VMC: Currency Hedging Strategies for Companies

This is a Valuation Master Class student essay by Teeradon Piyakiattisuk from 31 May, 2019. Teeradon wrote this essay in Module 3 of the Valuation Master Class. The post was originally published here.

The world has become globalized; companies who have cross-border activities are engaged in currency exposure. As everyone knows the fact that the currency exchange rate is highly volatile. Multinational companies may confront a loss of revenue when incomes from foreign subsidiaries converted to the home currency. Exporters would confront revenue uncertainty if their home currency appreciated. Importers may have a low-profit margin from an increase in the cost of goods, which resulted from currency depreciation. All of these are forcing management to think about protecting their profit against the exchange rate risk through hedging strategies and derivative instruments.

External hedging – hedging instruments

1. Currency forwards contracts

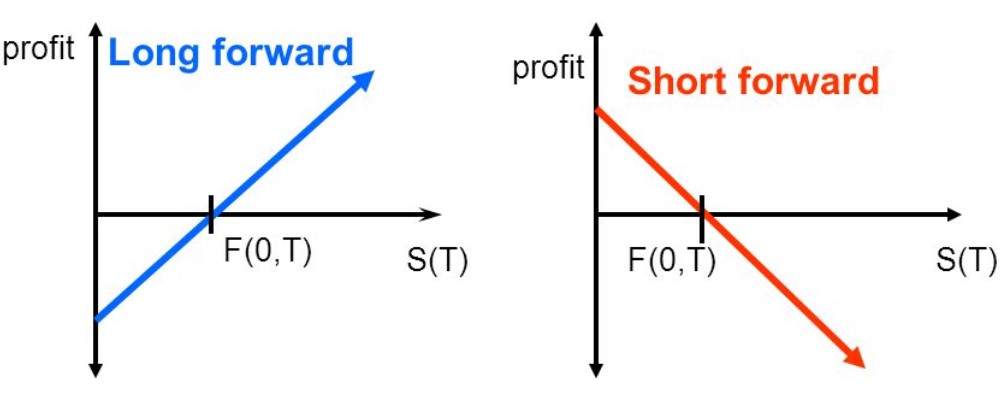

A currency forward contract is an agreement between a buyer and a seller to trade an underlying asset (a currency) at a future date for a certain price. The forward contracts are not traded on organized exchanges such as a clearinghouse. They are traded directly between 2 parties, which are a customer and a bank. The bank usually acts as a dealer who matches the agreements between short contracts and long contracts. The contract size can be whatever amount. There is a cash transaction at the time of entering a contract.

Imagine a Thai importer; their inventories are 100% imported from a US exporter. The importer’s transactions are to pay the US exporter. If the Thai importer needs to pay the goods in 10 days and concerns the volatility of the exchange rate between the Thai Baht and US Dollar. This means the Thai importer needs to convert Thai Baht to US Dollar to pay the US exporter in 10 days. The Thai importer will enter into short forward contracts with a dealer bank, which means the bank agrees to sell US Dollars to the Thai importer at a certain exchange rate in 10 days.

On the other hand, imagine a Thai exporter produces goods which 100% sell to a US importer. The buyer agrees to pay in 10 days in US Dollars. The Thai exporter knows, they will receive money in US Dollars in 10 days. If the Thai seller wants to know a certain income on the date they agree to sell; they will lock the exchange rate by entering into long forward contracts. It means a dealer bank agrees to buy US Dollars from the Thai seller at a certain exchange rate in 10 days.

An advantage of forwarding contracts is that they are more tailor-made to the customer’s needs. They offer the possibility to adjust the quantity of currency and maturity. By contrast, the forward contracts are an obligation. The parties will be committed to complete the contracts on the maturity date.

