A. Stotz All Weather Strategies – December 2023

The All Weather Strategy is available in Thailand through FINNOMENA. If you’re interested in our allocation strategy, you can also join the Become a Better Investor Community. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

What happened in world markets in December 2023

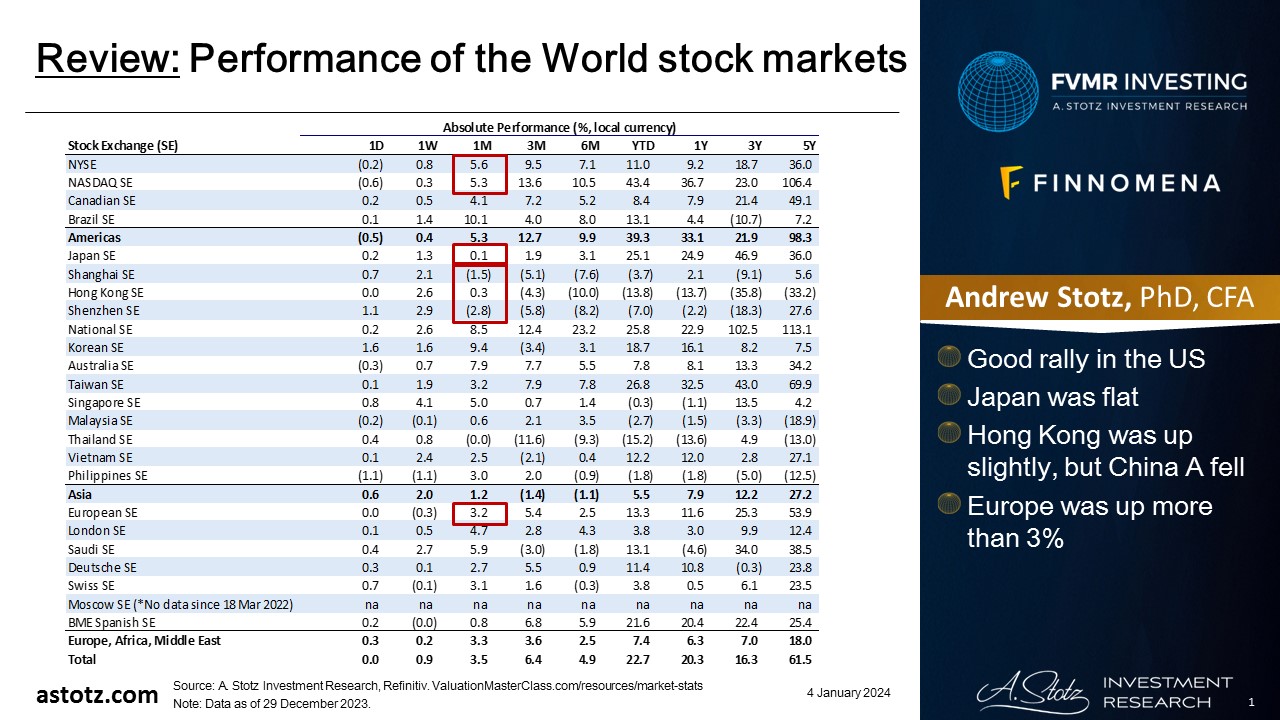

Performance of the World stock markets

- Good rally in the US

- Japan was flat

- Hong Kong was up slightly, but China A fell

- Europe was up more than 3%

Find the updated Performance of the World stock markets here.

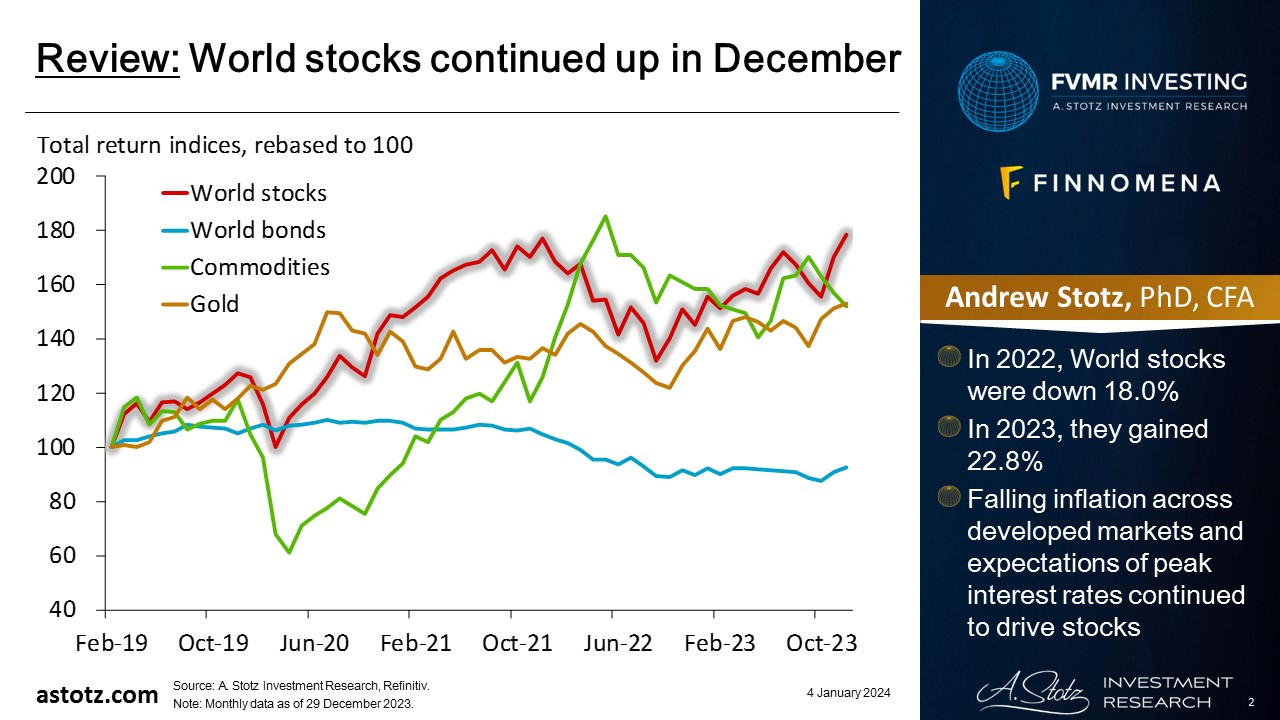

World stocks continued up in December

- In 2022, World stocks were down 18.0%

- In 2023, they gained 22.8%

- Falling inflation across developed markets and expectations of peak interest rates continued to drive stocks

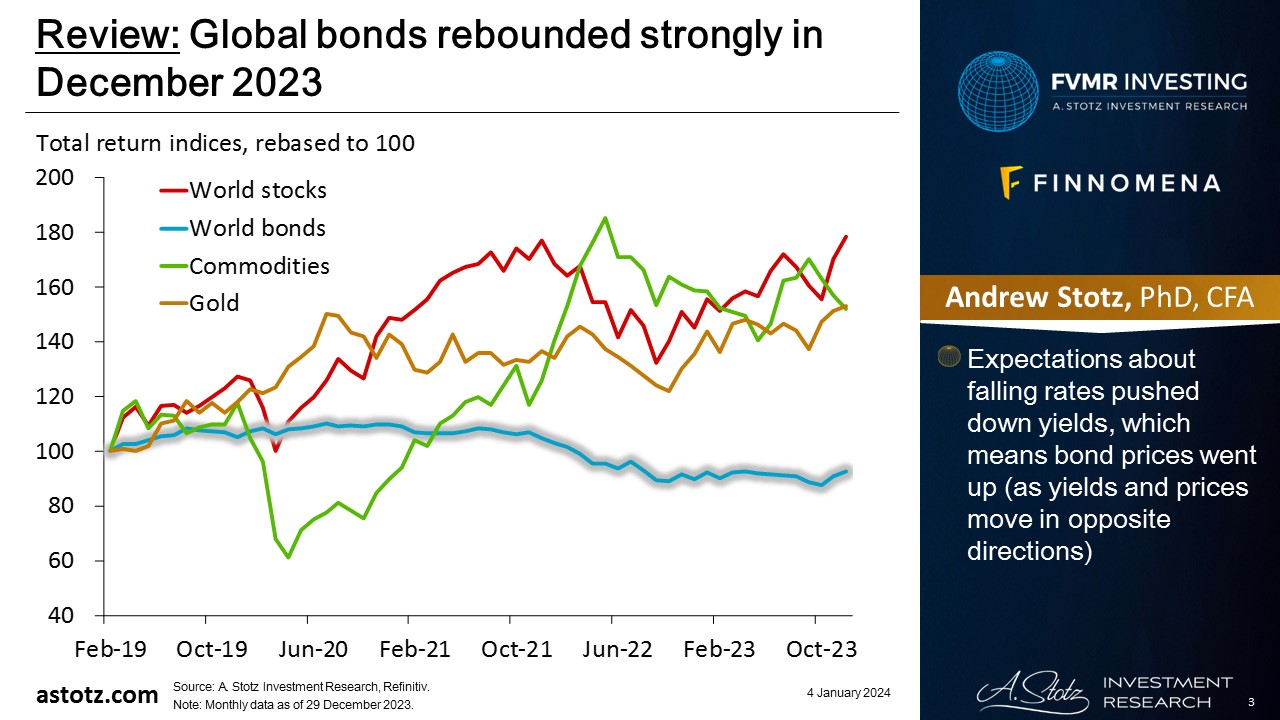

Global bonds rebounded strongly in December 2023

- Expectations about falling rates pushed down yields, which means bond prices went up (as yields and prices move in opposite directions)

