A. Stotz All Weather Strategies – August 2022

Executive summary

- The market expects Fed and the ECB to hike aggressively, even if it causes a recession.

- Europe’s energy crisis is far from over.

- Global inflation hits poorer nations the worst.

- Slowdown concerns for China as well.

- Central bankers appear to be raising rates into a recession to stifle inflation, stagflation would be the worst outcome.

- Demand for necessities (food and energy), inflation, and supply-chain disruptions are going to drive Commodities higher.

- Bonds and Gold to protect capital.

The All Weather Strategy is available in Thailand through FINNOMENA. If you’re interested in our allocation strategy, you can also join the Become a Better Investor Community. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

What happened in world markets in August 2022

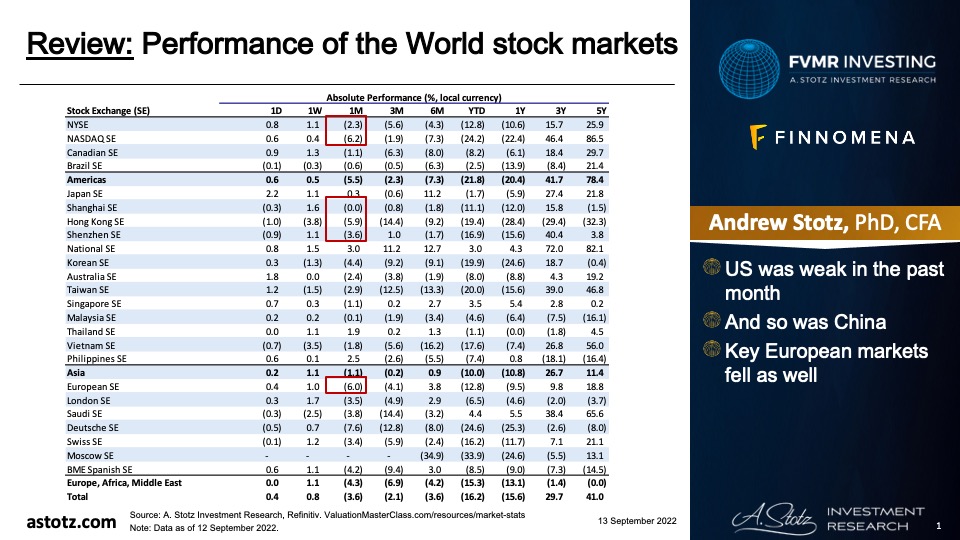

Performance of the World stock markets

- US was weak in the past month

- And so was China

- Key European markets fell as well

Find the updated Performance of the World stock markets here.

The market has begun to expect the Fed to hike faster and higher

“War is inflationary.” Credit Suisse’s Pozsar says traders underestimate the pain needed to get inflation under control. He sees a risk that the Fed will raise benchmark US rates to 5-6% to reduce demand enough to match structurally constrained supply. https://t.co/LHRyFWToZ7

— Lisa Abramowicz (@lisaabramowicz1) August 2, 2022

The reaction to JPow’s speech at the Jackson Hole Economic Symposium

No one:

Jerome Powell today: pic.twitter.com/D6BZByV07p

— Wall Street Memes (@wallstmemes) August 26, 2022

The EU redistributes to the troubled member states

The #ECB‘s ‘game’ is pretty obvious! pic.twitter.com/f9L2HBXNHd

— jeroen blokland (@jsblokland) August 8, 2022

Investors are pessimistic about Europe

🇪🇺 Investors increase bets against #euro – FT

*Net short positions hit their highest levels since the start of the pandemic

*Link: https://t.co/L0cInFilaf pic.twitter.com/lMz3DdnaqQ— Christophe Barraud🛢🐳 (@C_Barraud) August 29, 2022

The Germans seem to prepare for the worst

Google Searches for ”firewood” in Germany. pic.twitter.com/ECVVHtxDXJ

— Alf (@MacroAlf) August 13, 2022

Only a few may have enough to pay their bills this winter

I’ve already put some money aside to cover my electricity bill here in Germany. pic.twitter.com/Vcgs5k624h

— Marc-André Fongern (@Fongern_FX) August 30, 2022

German producer price index (PPI) overshot already high expectations

German PPI. And the @ECB is running zero rates.

Via @SoberLook pic.twitter.com/LTR7jRI9WF— Sven Henrich (@NorthmanTrader) August 24, 2022

German CPI saw new records as well

To put things into perspective: Supermarket prices in #Germany are rising at a record pace. Food CPI jumped 16.6% YoY in August, the highest food price #inflation since the start of the statistic. pic.twitter.com/fNmSxRg5g1

— Holger Zschaepitz (@Schuldensuehner) August 30, 2022

To be fair, power prices seem to be coming down in Germany

German 1y ahead Power Price has almost halved within 2 days from €1,050 per MWh to €545 today. This raises the question of who is operating in the electricity market. Is it pure speculation? Are these meaningful prices that reflect real scarcities? pic.twitter.com/1OyzB6uVZR

— Holger Zschaepitz (@Schuldensuehner) August 31, 2022

- Though 1 year ago, the price was less than €100 per MWh

France’s energy crisis is worse

Right about every FinTwit energy pundit and mainstream media report that Germany is THE energy problem child

France is in much deeper shit on the electricity front than Germany..