2. Currency options

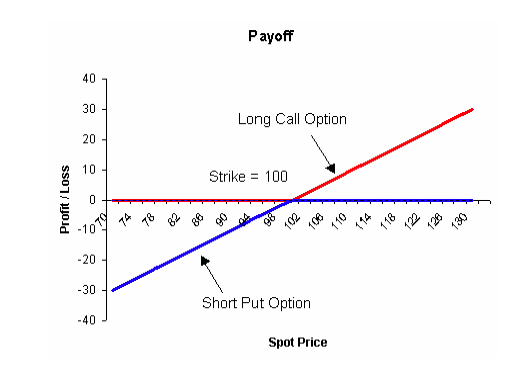

An option is a contract that gives a company the rights, but not the obligation, to buy or sell a giving amount at a certain exchange rate for a future date. It seems that options are insurance that a company pays a premium to enter into a right to buy or sell a currency. There are 2 basic types; call options and put options, which can be summarized to the 4 basic positions.

• A long position in a call option – the person buys the right to buy a currency.

• A long position in a put option – the person buys the right to sell a currency.

• A short position in a call option – the person sells the right to sell a currency.

• A short position in a put option – the person sells the right to buy a currency.

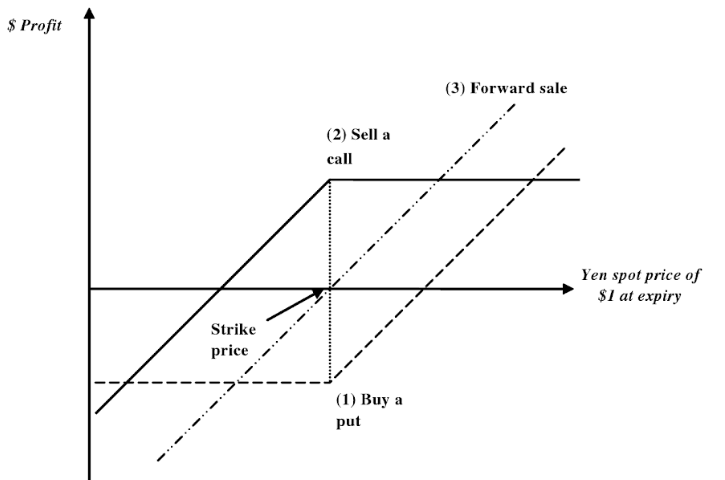

Options can replicate the payoff of forward contracts by creating synthetic forwards. The graph below shows the payoff between a long call option and a short put option equals to a long forward contract.

• Long forward contracts = long call option + short put option

• Short forward contracts = short call option + long put option

To create the synthetic forwards, a company needs to buy and sell both positions on the same currency, same strike price, and same maturity. These will give a company the same as the forward contracts without an obligation. However, options are relatively complicated, and a company needs to pay a premium.

Companies Internal hedging strategies

A company can internally manage or reduce the currency risk, which is called natural hedging.

1. Choice of invoice currency

The best way to reduce the currency risk is to make invoices in the domestic currency. Not all foreign importers are willing to be invoiced in the domestic currency of the exporter. It depends on negotiation, which parties have more market power.

2. Netting

If a company has receivables and payables in different currencies, it can offset exposure in one currency with exposure in another or the same currency. Multinational companies use netting strategies whose currency exposures can be managed as a single portfolio.

3. Matching

As it is not possible to enter into forward contracts with a period over 1 year, the matching strategy can be used when a company has continuing export sales and use the cash inflow from export sales to pay the principal and interest expense in the same currency.

Mistakes to be avoided

It is probably better to avoid making mistakes on misguided FX risk management policy. There is a thin line between hedging and speculation. Management should have clear objectives that their strategies aim at stabilizing the balance sheet, rather than speculation. Management should be aware of their risk aversion and the impact of large aversion movements. Moreover, hedging comes with costs. Overusing derivatives increase unnecessary costs.

References

http://dspace.unive.it/bitstream/handle/10579/3787/836638-1169232.pdf?sequence=2

Join the Bootcamp for Valuation!

The Valuation Master Class is the complete, proven, step-by-step course to guide you from novice to valuation expert.

Save US$50 with coupon code: get-smarter

Click here to learn more and register.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.