Become a Better Investor Newsletter – 8 April 2023

Noteworthy this week

- The market doesn’t believe the Fed

- Gold surpasses US$2,000/oz t

- Central banks seem to like gold again

- Surprise oil production cuts

- War is also business (unfortunately)

The market doesn’t believe the Fed: There’s a huge gap between what the Fed has said it will do and what the market thinks the Fed will do. Time will tell who is correct, but this mistrust is troublesome for the Fed either way.

The gap between what the #FederalReserve intends to do (at least a couple of weeks ago) and what markets expect the Fed to do is, again,

HUGE!! pic.twitter.com/AvwX2tCylK— jeroen blokland (@jsblokland) April 5, 2023

Gold surpasses US$2,000/oz t: This week, gold broke the US$2,000 mark for the first time since August 2020. The market seems to expect continued uncertainty.

Gold has broken out above $2,000 👀

The all time high was $2,075 / oz in August 2020, ~18 months before global Central Bank balance sheets peaked.

Gold is sniffing out the next wave of fiat debasement. pic.twitter.com/UNkLCPHBEz

— Stack Hodler (@stackhodler) April 4, 2023

Central banks seem to like gold again: under Bretton Woods, the US$ was pegged to gold. After that, US Treasuries became the preferred central bank asset. Now, we seem to be back to gold.

3 monetary systems on one chart:

1946-68: USD is GRC, gold pegged to USD is primary global reserve asset.

1971-2009: USD is GRC, USTs are primary global reserve asset.

2014-present: USD is GRC, gold floating in all fiat currencies (based on BoP) is primary global reserve asset pic.twitter.com/HDx500b3sN

— Luke Gromen (@LukeGromen) April 4, 2023

Surprise oil production cuts: Many members of the OPEC+ oil cartel announced production cuts, which pushed WTI oil up to around US$80/bbl. This could make it more costly for the US to refill its strategic petroleum reserve (SPR) or make the US deplete it further.

OPEC and non-OPEC members announce oil production cuts that total more than 1.6 million barrels per day. Thoughts on second and third order consequences? pic.twitter.com/ld2tQfeirG

— kanekoa.substack.com (@KanekoaTheGreat) April 2, 2023

War is also business (unfortunately): Holger highlights Germany’s share. But it’s more interesting (and unsurprising) to note that the US accounts for almost half of global arms exports.

Good Morning from #Germany where business is booming for defense contractors. The German arms industry is a prime beneficiary of global rearmament. Germany ranked sixth in arms exports in 2022, trailing the US, France, Russia, China, and Italy. https://t.co/2OLCQNb6pD pic.twitter.com/zWKtJehsRz

— Holger Zschaepitz (@Schuldensuehner) April 5, 2023

Join the world’s toughest valuation training

Become a Valuation Expert. Valuation Master Class Boot Camp graduates can confidently value any company in the world and possess in-demand industry skills.

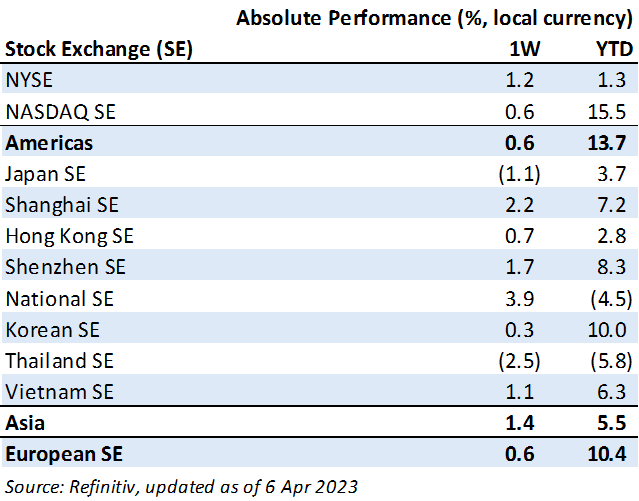

Weekly market performance

Click here to see more markets and periods.

