Don’t Rush into Korea Just Because It’s Super Cheap

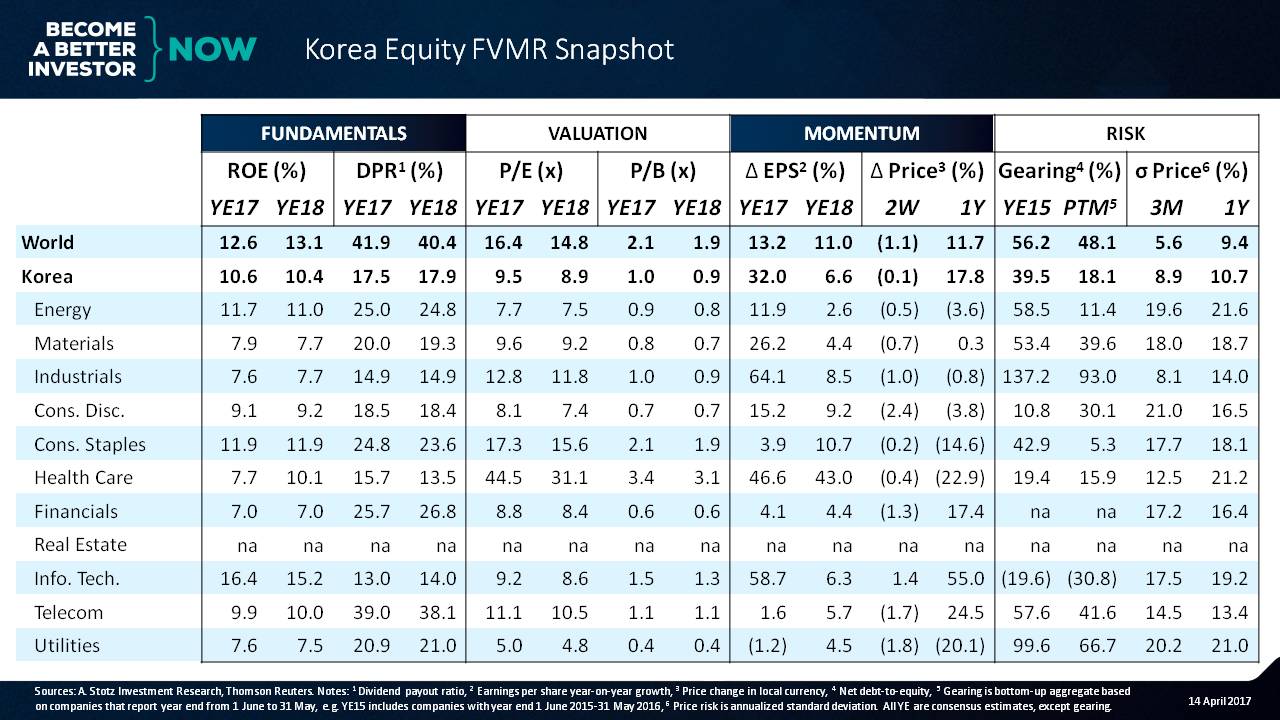

Korea Equity FVMR Snapshot

Fundamentals: Profitability and dividends are low

Remember that FVMR stands for fundamentals, valuation, momentum and risk.

The first thing we want to look at is the ROE. What we can see is that the worldwide ROE sits at 12.6%; but in Korea, it’s about 10.6%.

So the profitability of Korean companies is pretty low. In fact, look at the number of sectors that have ROEs below 10% ─ one, two, three, four, five, six, seven. We can say that it is a low ROE country, for sure.

The highest ROE ratios are in the consumer staples and the information technology sector.

Let’s take a look at the next thing, which is dividend payout ratio.

We can also say that this is a very low dividend country at about 17.5% versus 40% in the rest of the world ─ half the dividend payout ratio.

Sometimes, we look at Korea and we look at the big conglomerates and think that there’s an issue with governance.

I think one way that we can look at it is that one of the reasons why we like high dividend payout ratios is because it forces the “corporates” to give out their cash rather than continuing to reinvest.

Really, why would you want to have a company reinvesting almost 80% of their profits at a low rate of 10%?

Pay it out!

Valuation: Traditionally low

If you look at the PE of the Korean market, what we’re going to see is that the PE is almost half the global average. I’ve written before about this Korea discount, and there are many different reasons for it.

I wouldn’t say that you’d want to rush into this market just because it’s super cheap.

What we can also see is that price-to-book is now about 1x versus the world at about 2x ─ so again, half the valuation.

Momentum: Overly optimistic analysts

We always see that Korea has this very big discount.

Why?

One of the reasons is this very low ROE. But analysts are forecasting 32% earnings growth.

But the dissertation that I did for my PhD looked at the performance of financial analysts in the stock market based on their forecasts, and Korea tended to be the one that had the highest amount of optimism in their earnings forecast.

So you may be looking at earnings where instead of coming in at 32%, they may be coming in more at about 10% or 15% for Korea.

If we look at some of the sectors, I’m going to look for where there’s sustained growth. And here we have two years of 40+% earnings growth.

I’m not so interested in some of the sectors with bumpy earnings, because this tends to be a turnaround sector such as industrials.

Healthcare looks like an interesting sector except ─ oh my goodness ─ I’ve got to pay 40x for that in a market that’s trading on 10x. That’s pretty rough.

If we look at the price game, we can see that the Korean market has gone up by about 18% versus about 12% or so for the overall world in the last 12 months.

Volatility: A low gearing environment

But the good news is that Korea has low gearing. That’s good, but what we can see is it’s probably depressing the ROE here. They’ve got a lot of equity on their balance sheets compared to the rest of the world.

We could compare their ROA and try to understand the difference. I use ROA in my World Class Benchmarking.

So maybe that ROE is not so bad. But why do they need so much equity?

The last thing we can look at is the volatility in price.

We can see the high volatility sectors. Here we have the energy sector with high volatility, and we can say that the health care sector has high volatility.

Wow, that’s interesting ─ low ROE, high PE, but fast growth and lots of volatility!

Let’s look at our lowest volatility sector, and we can see that this is industrials. That’s the lowest volatility.

Overall, the Korean discount remains with the Korean market earning an ROE on a very low amount of leverage of 10%, paying out a tiny amount with only 20% of the profits as dividends, and trading on a PE of about 9x and a price-to-book of about 1x.

And while analysts are expecting about a 32% growth in 2017, they tend to be very optimistic in Korea, so I would pull that down.

Overall, Korea is not a particularly exciting market to me at this moment.

Do you want to look at your own country?

Just let me know in a comment below and I will try to do it if I have it.

Get our Equity FVMR Snapshots for free to your inbox every Monday!

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.