The German energy crisis is probably overreported and even slightly exagerated by now imho .. pic.twitter.com/1iTrZ93zcX

— AndreasStenoLarsen (@AndreasSteno) August 14, 2022

The French gov’t prepare its people for a tough winter

🇫🇷 FRENCH FINANCE MINISTER BRUNO LE MAIRE SAYS WE NEED TO PREPARE FOR HARD WINTER WITH LESS GAS AVAILABLE AND NEED TO THINK ABOUT RATIONING OF GAS TO INDUSTRY – RTRS

— Christophe Barraud🛢🐳 (@C_Barraud) August 30, 2022

OPEC+ continues to miss production targets, not helping on the supply side

Woozer#OPEC+ missed output targets by 2.9 million barrels per day in July

Compliance with the production targets stood at 546% in July vs 320% in Junehttps://t.co/TWB5dbtltV

— Tracy (𝒞𝒽𝒾 ) (@chigrl) August 22, 2022

High gas prices could hit farm yields

European fertilizer giant Yara International says that record gas prices are forcing it to cut its European ammonia capacity utilization to about 35% https://t.co/ZHBqVUozsi

— Bloomberg Energy (@BloombergNRG) August 25, 2022

Higher prices hit poorer countries the worst

BREAKING: Protests break out in Lahore, Pakistan.

People took to the streets after receiving huge utility bills despite 12-16 hour daily black out 🚨 pic.twitter.com/coQU6Y7ozD

— Wall Street Silver (@WallStreetSilv) August 23, 2022

BREAKING: Nationwide strike and protests in South Africa against rising cost of living, power cuts and mass unemployment which is at 34% #NationalShutdown 🚨

— Wall Street Silver (@WallStreetSilv) August 25, 2022

Thousands of protesters break through a police squadron in Bangladesh. Rising cost of living and power cuts continue for third day in a row 🚨 🚨🚨

🔊sound pic.twitter.com/bd3LEdhrSr

— Wall Street Silver (@WallStreetSilv) August 25, 2022

Voices of concern about China

The government has agreed to pay up to $15,000 dollars for lost deposits, but only if the banks weren’t involved in “non-compliant” transactions.

The government’s strategy for overleveraged properties is to lend more money to finish them and pretend that everything is fine. pic.twitter.com/oFfJcg3a5d

— Graham Stephan (@GrahamStephan) August 17, 2022

Key takeaways

- The market expects Fed and the ECB to hike aggressively, even if it causes a recession.

- Europe’s energy crisis is far from over.

- Global inflation hits poorer nations the worst.

- Slowdown concerns for China as well.

- Performance review: All Weather Inflation Guard.

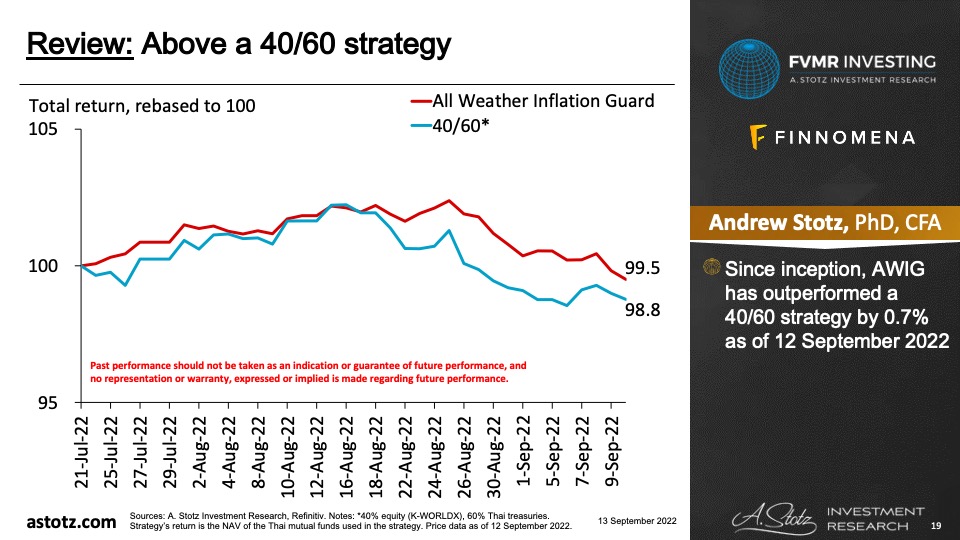

Performance review: All Weather Inflation Guard

Good start for All Weather Inflation Guard

- Since inception, AWIG has outperformed a 40/60 strategy by 0.7% as of 12 September 2022.

Inflation Guard was down slightly

- The strategy was 0.7% better than the 40/60 portfolio.

