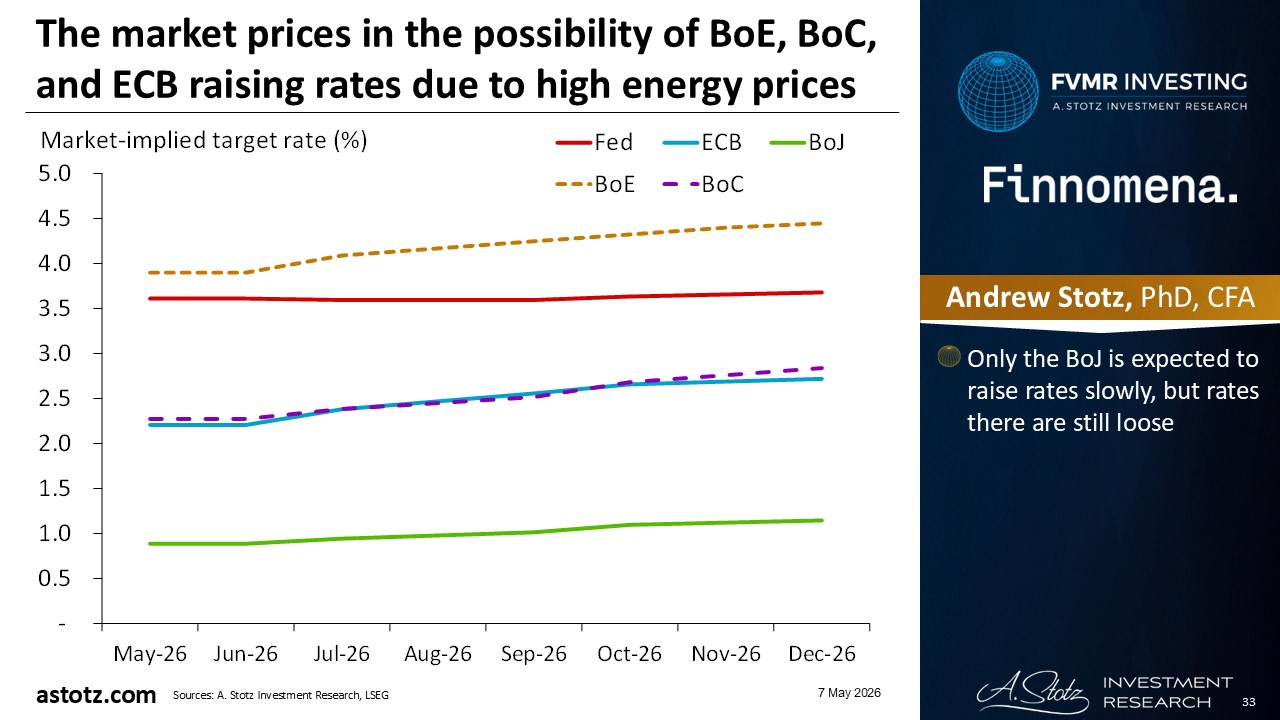

The market prices in the possibility of BoE, BoC, and ECB raising rates due to high energy prices

- Only the BoJ is expected to raise rates slowly, but rates there are still loose

