A. Stotz All Weather Strategy – November 2020

The All Weather Strategy underperformed as World equity recovered in the past three months. President Biden, stimulus checks, and vaccine news lead to positive sentiment. We increase our equity allocation to the strategy maximum of 85%.

The A. Stotz All Weather Strategy is Global, Long-term, and Diversified:

- Global – Invests globally, not only Thailand

- Long-term – Gains from long-term equity return, while trying to reduce a portion of losses during equity market downturns

- Diversified – Diversified globally across four asset classes

The All Weather Strategy is available in Thailand through FINNOMENA. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

Review

Equity markets rebounded in the past three months, US lagged

- In the past three months, equity markets rebounded

- We increased our equity allocation in the past revision, but it remained conservative at 50%

- Reducing bonds, and increasing equity and commodities enhanced the performance

- Japan and Asia Pacific ex Japan were the strongest performers, followed by Developed Europe and Emerging Markets

- The US was the weakest performing equity market

- In the past three months, we correctly overweighed Asia Pacific ex Japan with a 25% target allocation

Bonds stayed flattish, adding to underperformance

- Our bond target allocation was 15% in the past three months, down from 30%

- Which is comprised of only Thai government bonds, rather than a mix of global government and corporate bonds

- We had our bond allocation to protect the downside

Commodities recovered in the past three months but underperformed equity

- We’ve had a 5% target allocation to commodities

- Increased Chinese demand and increased risk appetite on COVID-19 vaccine news supported prices of industrial metals and energy

- Though commodities showed a positive return in the past three months, it lagged equity markets

Risk-on mode hurt gold price

- Our target allocation for gold was 30%

- As the vaccine news has spread across the world, investors have returned to risk assets

- This has been bad for gold, which traded close to a five-month low in November 2020

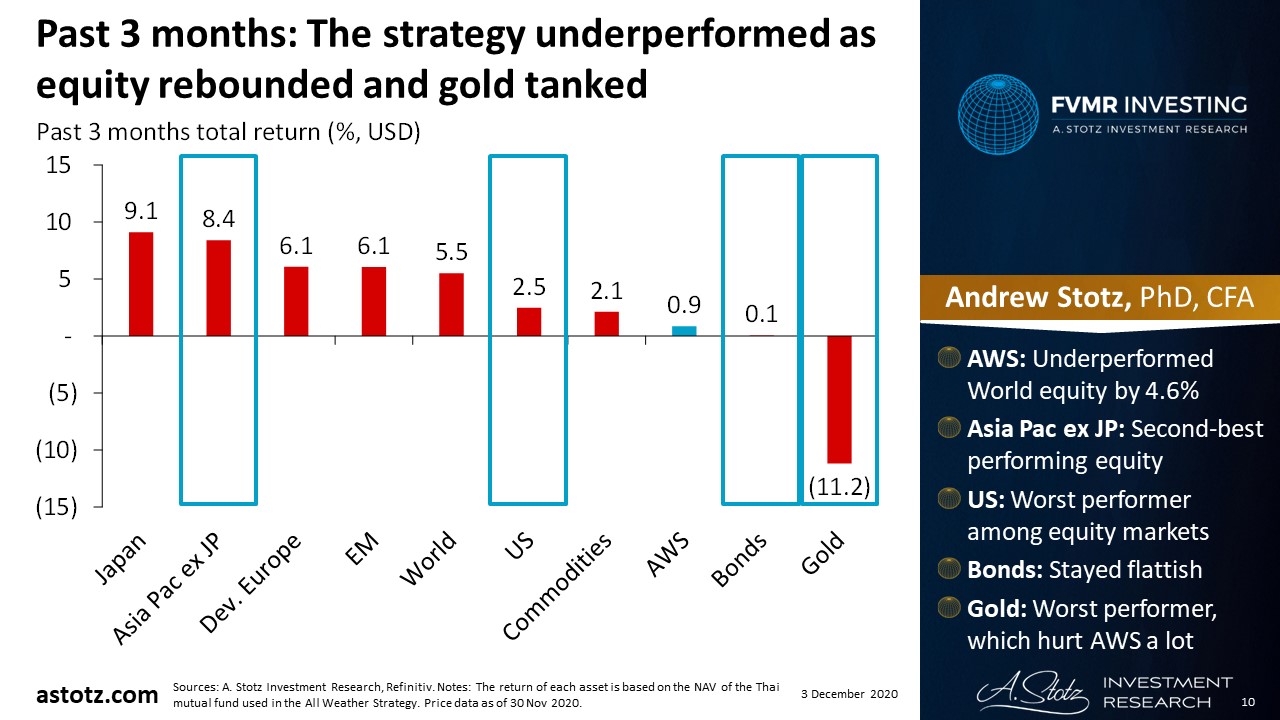

Past 3 months: The strategy underperformed as equity rebounded and gold tanked

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- All Weather Strategy: Underperformed World equity by 4.6%

