What Academia Say about High Cash Levels in the US

Watch the video with Andrew Stotz or read a summary of it below.

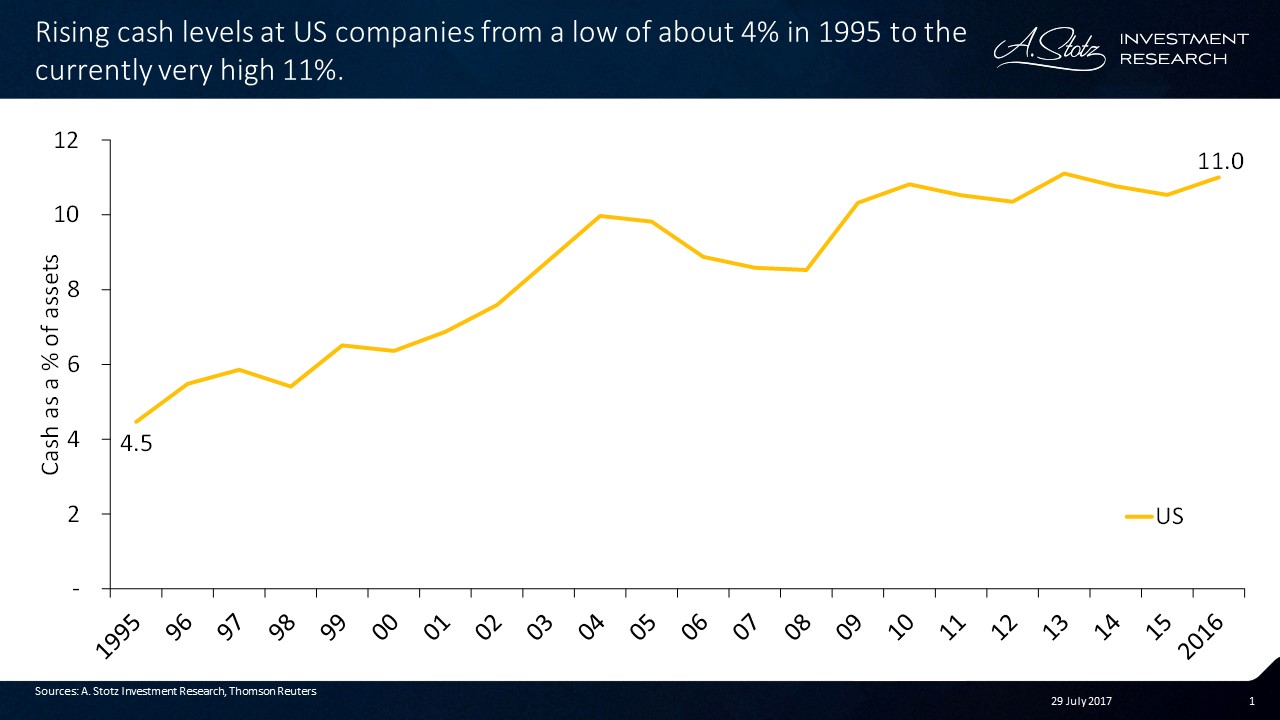

Over the last few weeks, we have been considering the causes of the rising cash levels at US companies from a low of about 4% in 1995, to the currently very high 11%.

To investigate this further, I spent some time reviewing relevant academic research on the topic. The following proposed reasons for increased levels of cash are:

Agency problems

Entrenched managers (agents of shareholders) of firms with poor investment opportunities prefer to hold more cash than pay it out as dividends to shareholders. Also, entrenched managers tend to spend this excess cash more quickly.

Tax repatriation issue

The US taxes the difference in the tax rate on profits a US company has earned in a foreign country when that company repatriates the funds to it US parent. So, if it has earned a lot of profit in its Irish subsidiary and that is taxed at 5% rather than the US rate of 35%, the 30% difference is only paid when the company brings the cash back to the US. So, the choice is made to mainly keep the funds outside of the country. From what I can see, this is not the main driver of the rising cash levels.

Refinancing risk

One research paper showed that companies that would find it hard or costly to refinance their short-term debt tend to hold elevated levels of cash. I would say this is obvious and is not something that has driven the shift to higher cash levels.

High R&D spending and the shift to intangible assets

Some research claims that the rise in cash levels has come from companies and industries that have high R&D costs and also have high levels of intangible assets (think about a software company). The idea is that banks prefer to lend based on tangible assets. Hence, these companies can be starved out of funding and they therefore need to maintain high levels of cash. I doubt this is the reason for the rise in cash levels but I do see how researchers could discover a positive correlation between these items and cash levels.

Inventory and capex had fallen

Some research showed that the fall in inventory and capex from 1980 to 2006 caused companies to accumulate cash. A simple and apparent reason, but this does not convince me that it is the cause of this rise.

Volatility in cash flow

Companies that have highly volatile cash flow tend to hold excess cash as a buffer against periods when cash flow is low. Makes sense, but this is too narrowly focused on a sub-set of companies to explain the change.

Learn our surprising finding about the cash levels in the US

12 relevant academic research papers

What follows is my list of 12 academic research papers that I think have relevance to this question.