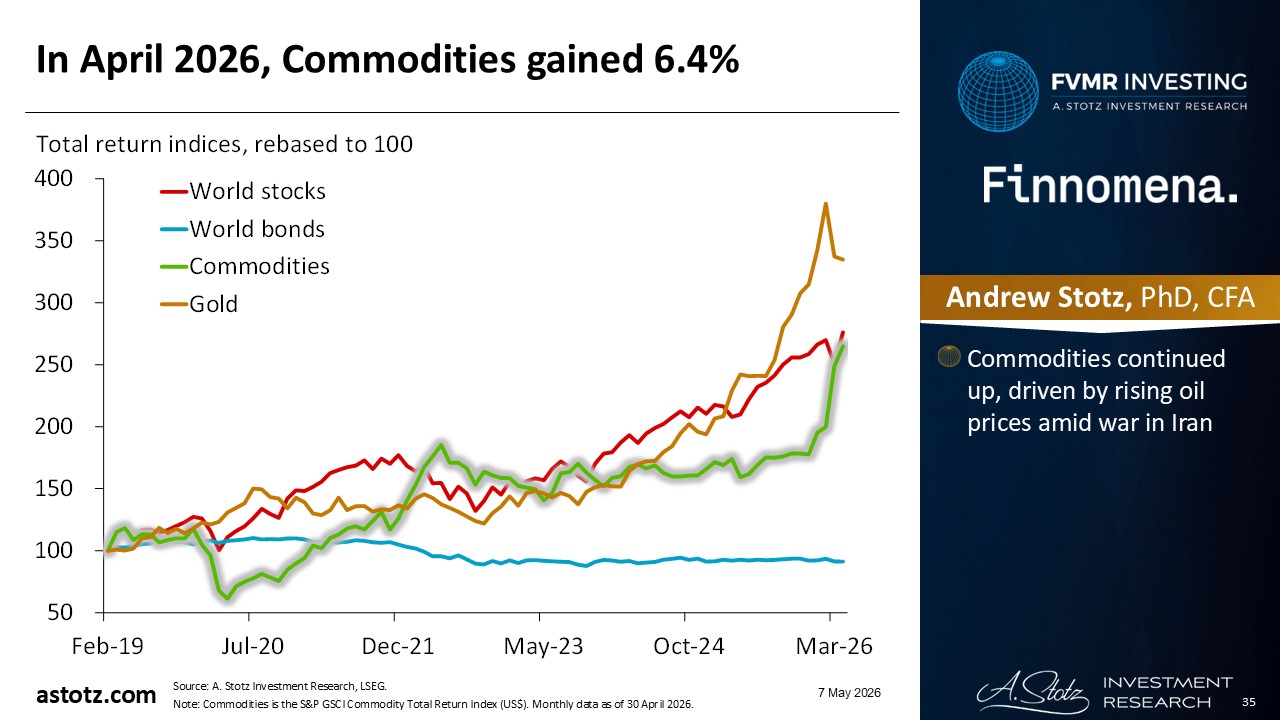

In April 2026, Commodities gained 6.4%

- Commodities continued up, driven by rising oil prices amid war in Iran

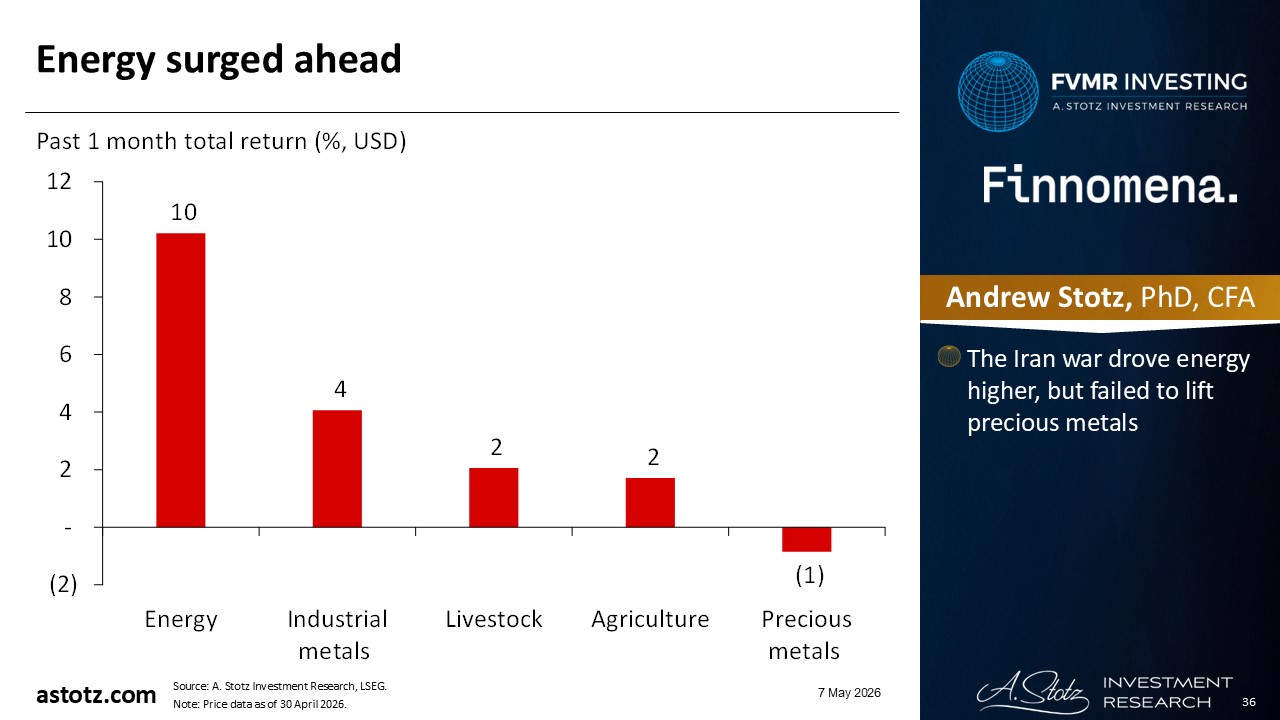

Energy surged ahead

- The Iran war drove energy higher, but failed to lift precious metals

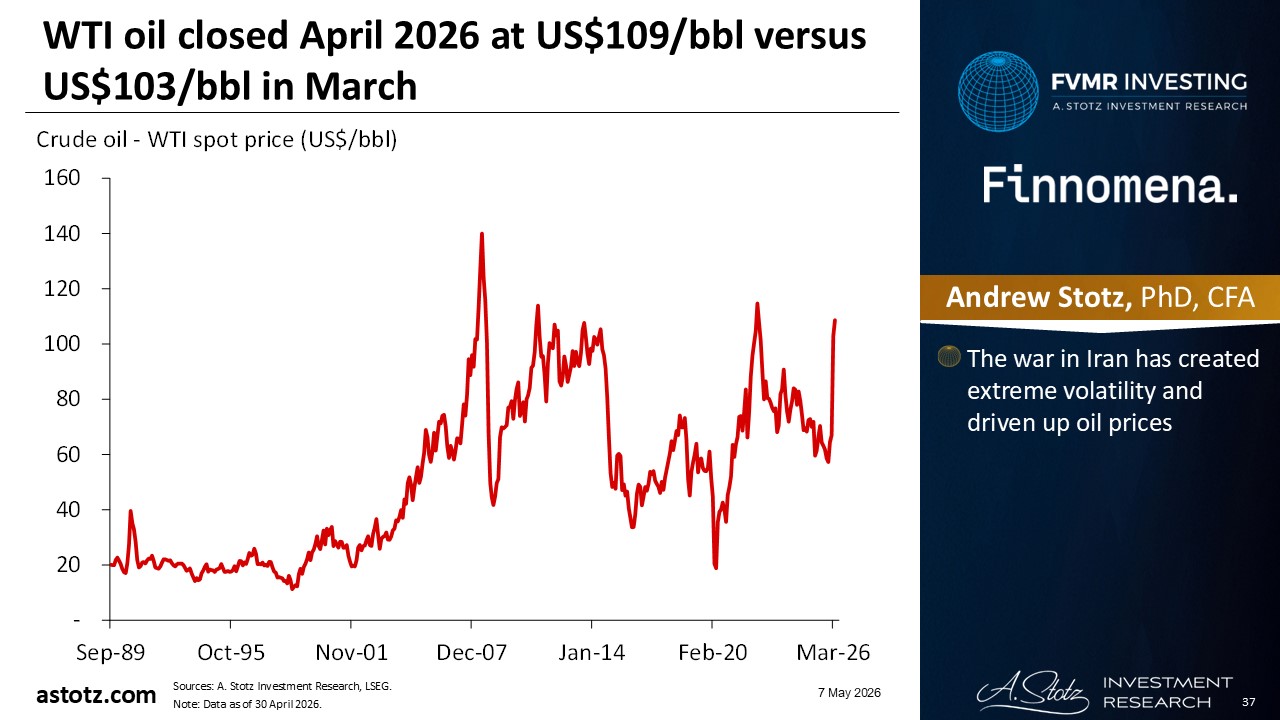

WTI oil closed April 2026 at US$109/bbl versus US$103/bbl in March

- The war in Iran has created extreme volatility and driven up oil prices

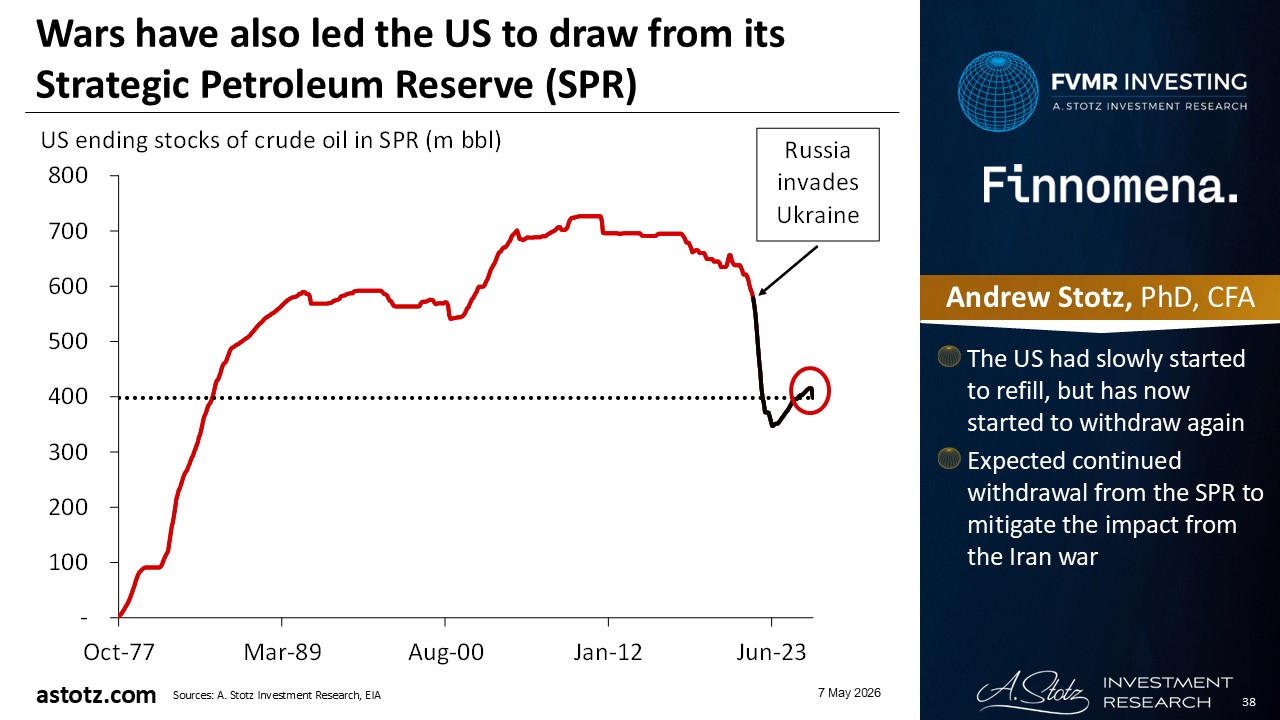

Wars have also led the US to draw from its Strategic Petroleum Reserve (SPR)

- The US had slowly started to refill, but has now started to withdraw again

- Expected continued withdrawal from the SPR to mitigate the impact from the Iran war

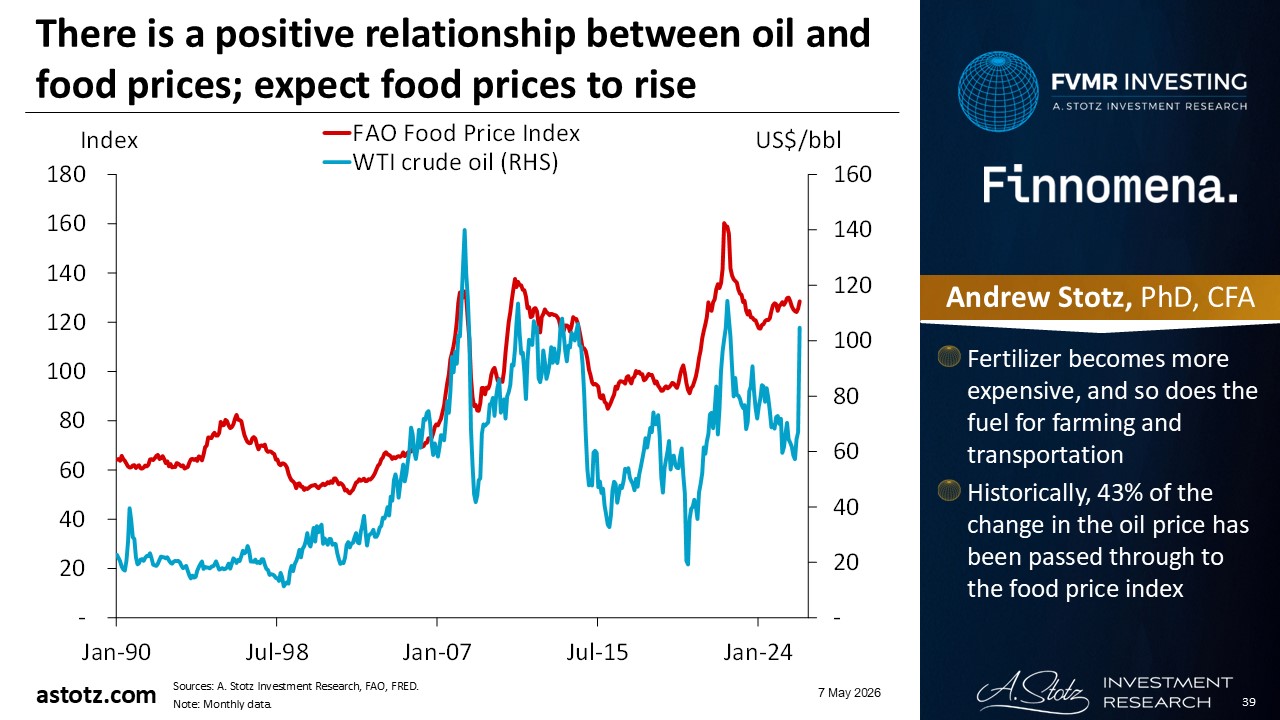

There is a positive relationship between oil and food prices; expect food prices to rise

- Fertilizer becomes more expensive, and so does the fuel for farming and transportation

- Historically, 43% of the change in the oil price has been passed through to the food price index