- Asia Pac ex Japan: Second-best performing equity

- US: Worst performer among equity markets

- Bonds: Stayed flattish

- Gold: Worst performer, which hurt All Weather Strategy a lot

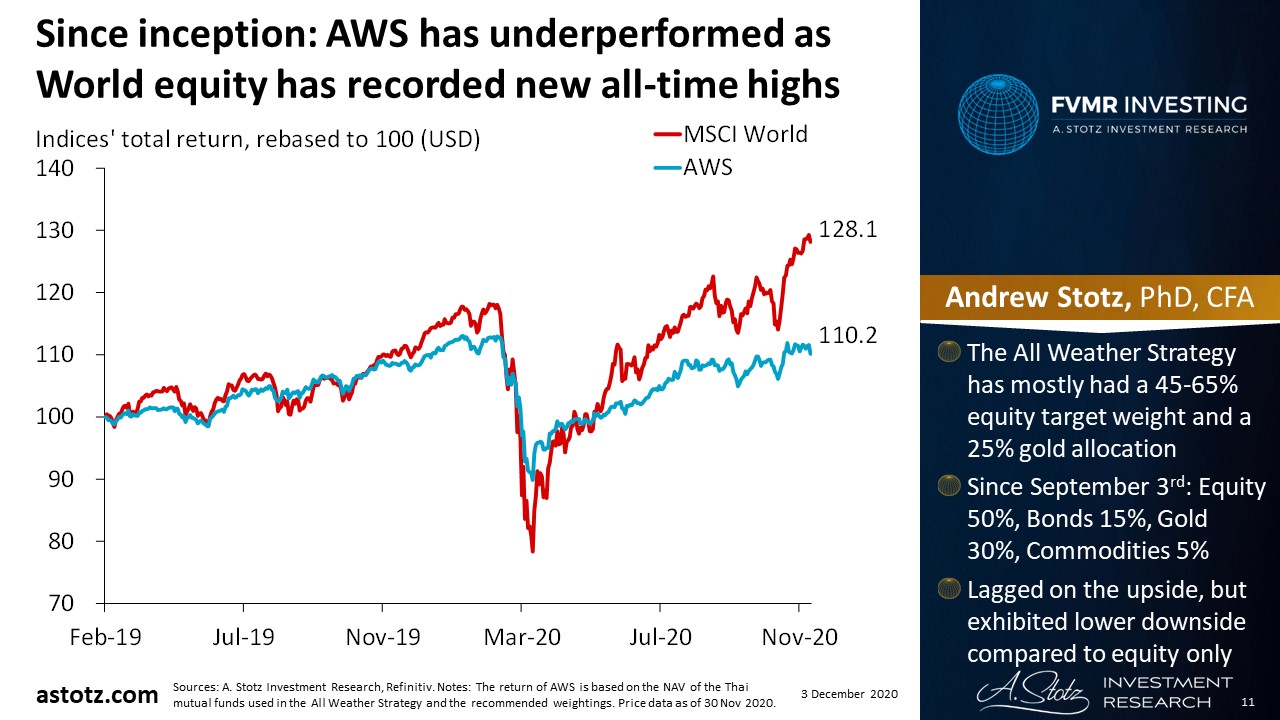

Since inception: All Weather Strategy has underperformed as World equity has recorded new all-time highs

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- The All Weather Strategy has mostly had a 45-65% equity target weight and a 25% gold allocation