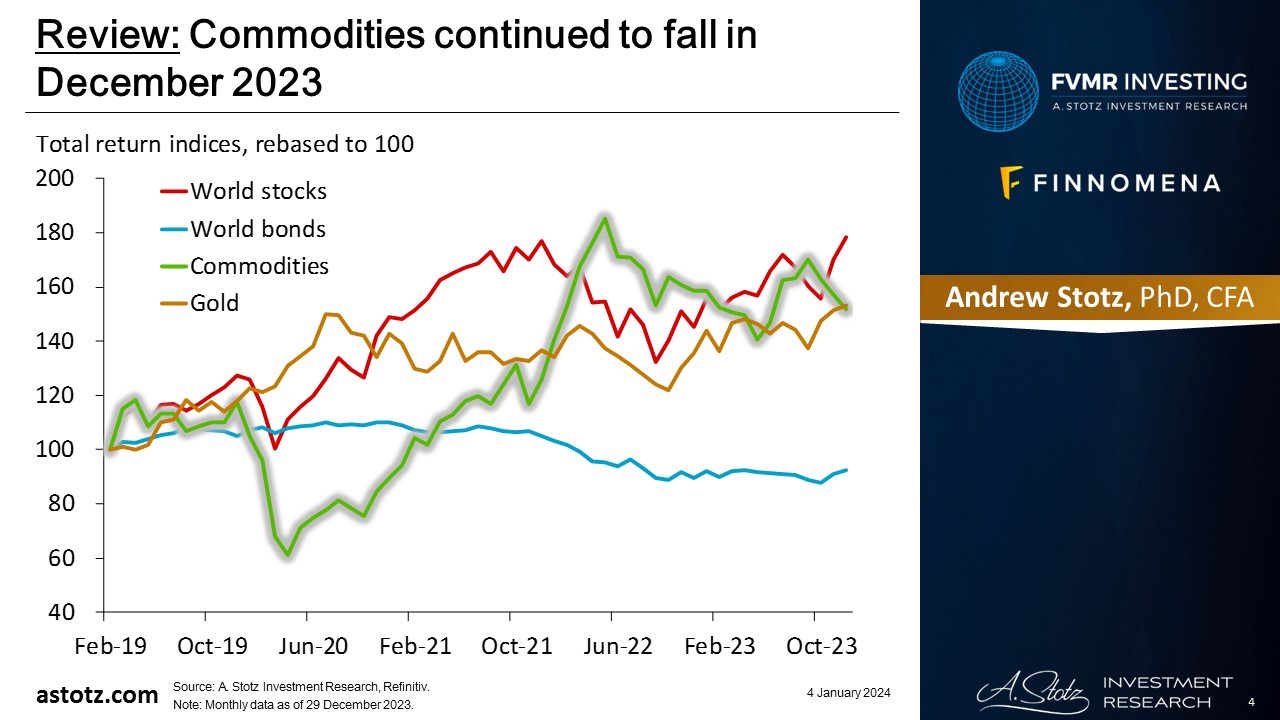

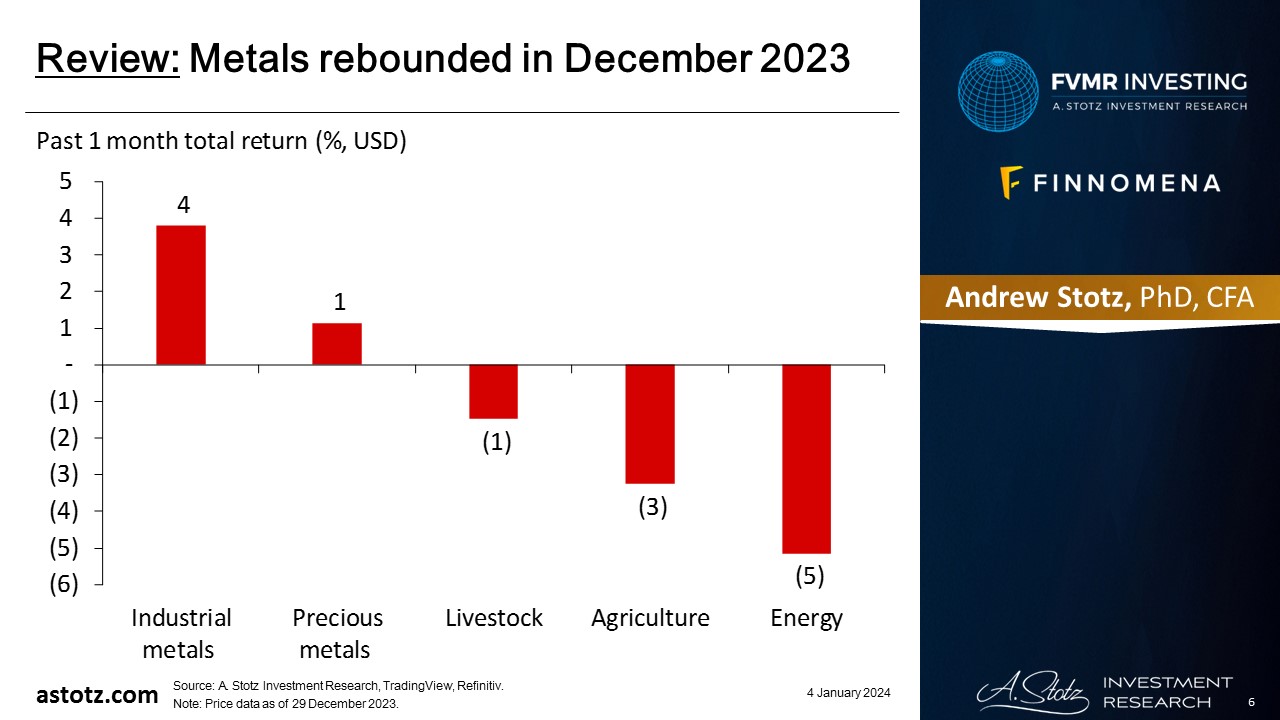

Commodities continued to fall in December 2023

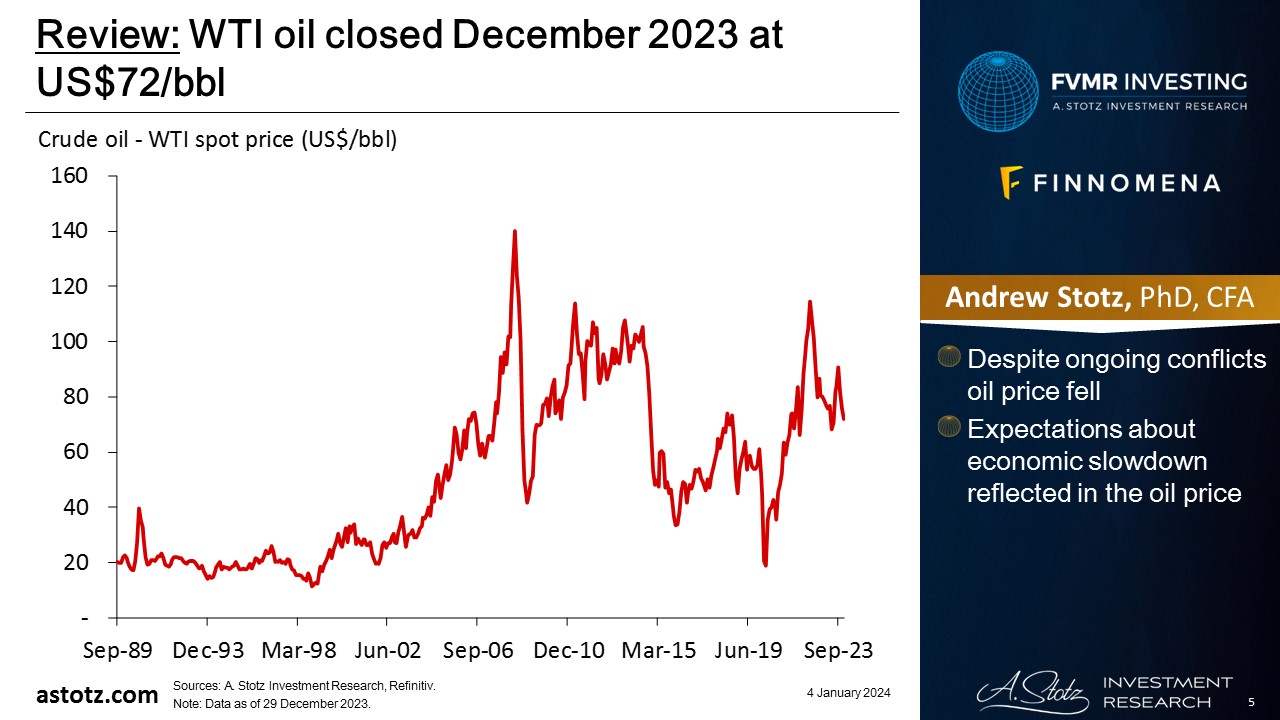

WTI oil closed December 2023 at US$72/bbl

- Despite ongoing conflicts oil price fell

- Expectations about economic slowdown reflected in the oil price

Metals rebounded in December 2023

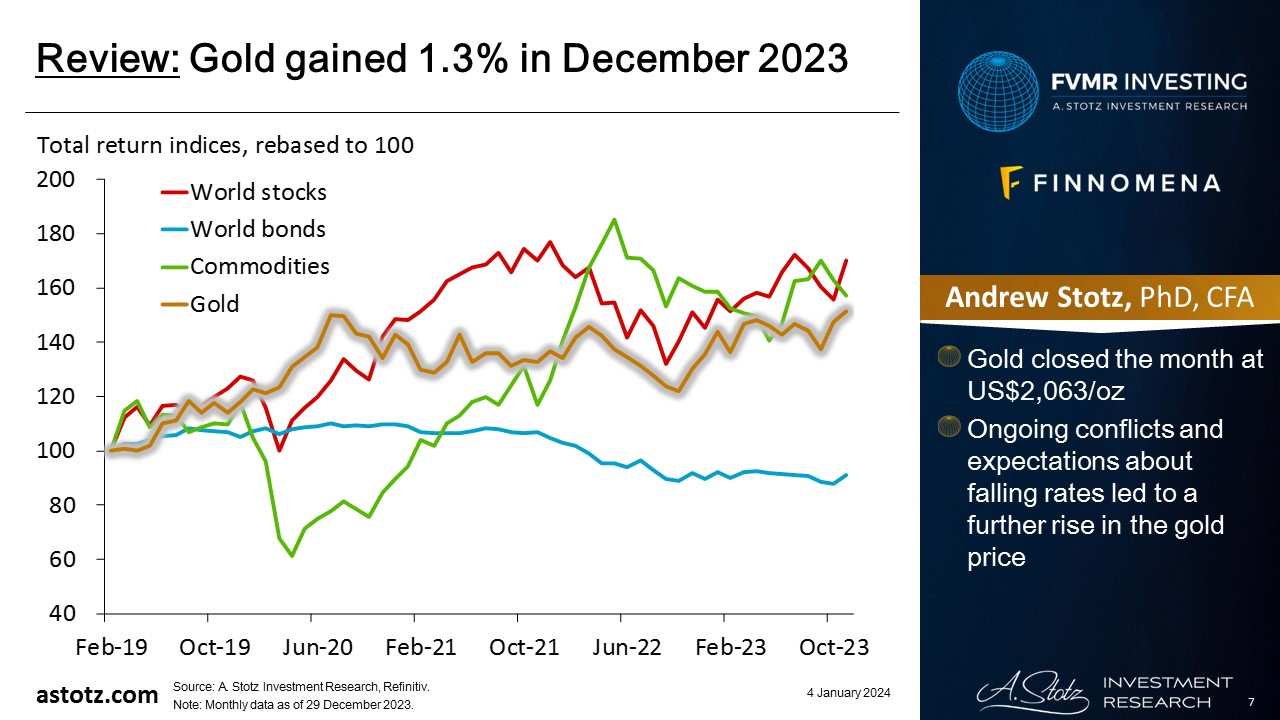

Gold gained 1.3% in December 2023

- Gold closed the month at US$2,063/oz

- Ongoing conflicts and expectations about falling rates led to a further rise in the gold price

