What Type of Investor Are You? Active, Passive or DIY Investing?

You are your own worst enemy when it comes to investing. You can either decide to let someone else do it for you or create a solid investment framework to improve your chances of investment success.

What type of investor are you?

First and foremost, you need to ask yourself what kind of investor you are. Our CEO Andrew Stotz helps you with this in his book, How to Start Building Your Wealth Investing in the Stock Market by asking three questions. There is no “one size fits all” solution, but you’ll get a good idea about how to invest and where to focus by asking yourself; “Am I interested in picking stocks? Do I have time to pick stocks? Do I have the necessary knowledge to pick stocks?”

If you answer “yes” to all these questions, then you may choose to do-it-yourself and build your own stock portfolio. You may also choose not to do it alone, but try to identify a fund manager who aims to earn you above-market returns, after fees, due to his/her skill.

If you have little time, interest and/or knowledge, then keep it simple. Go for a passive, widely diversified index fund or ETF that aims to track the market return at the lowest fees possible.

Still curious about doing it yourself or going with an actively managed fund? First, learn that you are your own worst enemy.

You are your own worst enemy

There are a wealth of academic papers, books, articles, blog posts,—this could go on forever—already out there, about how behavioral biases and heuristics lead you to poor decision making, in investments and other areas of life. To give you the short version: you are your own worst enemy.

If you, like me, want some hard evidence to prove this argument, let’s have a look at some common behavioral shortcomings most of us (if not all) suffer from often.

You feel a loss two to two-and-a-half times stronger than an equal gain, and this makes you loss averse (Kahneman & Tversky, 1979). This aversion can be a problem as you don’t dare to invest due to the risk of losing money and, therefore, certainly will not gain anything from investing either. Loss aversion can also result in taking on more risk to avoid sure losses, e.g. by holding on to a stock that has fallen by 50% just to avoid realizing that loss.

Have you ever had a friend or financial advisor who claims, “I knew it all along” after an event has already happened? That’s called hindsight bias, and it leads you to believe that the world is more predictable than it really is, and can lead you to become overconfident in your abilities.

Overconfidence is a concern as it can impact your assessment of the quality of the information you have and your ability to act on that information. For example, 93% of American and 63% of Swedish drivers rate themselves an above average driver (Svensson, 1981).

Of course, these are impossible odds; over half of all drivers can not be better than the average. In the world of investing, overconfident traders hold undiversified portfolios and trade more, which leads to worse performance (Odean, 1998 and Barber & Odean, 2009).

I may sound overconfident saying this, but I believe you are overconfident. Admit this to yourself too; be humble, do your research, and acknowledge that you don’t know everything.

Do it yourself

If you feel that you might, in fact, be your own worst enemy that doesn’t necessarily mean that you can’t do it yourself. Remember that professional investors also suffer from behavioral biases too. A solid investment framework can help you deal with this; here are some basic principles of the framework we use successfully at A. Stotz Investment Research.

You’ll learn how to evaluate the attractiveness of a stock, how to reduce the risk in your portfolio, how to deal with both winning and losing stocks, and, ultimately, how to deal with yourself by avoiding acting emotionally when you’re investing.

Four elements of return

We call our framework “FVMR” and it stands for Fundamentals, Valuation, Momentum, and Risk. It’s the four different elements to look at when determining a stock’s attractiveness.

Fundamentals

A company’s profitability shows if it is managed well. Choose companies with high or rising profitability. Some financial ratios to look at here are return on assets, return on equity, asset turnover or operating profit margin.

Valuation

How the market perceives this stock. Look for good fundamentals at low prices, and consider a balance of valuation and fundamentals. A stock with great fundamentals might still be attractive at a higher valuation. A few common multiples to determine the valuation are price-to-earnings, price-to-book, and price-to-sales.

Momentum

Avoid “value traps” by looking for positive momentum in both price and earnings. Momentum in price examines if the share price has been going up over a certain period and positive momentum in earnings is if the company’s earnings have risen for some time. A strong price momentum tells you that the market is optimistic about the stock.

Risk

Opt for low business and price risk. Not every stock is going to fly, so, consider holding some that provide stable returns and strong dividends.