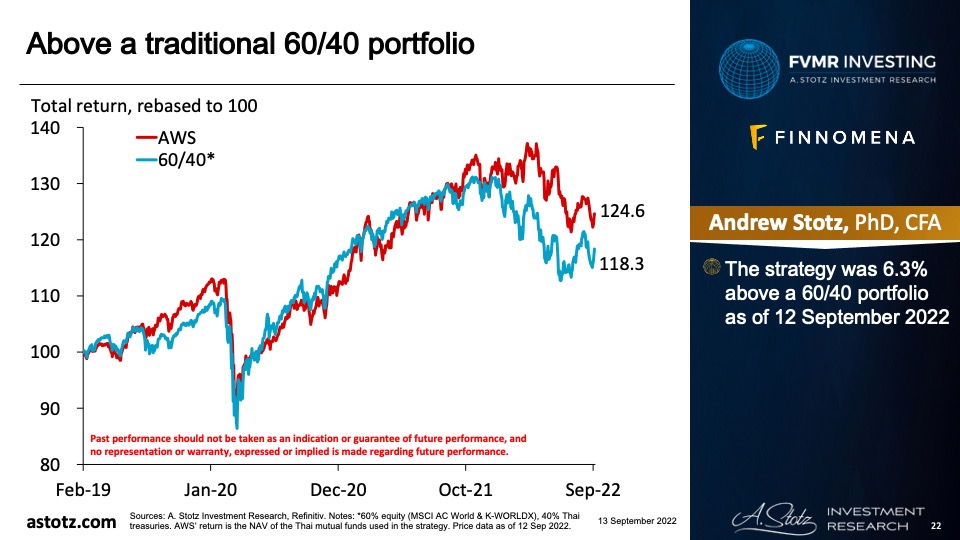

Performance review: All Weather Strategy

Above a traditional 60/40 portfolio.

- The strategy was 6.3% above a 60/40 portfolio as of 12 September 2022.

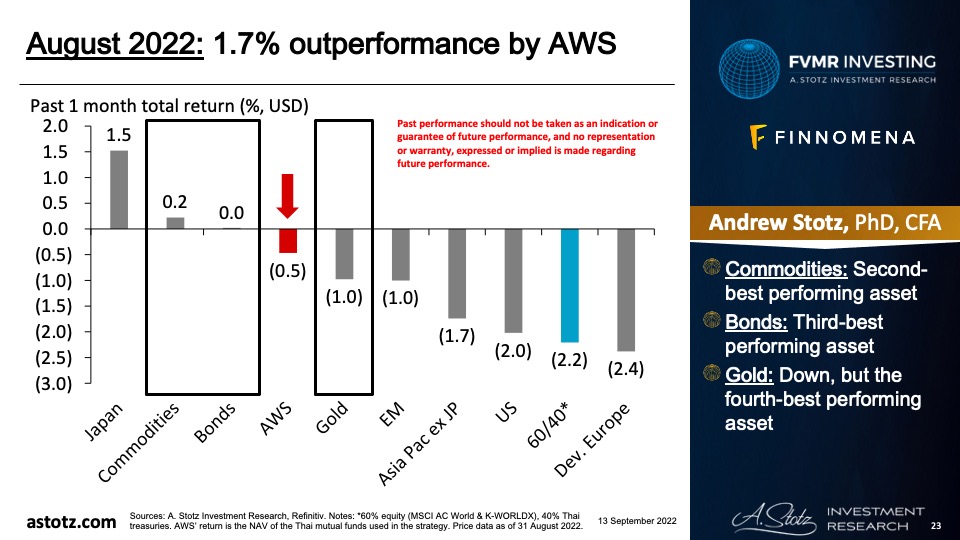

1.7% outperformance by AWS

- Commodities: Second-best performing asset.

- Bonds: Third-best performing asset.

- Gold: Down, but the fourth-best performing asset.