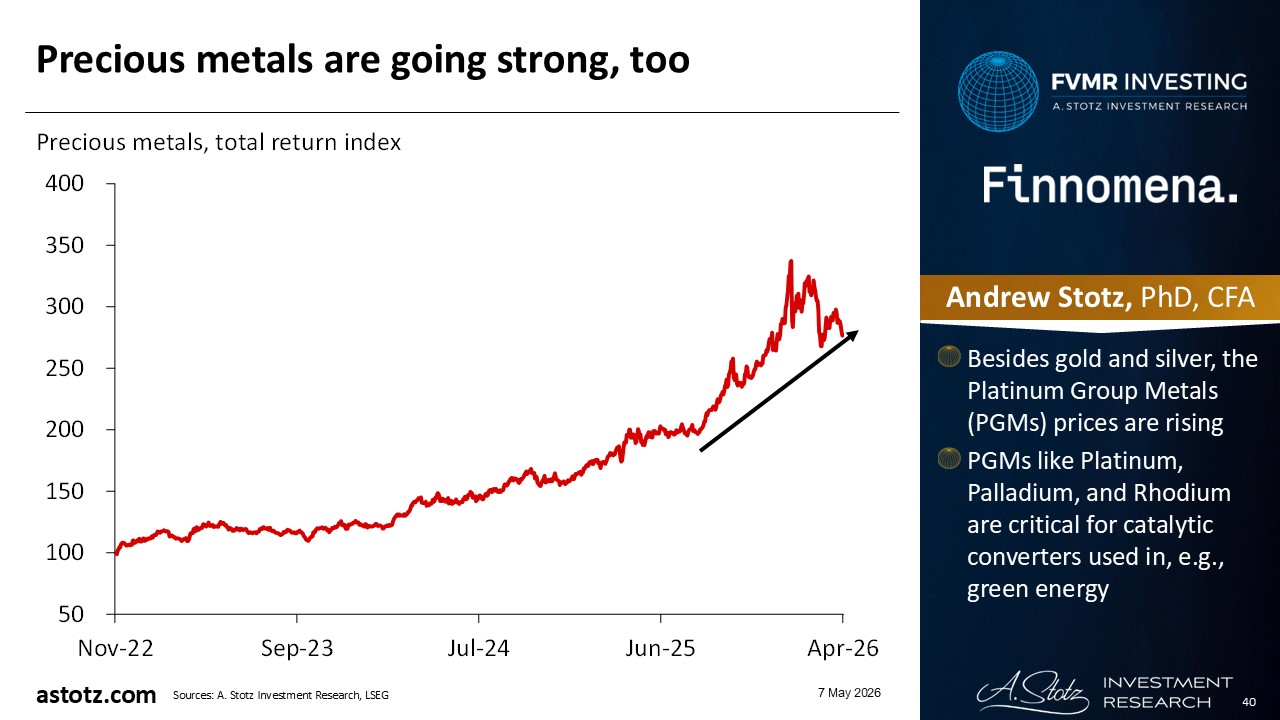

Precious metals are going strong, too

- Besides gold and silver, the Platinum Group Metals (PGMs) prices are rising

- PGMs like Platinum, Palladium, and Rhodium are critical for catalytic converters used in, e.g., green energy

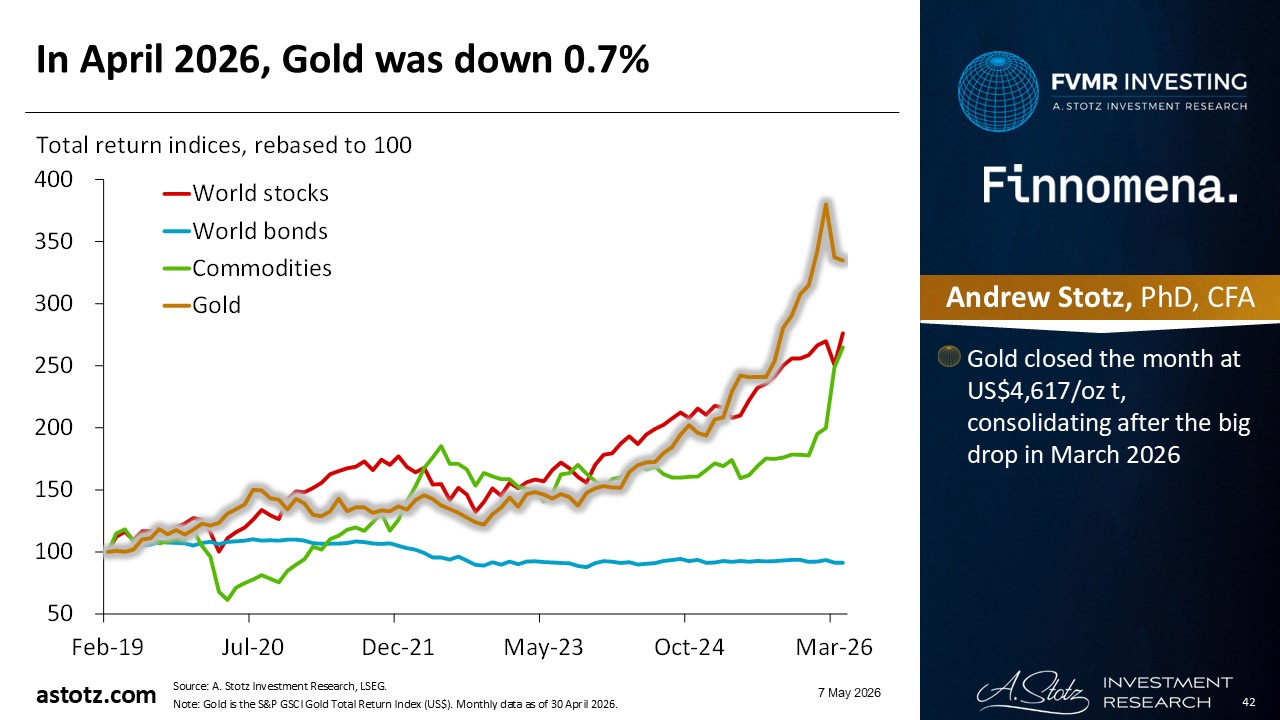

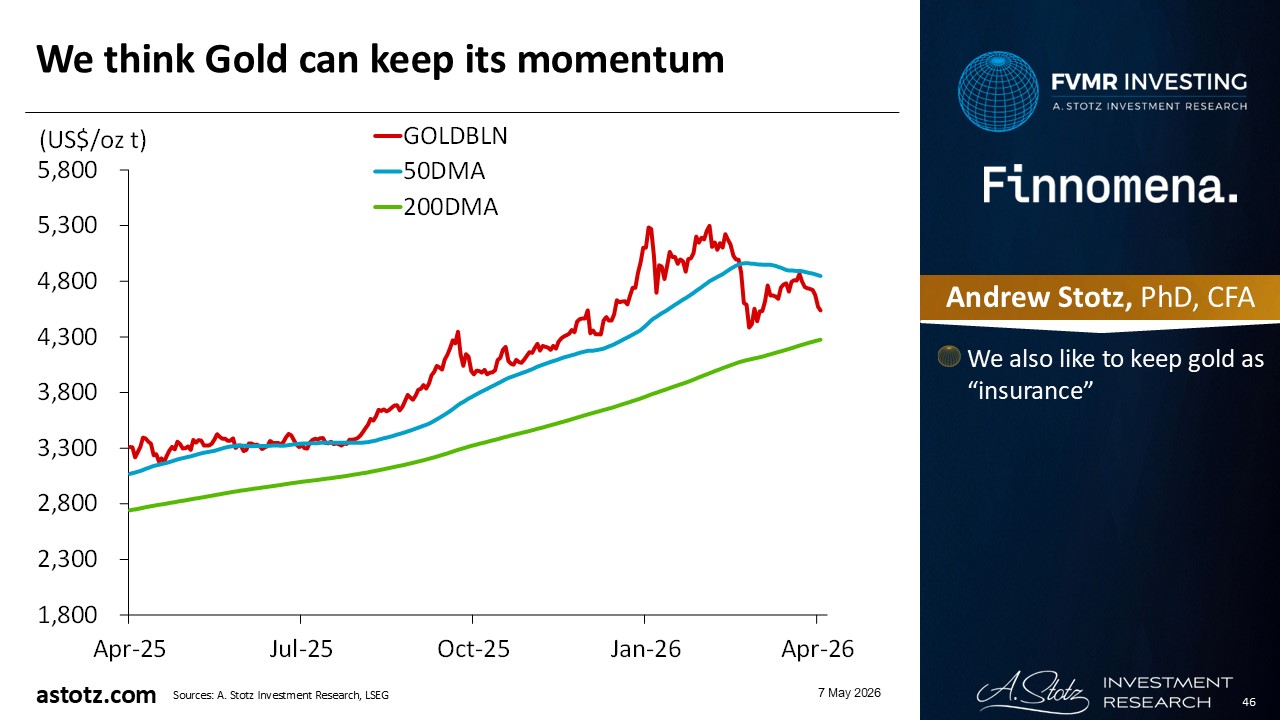

In April 2026, Gold was down 0.7%

- Gold closed the month at US$4,617/oz t, consolidating after the big drop in March 2026

