Years of Earnings Underperformance Lead to Singaporean ‘Sell’

Watch the video with Andrew Stotz or read Watching the Street: Singapore below

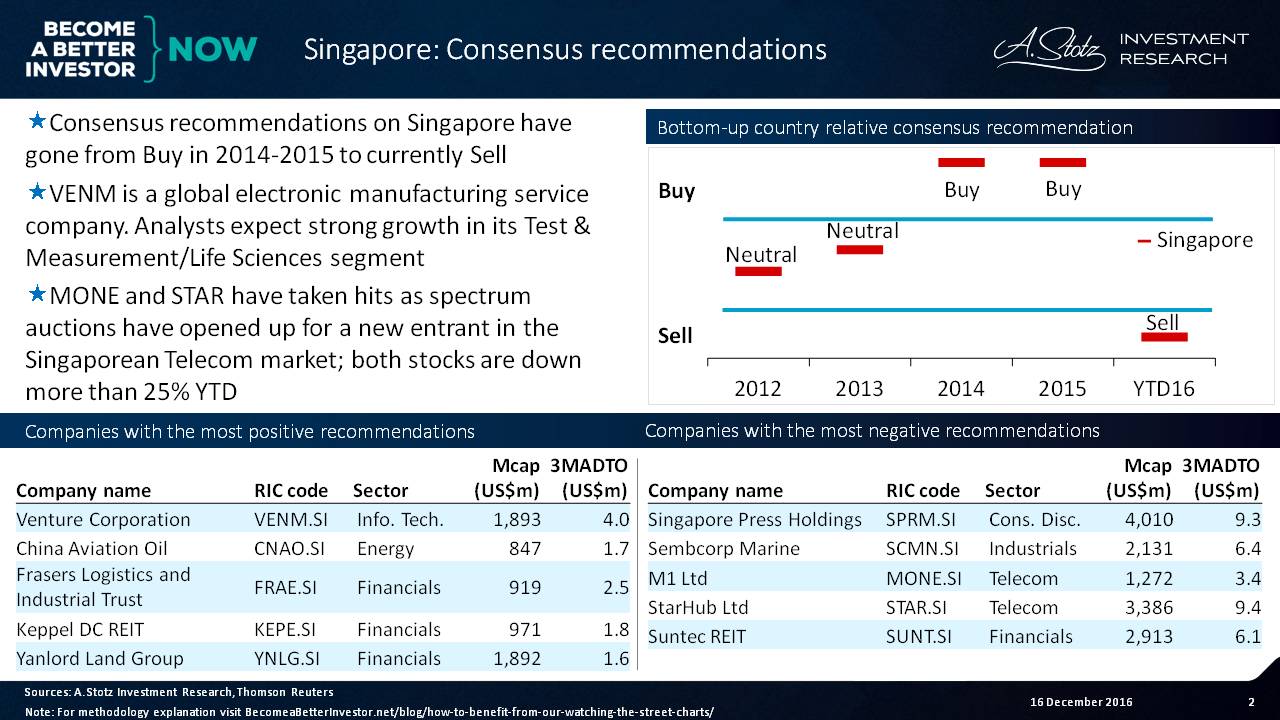

Consensus Recommendations: Singapore

Consensus recommendations on Singapore have gone from a “buy” rating in 2014 and 2015 to a hard “sell” rating in 2016. This may be a consequence of falling earnings results during the last few years.

Learn more: How to Benefit from Our Watching the Street Charts

Among companies with the most positive recommendations, Venture Corporation is a global electronic manufacturing service company. Analysts expect strong growth in its Test & Measurement/Life Sciences segment.

Among companies with the most negative recommendations, M1 and StarHub are two telecoms that have taken a hit as spectrum auctions have opened up for a new entrant in the Singaporean telecom market. Both stocks are down more than 25% YTD.