- Since September 3rd: Equity 50%, Bonds 15%, Gold 30%, Commodities 5%

- Lagged on the upside, but exhibited lower downside compared to equity only

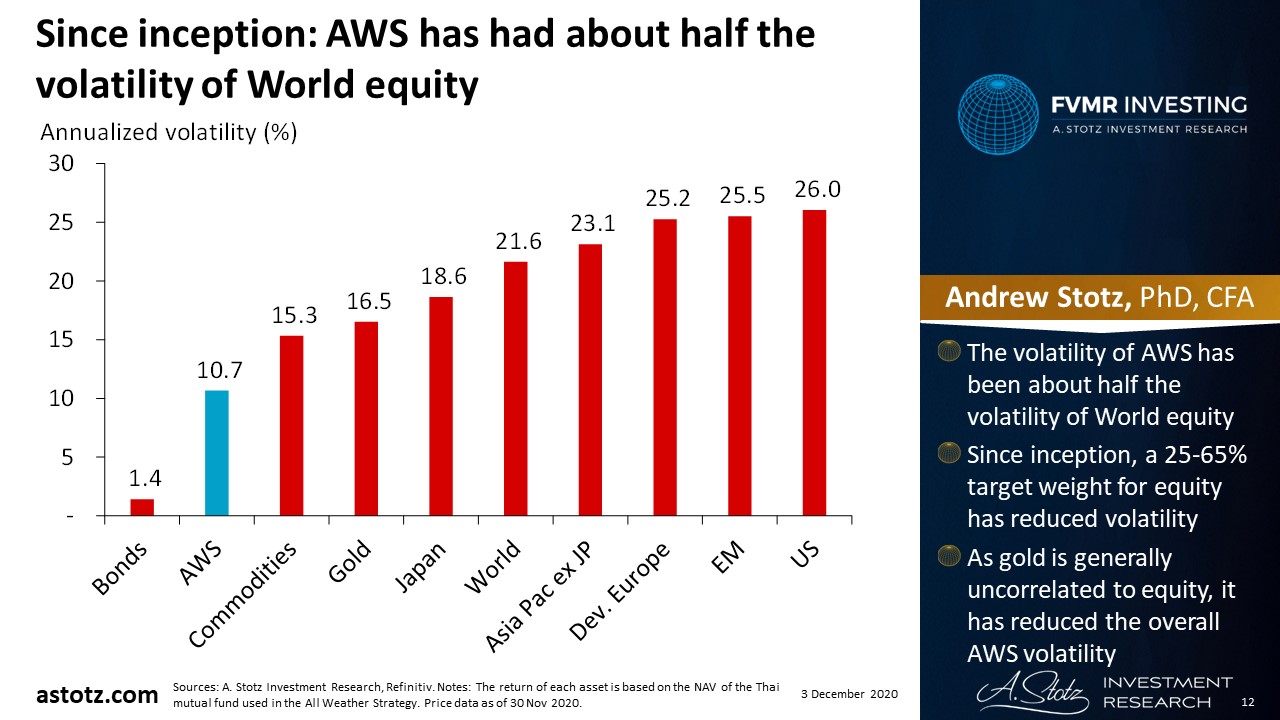

Since inception: The All Weather Strategy has had about half the volatility of World equity

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- The volatility of All Weather Strategy has been about half the volatility of World equity

- Since inception, a 25-65% target weight for equity has reduced volatility

- As gold is generally uncorrelated to equity, it has reduced the overall All Weather Strategy volatility