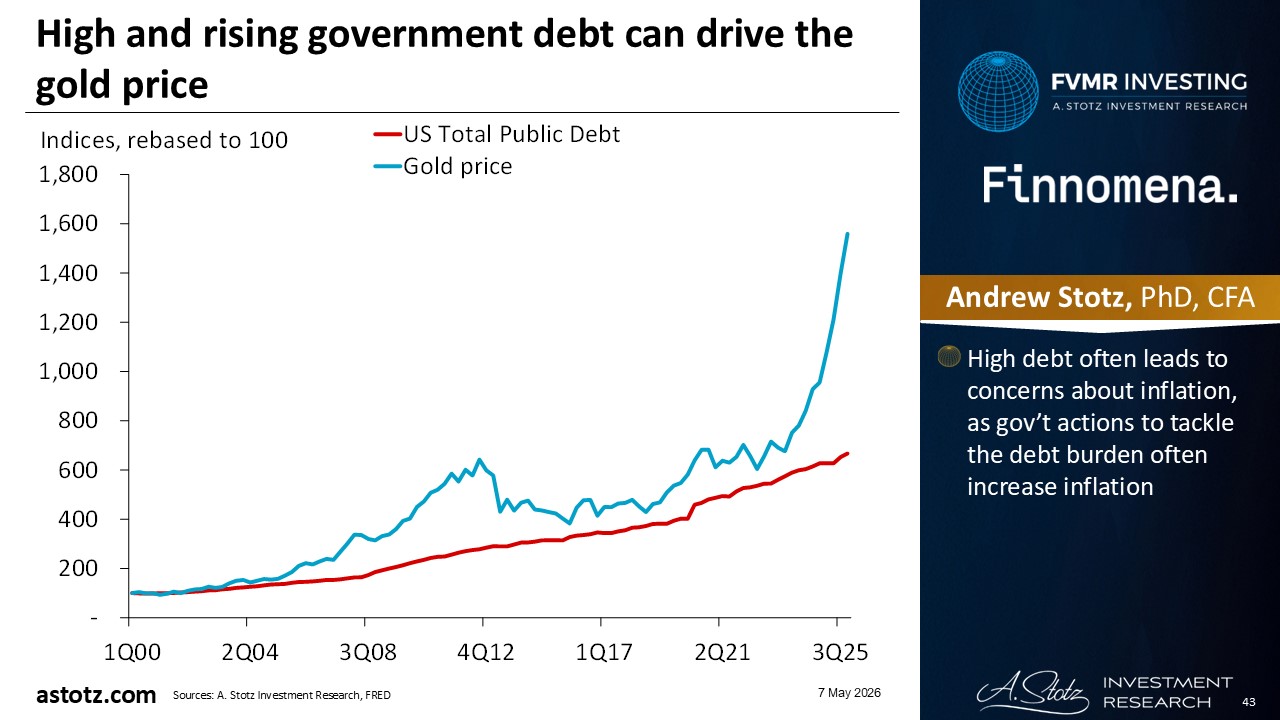

High and rising government debt can drive the gold price

- High debt often leads to concerns about inflation, as gov’t actions to tackle the debt burden often increase inflation

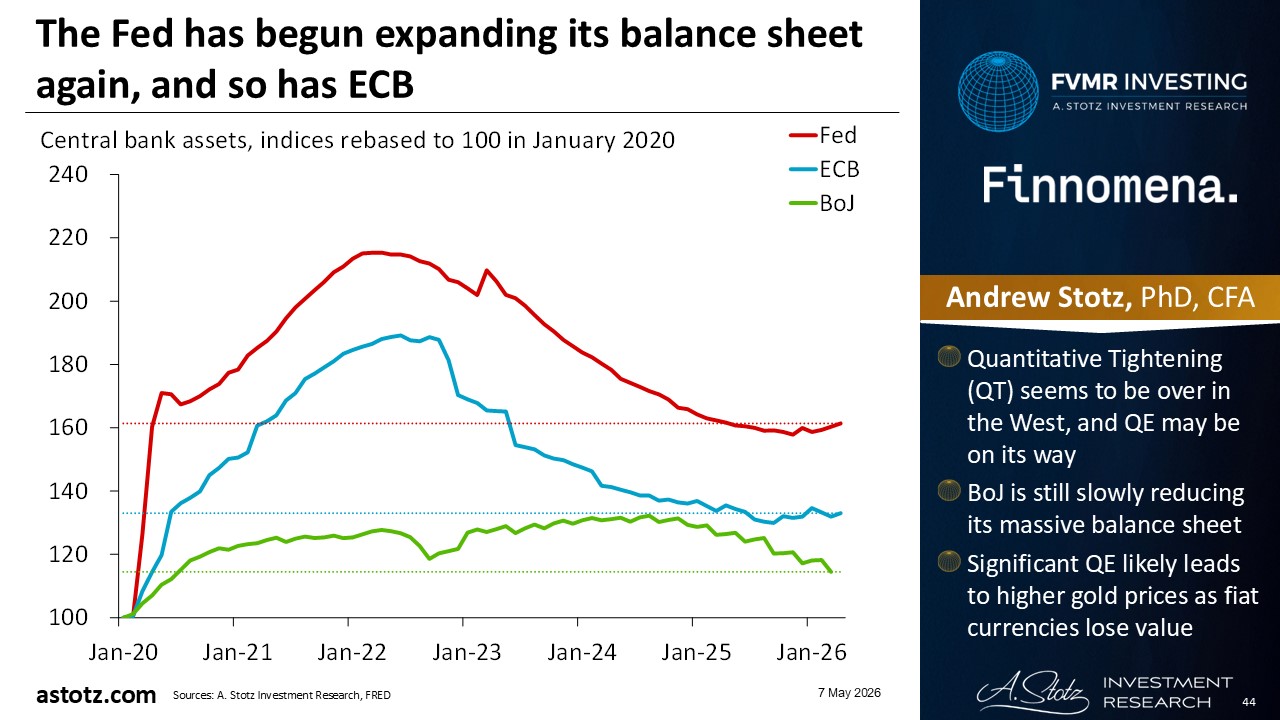

The Fed has begun expanding its balance sheet again, and so has ECB

- Quantitative Tightening (QT) seems to be over in the West, and QE may be on its way

- BoJ is still slowly reducing its massive balance sheet

- Significant QE likely leads to higher gold prices as fiat currencies lose value

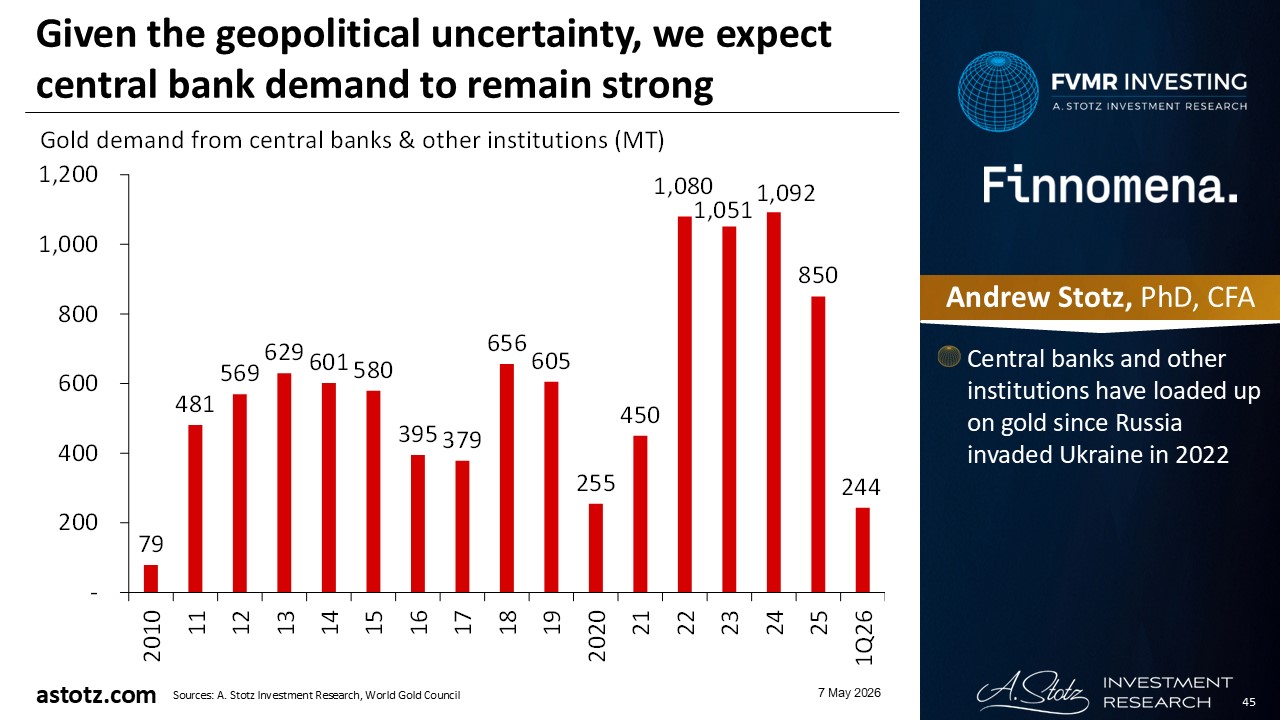

Given the geopolitical uncertainty, we expect central bank demand to remain strong

- Central banks and other institutions have loaded up on gold since Russia invaded Ukraine in 2022