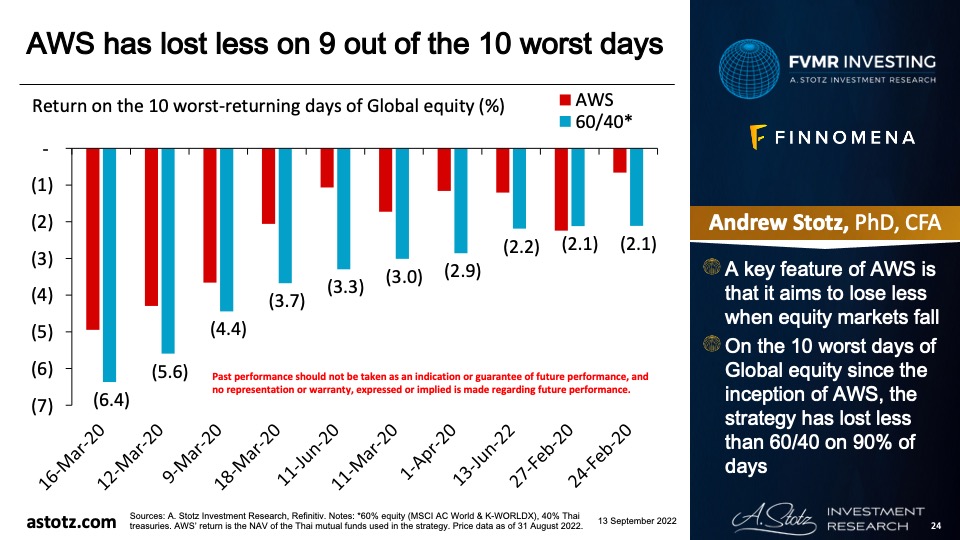

AWS has lost less on 9 out of the 10 worst days

- A key feature of AWS is that it aims to lose less when equity markets fall.

- On the 10 worst days of Global equity since the inception of AWS, the strategy has lost less than 60/40 on 90% of days.

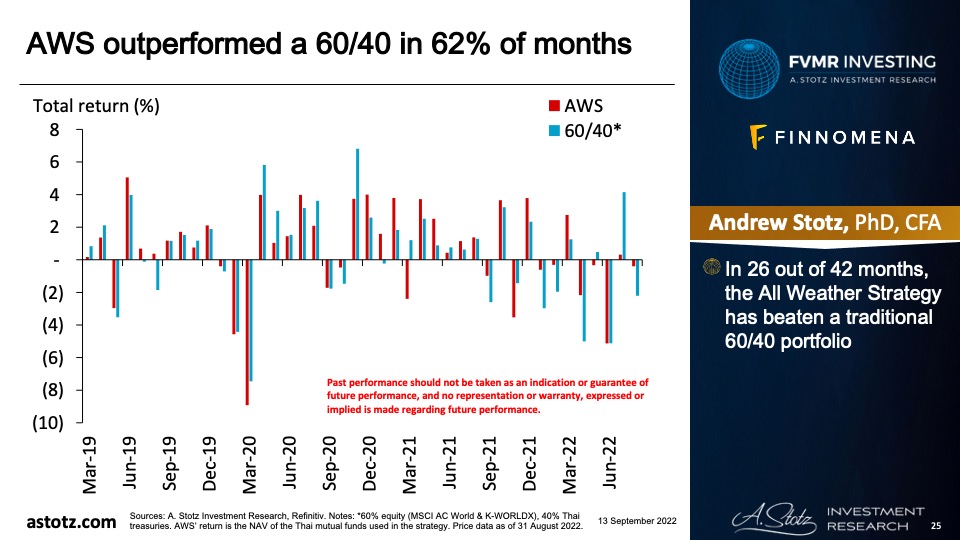

AWS outperformed a 60/40 in 62% of months

- In 26 out of 42 months, the All Weather Strategy has beaten a traditional 60/40 portfolio.

Performance review: All Weather Alpha Focus

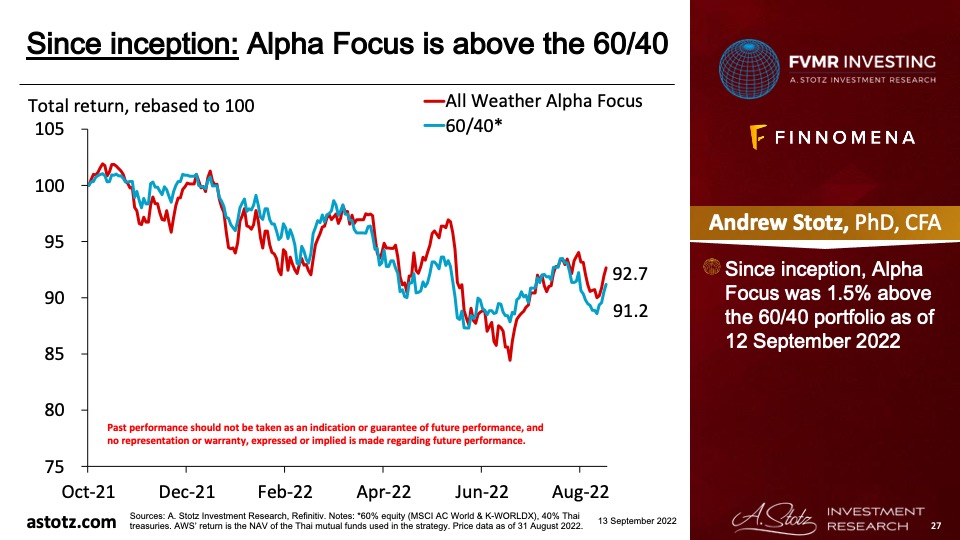

Alpha Focus is above the 60/40

- Since inception, Alpha Focus was 1.5% above the 60/40 portfolio as of 12 September 2022.

