Why Are Korean Stocks So Cheap?

My recent time in Korea refreshed my memories of the tenacity of the people and their desire to learn. I was also reminded of the immense societal pressure: from women and beauty to executives and work (and drinking!). This contrasts to Thailand, where there is more pressure to enjoy life, smile and be happy; but that’s the beauty of Asia, the contrasts.

Being a financial analyst at heart, I was searching for answers to questions, such as: Why has the Korean stock market been so cheap, for so long? Is this going to reverse (providing a great buying opportunity)? My short answer: Small changes are coming, but don’t expect the structure of society to change; and, like the Thai smile, expect the “Korea Discount” to remain for the near future.

The “Korea Discount” has been around for a long time

So first, does the “Korea Discount” actually still exist? Ferris et al. (2003) looked at the cost and benefits of Korean chaebols (family-controlled conglomerates) and concluded that “the costs associated with chaebol membership exceed its benefits” and highlighted three reasons. They: 1) pursued profit stability, rather than profit maximization; 2) they over-invested in low-performing industries; and 3) they cross-subsidized weaker members of their groups.

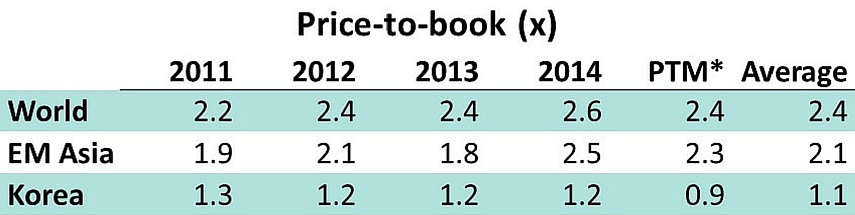

And it has still been around over the past five years

From our own bottom-up aggregation of on average 1,174 non-financial Korean companies from 2011 to 2015 we find that that the average price-to-book for Korean companies was 1.1x. This compares to Emerging Asia (from our bottom-up aggregation of on average 6,700 non-financial companies) which was trading at an average of 2.1x and the World (our bottom-up aggregation of on average 19,000 non-financial companies) on 2.4x. So, yes, the Korea Discount still exists. What is the cause?

Families make it cheap

So, why this discount? First, the corporate landscape in Korea is unique. At the top of the country’s economy are the large, family-controlled conglomerates, so called chaebols. A recent Bloomberg article by Jungah Lee showed that the revenues of the five largest chaebols; Samsung, Hyundai, SK, LG, and Lotte were equal to about half of Korea’s GDP. The chaebols are one major reason that the Korean economy has become what it is today, but in the recent years it seems to also have become the problem.

After the 1997 Crisis the chaebols improved themselves, a bit

The chaebols seem to have generated benefits for their shareholders due to certain advantages. In a 2010 paper Lee et al. showed that in the 1980-90’s the chaebols were mainly successful due to government support (e.g. tax breaks) while after the Asian financial crisis in 1997 they improved and became more efficient and profitable on their own. But Korea still lag far behind the world and Emerging Asia in terms of return on equity.

Below average return on equity driven by a low profit margin

But did they really improve themselves? Our research of the last five years showed that in seven out of ten industries, Korean company net profit margins were substantially below the global industry average. Worst performing industries were Industrials, Utilities and Energy. The average net profit margin in Korea over that time was 3.4% versus the world’s 5.3%. This net profit margin discount drove an ROE discount, both of which explain why Korean companies trade at a discounted valuation compared to the region and the world.

Coming from chaebols extracting profits?

Kim & Lee (2003) and Baek et al. (2004) found that the “Korea Discount” to some extent could be explained by poor corporate governance mainly in the chaebols. Baek et al. (2006) found evidence for tunneling within the chaebols (e.g. for intragroup deals they buy/sell companies at discount/premium to other group companies) and in that way the controlling shareholders in the chaebol get private benefits at the expense of other shareholders.

Pros and cons of chaebols: Preferential treatment, but long-term thinking

An article in The Economist on Feb 11, 2012 also talks about tunneling in terms of awarding contracts to companies within the chaebol. The author explained that the current situation with chaebols in Korea was like a double-edged sword. On the one hand, some at the top of the chaebols have been pardoned for various crimes in accordance with an old Korean adage “Yujeon mujwai, mujeon yujwai” meaning “money = innocence, no money = guilt”. On the other hand the chaebols’ long-term thinking is something that Western companies and investors could learn from, instead of their short-term thinking and focus on quarterly results.

Not cash hoarders, but carry less debt

One last explanation for the discount is that chaebols are hoarders of cash and Korean companies have historically lower dividend yield than in other countries. However, our research into this over the last five years shows that the current ratio of Korean companies was close to the world average, so no evidence of cash hoarding. What we do see is that the level of debt in Korean companies is slightly below the global average, which, combined with the lower net profit margin depresses ROE.

Can things change?

For the past couple of years the government has attempted to address the chaebol issue. It has even gone as far as a government crackdown on family members of chaebols and actually sent some to jail. At the end of 2014 the Korean government imposed a tax for companies holding excess cash, while it will give tax breaks for companies that spend on investments and employment. Samsung Electronics, Hyundai Motor Company and its sister company Kia Motors Corp. have, subsequently, increased their dividends.

A sustained improvement in net profit margin could drive a re-rating… if it happened!

If the Korean government could show that chaebols are not above the law, and the chaebols’ start to treat minority shareholders as equals then there might be a great opportunity in Korea. An improving net profit margin, if sustained could lead to a re-rating of the stocks.

Unfortunately, from our research we have yet to see this structural shift in the numbers. We are reminded of the contrasts in Asia, and how they are driven by the ways the various societies developed. Since the Korea Discount seems to be driven by the structure of society, more than a phase of development, we believe that it is likely to remain for the near future.

We keep an eye on the Korea Discount through our Korea Equity FVMR Snapshot. If you are interested in following it with us, just click here for your free snapshot.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.