We think Gold can keep its momentum

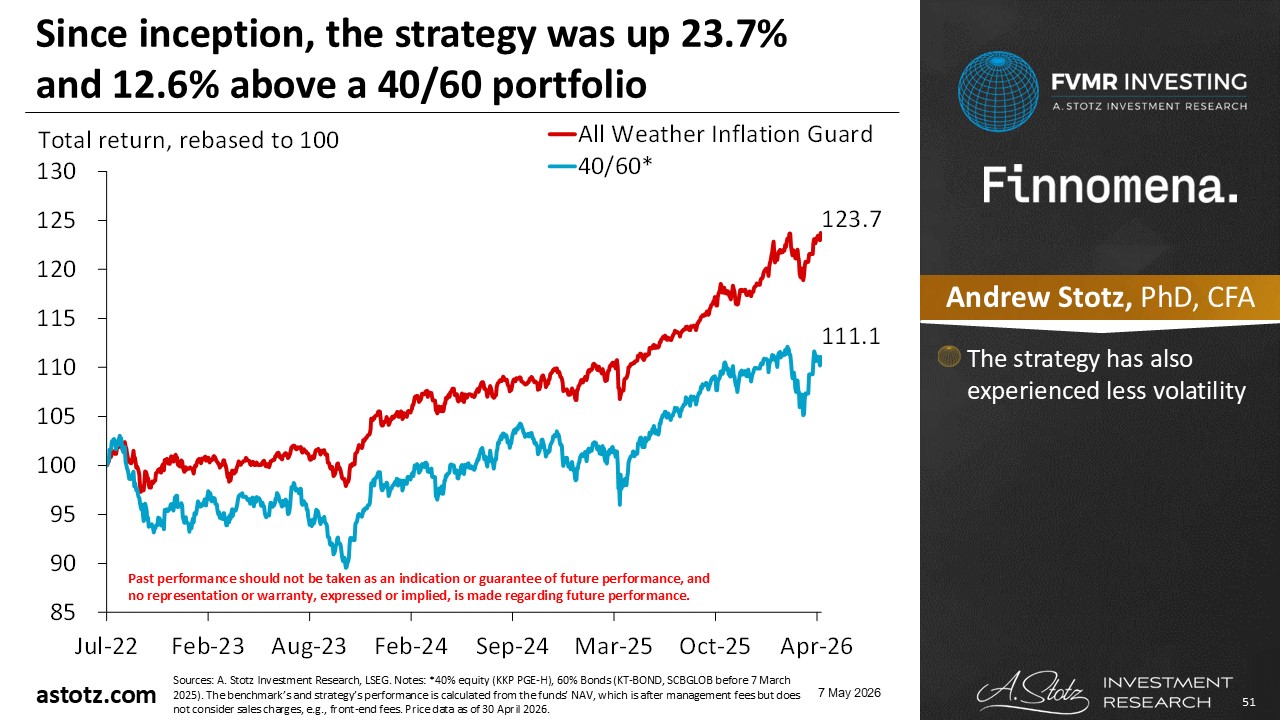

Performance review: All Weather Inflation Guard

All Weather Inflation Guard gained 2.8%

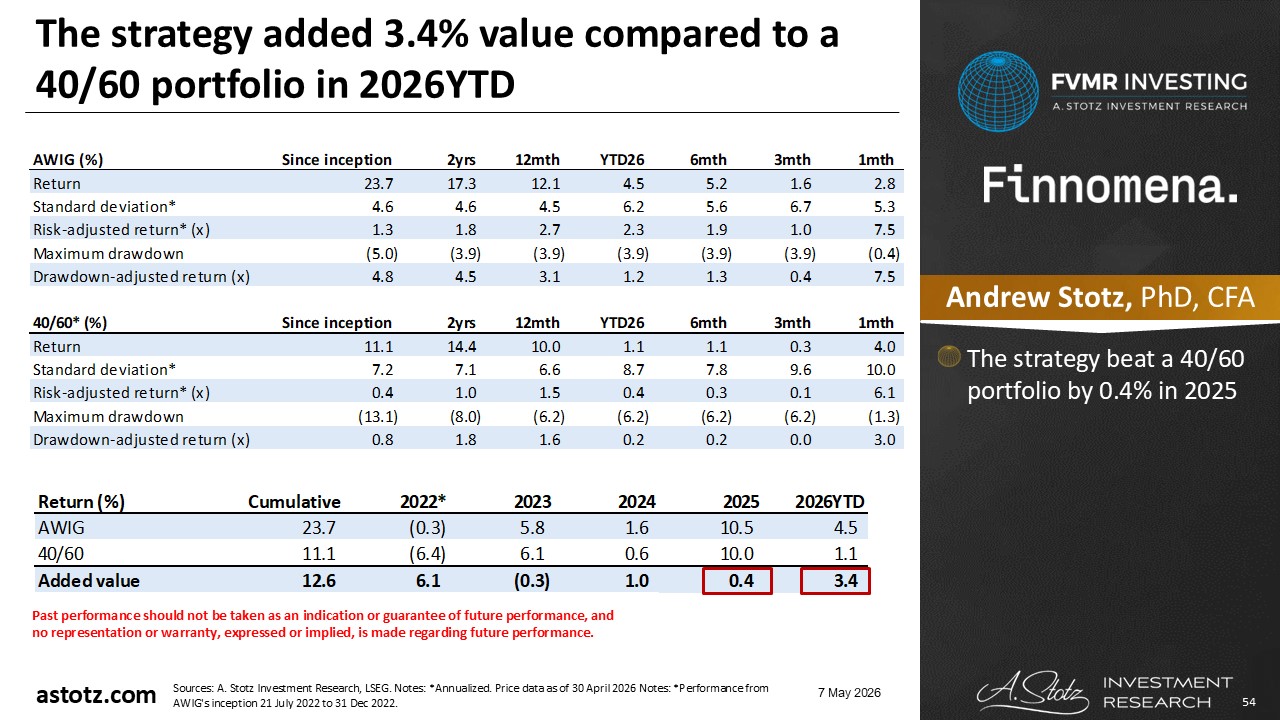

Since inception, the strategy was up 23.7% and 12.6% above a 40/60 portfolio

- The strategy has also experienced less volatility

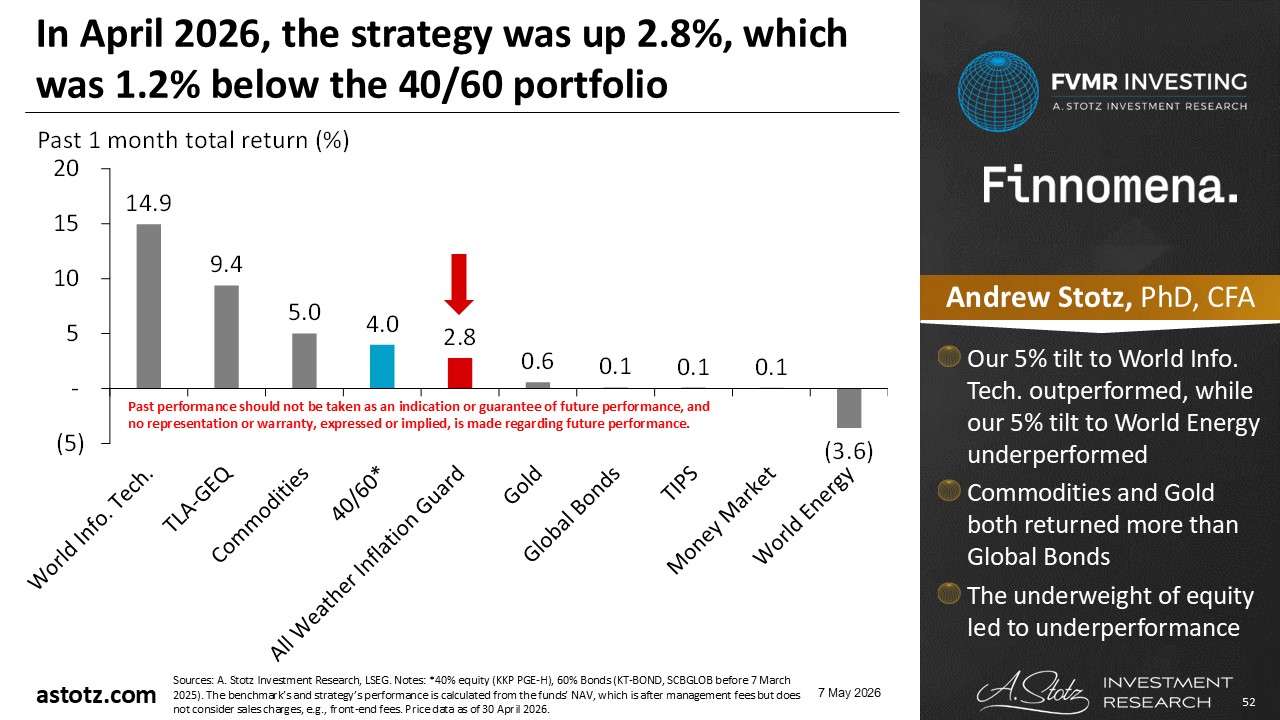

In April 2026, the strategy was up 2.8%, which was 1.2% below the 40/60 portfolio

- Our 5% tilt to World Info. Tech. outperformed, while our 5% tilt to World Energy underperformed

- Commodities and Gold both returned more than Global Bonds

- The underweight of equity led to underperformance

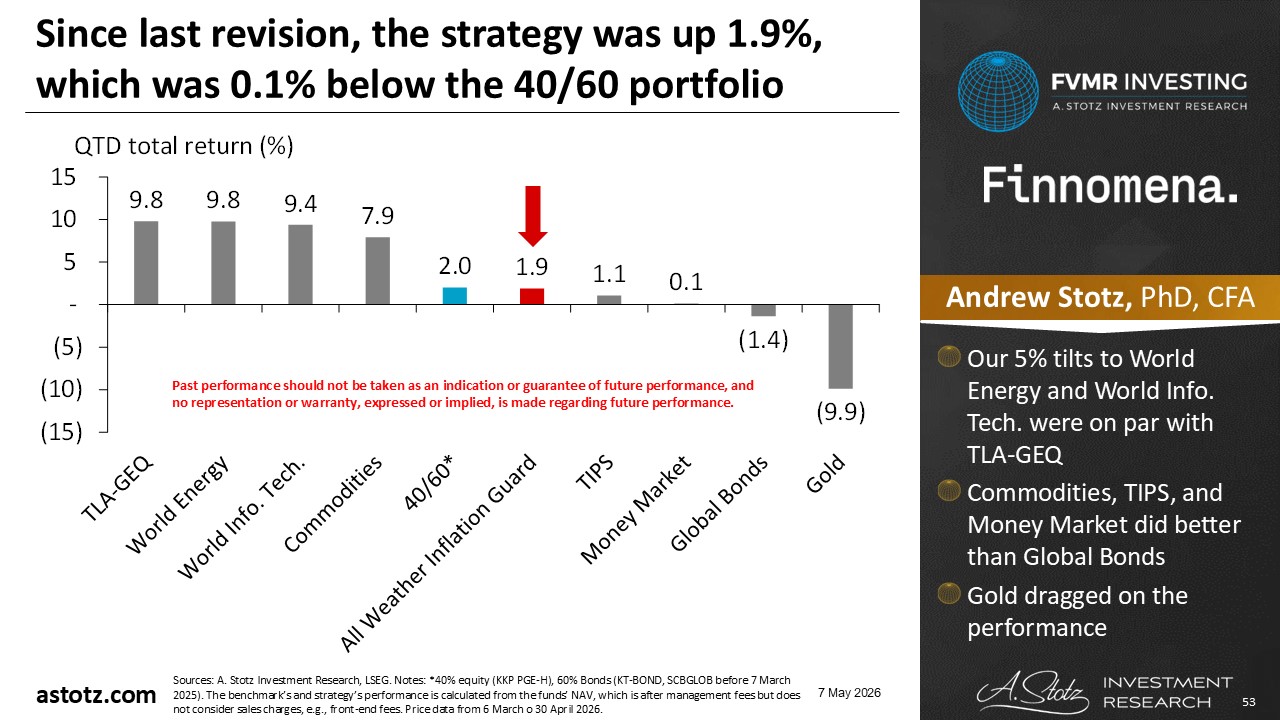

Since last revision, the strategy was down 1.9%, which was 0.1% below the 40/60 portfolio

