Noodles in Exchange for Investing Advice

The Chinese stock market may only appear cheap

During my recent trip to my university in China, I explored the topic of the Chinese stock market, which appears cheap at a 13x price-to-earnings (PE) ratio. However, this is distorted by a very low PE financial sector that is a third of overall stock market value. That Chinese investors trade the financial sector at such a low PE could spell trouble.

By stripping out the financial sector, I show that the Chinese stock market is actually trading on 20x PE, a 32% premium to the world PE. The sector which looks most reasonable value seems to be the Chinese Consumer Discretionary sector.

China A-shares appears cheap…

The China A-shares stocks appear cheap at first pass, trading at about a 20% discount to the world. China’s 13x price-to-earnings (PE) ratio, is slightly below the global average of 15x 2016 earnings. Price-to-book is the same, China trades on 1.5x book value versus the global 1.8x. However, like many things in China, looks can be deceiving.

…But valuation is distorted by massive financial sector

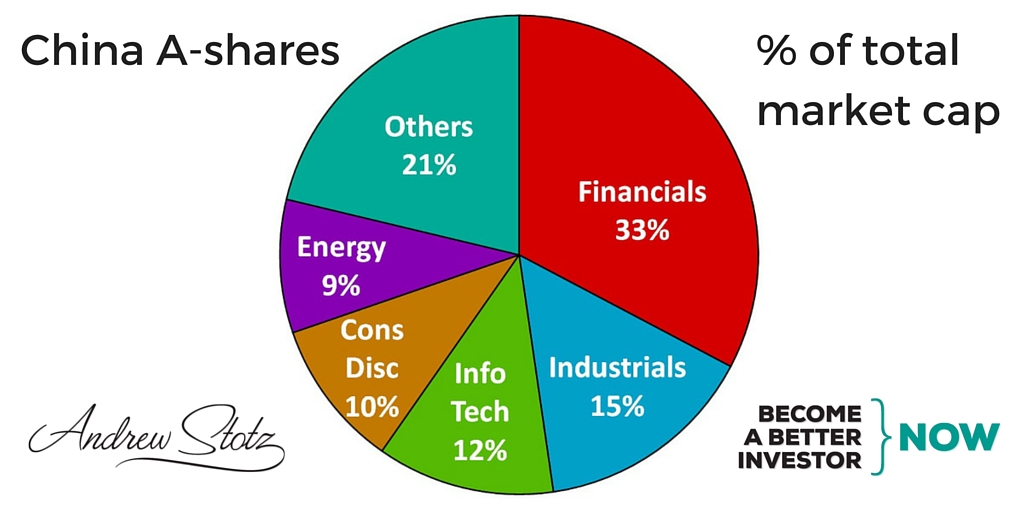

The market capitalization of the Chinese stock market is now more than US$6tn, the largest sector by far is the financial sector which accounts for 33% of total market value. The next largest is the Industrials sector accounting for 15%, followed by Information Technology at 12%, and then Consumer Discretionary sector at 10%.

Cheap banking sector is a bad sign

The banking sector in China trades on a PE multiple of 7x which is 35% cheaper than financial stocks in the rest of the world, this despite that they produce an ROE of 14.4% which is nearly 60% higher than the rest of the world. Since foreign investors generally cannot invest in the China A-shares market, then we can see exactly how Chinese, rather than foreign, investors feel about their banking system. It doesn’t look good and could be a warning sign.

Central bank loosening of bank equity ownership limits

I consider banking globally a commodity business, most of the times it is a transmission mechanism for central bank policies, just two of the reasons I do not invest in them. Chinese banks are even more so such an instrument. Recent loosening of Chinese government policies allows the banks to increase their equity holdings in companies if acquired through debt-to-equity swaps-a method of restructuring bad loans.

Generally central banks restrict bank ownership of equity in companies as this is a higher risk activity than lending and could bring down a bank, increasing the risk of a run on deposit and a burden on the central bank. So, to me, the loosening of this policy is an indication that the central bank is anticipating a need for banks to have more flexibility to deal with a potential restructuring of customer loans.

Giving banks this flexibility is one of a few tools that central banks have to prevent pain at struggling companies, which in turn can hold off a banking system crisis.

Banks could suffer fall in interest income, but some long term gain

The impact of such transactions in Thailand after the 1997 economic, hence banking crisis, was a substantial fall in interest income and eventually a small overall net gain on this equity acquired through debt-to-equity swaps. Chinese investors may be right to be spooked about Chinese banks, hence to trade them down at a low level of PE.

Noodles in exchange for stock market investing advice

While visiting Hefei, Anhui province a friend took me to a noodle shop. The 24-year-old owner of the shop had asked my friend if he knew anything about investing because he had lost a lot of money in the stock market. Since it was not his area of expertise, my friend brought me for a bowl of noodles and a chat.

The young noodle shop owner told me that in addition to his recently set up noodle shop he also had been investing in the stock market. I asked my standard questions and found that he had no prior education in investing, he owned an undiversified portfolio of three stocks and he had lost more than 50% of his original investment.

Most people in this situation say the same thing to me, “I will never invest in the stock market again”, but not this man, he wanted to learn how to do it better next time. My main advice was to pause and study a bit before proceeding.

The Chinese stock market may appear cheap, but is actually relatively expensive

One of my recent (very unscientific!) Twitter polls showed that 62% of the 40 respondents thought that the Chinese stock market was expensive.

Is the Chinese stock market

— Andrew Stotz, CFA (@Andrew_Stotz) March 14, 2016

A similar poll I did of my friends who are CFA charterholders in Guangzhou showed about the same results. To answer this question more scientifically we can remove the heavily weighted and deeply discounted banking sector from the calculation of PE and we find that instead of the Chinese market trading on 13x PE it is trading on 20x PE, a 32% premium to the world PE.

Consumer discretionary shows the most reasonable value

The Consumer Discretionary sector, a sector that is usually hit hard going into a financial crisis, seems to be one of the most attractive sectors relative to the world. The sector is earning a return on equity, which is in line with the world average of its sector and trades at a PE which is in line with the world average.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.