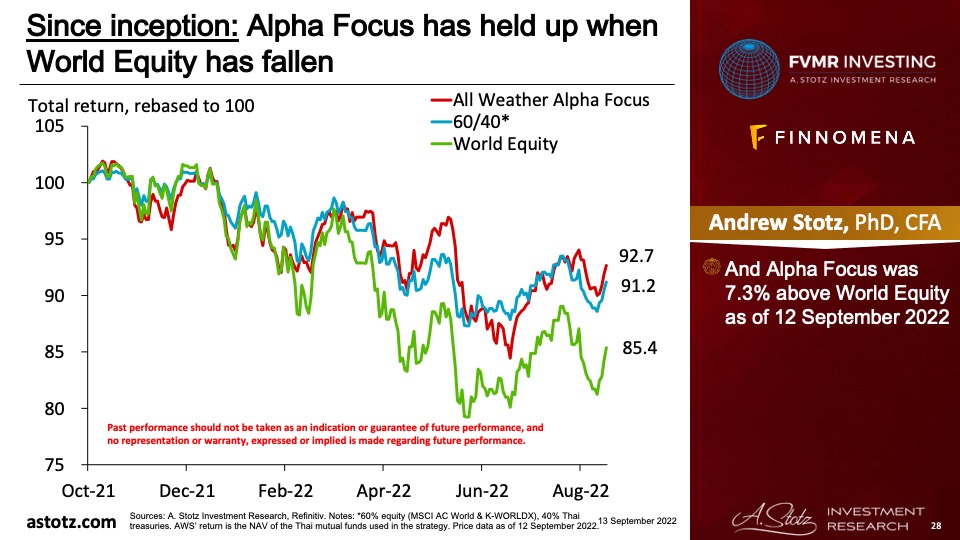

Alpha Focus has held up when World Equity has fallen

- And Alpha Focus was 7.3% above World Equity as of 12 September 2022.

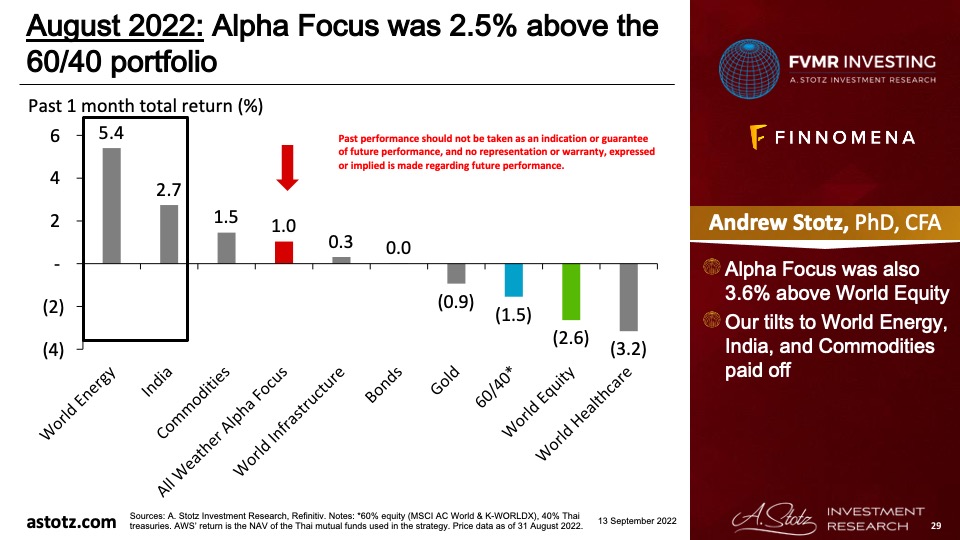

Alpha Focus was 2.5% above the 60/40 portfolio

- Alpha Focus was also 3.6% above World Equity.

- Our tilts to World Energy, India, and Commodities paid off.

Global outlook that guides our asset allocation

JPow seems ready to bring on the pain

- “While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses.”

- “These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

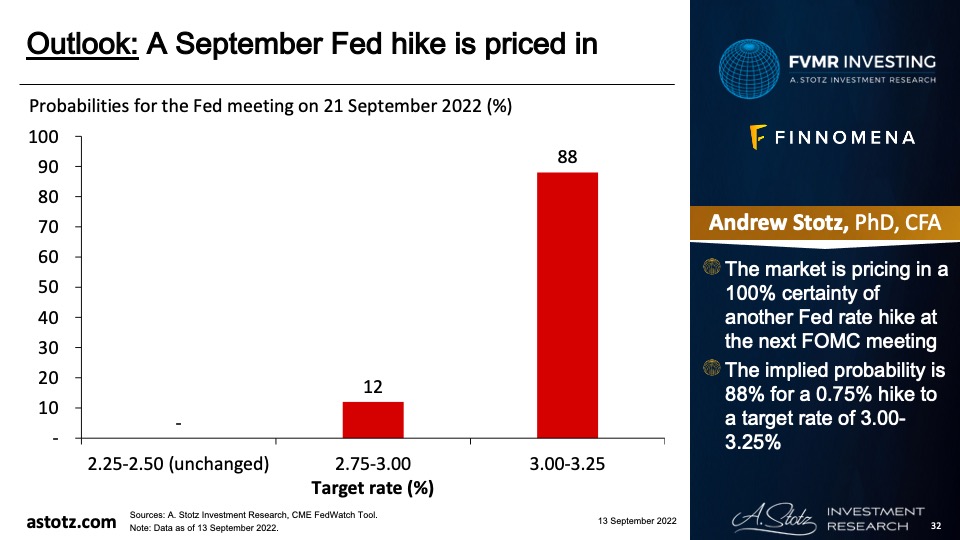

A September Fed hike is priced in

- The market is pricing in a 100% certainty of another Fed rate hike at the next FOMC meeting.