- Our 5% tilts to World Energy and World Info. Tech. were on par with TLA-GEQ

- Commodities, TIPS, and Money Market did better than Global Bonds

- Gold dragged on the performance

The strategy added 3.4% value compared to a 40/60 portfolio in 2026YTD

- The strategy beat a 40/60 portfolio by 0.4% in 2025

Performance review: All Weather Strategy

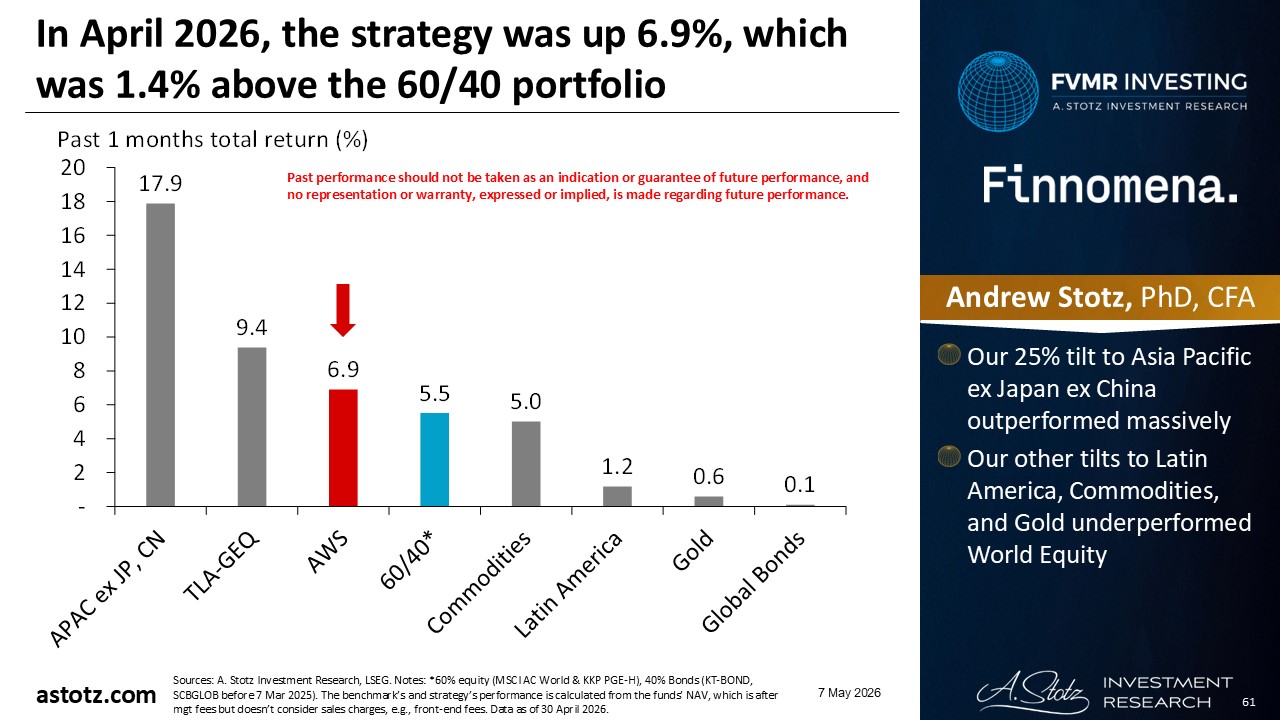

All Weather Strategy gained 6.9%

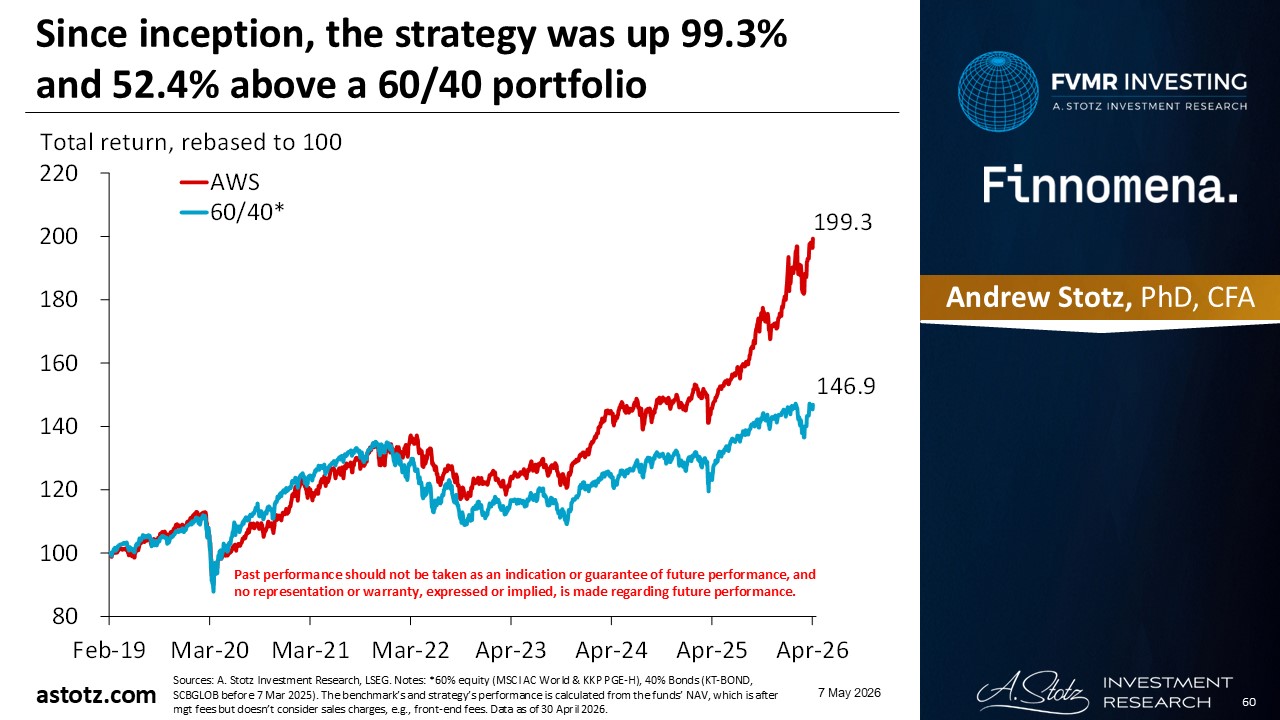

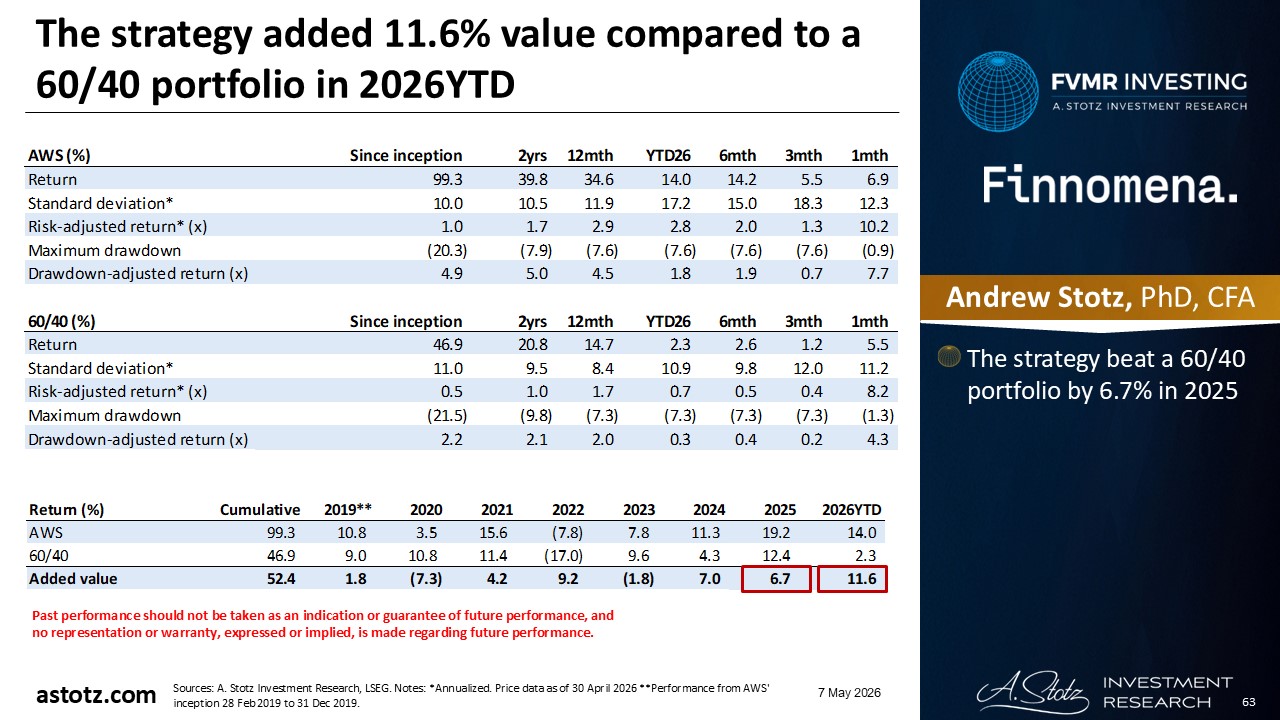

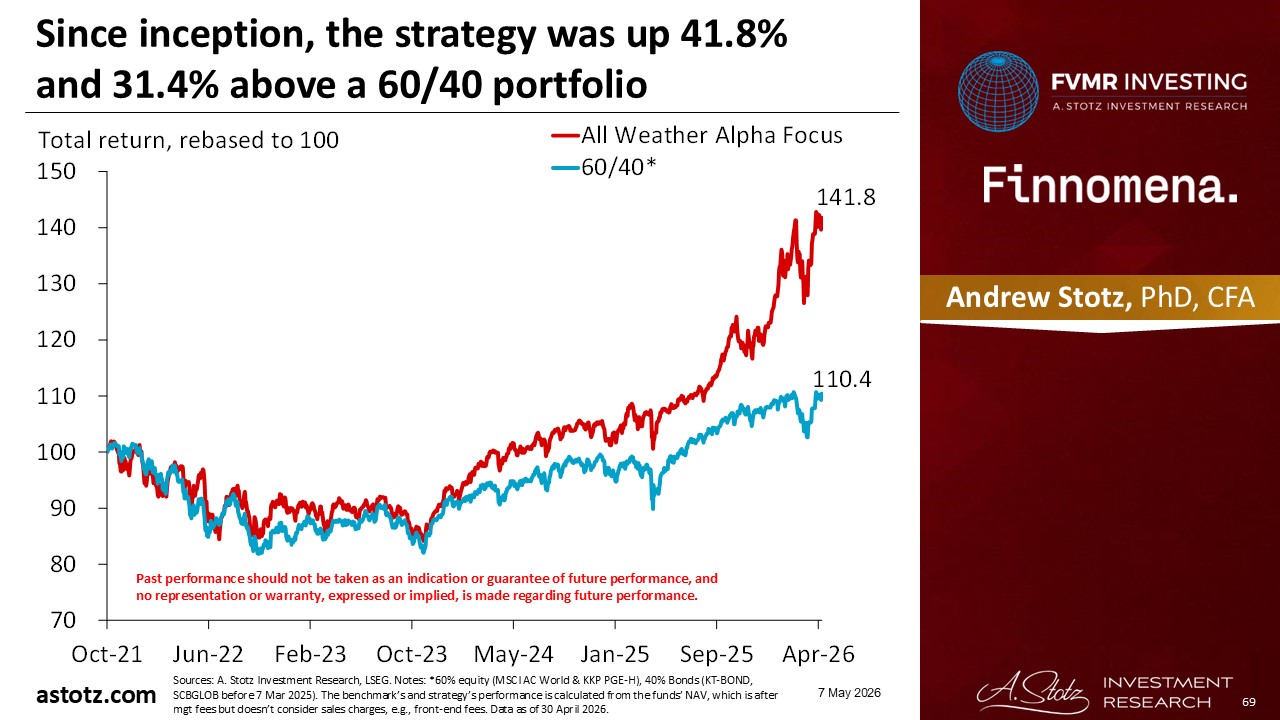