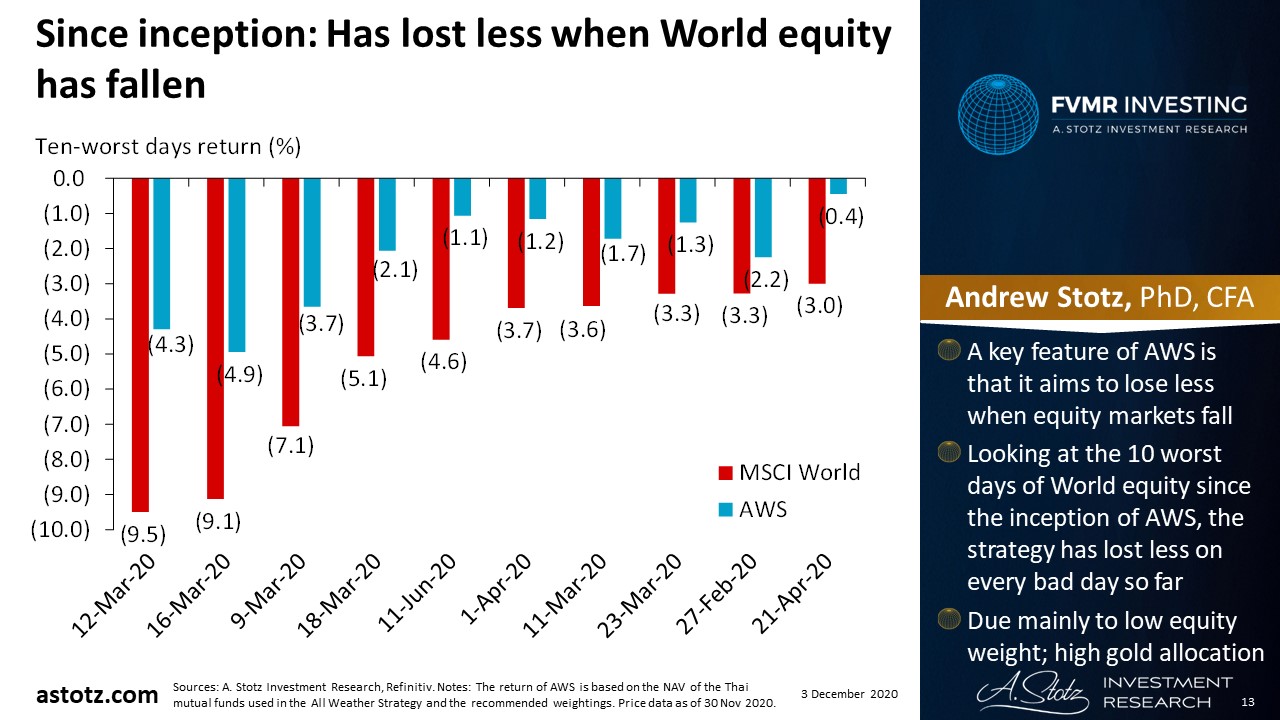

Since inception: Has lost less when World equity has fallen

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- A key feature of All Weather Strategy is that it aims to lose less when equity markets fall

- Looking at the 10 worst days of World equity since the inception of All Weather Strategy, the strategy has lost less on every bad day so far