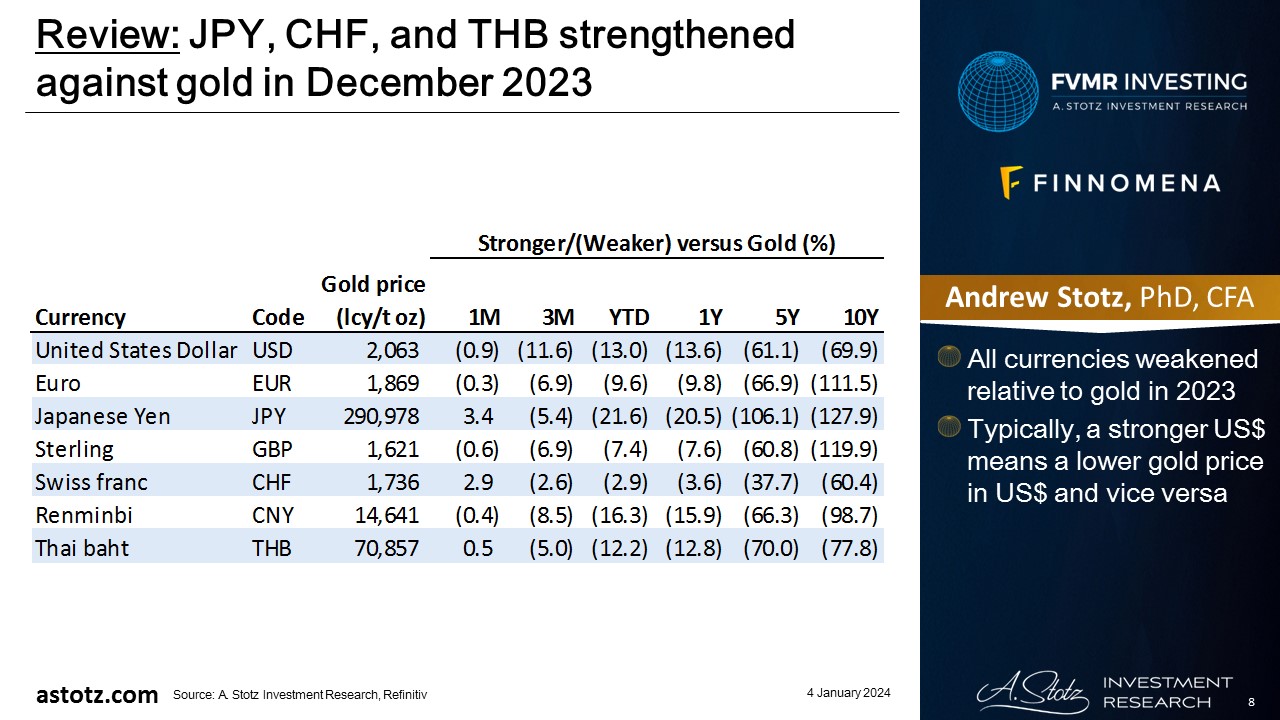

JPY, CHF, and THB strengthened against gold in December 2023

- All currencies weakened relative to gold in 2023

- Typically, a stronger US$ means a lower gold price in US$ and vice versa

US CPI fell to 3.1% YoY in November

Overall US CPI moved down to 3.1% YoY in November from 3.2% in October. Lowest since June.

US Core CPI (ex-Food/Energy) moved down to 4.0% YoY, the lowest core inflation reading since September 2021. pic.twitter.com/nHEjKPAp02

— Charlie Bilello (@charliebilello) December 12, 2023

Fed left rates unchanged for 3rd straight meeting

SUMMARY OF FED DECISION (12/13/23):

1. Fed leaves rates unchanged for third straight meeting

2. Fed says growth of economy “has slowed” since Q3 2023

3. Most Fed officials see interest rate cuts in 2024

4. Median projection shows 3 rate cuts in 2024

5. Fed sees 4.1%…

— The Kobeissi Letter (@KobeissiLetter) December 13, 2023

US yield curve has been inverted for 400+ consecutive days – 2nd longest on record

The US Yield Curve (10-year minus 3-month) has now been inverted for 427 consecutive days, the 2nd longest streak in history. Will likely become the longest inversion ever in February 2024. pic.twitter.com/l1q7cVMwSx

— Charlie Bilello (@charliebilello) December 27, 2023

US stock valuations at crazy (?) levels

A good chart to reflect on a day like today.

US stocks have an exorbitant valuation compared to global equities.

Primarily propelled by technology firms, the current environment stands out as one of the most speculative periods for American stocks in history.

The next decade… pic.twitter.com/l9uosPJgAy

— Otavio (Tavi) Costa (@TaviCosta) December 11, 2023

Magnificent 7’s weight in the MSCI AC World Index is > Japan + France + China + UK

Mind-boggling fun fact…

Combined weighting of Magnificent Seven in MSCI All Country World Index is > *all* stocks from Japan, France, China, & UK.

via @hardikasingh28 pic.twitter.com/ETY4qxMnff

— Nate Geraci (@NateGeraci) December 17, 2023

Moody’s downgrades China’s credit outlook to negative

🇨🇳Moody’s Cuts China Credit Outlook to Negative on Rising Debt

Moody’s Investors Service cut its outlook for Chinese sovereign bonds to negative, underscoring deepening global concerns about the level of debt in the world’s second-largest economy.

Moody’s lowered its outlook… pic.twitter.com/zPJKGDreNE

— Tracy (𝒞𝒽𝒾 ) (@chigrl) December 5, 2023

Argentina’s new president initiated shock treatment by devaluing the Peso by 54%

⚠️BREAKING:

*ARGENTINA DEVALUES THE PESO BY 54%, LETTING IT FALL TO 800 PESOS/DOLLAR, AS PART OF PRESIDENT JAVIER MILEI’S SHOCK PROGRAM TO REVIVE THE ECONOMY

🇦🇷🇦🇷 pic.twitter.com/1Xq5i5tOVS

— Investing.com (@Investingcom) December 12, 2023

Gold hits new all-time high

⚠️BREAKING:

*GOLD RISES ABOVE $2,100/OZ TO HIT NEW ALL TIME HIGH AMID MIDDLE EAST TENSIONS$GC_F pic.twitter.com/EgndgGEnhu

— Investing.com (@Investingcom) December 3, 2023

- Gold traded as high as US$2,135/t oz, beating the previous record of US$2,072/t oz in August 2020

Key takeaways

- US CPI fell to 3.1% YoY in November

- Fed left rates unchanged for 3rd straight meeting

- US stock valuations at crazy (?) levels

- Moody’s downgrades China’s credit outlook to negative

- Gold hits new all-time high

Performance review: All Weather Inflation Guard

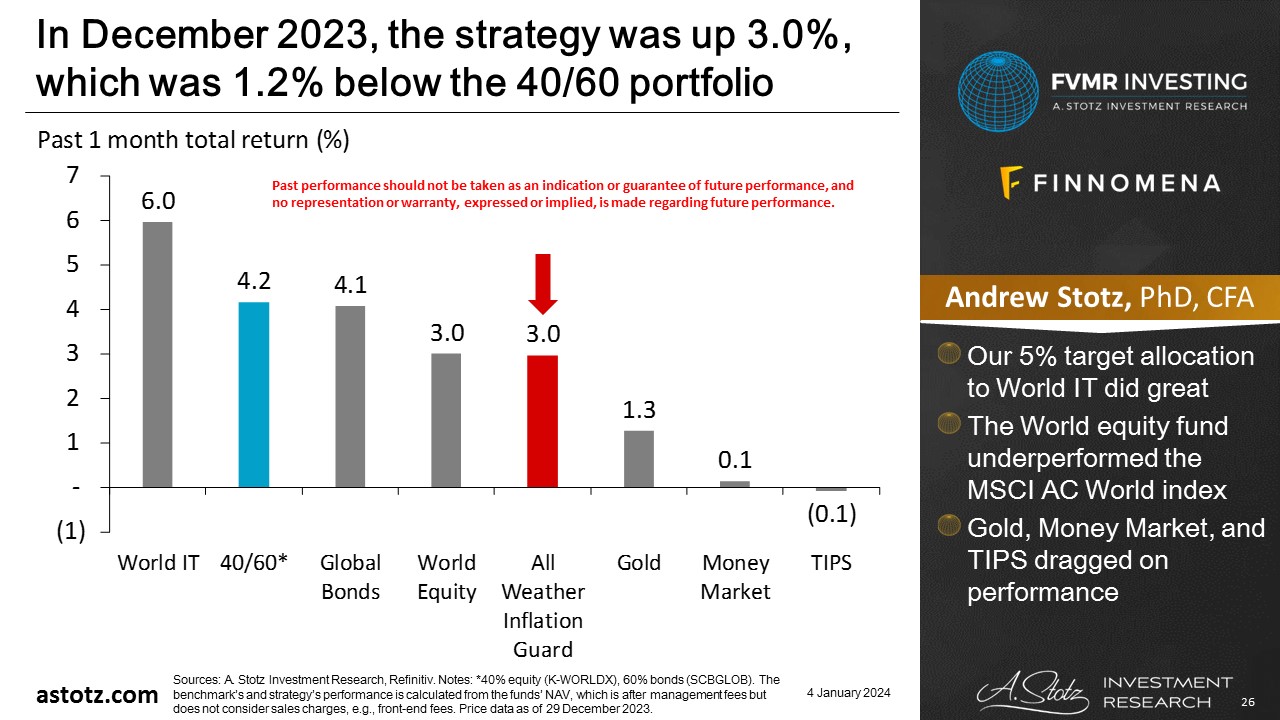

All Weather Inflation Guard gained 3.0%

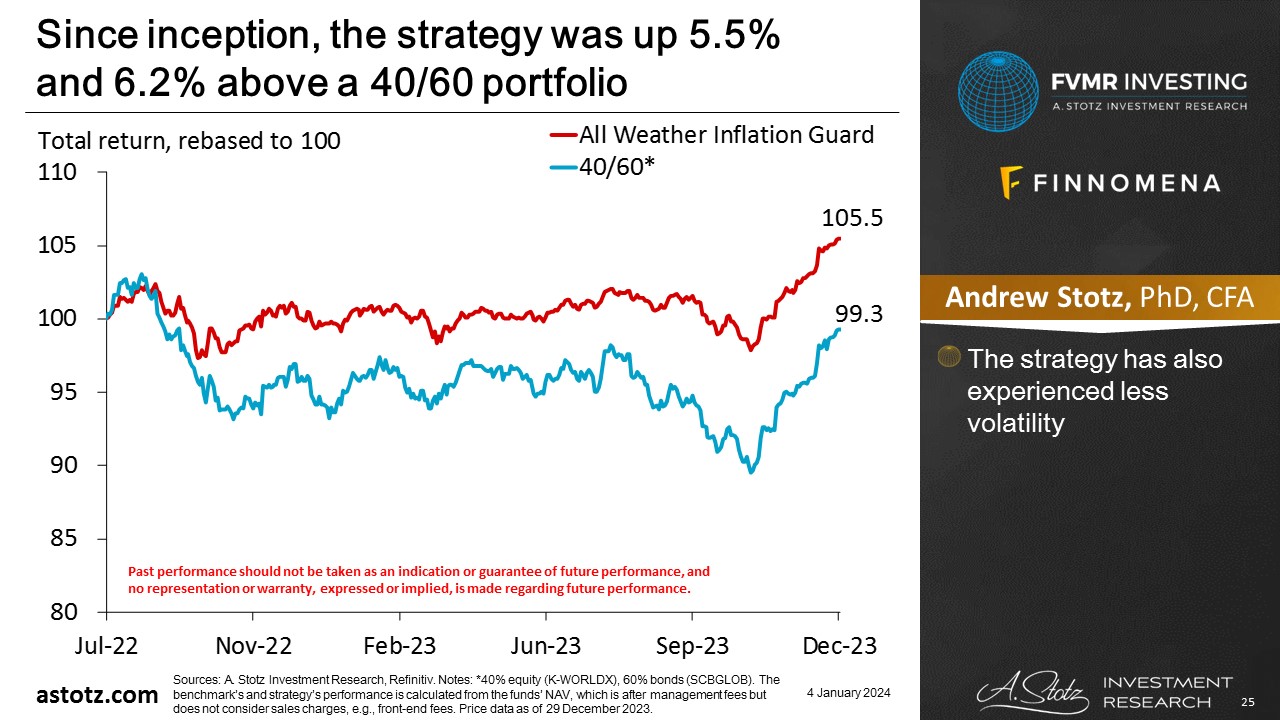

Since inception, the strategy was up 5.5% and 6.2% above a 40/60 portfolio

- The strategy has experienced less volatility

In December 2023, the strategy was up 3.0%, which was 1.2% below the 40/60 portfolio