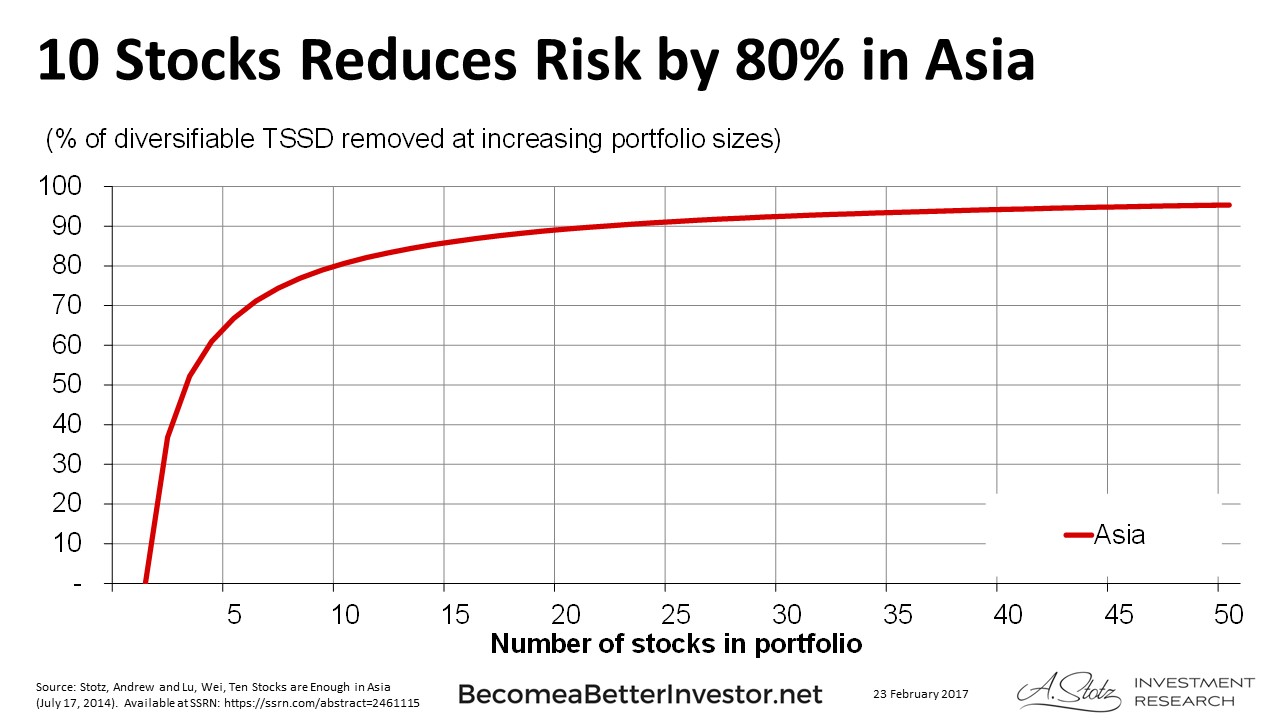

Hold a concentrated portfolio

Diversification is the necessary concept of reducing risk measured as volatility in your portfolio by holding a large number of stocks. A passive fund as an example will hold almost all stocks in the market and theoretically eliminate all company-specific risk.

Diversify and avoid taking unnecessarily high risk. Too much diversification though, reduces your chance of getting an above-market return which should be the goal for any active investor (otherwise, save time and effort; just buy a low-cost passive index fund).

In the paper Ten Stocks Are Enough in Asia, Stotz and Lu showed that by holding ten stocks in your portfolio instead of one, you reduce company-specific risk by 80%. A concentrated portfolio of ten stocks uses diversification to reduce risk but also increases the chance to outperform.

Manage risk by determining future actions

The investment guru Warren Buffet said: “Rule #1: Never lose money; Rule #2: Never forget Rule #1.” While it might be hard— or impossible even—to never lose money these words of wisdom tell us that a crucial part of investing is to manage your risk.

I would even go so far to say that managing your risk is more important than finding the absolute best stocks. The reason is quite simple; we know that stocks and markets crash now and then, if you can limit your losses when this happens, you have a larger chunk of wealth to accumulate returns on when it turns and goes up.

Stop loss is a simple, yet powerful, risk management tool. The benefit of a stop loss is that you predetermine future action. When you invest in a stock, you decide that if the price drops to a certain level, you will sell the stock.

The level of stop loss can vary with markets and investment strategies, but 20% is often enough, i.e. if the share price falls by 20% from your buying price, you’ll sell your holding; helping you preserve capital and protect yourself from your emotions.

Don’t forget to take profit

On the flipside, you also need to take profit on your winners. It’s not easy to know when the right time is to sell a winning stock. One method is to set a take profit point, like a reverse stop loss, so when the price has gone up to a certain level, you will sell it and lock in the profit.

This could though, result in losing future returns as you’re selling too early. So, another way is to regularly rebalance your portfolio. Let’s say you start with an equally-weighted ten stock portfolio, i.e. each stocks’ weight in your portfolio is 10%, and one stock’s price performs exceptionally well so that its weight become 15% of your total portfolio. When rebalancing, you would sell some of your shares until the stock’s weight is 10% again, and by that, locking in some of the profit too.

Whether you choose to go with passive index funds, actively managed funds or you choose to do it yourself, you need to first decide what is right for you. If you choose passive investing; focus on minimizing fees. Don’t pay an active fund manager more than his/her worth either and don’t pay your adviser or broker too much. Most importantly, you need to have an investment plan or framework in place, and stick to it.

This post was originally written for and published in ScandAsia Magazine.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.