Sweden Equity FVMR Snapshot: ‘Sweden in Your Hand—Every Week’

Watch the video with Andrew Stotz or read about how to use the Sweden Equity FMVR Snapshot below.

Sweden in Your Hand—Every Week

The Sweden Equity FVMR Snapshot uses the same format we first introduced with our Global Equity FVMR Snapshot.

When you sign up, every week you will receive our Sweden Equity FVMR Snapshot, you will always be up to date. You’re going to know all your numbers, as this one-page document covers Fundamentals, Valuation, Momentum, and Risk—our FVMR framework.

You’re going to be professional as this is the same information used by institutional investors and fund managers.

And here’s the best part: You do nothing because after signing up, you’re going to receive a one-page PDF every Monday with updated numbers.

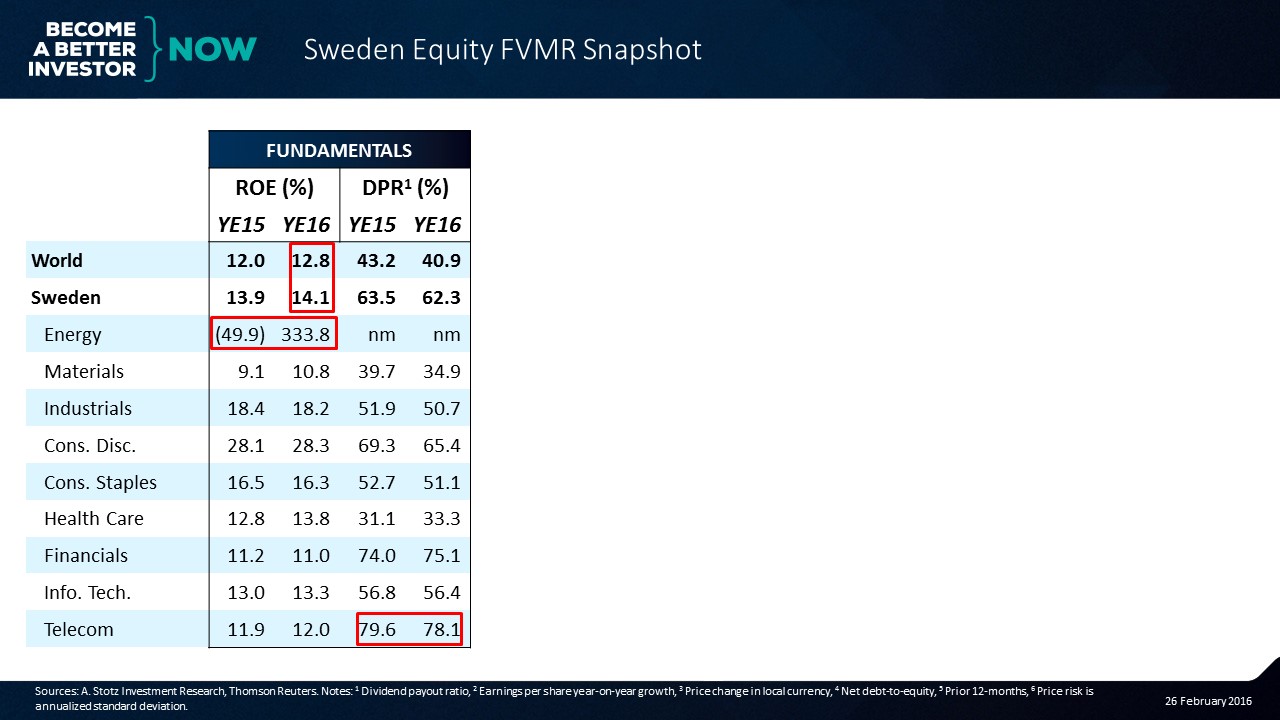

Fundamentals

So let’s take a look and see what it’s about. We start with looking at fundamentals. If we look at the world, we can see that the world ROE is about 12.8% in 2016. That’s the expectation.

Sweden is slightly above it. But we’re going to see in a moment that there’s a real reason why it’s actually “not so real”. It’s because we’ve got a big problem with energy companies in Sweden. What we can see is a negative equity in 2015 and a very massive positive equity which is coming from a distressed level. When there’s a tiny amount of equity, a tiny amount of profit makes it seem like a huge ROE.