- Our 5% target allocation to World IT did great

- The World equity fund underperformed the MSCI AC World index

- Gold, Money Market, and TIPS dragged on performance

Performance review: All Weather Strategy

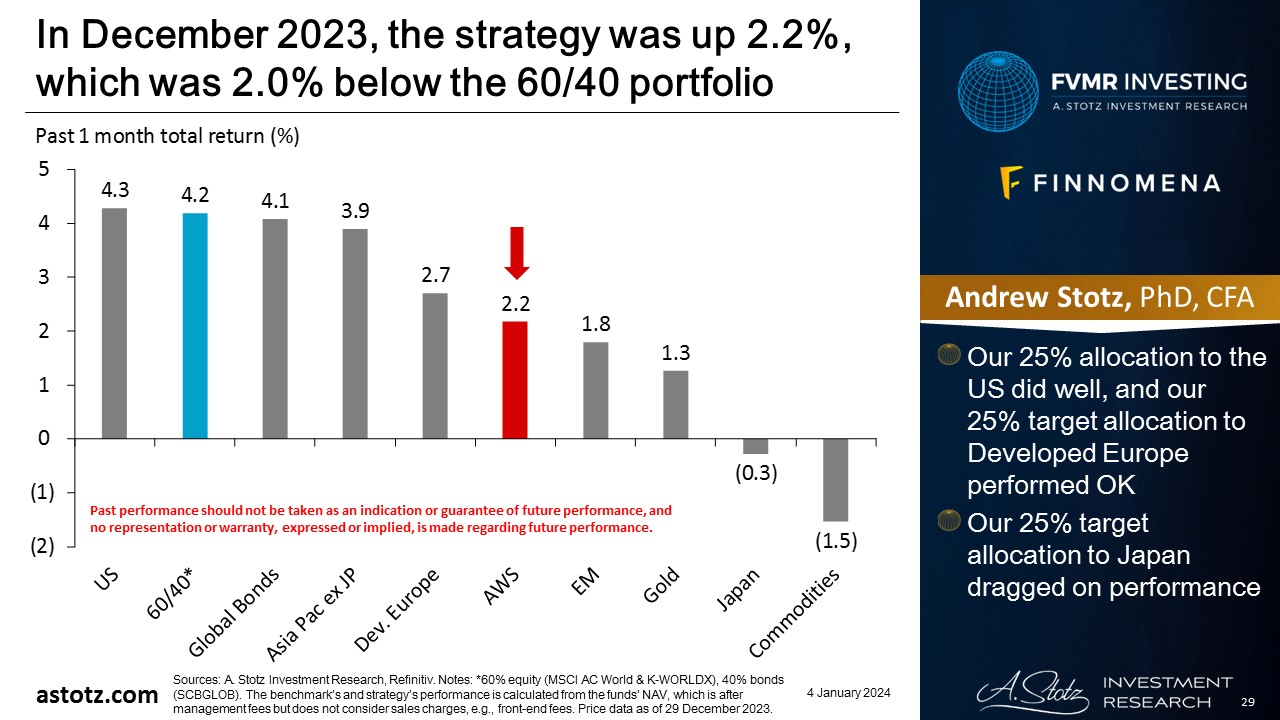

All Weather Strategy gained 2.2%

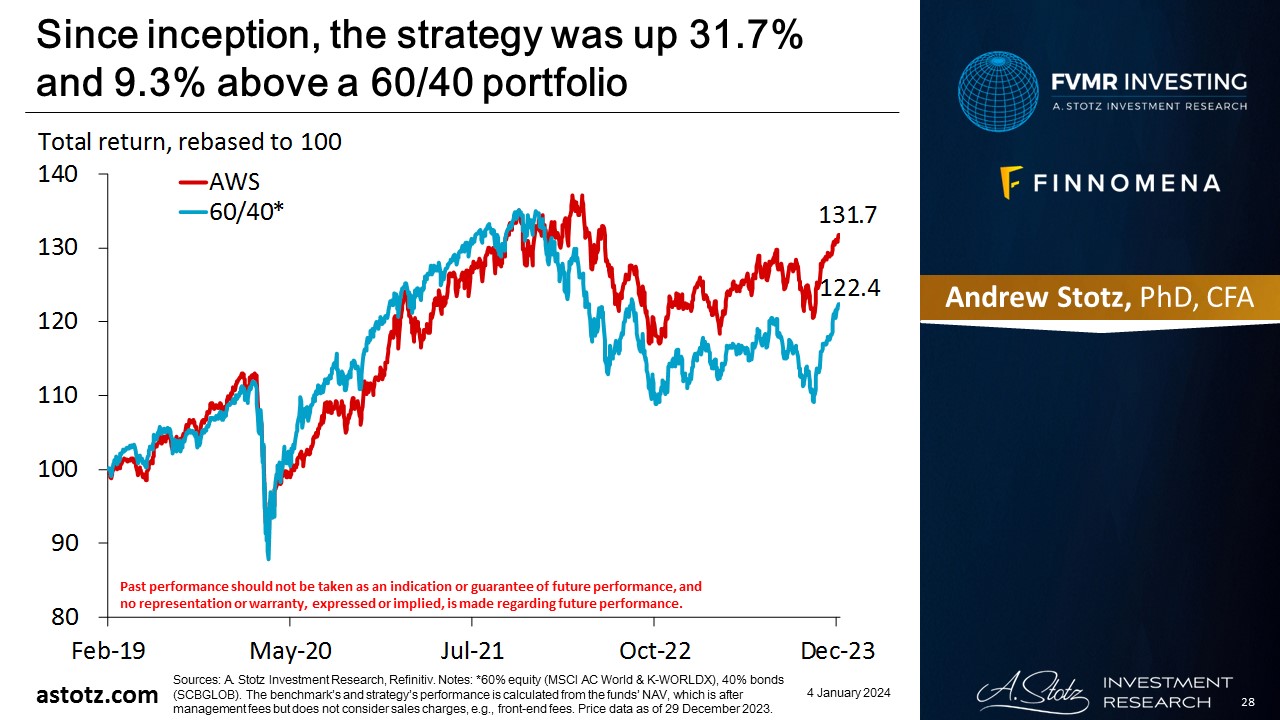

Since inception, the strategy was up 31.7% and 9.3% above a 60/40 portfolio

In December 2023, the strategy was up 2.2%, which was 2.0% below the 60/40 portfolio

- Our 25% allocation to the US did well, and our 25% target allocation to Developed Europe performed OK