Since inception, the strategy was up 99.3% and 52.4% above a 60/40 portfolio

In April 2026, the strategy was up 6.9%, which was 1.4% above the 60/40 portfolio

- Our 25% tilt to Asia Pacific ex Japan ex China outperformed massively

- Our other tilts to Latin America, Commodities, and Gold underperformed World Equity

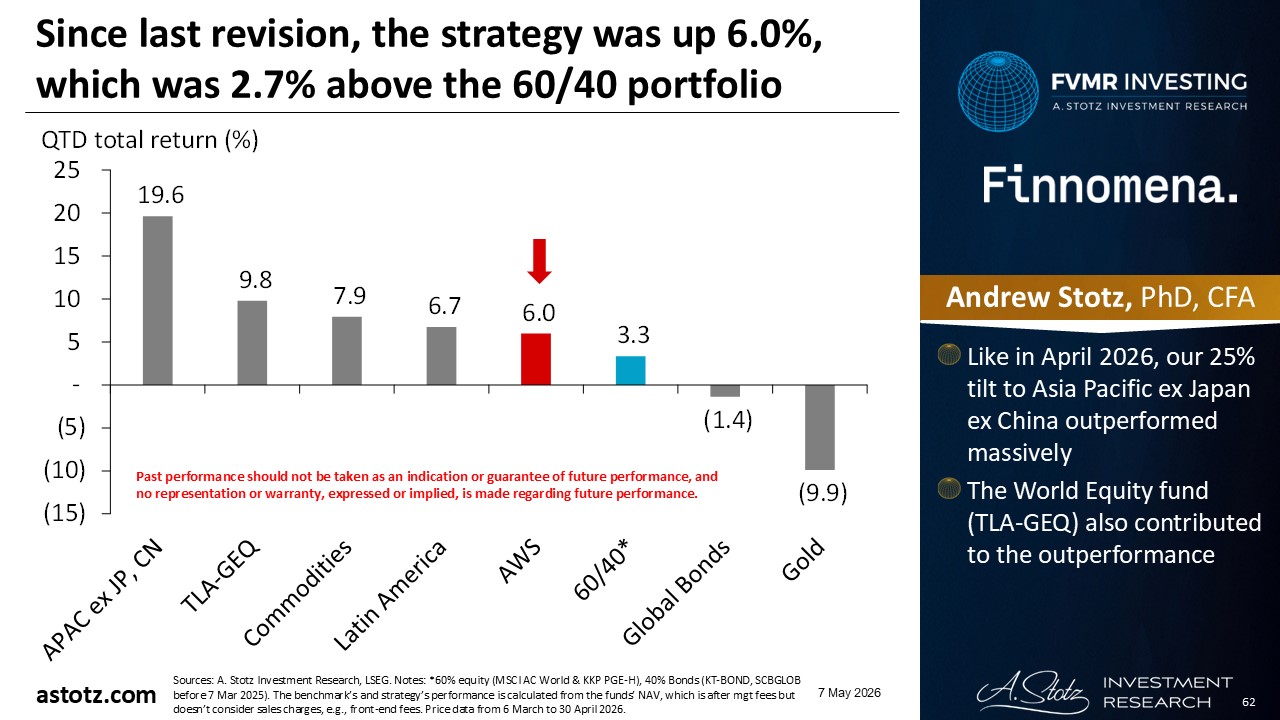

Since last revision, the strategy was down 6.0%, which was 2.7% above the 60/40 portfolio

- Like in April 2026, our 25% tilt to Asia Pacific ex Japan ex China outperformed massively