- The implied probability is 88% for a 0.75% hike to a target rate of 3.00-3.25%.

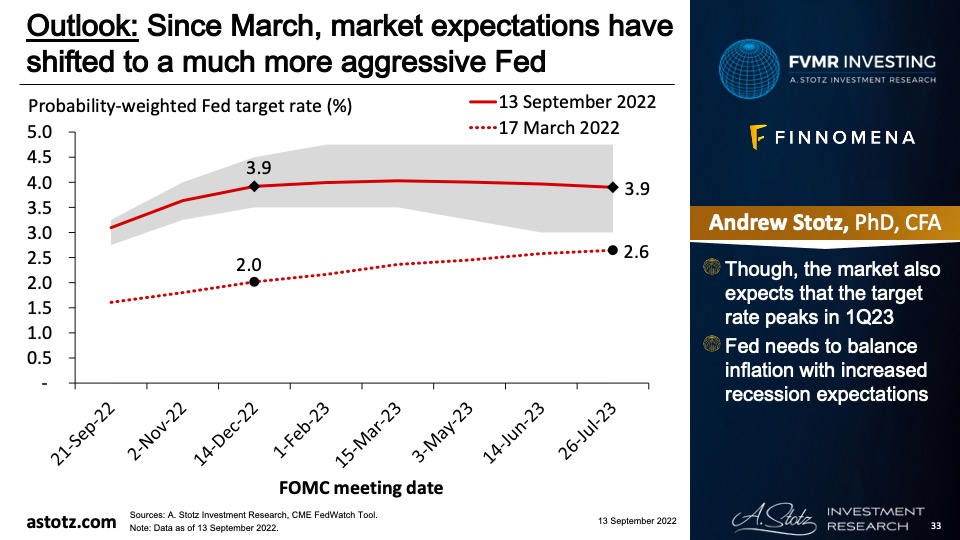

Since March, market expectations have shifted to a much more aggressive Fed

- Though, the market also expects that the target rate peaks in 1Q23.

- Fed needs to balance inflation with increased recession expectations.

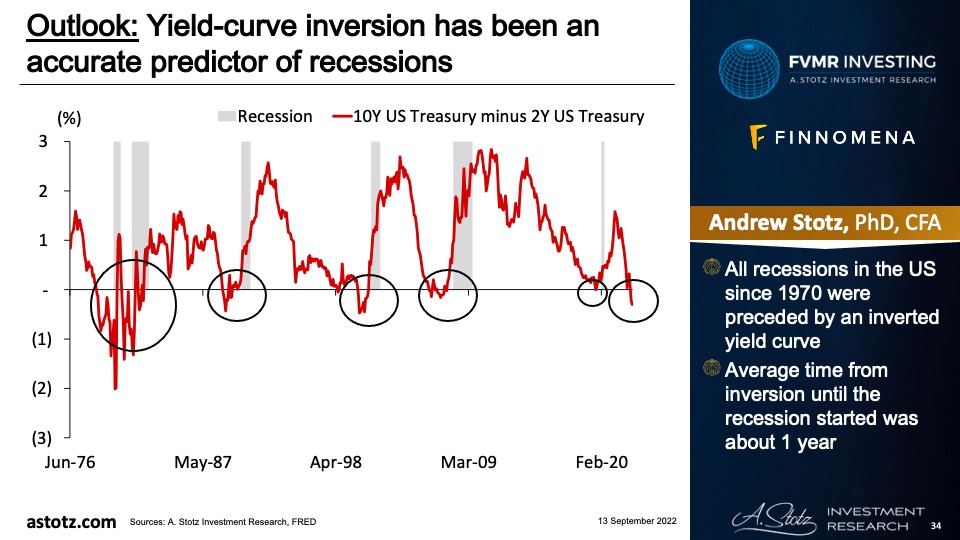

Yield-curve inversion has been an accurate predictor of recessions

- All recessions in the US since 1970 were preceded by an inverted yield curve.

- Average time from inversion until the recession started was about 1 year.

ECB follows the Fed

- The hike in July brought the key rate to zero, compared to zero since 2014.

- Like the Fed, ECB reiterates its commitment to combat inflation.

- 0.75% hike at the September 8th meeting, and further hikes are expected in October.

- ECB needs to at least keep up with the Fed in terms of hikes, if not, the Euro would weaken further and exacerbate the trade deficit.