- Our 25% target allocation to Japan dragged on performance

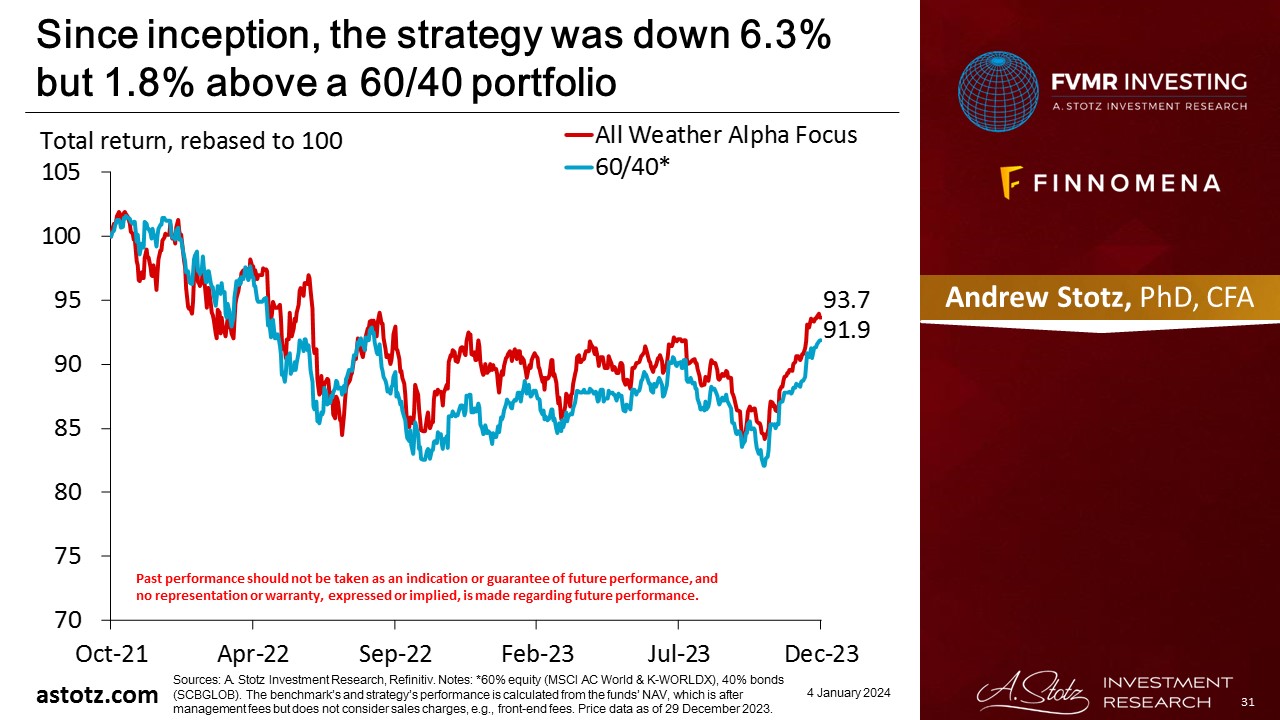

Performance review: All Weather Alpha Focus

All Weather Alpha Focus gained 3.9%

Since inception, the strategy was down 6.3% but 1.8% above a 60/40 portfolio

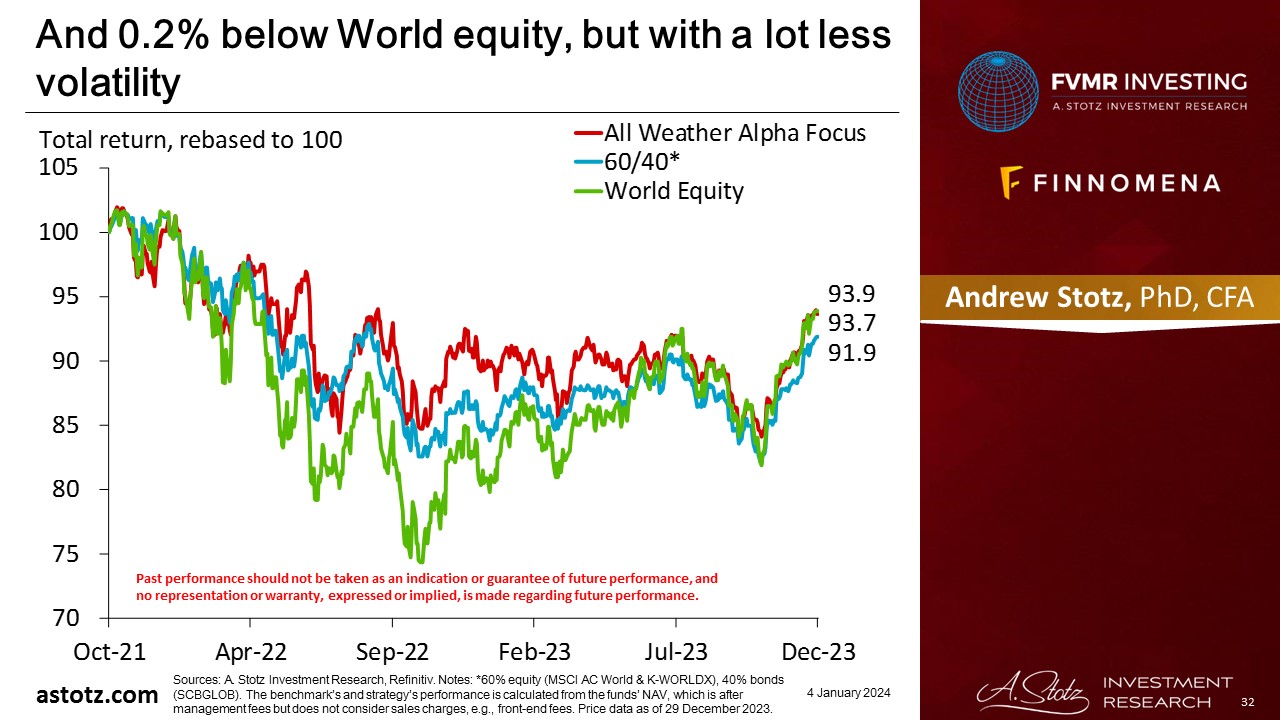

And 0.2% below World equity, but with a lot less volatility

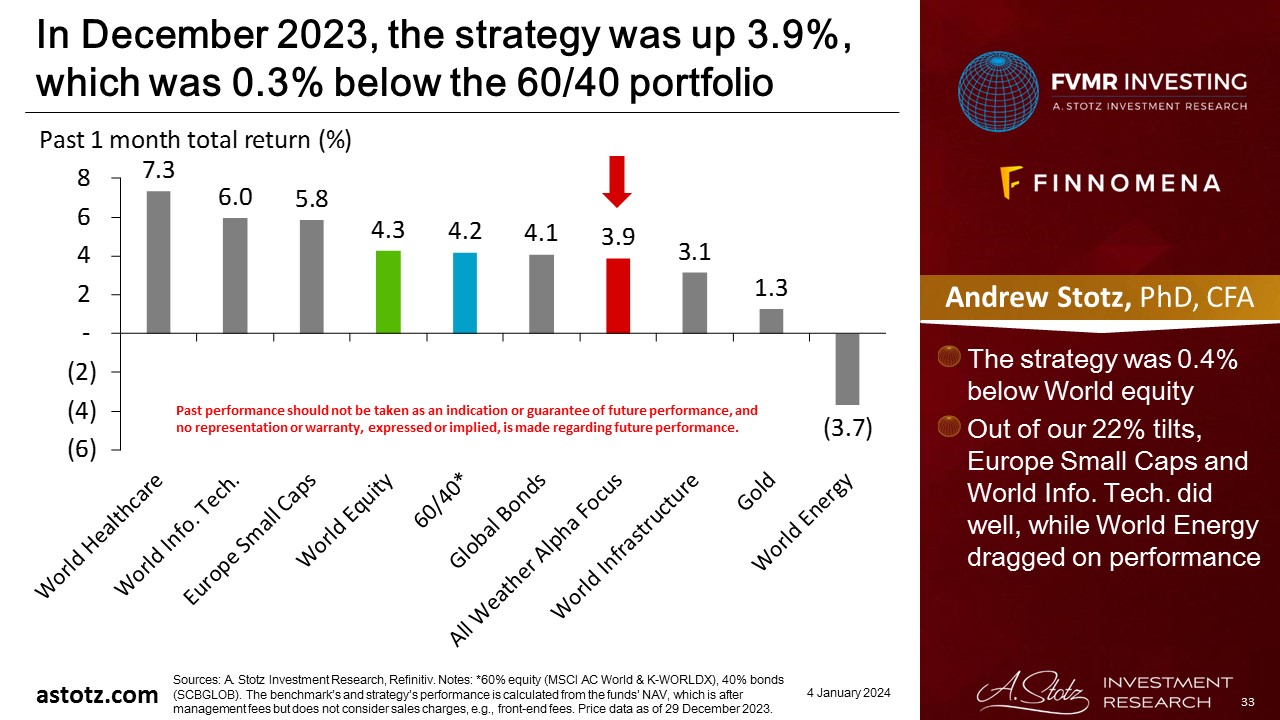

In December 2023, the strategy was up 3.9%, which was 0.3% below the 60/40 portfolio

- The strategy was 0.4% below World Equity

- Out of our 22% tilts, Europe Small Caps and World Info. Tech. did well, while World Energy dragged on performance

Global outlook that guides our asset allocation

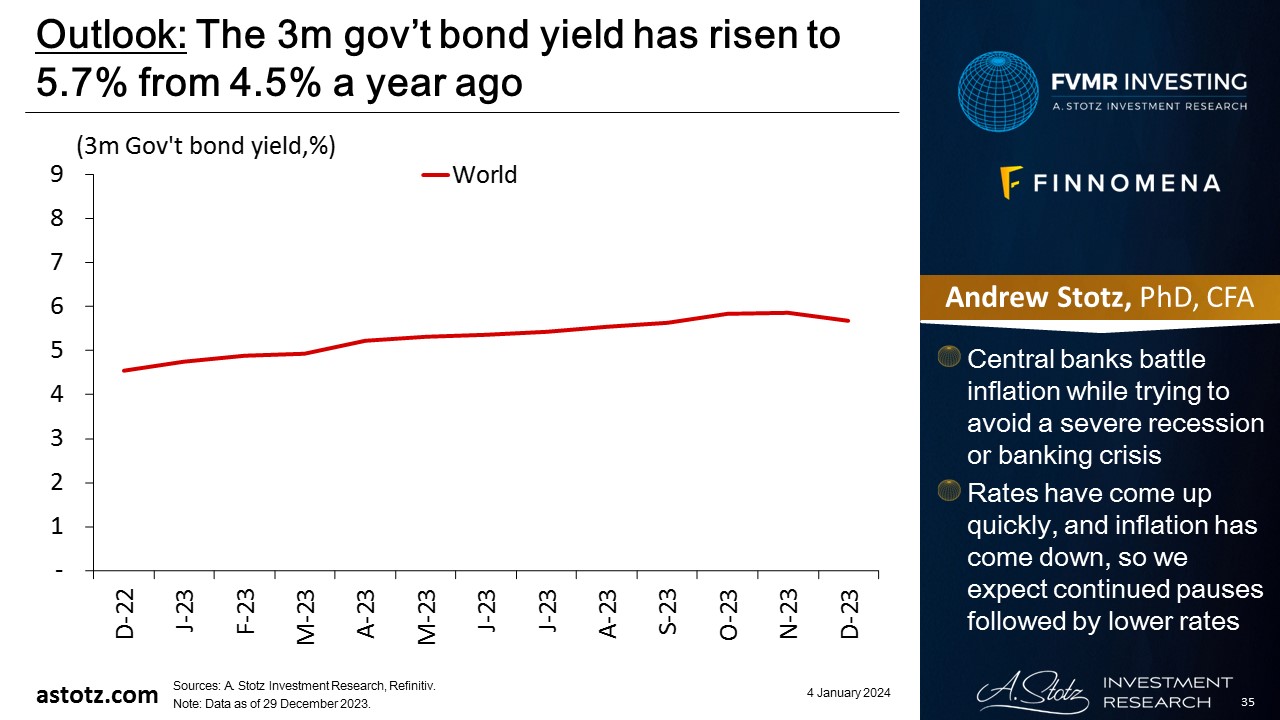

The 3m gov’t bond yield has risen to 5.7% from 4.5% a year ago

- Central banks battle inflation while trying to avoid a severe recession or banking crisis

- Rates have come up quickly, and inflation has come down, so we expect continued pauses followed by lower rates

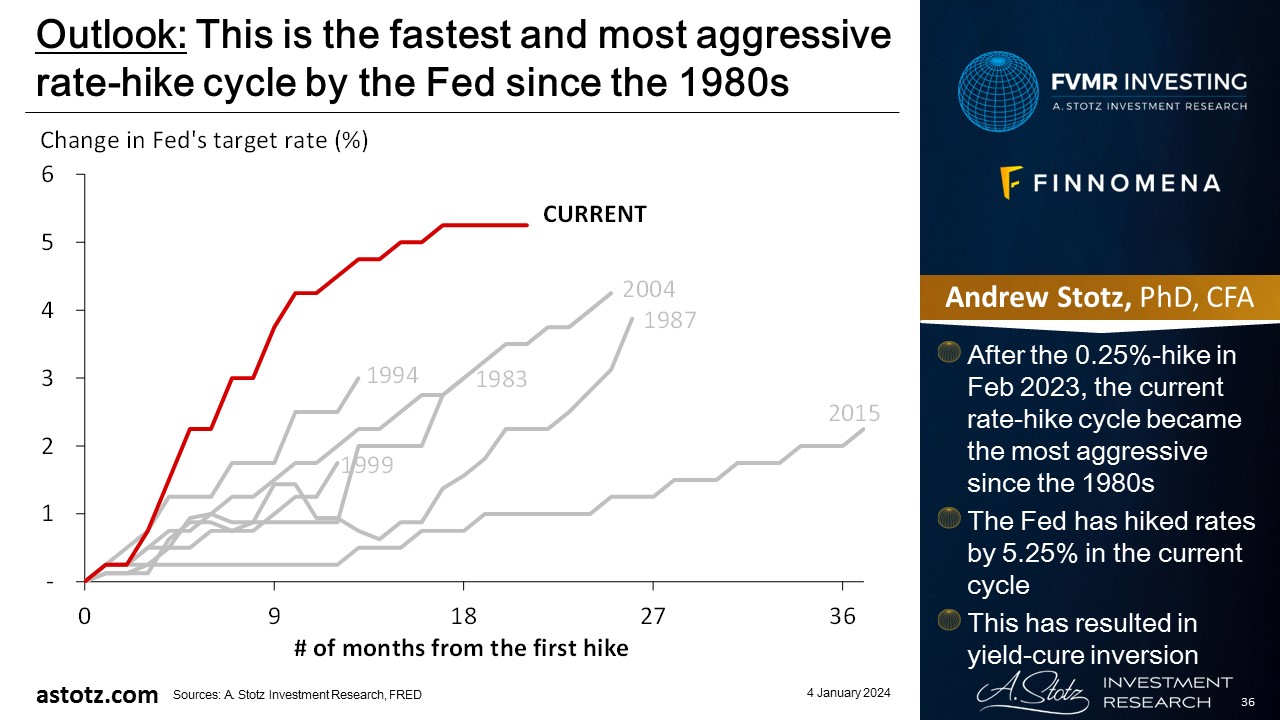

This is the fastest and most aggressive rate-hike cycle by the Fed since the 1980s

