Momentum Investing Explained Through Physics and a Hummer H2

Factor investing has started to win popularity lately. You can now find investment products that help you take advantage of the size or value premium, for example, benefitting from small caps generally outperforming large caps and value stocks generally beating growth stocks.

The value and size premiums are usually not very controversial, but momentum is one of the factors that many times leads to a discussion among investors. Let’s take a look at what momentum investing is, what evidence supports the momentum premium and how momentum can help you become a better investor.

Defining momentum investing

Momentum investing focuses on the fact that stocks tend to move in the same direction for some period of time. In contrast to the value oriented “buy low, sell high”, momentum investing is “buy high, sell higher” or if taking short positions “sell low, buy lower”.

Physics and a Hummer H2

I don’t know much about physics but do know that momentum is something talked about there and I remember it has to do with the weight and speed of an object. Luckily Wikipedia can always freshen up one’s mind. In physics, momentum equals mass multiplied by velocity; something heavy in high speed takes a longer time to reach that speed and it takes longer to slow down.

Think about a Hummer H2 (yes, I think that car is cool 😉 and even cooler if it could be a bit more climate friendly) going 100km/h versus a motorcycle running at 40km/h. Which of them reaches their speed first? Which will need the longest time and distance to stop? The Hummer will take a longer time to reach 100km/h and will certainly take longer to stop. Hence, it will have higher momentum.

When momentum investing you want to find the Hummer that has just started to accelerate.

Evidence from the academia

Jagadeesh and Titman (1993) found evidence that momentum worked for US-listed stocks from 1965 to 1989. They found “that strategies which buy stocks that have performed well in the past and sell stocks that have performed poorly in the past generate significant positive returns over 3- to 12-month holding periods”.

Carhart (1997) expanded the Fama-French three-factor model to include a fourth factor—momentum. Carhart found significant outperformance by “buying last year’s top-decile mutual funds and selling last year’s bottom-decile funds”. Later Fama and French (2012) found evidence for momentum returns in North America, Europe and Asia-Pacific (but not Japan).

These are just a few selected papers on momentum. There are a lot more and there is also research that questions whether momentum investing really works. From my own studies, I think it’s fair to say that there is enough evidence to support the idea that you can make good money from momentum investing; but it also creates additional risk.

Risks with momentum investing

Momentum investing in general leads to higher turnover, i.e. you’ll buy and sell more often compared to many other strategies like value investing. A high turnover will increase your trading costs which lower your return; and in some countries your taxes will increase as your holding period in certain stocks may be short.

Another risk is that it’s very hard to predict when momentum ends. If not cautious it can be like driving that Hummer H2 at 100km/h blindfolded. As long as the road is straight and there are no hurdles in your way everything will go fine. But as soon as the road turns or a car driving at a slower speed comes up in front of you, then you’ll be in trouble and it’s very likely to be painful.

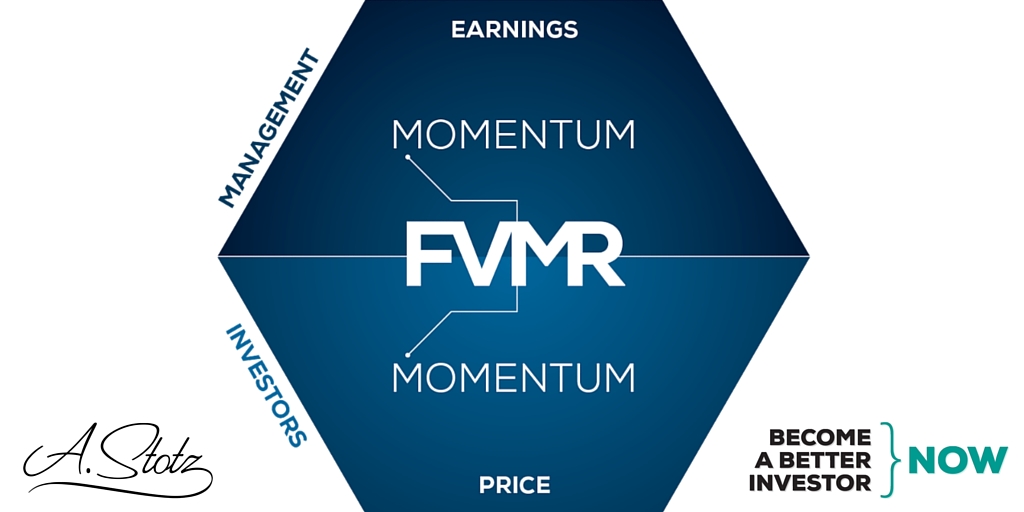

How we use momentum when selecting stocks

When selecting stocks for our portfolios at A. Stotz Investment Research we use our FVMR framework considering four elements; Fundamentals, Valuation, Momentum, and Risk. When considering momentum, we look at both price momentum and momentum in earnings.

This is a way to avoid value traps, i.e. a stock that looks cheap and attractive but will not turn, and instead continues to deteriorate. If you instead find a cheap stock where you can see momentum in price and/or earnings it’s less likely to be a value trap and could potentially become a really good investment.

Low price momentum can give you a signal that a specific investment is out of favor, i.e. that for some reason the market doesn’t find the stock attractive. Some may say this is an opportunity, and it could be; but if the stock won’t move for a long period of time your capital might yield you better returns elsewhere.

At times, you can also find companies where you see momentum in earnings, but the price hasn’t started to move just yet. This could indicate that you’ve found yourself a turnaround case and that you’ve found it before the crowd. Momentum in earnings is, in general, a good indicator as it shows that the business is profitable and growing.

Don’t drive a Hummer blindfolded

Today, there are various financial products that are based on factor investing and can, for example, give you exposure to only momentum stocks. As always with investing I think it’s important to diversify and have a balanced view. Hence, I’d avoid going full throttle on only momentum.

I do however believe it’s a factor you should be aware of and consider, regardless of your investment style. It can enhance your returns by helping you to identify “hot stocks” as well as avoiding “value traps”.

Don’t drive your Hummer H2 blindfolded. Know that there is more to the car than just its weight and speed; but do also acknowledge that its heavy weight at high speed will be harder to slow down than a light-weight motorcycle.

Do you consider momentum when #investing in #stocks?

— Alexander Wetterling (@BkkBanker) May 6, 2016

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.