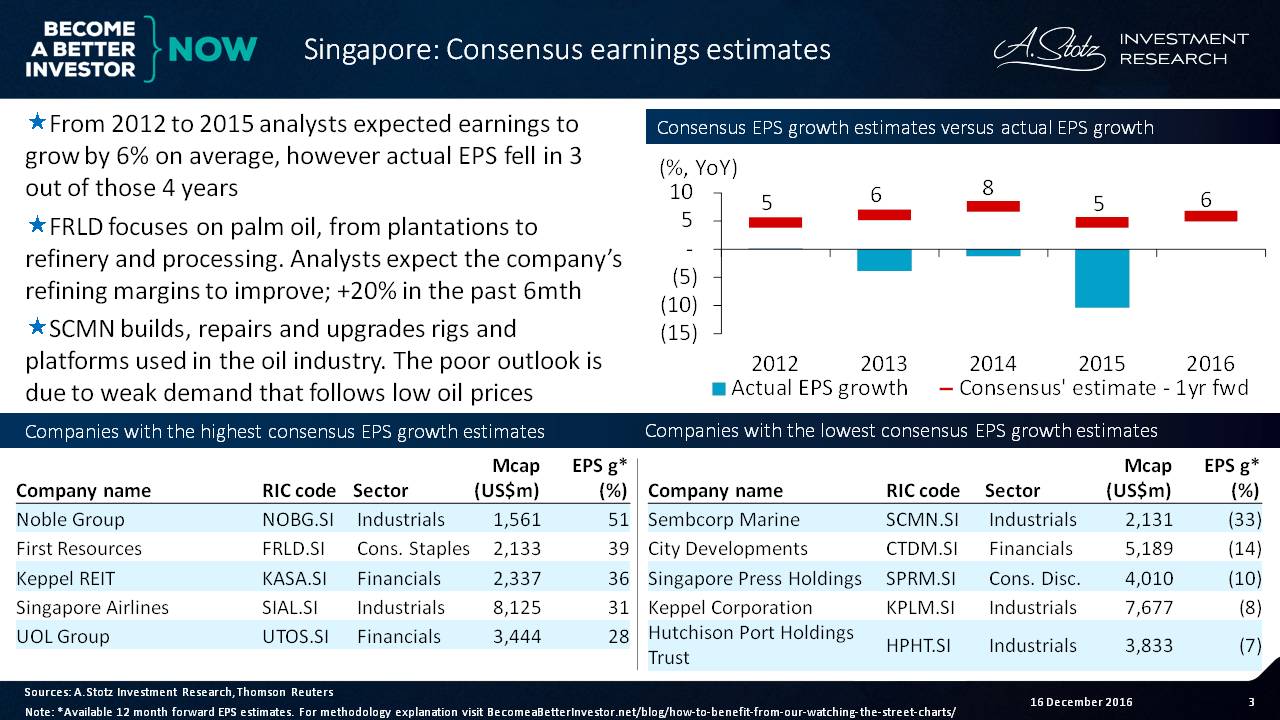

Consensus Earnings Estimates: Singapore

From 2012 to 2015, analysts expected earnings to grow by 6% on average, however, actual EPS fell in 3 out of those 4 years.

Among companies with the highest consensus earnings growth, First Resources focuses on palm oil: everything from plantations to refinery and processing. Analysts expect the company’s refining margins to improve. Price has gained more than 20% in the past 6 months.

Sembcorp Marine builds, repairs and upgrades rigs and platforms used in the oil industry. The poor outlook is due to weak demand that follows low oil prices.

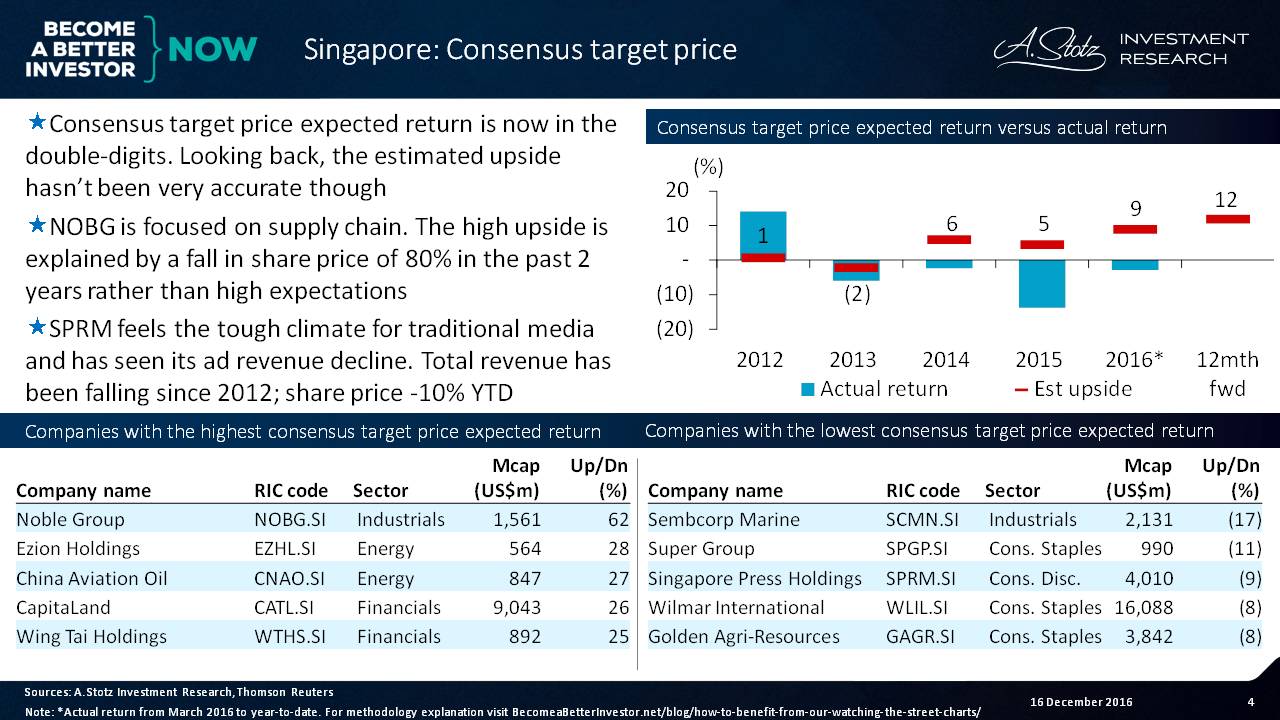

Consensus Target Prices: Singapore

Consensus target price expected return is now in the double-digits. Looking back, the estimated upside hasn’t been very accurate though. Estimates have overstated actual returns in 4 out of the last 5 years.

Noble Group is focused on supply chain logistics. The company’s high upside is explained by a fall in its share price of 80% in the past 2 years rather than any high growth expectations.

Singapore Press Holdings is feeling the tough climate for traditional media and has seen its ad revenue decline. Total revenue has been falling since 2012. Its share price has fallen by 10% YTD.

Do YOU use any kind of analyst estimate when considering an investment?

Let us know in a comment below.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.