2016

The stock market values excess cash less at US companies after the 2008 crisis proving that the agency problem (that managers are incentivized to invest extra cash) must be the main cause.

Joh, Sung Wook, and Yoon Young Choy. “Why Do US Firms Hold Too Much Cash?” (2016).

US firms operating abroad, with a high repatriation tax burden, tend to hold higher cash levels (at their foreign entities). Since to pay out excess cash as dividend would cause the company to realize the yet unrealized repatriation tax burden, they would prefer to hold the cash.

de Leeuw, Daniël. “US Repatriation Taxes and Corporate Cash Holdings.” (2016).

2014

Refinancing risk, the risk that a firm will not be able to continue to get funding when its current short-term debts come due, is a major reason why US firms maintained elevated levels of cash. Firms with larger short-term debt or debt with a short maturity hold more cash to reduce costs and risks related to refinancing their debt.

Harford, Jarrad, Sandy Klasa, and William F. Maxwell. “Refinancing risk and cash holdings.” The Journal of Finance 69, no. 3 (2014): 975-1012.

2013

Rising US cash levels are driven by increased R&D spending. The evidence they cite is that the increase in cash levels is happening in R&D heavy sectors such as Pharmaceutical and Information Technology.

Sánchez, Juan M., and Emircan Yurdagul. “Why are corporations holding so much cash?” The Regional Economist 21, no. 1 (2013): 4-8.

Technological change has led to the rise in intangible assets on the balance sheets of US firms. This is the most important determinant of the rise in corporate cash holdings. This is because higher intangibles mean less tangible assets are available to pledge with banks, leaving these companies with lower borrowing capacity. To compensate they hold excess cash.

Falato, Antonio, Dalida Kadyrzhanova, and Jae Sim. “Rising intangible capital, shrinking debt capacity, and the US corporate savings glut.” (2013).

2012

Studied 45 countries from 1998 to 2010 and confirmed that the increase in cash holdings is largely a US phenomenon. They found little support for the theory that cash levels are rising due to the repatriation tax issue. Part of the explanation is that high R&D companies tend to be companies with high levels of cash.

Pinkowitz, Lee, René M. Stulz, and Rohan Williamson. “Multinationals and the high cash holdings puzzle.” No. w18120. National Bureau of Economic Research, 2012.

2010

Found that greater cash holdings for US companies that are financially constrained are a rational, value-increasing response to that firm’s excessive cost of raising external financing.

Denis, David J., and Valeriy Sibilkov. “Financial constraints, investment, and the value of cash holdings.” The Review of Financial Studies 23, no. 1 (2009): 247-269.

2009

Demonstrated a dramatic rise in cash held by US companies from 1980 to 2006. Reasons supported by this research were: Inventories had fallen, cash flow risk had risen, capex by companies had fallen, and R&D expenses had risen. Showed that companies with high R&D expenses relative to CAPEX buffer themselves against future volatility of cash flows by keeping high levels of cash.

Found no strong evidence that high cash levels are related to the agency problem (that cash grows for firms with entrenched management). Also found that rising cash also seemed to be correlated to a reduction in debt.

They also found that increases in cash were concentrated in firms that did not pay dividends, firms with recent IPOs, and firms that experienced the highest volatility in cash flows. Also proposed that lower levels of tangible assets meant that R&D may have had an increased impact since intangible assets are costlier to finance from external sources.

Bates, Thomas W., Kathleen M. Kahle, and René M. Stulz. “Why do US firms hold so much more cash than they used to?” The journal of finance 64, no. 5 (2009): 1985-2021.

2008

US Firms with weak corporate governance protections for minorities tended to keep lower cash reserves. These firms prefer to buy back shares rather than to commit to issuing consistent dividends.

Harford, Jarrad, Sattar A. Mansi, and William F. Maxwell. “Corporate governance and firm cash holdings in the US.” In Corporate governance, pp. 107-138. Springer Berlin Heidelberg, 2012.

2007

They suggest that repatriation taxes were an important driver of corporate cash holdings. First, they find that firms retain more cash if they are faced with relatively higher tax costs upon repatriating income. Second, they find that firms keep a larger percentage of their cash holdings abroad when they face a higher repatriation tax burden. Third, they find firms hold higher amounts of cash in affiliates that are responsible for the earnings creating high repatriation tax burdens.

Foley, C. Fritz, Jay C. Hartzell, Sheridan Titman, and Garry Twite. “Why do firms hold so much cash? A tax-based explanation.” Journal of Financial Economics 86, no. 3 (2007): 579-607.

Showed that firms facing severe agency problems suffered from the negative effect of large cash holdings on their operating performance.

Dittmar, Amy, and Jan Mahrt-Smith. “Corporate governance and the value of cash holdings.” Journal of financial economics 83, no. 3 (2007): 599-634.

1999

Developed a predictive model for firm cash levels and compared firm behavior relative to that model. Found that US firms that hold more cash are generally those with higher growth opportunities and firms with more uncertain prospects. Firms with higher capital expenditures hold less cash.

Opler, Tim, Lee Pinkowitz, René Stulz, and Rohan Williamson. “The determinants and implications of corporate cash holdings.” Journal of financial economics 52, no. 1 (1999): 3-46.

Learn what we later found out about the cash levels in the US

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.