- Due mainly to low equity weight; high gold allocation

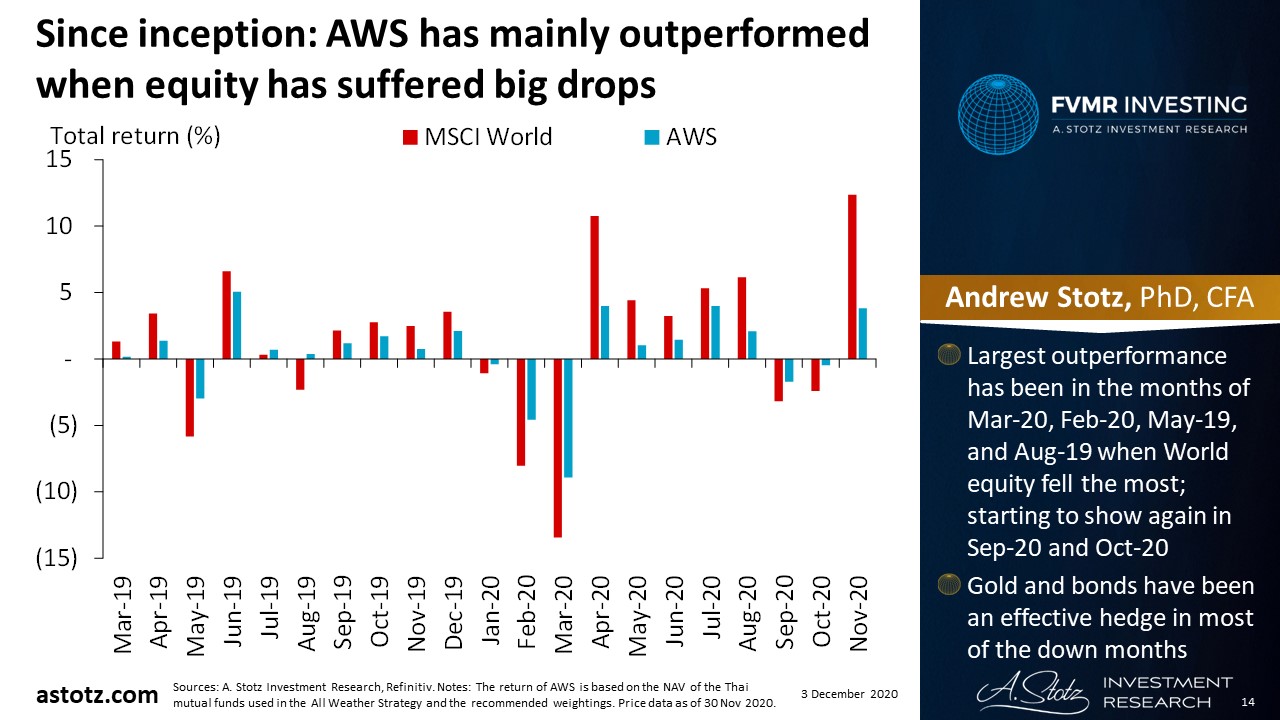

Since inception: The All Weather Strategy has mainly outperformed when equity has suffered big drops

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- Largest outperformance has been in the months of Mar-20, Feb-20, May-19, and Aug-19 when World equity fell the most; starting to show again in Sep-20 and Oct-20

