Business Managers and Owners should Look for Profitable Growth

Profitable Growth is what matters

In April I blogged about EPS Growth, and followed this with a post about profitability (Replace “E” with “A” to Truly Understand Business Profitability). Today, I focus on a combination of these profitability and growth measures, which I call “Profitable Growth”.

Profitability: It’s about how Much Profit can be Generated from Assets

If a company can generate a good net profit relative to the assets it invests in, its return on assets (ROA) is strong. ROA is a measurement that matches the way a manager thinks about business, asking questions like “What assets do I need (think factories, offices, computers, and employees)? What profit will I generate in return?” The decision of how to pay for those assets, whether using debt or equity, is almost irrelevant when it comes to creating long-term value. Hence, I rarely look at the common measure, return on equity. ROA’s major weakness is that it is industry specific, meaning that an asset-intensive utility company cannot be compared to an asset-light software company, but for those with access to data, this should not be a problem.

Growth: Earnings Growth is the Ultimate Proof of Competence

Whether managing a business or investing in one, it is critical to also focus on earnings-per-share (EPS) growth. This one measure tells almost the whole story of a business. EPS growth starts with sales growth, which I call “proof of concept”, that is proof that the market wants your product. Think of Nokia Corporation versus Apple, Inc. 20 years ago against how they are today – their roles have reversed.

However, sales growth is only the half of it. A successful management team also controls costs to earn a strong net profit margin and generate EPS growth, consistent EPS growth I call “proof of competence”. This is proof that management can go beyond product development and sales. Finally, investors should prefer companies that do not dilute this growth through issuing new shares.

It’s all Relative: How you Perform Relative to your Peers is what Really Matters

In recent talks with one company’s management team they told me with pride about how they had improved their net profit margin to 5% in the current year from the previous year’s 3%. Seemed good, but they complained that their share price didn’t rise, and later said that the stock market did not understand their business. Upon further investigation, I found that over the same period, the company’s sector peers had moved to 7% from 4%, a higher absolute level of profitability, as well as a larger increase. When I brought this to their attention, the management team told me that they don’t compare their performance to the overall sector; rather, they focus on beating their direct competitor, which in this case, they did.

Investors See your Company as just One in Thousands of Investment Options

Though it is tempting to focus on beating a direct competitor, the reality of today’s globalized stock markets is that investors have so many excellent choices that today they’ll compare your company to all the other companies that they could invest in. I can prove that, but before I do, let me explain the way I rank companies.

One Step in my Investment Process is to Rank the Company

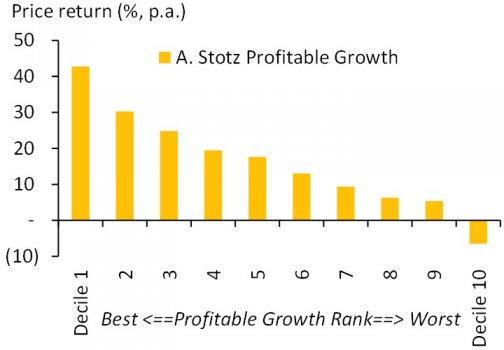

One of the steps I take as an investor is to rank a company’s Profitable Growth relative to its global sector peers. This allows me to understand the true relative financial performance of the company. I use a scale of 1 to 10 (1 being best) and find that when picking stocks, finding a company that is ranked around 5 and rising provides the best chance to make money investing in the company. Of course, when I talk to company management, I advise them to be in the top three deciles. This is easy to say but hard to do… and even harder to maintain.

I can Prove that Profitable Growth matters for Share Price

The chart below shows the coincident share price performance of companies that are ranked in various deciles when compared to their peers on my combined Profitable Growth ranking. I looked at this data across listed companies in Asia (though I also look at a company’s global rank). In this case, I don’t even take into account the industry that the company is in. What it shows is that a strong ranking produces strong share price performance, and a poor ranking produces poor share price performance… simple as that.

Annual return of a portfolio holding companies ranked on Profitable Growth.

What do you think about Profitable Growth? Makes sense to you as an investor? I would love to hear your thoughts! Any comments or question you might have, I would like to know. Is anything unclear? Please let me know in a comment below.

If you enjoyed this article, feel free to share it with your friends.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.

Originally published on July 23, 2015 at: www.equities.com.