- After the 0.25%-hike in Feb 2023, the current rate-hike cycle became the most aggressive since the 1980s

- The Fed has hiked rates by 5.25% in the current cycle

- This has resulted in yield-cure inversion

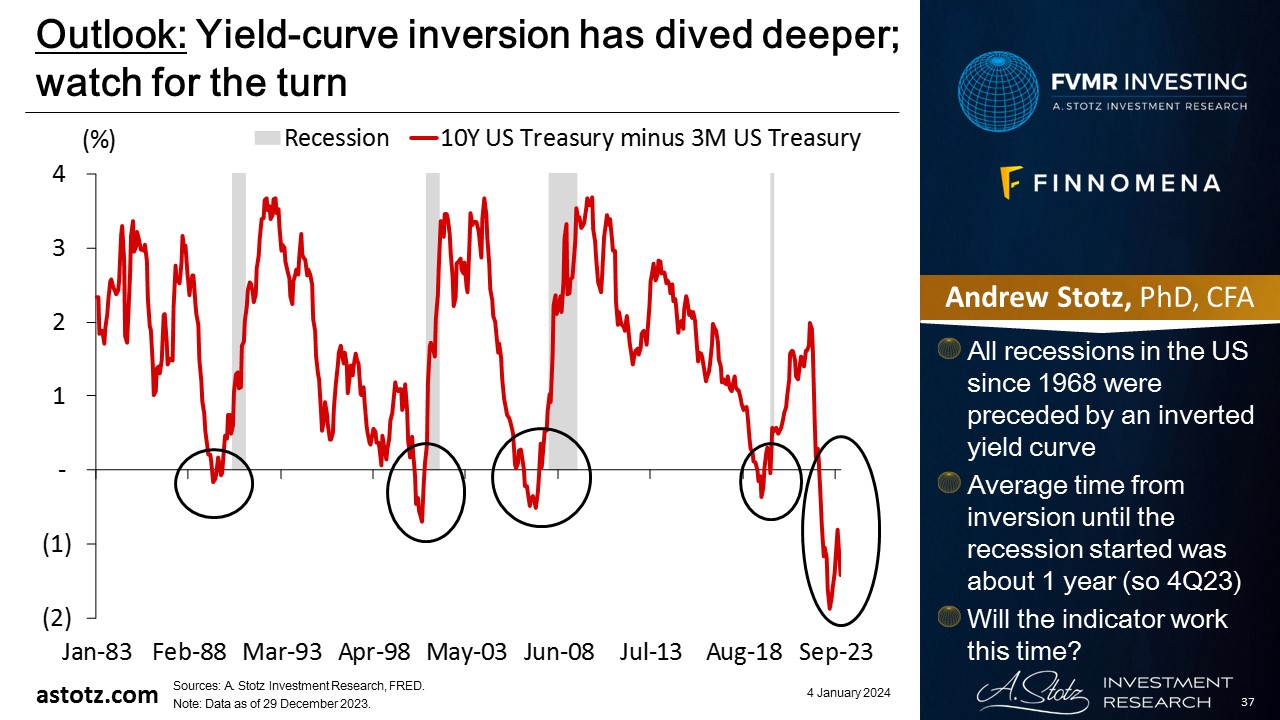

Yield-curve inversion has dived deeper; watch for the turn

- All recessions in the US since 1968 were preceded by an inverted yield curve

- Average time from inversion until the recession started was about 1 year (so 4Q23)

- Will the indicator work this time?

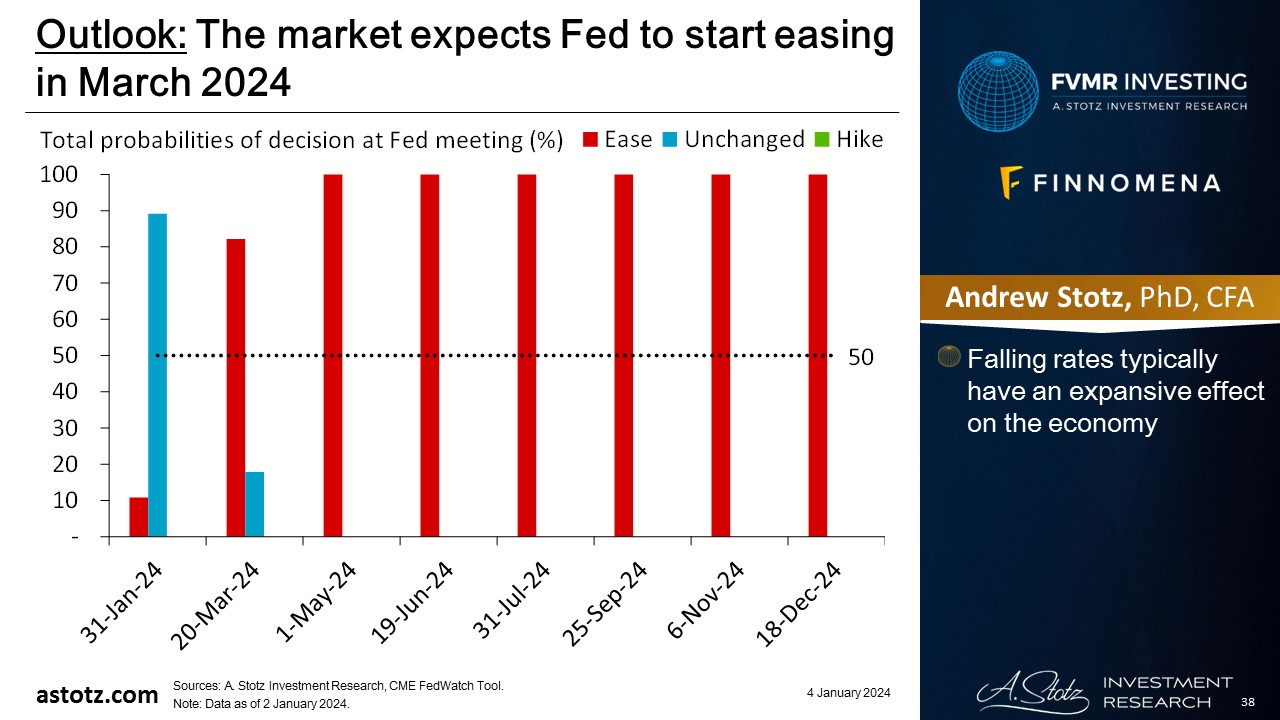

The market expects Fed to start easing in March 2024

- Falling rates typically have an expansive effect on the economy

For the past year, we’ve said that we think the course will eventually be reversed

- We still expect central banks will reverse course and return to accommodative policies as soon as something “breaks”

- The massive rise in rates will eventually break something

- When the news turns negative and markets and economies start weakening, we expect the Fed will reverse course and bring rates back to near zero

- This reversal could support equity

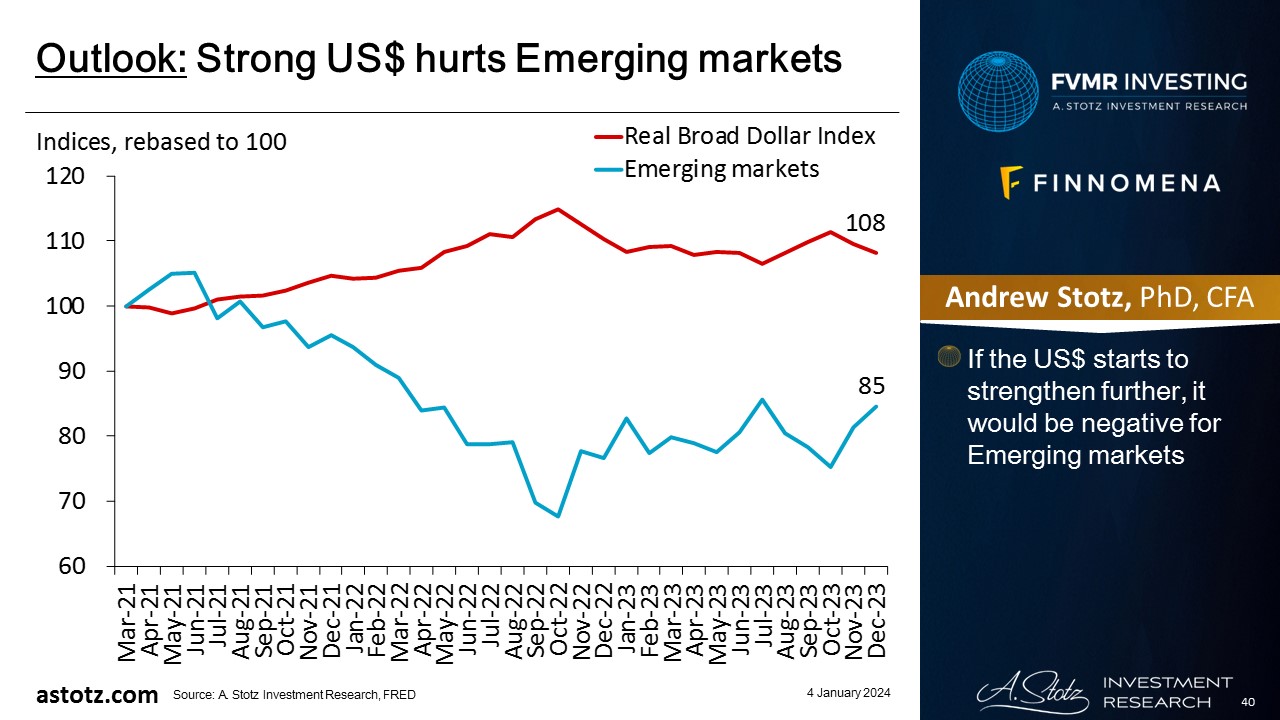

Strong US$ hurts Emerging markets

- If the US$ starts to strengthen further, it would be negative for Emerging markets

China is in trouble

- China continues with easier monetary and/or fiscal policy to stimulate the economy