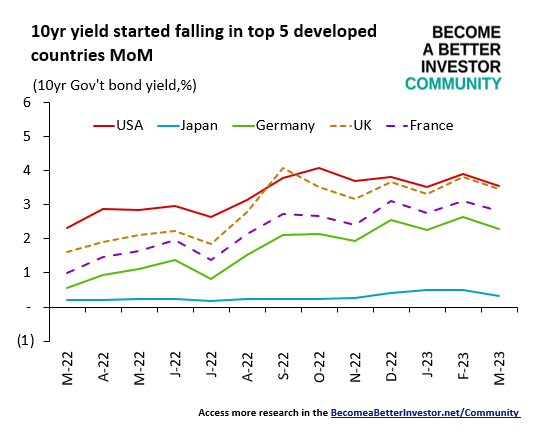

Chart of the week

Discussed in the Become a Better Investor Community this week

“Gold >$2,000”

“Peter Schiff will be partying tonight!!”

Try 1 month of the Become a Better Investor Community for FREE today!

You can cancel at any time. Click here to learn more.

Podcasts we listened to this week

The Morgan Housel Podcast – Getting Rich vs. Staying Rich

“Getting rich and staying rich are two different skills. They are often conflicting skills, so many people focus on one or the other. But you need both to do well over time.”

Readings this week

The Seven Virtues of Great Investors

“Last year, in my Wall Street Journal newsletter (and in my columns), I wrote a series about the essential attributes that all great investors seem to share.”

Is a Naive 1/N Diversification Strategy Efficient?

“The problem is that traditional portfolios are dominated by a single risk, or factor: the market factor. As the following example (using “risk points”) demonstrates, a traditional 60/40 portfolio, one that invests in total market funds, has much more than 60% of its risk in the market factor. That’s because stocks are much riskier (more volatile) than bonds.”

Book recommendation

The Ape that Understood the Universe: How the Mind and Culture Evolve by Steve Stewart-Williams

“It opens with a question: How would an alien scientist view our species? What would it make of our sex differences, our sexual behavior, our altruistic tendencies, and our culture? The book tackles these issues by drawing on two major schools of thought: evolutionary psychology and cultural evolutionary theory.”

Get the book on Audible or Kindle.

Audible is great; have you tried it? If not, click here to get 2 books for free.

Memes of the week

— Not Jerome Powell (@alifarhat79) April 5, 2023

Introducing Forbes 30 Under Arrest pic.twitter.com/aPJAl04Q3i

— tweet davidson 🍞 (@andykreed) April 5, 2023

New My Worst Investment Ever episodes

ISMS 17: Larry Swedroe – Do You Project Recent Trends Indefinitely Into the Future?

In this episode of Investment Strategy Made Simple (ISMS), Andrew and Larry discuss a chapter of Larry’s book Investment Mistakes Even Smart Investors Make and How to Avoid Them. In this second episode of the series, they talk about mistake number two: Do you project recent trends indefinitely into the future?

LEARNING: Hyper-diversify and rebalance your portfolio.

Access the episode’s show notes and resources

ISMS 16: Top 5 EM Country Interest Rates – Normal China Yield Curve

Emerging Countries – China and Russia with stable rates, LT rates up only slightly, yield curve inversion less severe except Russia

- India, Korea, and Brazil raised ST rates significantly; China and Russia were stable

- LT rates are up slightly in all EM countries but increased less than World

- Brazil and Korea saw yield curve inversion recently, Russia remains worst

Download the PDF with all charts and graphs

Access the episode’s show notes and resources

ISMS 15: Top 5 DM Country Interest Rates – Steep US Inversion

Developed Countries – Vast DM Country increases in ST and LT rates, Japan stays an outlier, US looks worst based on yield curve inversion

- Aggressive ST rate hikes led by the US and followed by European developed countries

- LT rates seem to have peaked and fell MoM

- Japan with different policy sees almost no movements in both ST and LT rates

- US faced steepest inversion among developed countries; Japan maintains positive yield curve

Download the PDF with all charts and graphs

Access the episode’s show notes and resources

ISMS 14: Regional Interest Rates – Low in Asia, Egypt and Frontiers on Fire

Developed Market Regions – ST rates about to peak, LT rates are falling, inverted yield curve in DM Americas and Europe widened