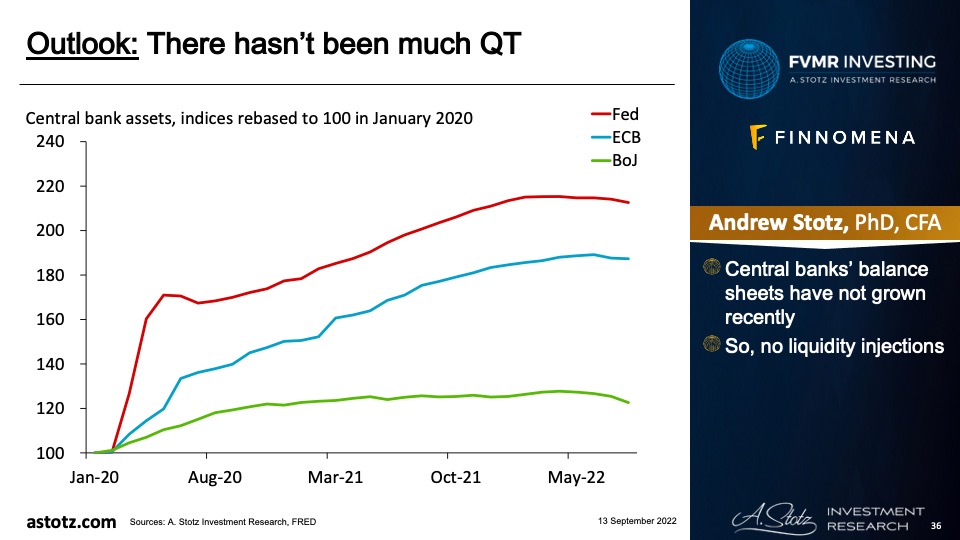

There hasn’t been much QT

- Central banks’ balance sheets have not grown recently.

- So, no liquidity injections.

We think the course will eventually be reversed

- Many central banks are communicating that they’re going to get inflation down, and investors seem to buy the rhetoric.

- We still think central bankers and politicians will change course and return to accommodative policies as soon as something “breaks”.

- Though many indicators look negative for stocks, we see opportunities to allocate to specific sectors and markets within equity.

Stagflation is the worst possible outcome

- If central banks manage to kill growth but not inflation, we’ll get stagflation.

- Stagflation is typically bad for both stocks and bonds.

- Commodities have typically done well during inflationary times, and gold has historically fared well during stagflation.

- Given the various possible outcomes, we like to be diversified across asset classes.

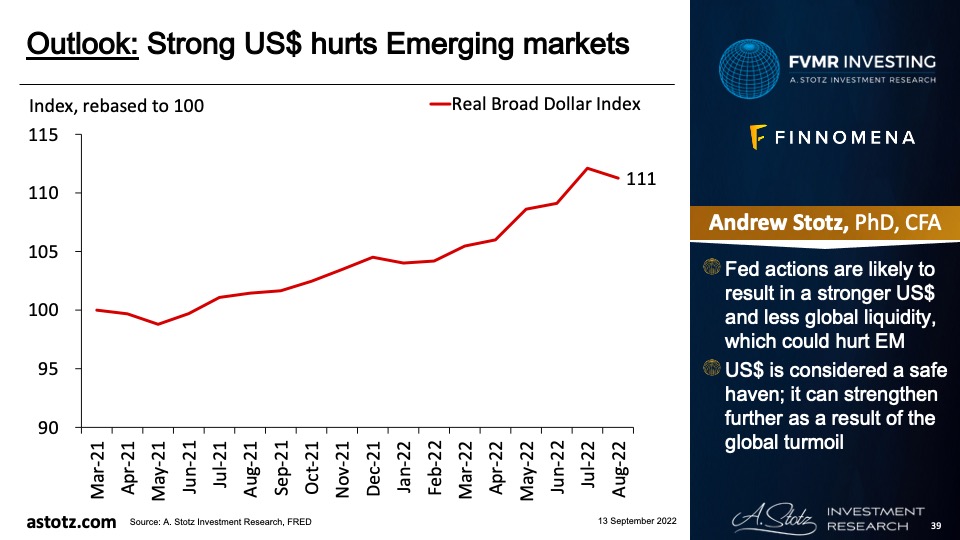

Strong US$ hurts Emerging markets

- Fed actions are likely to result in a stronger US$ and less global liquidity, which could hurt EM.

- US$ is considered a safe haven; it can strengthen further as a result of the global turmoil.

Poorer emerging markets and Asia could be hurt by the European energy crisis

Europe is so desperate for natural gas that it’s importing an LNG cargo from Australia (!!)

🇬🇧 🚢 🇦🇺🚢 LNG from Australia was re-loaded in Malaysia and is now going to UK

😮 Australia has never shipped LNG to Europe in Bloomberg data going back to 2016https://t.co/E5dmjmNYXD pic.twitter.com/SheUi93X1A— Stephen Stapczynski (@SStapczynski) August 16, 2022

- As Europe is desperately trying to find enough energy, prices keep rising.

