China No Longer Appears Cheap When Banks Are Excluded

China Equity FVMR Snapshot

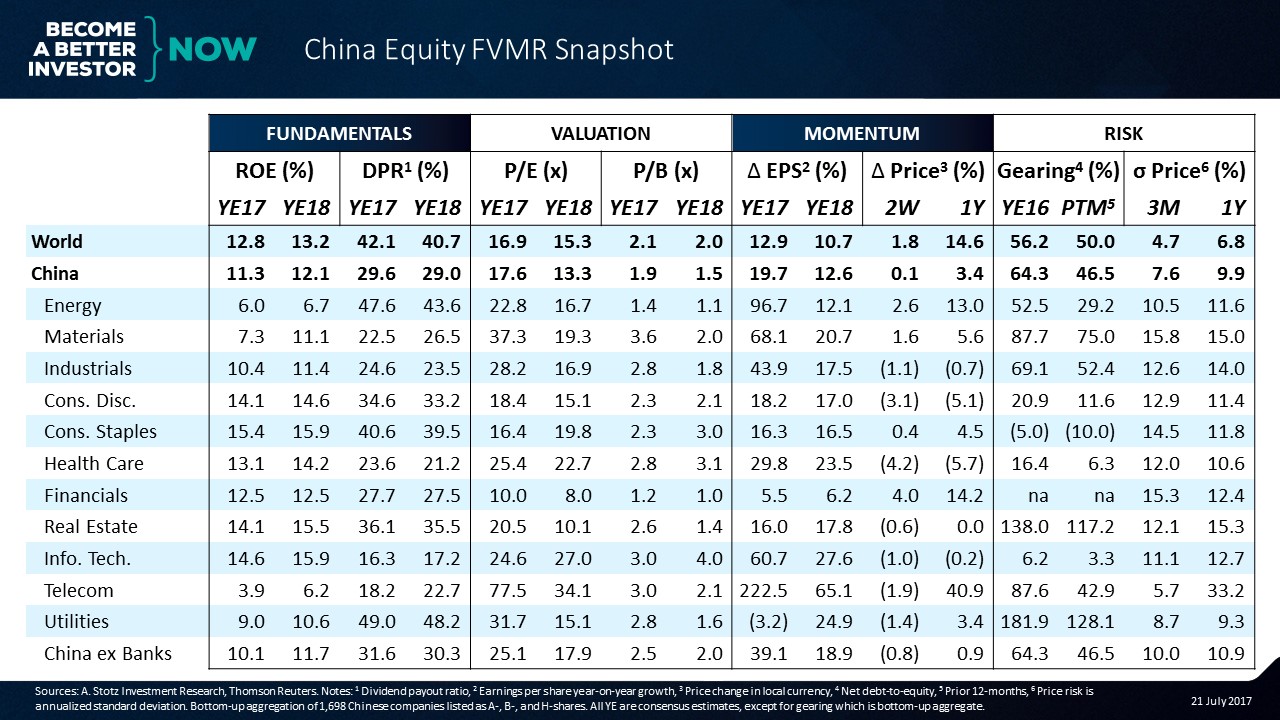

Remember that FVMR stands for Fundamentals, Valuation, Momentum, and Risk. Those are the factors that we look at to get an understanding of the market. This China Equity FVMR Snapshot is an aggregation of 1,698 Chinese companies listed as China A-, B-, and H-shares.

Fundamentals: China has lower profitability compared to the world

The return on equity (ROE) of China is about 11% versus the world, which is at 13% ─ a slightly lower ROE. It seems to be tough to be a Chinese Telecom company at the moment as the sector has the lowest expected ROE of only 3.9% in 2017. Consumer Staples is at the other end of the spectra with ROE of more than 15%.

Overall, the Chinese market has a lower dividend payout ratio (DPR) versus the world. Chinese companies only pay out about 30% of earnings as dividends, while the global average is about 40%.

Valuation: Financials weighing down rest of market

The overall Chinese market trades slightly above the world on 2017 price-to-earnings (PE) and slightly below on 2017 price-to-book (PB). However, the Chinese banks have a quite big impact on the overall market metrics, as you can see, China ex Banks PE on 2017 earnings is at 25.1x versus 17.6x when banks are included. Looking at PB, the Chinese market trades at 1.9x, but when we exclude banks the market trades at 2.5x which is above the world.

China no longer appears cheap when we exclude banks.

Momentum: China has underperformed the world by more than 10%

As noted above, China is expected to grow earnings faster than the world. Telecom is expected to have the fastest earnings per share (EPS) growth at 222.5%, however, this is due to a low base as EPS fell by 76% in 2016. The Energy sector also comes from a slight decline in earnings in 2016, which is expected to be more than offset in 2017.

Earnings in the Utilities sector fell by about 20% in 2016 and are expected to fall a bit further in 2017.

China has underperformed the world by more than 10% in the past one year in terms of price performance. Only the Telecom sector has had a better price performance in the past one year. In the past two weeks, only Financials and Energy have had a better price performance than the world average.

The worst performing sector in the past two weeks was Health Care.

Risk: Relatively low among utilities, financials

Gearing in China has fallen in the past 12 months and is now below the world average. Consumer Staples is the only net-cash sector in China at the moment. Utilities has the highest gearing, followed by Real Estate.

The Chinese market has been more volatile than the world. In the past one year, Utilities has been the least volatile sector and Telecom was the most volatile. However, in the past 3 months, Telecom was the least volatile sector and Financials was the most volatile.

Get our Equity FVMR Snapshots for free to your inbox every Monday!

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.