- It’s unclear if the Chinese economy has bottomed yet

- Even with a strong recovery, Chinese stocks could underperform due to geopolitical risk

Bonds are typically a safe place to be

- In recessions, safer assets like government bonds typically have performed well

- Though with high inflation, low yields could still lead to negative real returns

- We generally don’t allocate to bonds to speculate on the upside but rather use it to protect capital over time

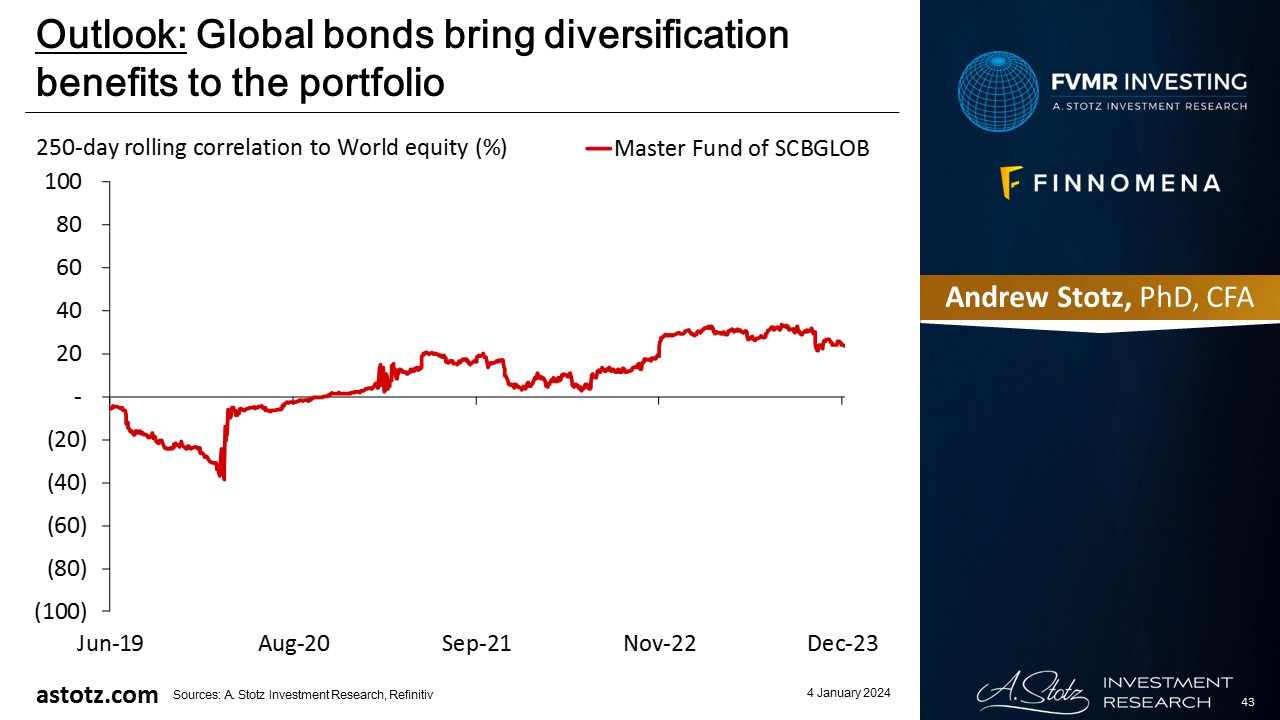

Global bonds bring diversification benefits to the portfolio

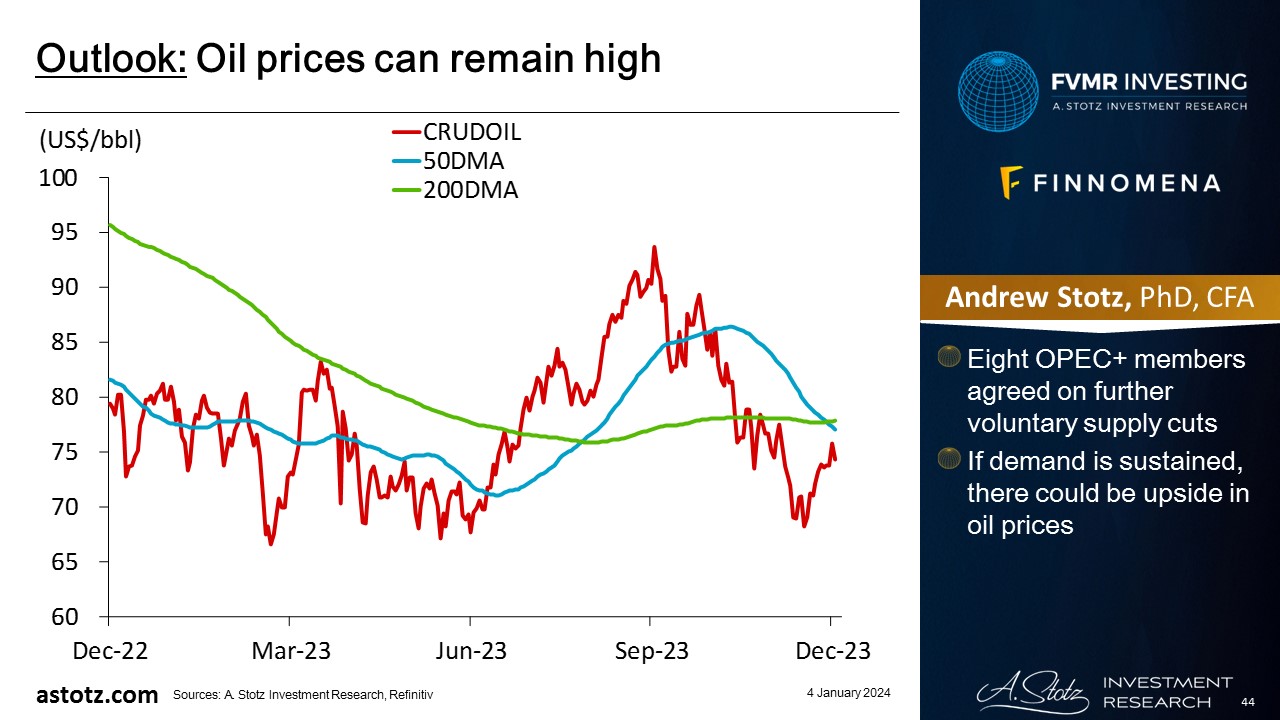

Oil prices can remain high

- Eight OPEC+ members agreed on further voluntary supply cuts

- If demand is sustained, there could be upside in oil prices

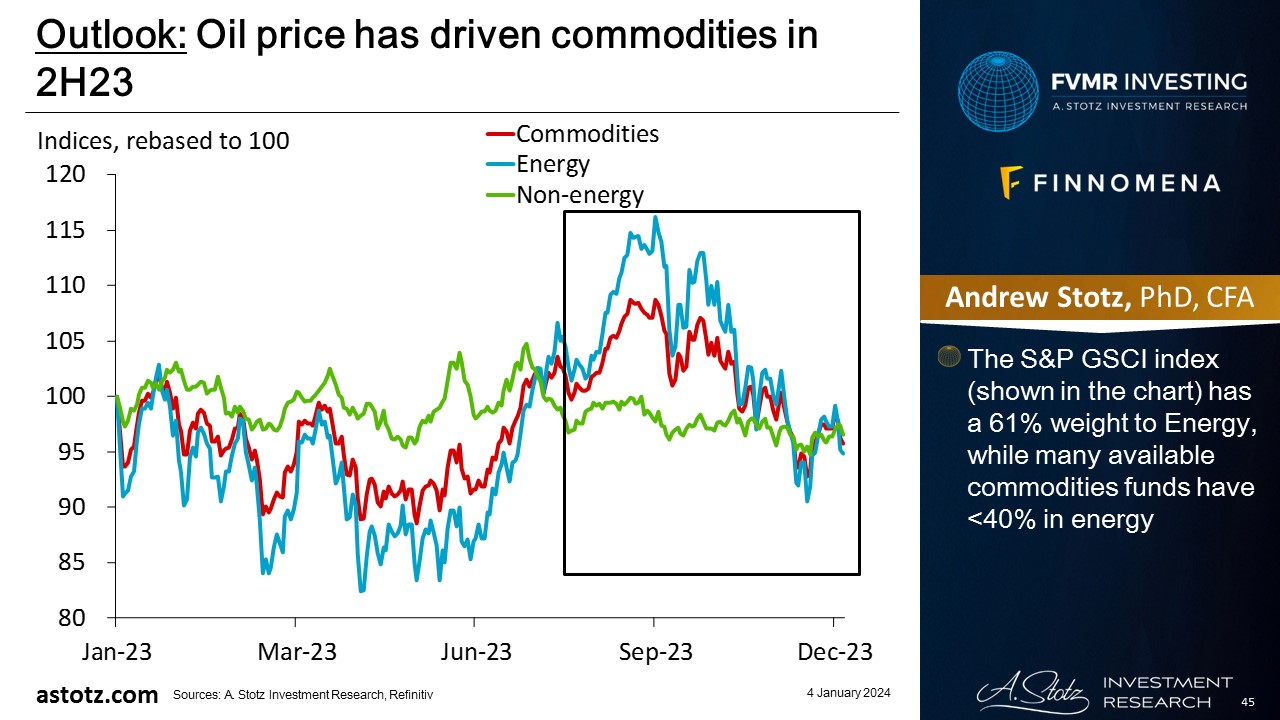

Oil price has driven commodities in 2H23

- The S&P GSCI index (shown in the chart) has a 61% weight to Energy, while many available commodities funds have <40% in energy