- Gold and bonds have been an effective hedge in most of the down months

Weights

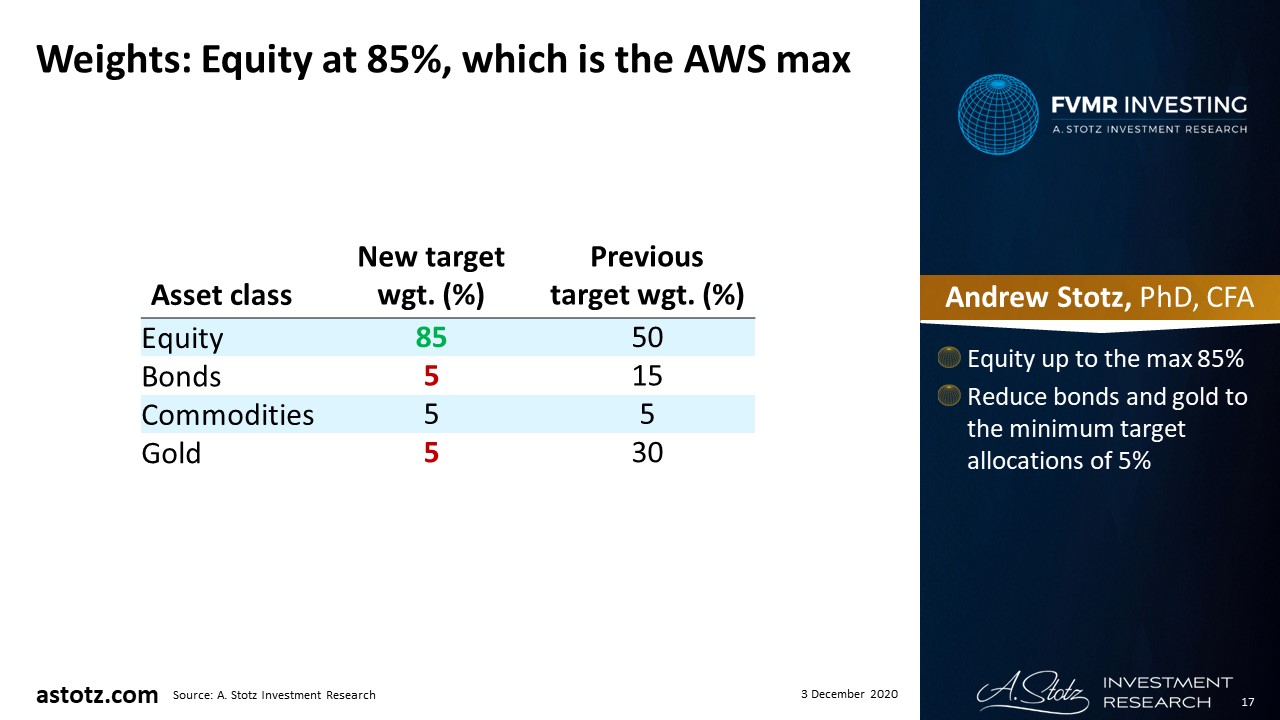

Raise to the max target equity allocation of 85%, reduce gold to 5%

- Reducing weight in bonds to 5% from 15%

- Raise equity exposure to 85% from 50%

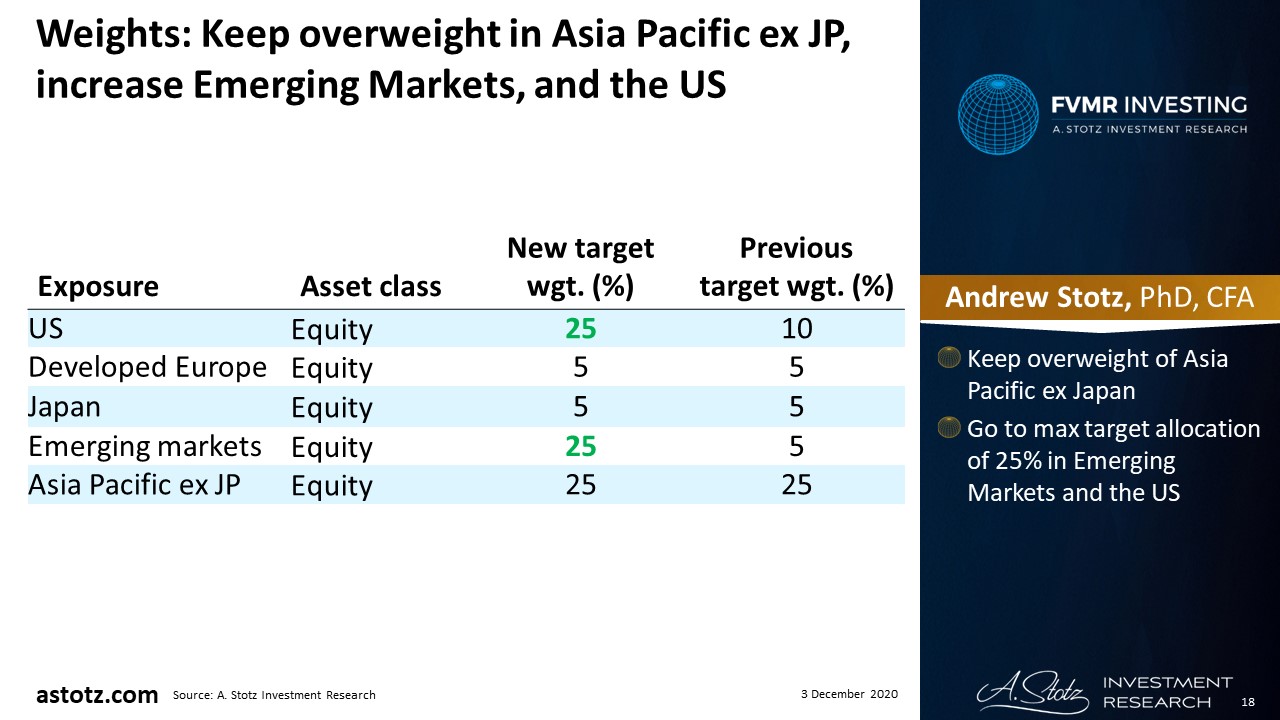

- We raise US equity weight to 25% from 10%

- We still see the biggest risk in US equity but see strength in the short run

Raise to the max target equity allocation of 85%, reduce gold to 5%

- Increase the target weight in Emerging Markets to 25% from 5%

- Reduce gold to 5% from 30%

Equity at 85%, which is the All Weather Strategy max

- Equity up to the max 85%

- Reduce bonds and gold to the minimum target allocations of 5%

Keep overweight in Asia Pacific ex JP, increase Emerging Markets, and the US

- Keep overweight of Asia Pacific ex Japan

- Go to max target allocation of 25% in Emerging Markets and the US

Outlook

President Biden, let the stimulus rain!

