VMC: WACC – Theory versus Reality

This post was originally published here.

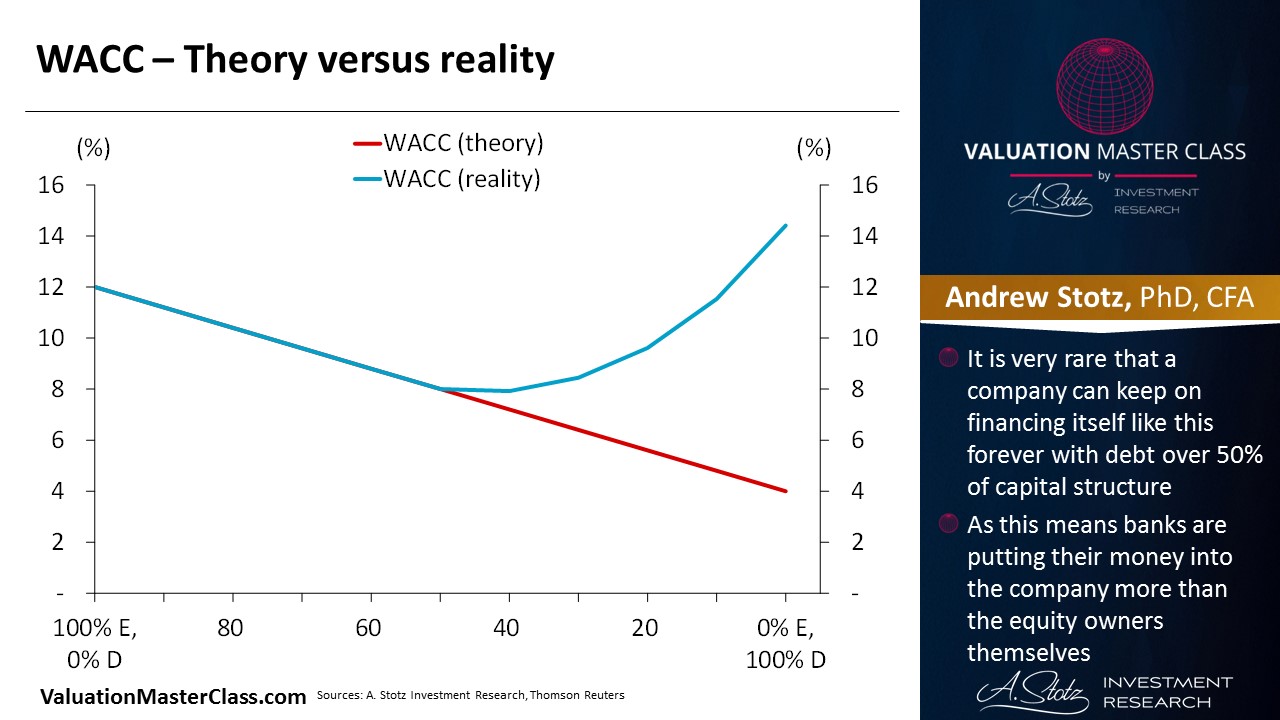

Since debt is cheaper than equity, in theory, this would mean that a company would prefer to be fully funded by debt to minimize its cost of capital. However, it’s not the case in reality that a company has a capital structure that is 100% debt. In this post, our main focus is on the cost of debt, to learn more about the cost of equity read this post.

The weighted average cost of capital (WACC) calculation

WACC = (E/V * COE) + (D/V) * COD * (1 – T)

Where,

E = Market value of equity

V = Total market value of equity and debt

COE = Cost of equity

D = Market value of debt

COD = Cost of debt

T = Corporate tax rate

WACC is what the company pay investors and creditors

The average rate of return that a company pays to all investors in the company. It is commonly referred to as the firm’s cost of capital. Investors include creditors, owners and other providers of capital.

A company has two primary sources of capital; debt and equity. WACC is the average cost of raising money from these two sources. The WACC is calculated taking into account the relative weights and costs of each.

What is Cost of debt (COD)?

The total amount of interest that a firm pays on all its debt. What lenders demand in compensation for the risk exposure they take lending to a company.

Since dividends are considered after taxes and they are part of the COE, then in the WACC calculation, we adjust the interest, reducing it depending on the tax rate.

An optimal capital structure is the capital structure that lowers the WACC to its lowest. Usually when the company grows the debt grows as well.

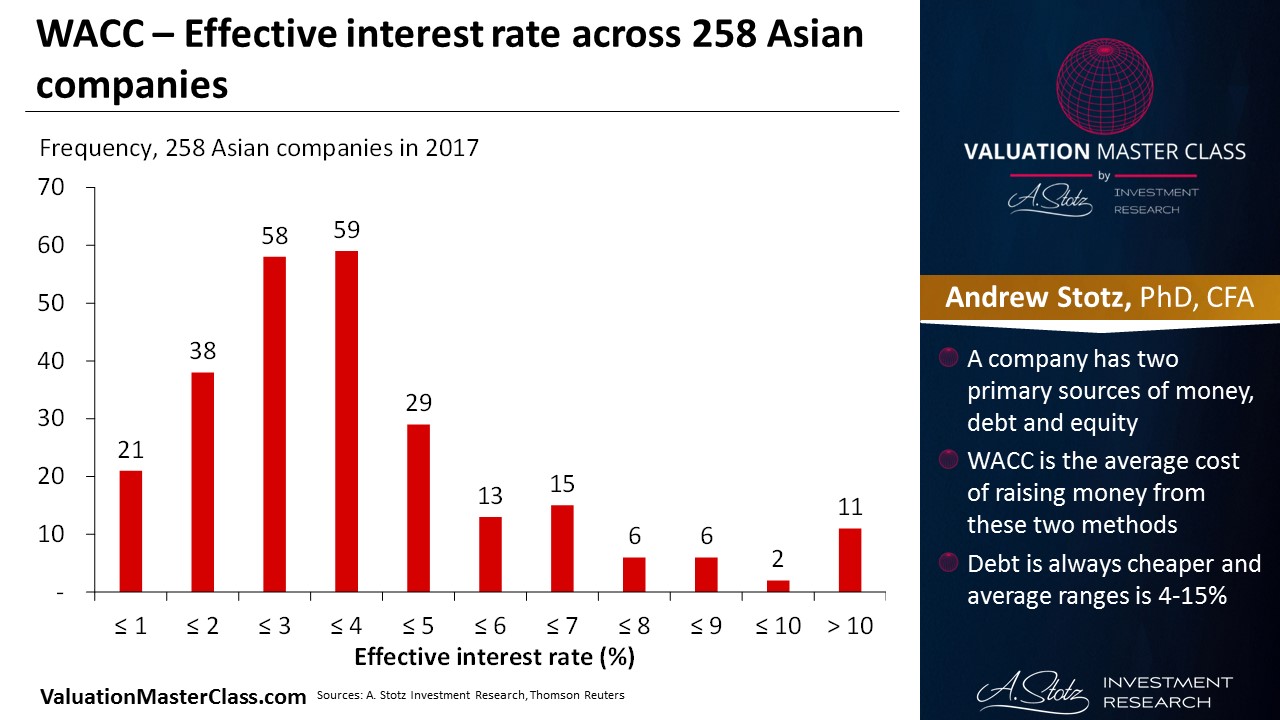

Debt is always cheaper, the average range is 4-15%. Equity usually ranges from 8-20%.

It is very rare that a company can keep on financing itself like this forever with debt over 50% of capital structure.

As this means banks are putting their money into the company more than the equity owners themselves.

This can happen for a short period when the company is distressed but not over long periods.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.