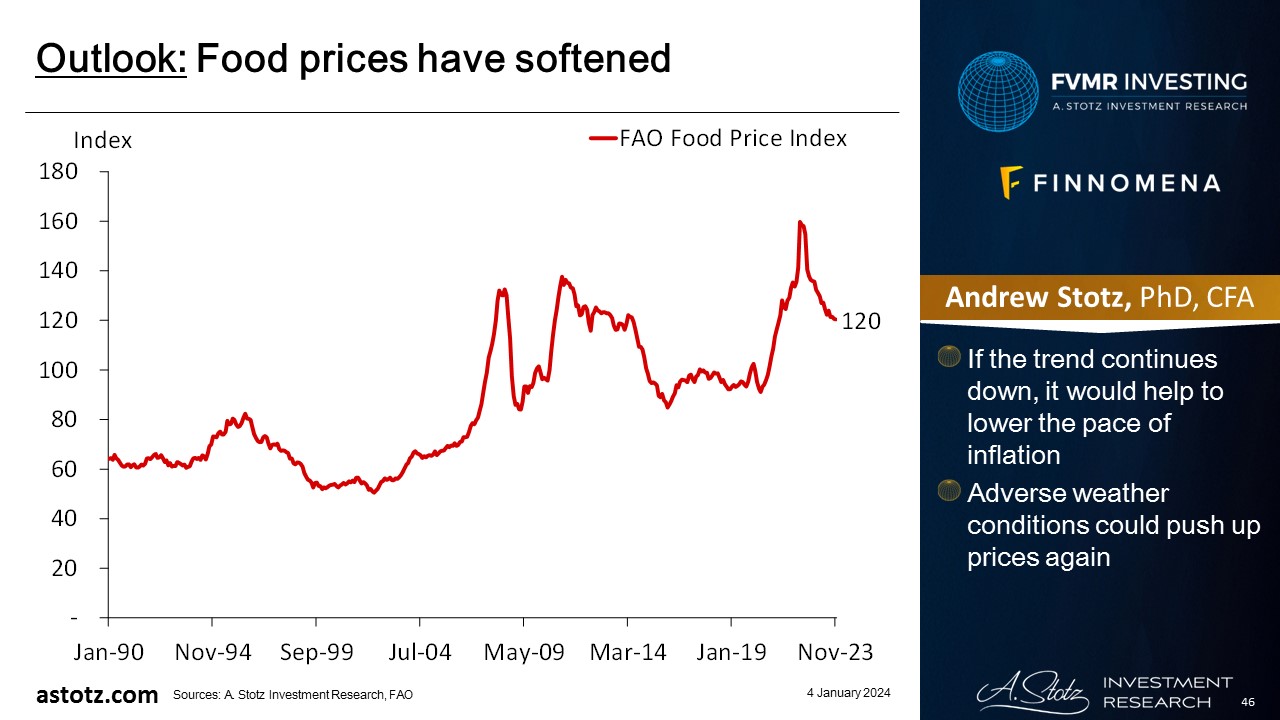

Food prices have softened

- If the trend continues down, it would help to lower the pace of inflation

- Adverse weather conditions could push up prices again

The global economic growth outlook remains uncertain

- The main upside in commodities would come from a supply shock, adverse weather conditions, or significantly higher demand due to an improved growth outlook

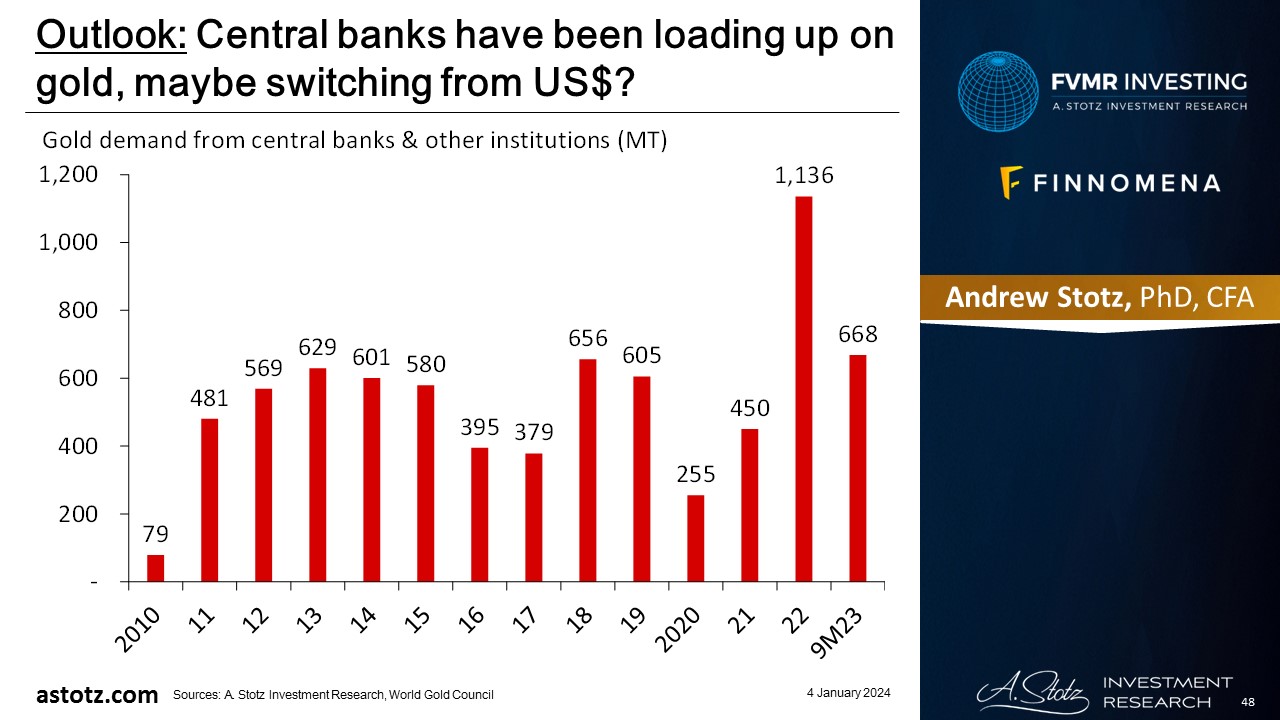

Central banks have been loading up on gold, maybe switching from US$?

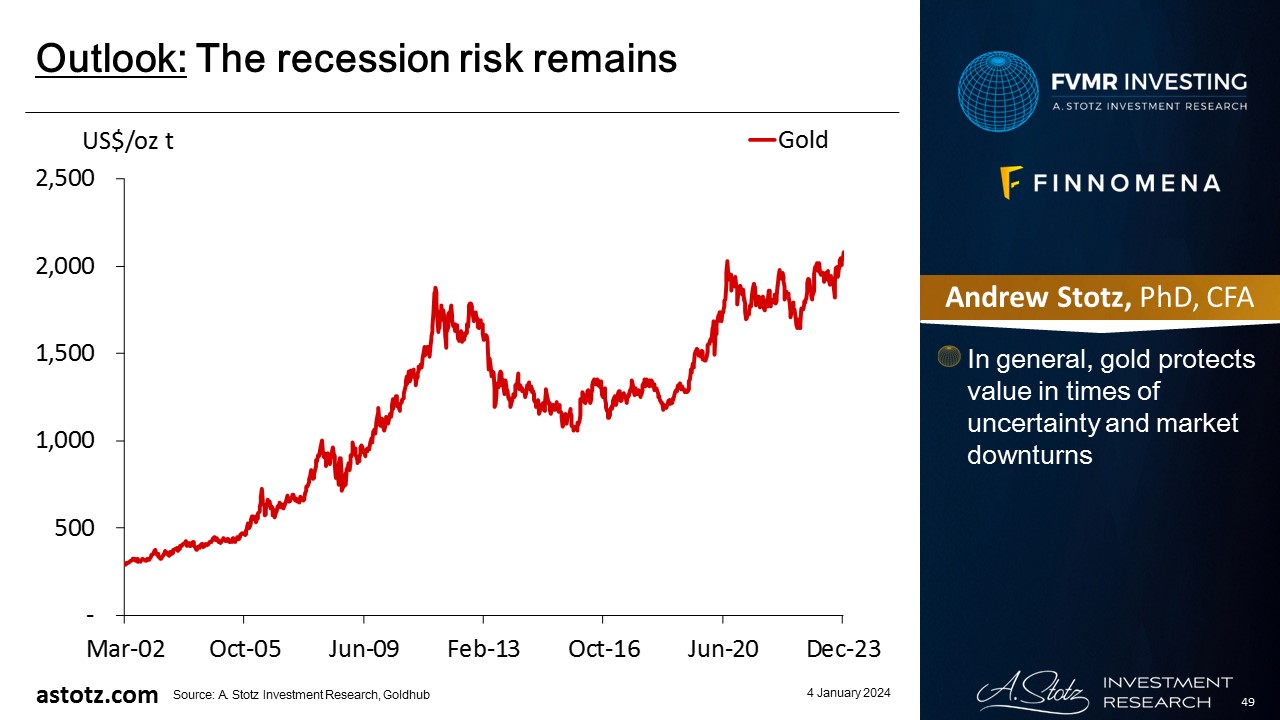

The recession risk remains

- In general, gold protects value in times of uncertainty and market downturns

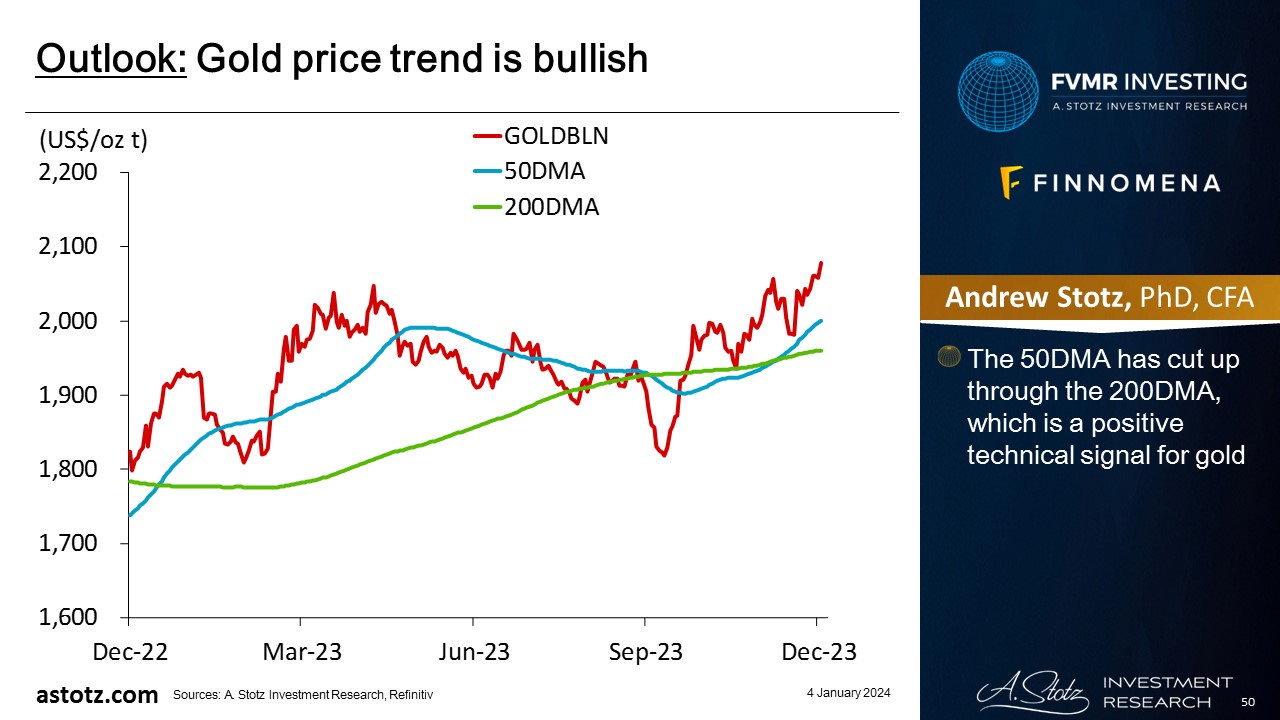

Gold price trend is bullish

- The 50DMA has cut up through the 200DMA, which is a positive technical signal for gold

Risk: Inflation reaccelerates

- Central banks’ aggressive rate hikes and QT crash the stock markets

- Continued rate hikes globally could lower bond yields (as higher rates mean lower bond prices)

- If inflation reaccelerates, we could miss out on rising commodities prices

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.