- The election was a tough fight but, as we expected, Joe Biden appears to be the next US president

- This is likely to lead to more fiscal stimulus

- There’s a new US senate proposal for a stimulus package of US$908bn

At least near-term support for equity

- Stimulus doesn’t resolve anything with regards to US overvaluation or debt issues

- However, we think it could boost the US stock market in the near term

- It could also put downward pressure on the US Dollar, which should be positive for Emerging markets and Developed Asia

Inviting to the after-after party

- Europe is likely to launch more stimulus packages as well to keep the party going

- The new motivation for putting the money printer to work is often green, stimulus to improve the environment and stimulate growth

DJ Xi Jinping makes Emerging Markets dance

- Goldman Sachs has DJ D-Sol, China has Xi Jinping who makes Emerging Markets dance

- China has seen a strong demand recovery, which we see as a positive for Asia

- We also see this as an important driver of Emerging Markets equity

COVID-19 vaccine is this party’s ecstasy

- News about vaccines has led to risk-on mode in the markets (even though Europe right now are seeing increased restrictions)

- It takes time until those vaccines are available, but financial markets are forward-looking

- So positive news with regards to winning over the virus is priced in today

- There is a risk that vaccines cause harm when administered at mass scale

All problems are far from resolved

- US remains overvalued, and the US gov’t debt is growing every day

- Even when COVID-19 is under control, many concerns remain, e.g., geopolitical tensions and mass unemployment

- So, while we’re now at the max allocation of 85% in equity, we’ll reconsider this decision in about three months

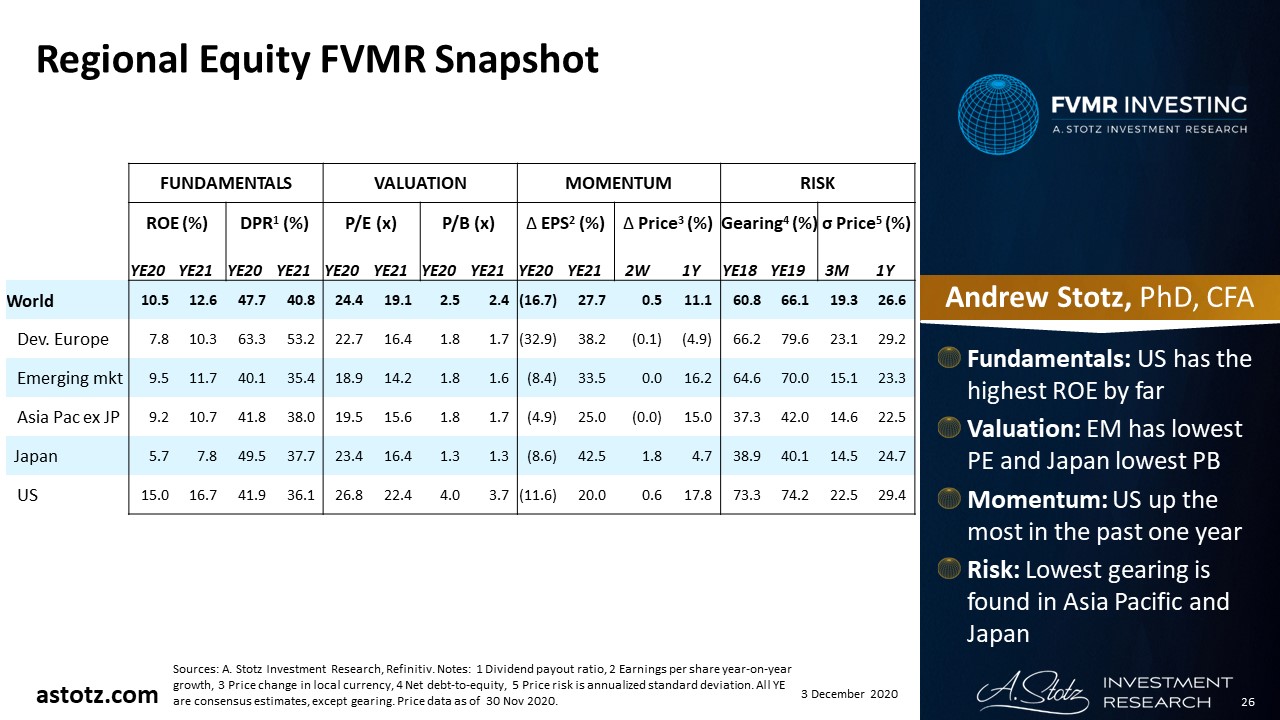

Regional Equity FVMR Snapshot

- Fundamentals: US has the highest ROE by far

- Valuation: EM has the lowest PE and Japan lowest PB

- Momentum: US up the most in the past year

- Risk: Lowest gearing is found in Asia Pacific and Japan

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.