- Richer countries are likely to outbid poorer countries for energy.

- Hurting poorer countries’ energy supplies.

Strong US$ and China are concerns

- A stronger US$ is negative for many Asian markets due to US$ denominated debt getting harder to pay back.

- We’re not yet convinced about the Chinese recovery.

- The Chinese gov’t is trying to support the economy but appears cautious to not use too much stimulus.

Bonds are typically a safe place to be

- In recessions, safer assets like gov’t bonds are typically performing well.

- Though with high inflation, low yields could still lead to negative real returns.

- We typically don’t allocate to Bonds to speculate in the upside, but rather use it as a way to protect capital over time.

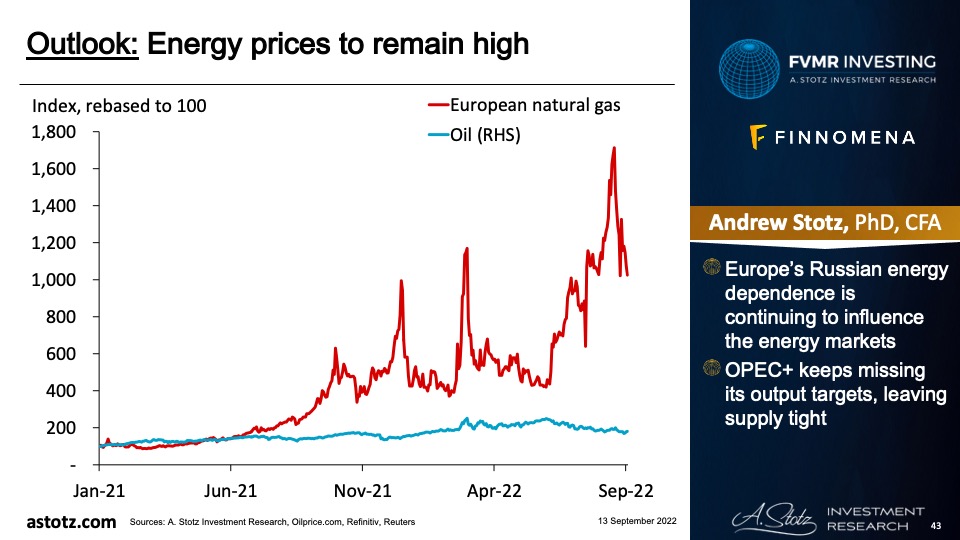

Energy prices to remain high

- Europe’s Russian energy dependence is continuing to influence the energy markets.

- OPEC+ keeps missing its output targets, leaving supply tight.

Fundamental support for energy prices

- Ukraine war could lead to further supply shocks.

- Energy prices can also remain high due to past underinvestment in new projects.

- A re-opening of China could lead to increased demand for commodities.

High energy prices feed through to food; cereals fell back in July and August

- Natural gas is used in fertilizer; pricier fertilizer mean higher grain prices.

- One of the world’s largest fertilizer producers have cut production by 50%.

- Corn is common feed of livestock and poultry, driving up meat prices.

World food price index hit a record 160 in March 2022, still at 138 in August 2022

- Export bans on food could exacerbate food shortages and push prices further.

- Oils and Cereals drove down the index in July, falling 19% and 11%, respectively.

- Oils dropped the most in August as well.

Commodities set to go higher

- “Global supply chains work only in peacetime, but not when the world is at war…” – Zoltan Pozsar.

- Demand for necessities (food and energy), inflation, and supply-chain disruptions related and unrelated to the war in Ukraine are going to drive the asset class higher.

- Also if we were to go into a stagflationary period, Commodities could show resilient.

We keep gold as an insurance

- The war in Ukraine spurs uncertainty, and inflation expectations could rise, making gold attractive.

- Though expected rate hikes and recession concerns are negative.

Key takeaways

- Central bankers appear to be raising rates into a recession to stifle inflation, stagflation would be the worst outcome.

- Demand for necessities (food and energy), inflation, and supply-chain disruptions are going to drive Commodities higher.

- Bonds and Gold to protect capital.

Risks

Global recession pushing down stocks

- If central banks are too aggressive with rate hikes and QT, it could crash stock markets and hurt our equity position.

- We are mainly exposed to Thai bonds, hence, the bond performance is most sensitive to BOT’s actions.

Inflation quickly gets under control

- We are positioned to benefit from rising inflation through our Commodities allocation.

- Weak Chinese economy could reduce commodities demand; leads to lower prices.

- Other commodities could fall with energy prices too, as it’s part of the production cost.

Global recession pushing down stocks

- If major central banks would surprise and be too aggressive with rate hikes and QT, it could crash the stock markets.

- Increased risk appetite could lead to defensive positions in World Healthcare and Infrastructure underperforming.

- A change in expectations towards lower inflation and interest rates could lead to poor performance of Gold.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.