Let’s move on to dividend payout ratio. We can see that the telecom companies, like in most countries, are paying a lot in dividends, in this case. In fact, Sweden at 62-63% dividend payout ratio is much higher than the rest of the world.

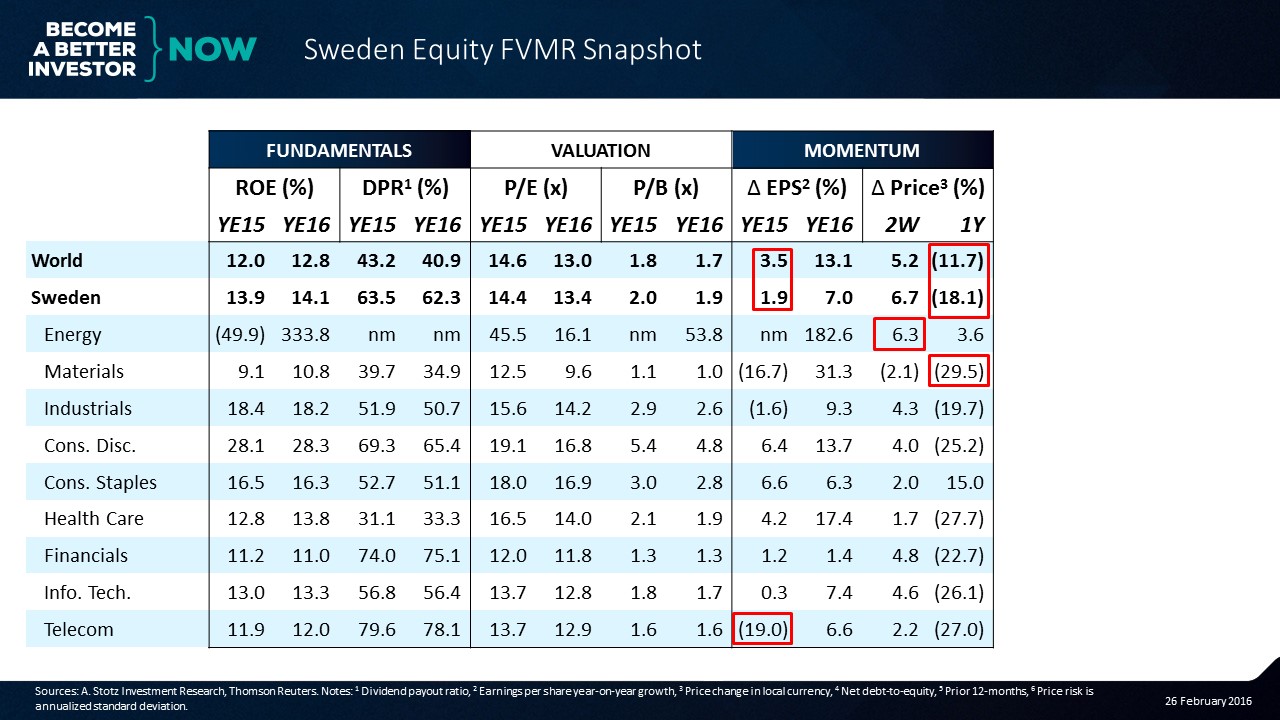

Valuation

If we look at the next measure which is valuation. How does Sweden look when it comes to valuation?

Here we can see the PE of 46x for energy companies. Again, this is because of a very distressed level of earnings in 2015, but we can see a recovery is expected in 2016 for the energy companies. Materials companies are trading low at about 12.5x.

If we just look at the PE of Sweden we see that it’s about in line and slightly above the rest of the world.

When we look at price-to-book ratio, we can see, again, that the energy companies’ PB is very high. This is because there’s a tiny bit of equity in the restructuring that’s going on there. Materials companies have not seen such a wipe out of equity. So they’re trading at about book value.

What does a 1x PB ratio mean?

It means that you’re only valuing the assets that exist in the business now and not any future income. So that generally means getting it cheap.

Momentum

We look at both price and earnings momentum.