- The World Equity fund (TLA-GEQ) also contributed to the outperformance

The strategy has added 11.6% value compared to a 60/40 portfolio in 2026YTD

- The strategy beat a 60/40 portfolio by 6.7% in 2025

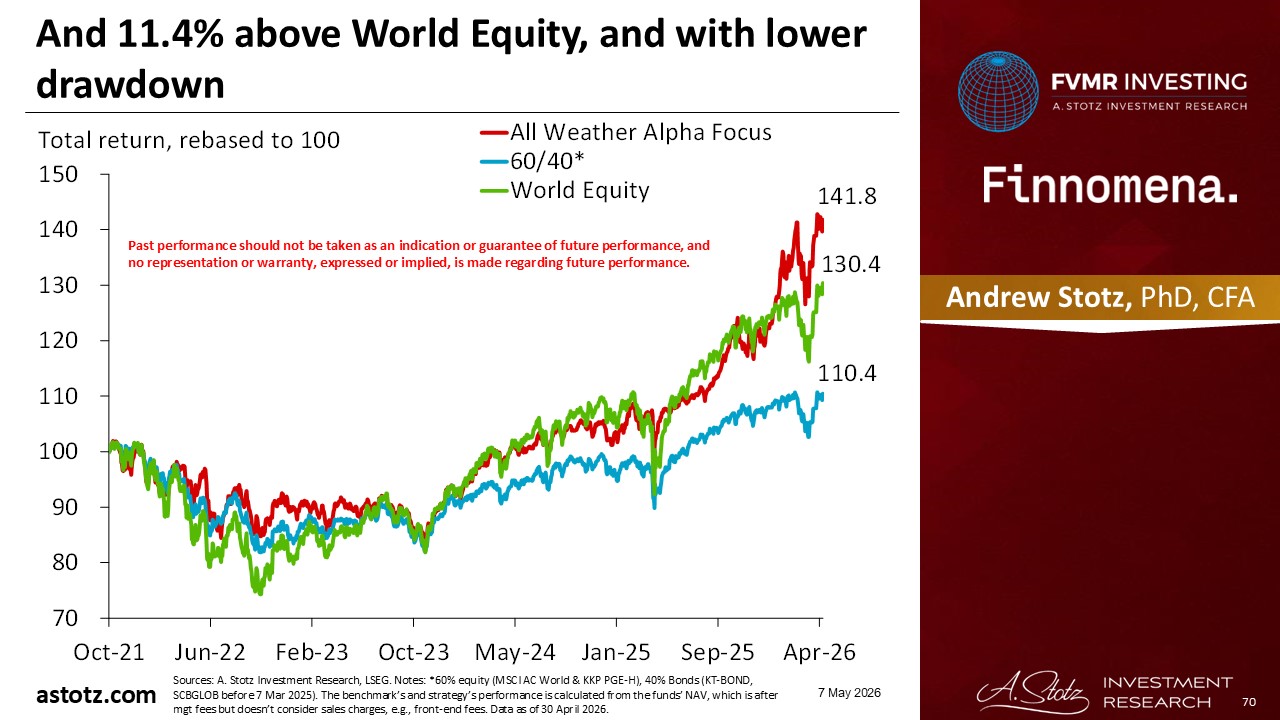

Performance review: All Weather Alpha Focus

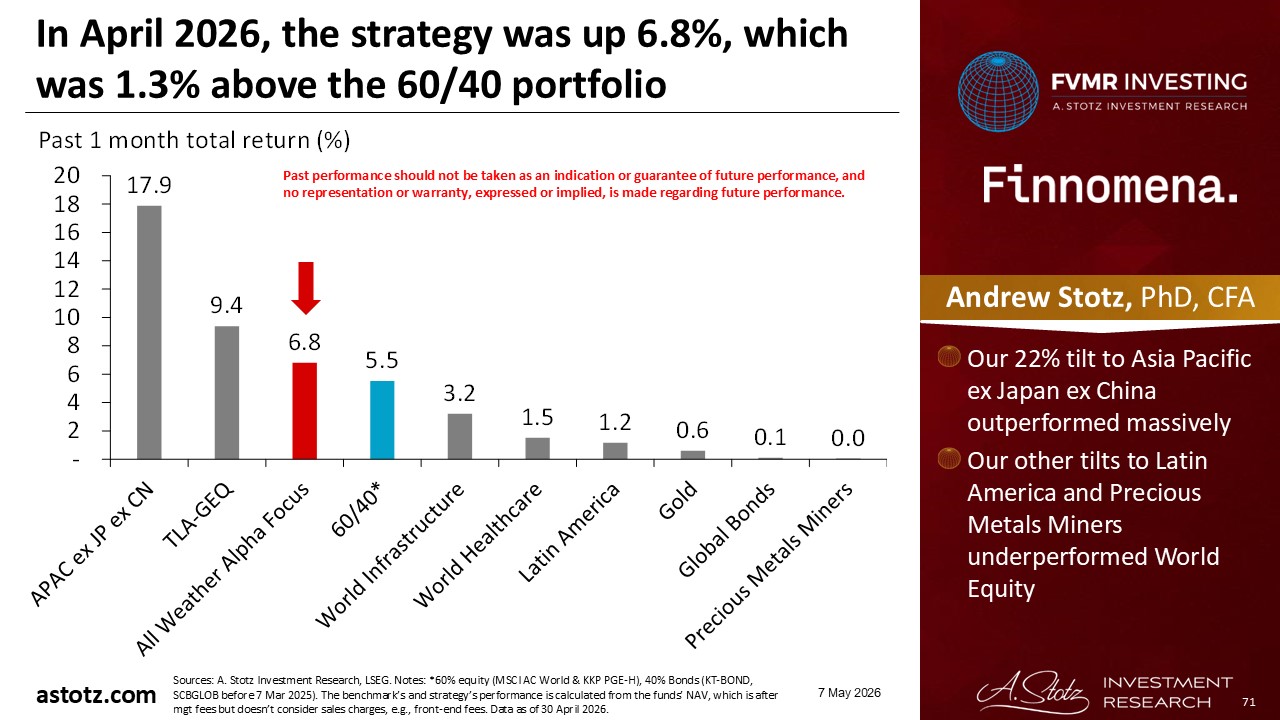

All Weather Alpha Focus gained 6.8%

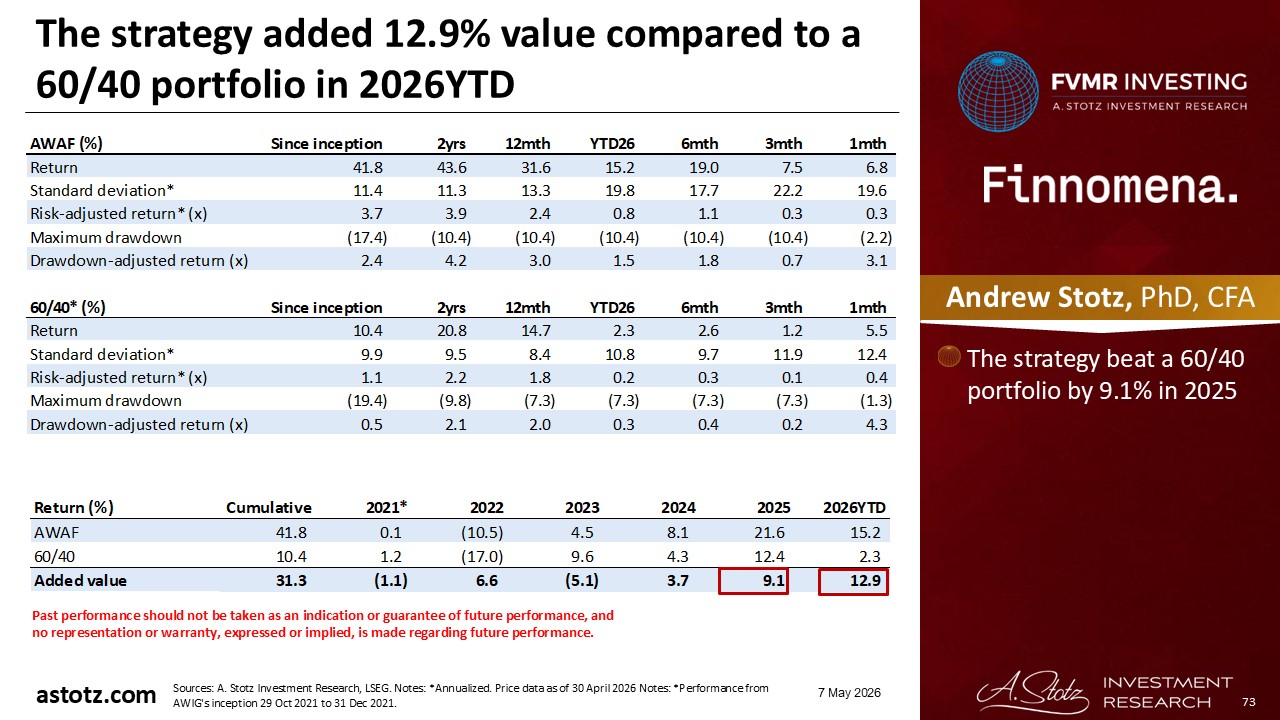

Since inception, the strategy was up 41.8% and 31.4% above a 60/40 portfolio

And 11.4% above World Equity, and with lower drawdown

In April 2026, the strategy was up 6.8%, which was 1.3% above the 60/40 portfolio

- Our 22% tilt to Asia Pacific ex Japan ex China outperformed massively

- Our other tilts to Latin America and Precious Metals Miners underperformed World Equity

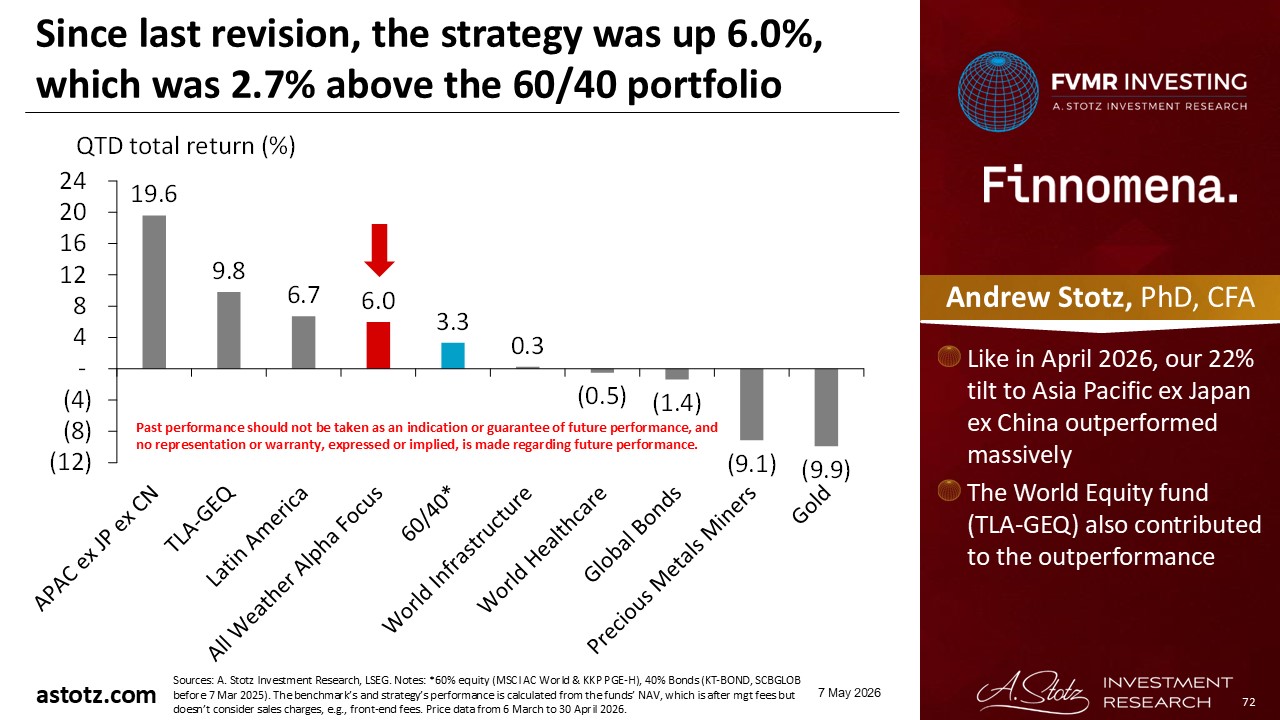

Since last revision, the strategy was down 6.0%, which was 2.7% above the 60/40 portfolio

- Like in April 2026, our 22% tilt to Asia Pacific ex Japan ex China outperformed massively

- The World Equity fund (TLA-GEQ) also contributed to the outperformance

The strategy has added 12.9% value compared to a 60/40 portfolio in 2026YTD

- The strategy beat a 60/40 portfolio by 9.1% in 2025

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.