- ST rates in DM Americas and Europe risen more aggressively than World, DM Pacific much slower

- Small increases in LT rate in all DM regions YoY, but fell MoM

- DM Pacific maintains a positive yield curve while inversion worsened in DM Americas and Europe

Emerging Market Regions – Massive ST rate hikes in ME&A and Frontier, LT rates more stable, no yield curve inversion in Asia

- ST rates exploded in ME&A and Frontier, EM Asia and Europe were more cautious in raising ST rates

- LT rates of all EM regions rose and remained above World; only EM Europe saw falling yield YoY

- Asia remains the sole EM region with no yield curve inversion, inversion looks painful for EM Europe, ME&A, and Frontier

Download the PDF with all charts and graphs

Access the episode’s show notes and resources

ISMS 13: Global Interest Rates – Hikes Slow, Inversion Signals Recession

World – End of DM ST rate rise, inverted yield curves remain, high rates in EM

- High ST global and EM rates, yield curve inversion

- ST rates up massively YoY, small increase in LT rates

- ST rate rise stopped in DM, DM LT rates fell MoM

- Yield curve inversion steepened, especially in EM

Download the PDF with all charts and graphs

Access the episode’s show notes and resources

Ep669: Peter Ricchiuti – Don’t Fall in Love With a Stock

BIO: Peter Ricchiuti is a graduate of Babson College and began his career with the investment firm Kidder Peabody in Boston. He later managed Louisiana’s $3 billion investment portfolio while serving as the assistant state treasurer.

STORY: Peter made the mistake of falling in love with a particular stock and hyped it to his clients. The company had no moat and couldn’t stand the competition. Peter’s reputation was severely affected after the stock price fell significantly.

LEARNING: Don’t fall in love with a stock. Diversification is key.

Access the episode’s show notes and resources

Ep668: Jason Hsu – The Market Can Be Crazy for Longer than You Have the Conviction

BIO: Jason Hsu is the founder, chairman, and CIO of Rayliant Global Advisors (RGA), a global investment management group with over US$15+ billion in assets managed using its strategies as of June 30, 2022.

STORY: Jason bet against the GameStop short squeeze and learned that John Maynard Keyens’ saying that “markets can remain irrational longer than you can remain solvent” still holds true.

LEARNING: The market can be crazy for longer than you have the conviction to stay invested. Apply position constraints and diversify.

Access the episode’s show notes and resources

Ep667: Shreekkanth Viswanathan – Qualitative Strengths of a Company Matter Too

BIO: Shreekkanth (“Shree”) Viswanathan is the founder and portfolio manager of SVN Capital, a Chicago-based, concentrated, long-only, global equity-focused fund.

STORY: Shree’s biggest mistake is an error of omission. That is, after studying a particular business, he decided not to invest in it for various reasons. The stock turned out to be a multi-bagger a couple of years later.

LEARNING: The qualitative strengths of a company are not always readily apparent in the financials. Get out and work in business; it will make you a better analyst and investor.

Access the episode’s show notes and resources

Published on Become a Better Investor this week

Are tests like the SAT – and a potential National Merit Scholarship that goes with a good score – the same as grading or ranking students? David and Andrew discuss the differences.

WICE Logistics Public Company Limited (WICE TB): Profitable Growth rank of 1 was same compared to the prior period’s 1st rank. This is World Class performance compared to 1,390 medium Industrials companies worldwide.

Read WICE Logistics – World Class Benchmarking

VGI Public Company Limited (VGI TB): Profitable Growth rank of 9 was same compared to the prior period’s 9th rank. This is poor performance compared to 260 medium Comm. Serv. companies worldwide.

Read VGI – World Class Benchmarking

Berli Jucker Public Company Limited (BJC TB): Profitable Growth rank of 8 was up compared to the prior period’s 9th rank. This is below average performance compared to 640 large Cons. Staples companies worldwide.

Read Berli Jucker – World Class Benchmarking

In March 2023, we published 20 new episodes of the My Worst Investment Ever podcast. Listen to all of them here.

Listen to My Worst Investment Ever March 2023

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.