Chinese Stocks Aren’t Cheap, Chinese Banks Are

China Equity FVMR Snapshot – October 2016

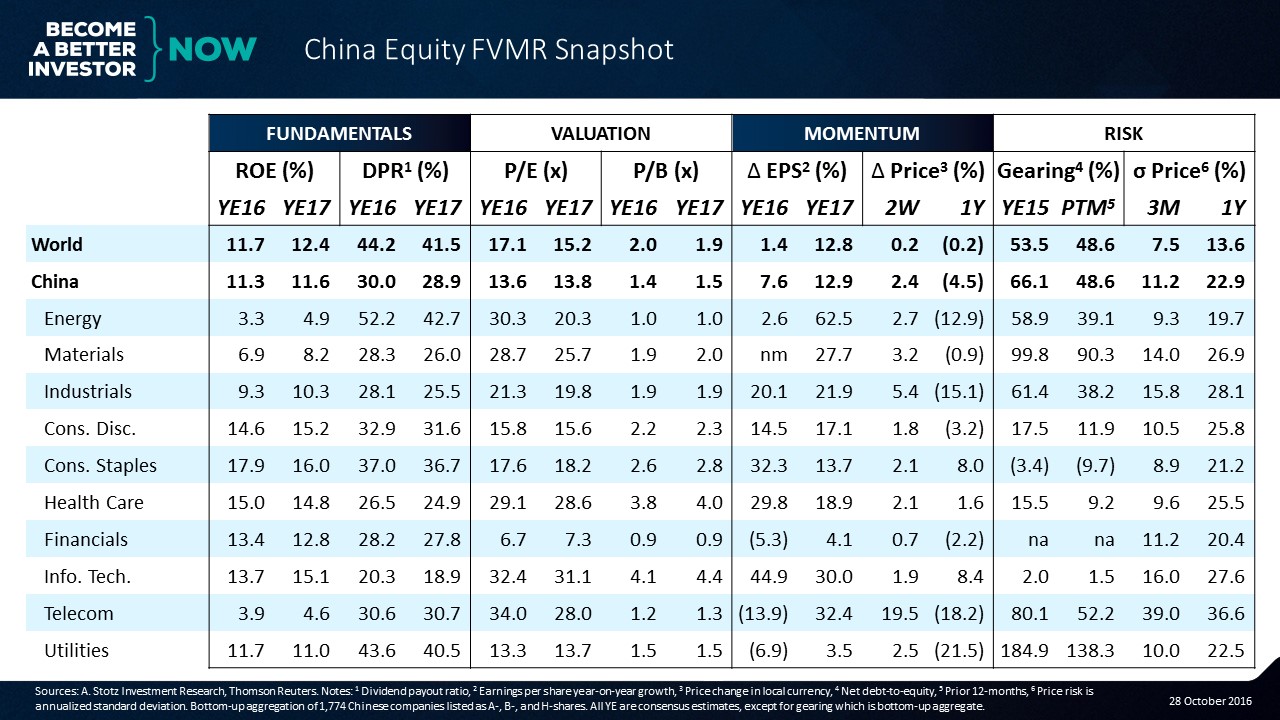

Note: This is a bottom-up aggregation of 1,774 Chinese companies listed as A-, B-, and H-shares.

Fundamentals

Four sectors stand out in terms of high profitability in China. The two consumer sectors with Consumer Staples being the sector that delivers the highest ROE in the country. Health Care delivers an ROE of 15% and the profitability of the Info Tech is expected to improve 1.4ppts in 2017.

Chinese companies pay out less of earnings in dividends than the world average. Energy is an exception but that is a result of low earnings rather than a generous dividend policy. Utilities is the sector with the most generous dividend policy in China.

Valuation

The PE for the Chinese market appears to be cheap relative to the World average. However, if you look at it sector by sector, you’ll find that there are only three sectors trading below the world average on 2016CE* PE: Financials, Utilities, and Consumer Discretionary. Financials is the reason that China appears cheap on PE, the sector is very cheap and constitutes about one-third of the Chinese market capitalization.

China excluding banks trades at 2016CE* 21.6x PE and 1.9x PB versus including banks at 2016CE* 13.6x PE and 1.4x PB.

On a price-to-book basis, valuations are more measured. Financials are trading below book value and Info Tech is most expensive. Chinese Info Tech is trading at 2016CE* 4.1x which is above World Info Tech at 3.4x PB. In addition, World Info Tech offers an ROE of 18.2% versus Chinese Info Tech at 13.7%.

China looks more attractive than the World on ROE/PB at 2016CE* 7.8% versus the World at 5.9%. This is again distorted by banks as China excluding banks trade at 2016CE* 4.9% ROE/PB.

Momentum

In terms of earnings growth, 2016 is expected to show strong growth in most sectors. Exceptions being Telecom, Utilities, Financials, and Energy. The Materials sector is expected to see a massive earnings rebound in 2016.

Earnings are expected to grow at a fast pace in 2017 as well. Financials is expected to continue to be a drag on EPS growth; including banks the 2017CE* EPS growth is expected at 12.9% and excluding banks the growth in earnings is expected to be 23.3%.

Price performance in the past two weeks has been exceptionally strong in the Telecom sector at 19.5%. Most sectors have not yet recovered from the Chinese crash that began in late December 2015 and bottomed out by the end of January 2016. Only Info Tech, Consumer Staples, and Health Care have shown a positive one-year price performance.

Risk

Chinese companies have geared down in the past 12 months and China is in line with the World on net debt-to-equity. The highest gearing is in Utilities and Materials, while Consumer Staples is net cash.

China is more volatile than the world. In the past three months, the Telecom sector has been extremely volatile and no sector is less volatile than the global average.

*CE is Consensus Estimates

Get Equity FVMR Snapshots to your inbox for free every Monday!

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.