The earnings momentum of Sweden has been low at 1.9% versus 3.5% for the world; and it’s slowly peaking up. But, still, it’s about half the rate of the rest of the world. In 2015, we can see that the telecoms companies had earnings growth that was actually contracted by 19%.

Now, what about price? Over the last year, the price of the Swedish market has fallen a lot more than the rest of the world. In fact, we can see that the fall in energy in the market is not being matched by a fall in the energy price stocks. Why is that?

Because the energy stocks have already fallen; and so, now, they’re kind of leveling out.

Let’s look at another sector—materials—where the share price over the last year has been crushed and over the last week, it was the worst performing sector—down by 2.1%.

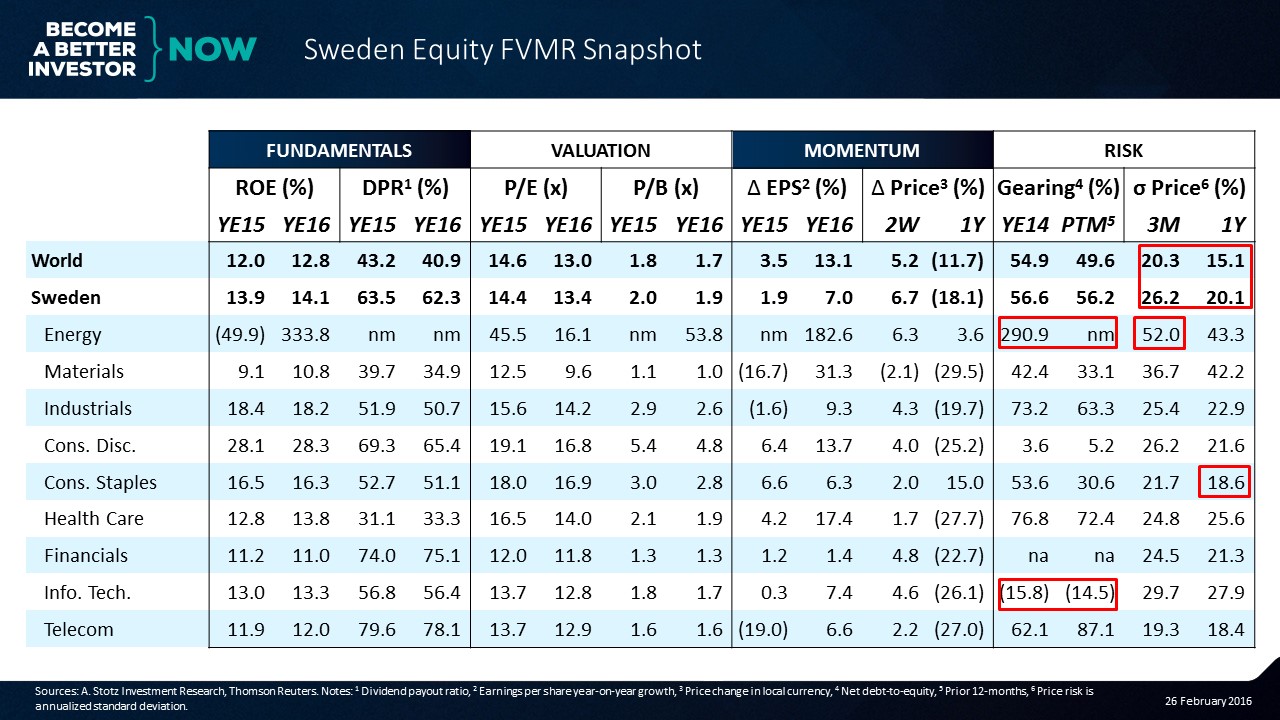

Risk

Now we move on to the final component of FVMR, and that’s risk.

We can see that the risk of the energy sector is very high because it’s got a high amount of gearing, meaning, net-debt to equity is very high. There’s a tiny amount of equity in the businesses.

If we look at the information technology sector, they don’t have debt. They mainly have cash and that’s why the gearing is negative. That’s good, that’s very good.

The volatility of price is what we’re interested in; and, of course, any one country is in general going to have more volatility than the world because the world has more stocks in it. So the volatility is slightly above the rest of the world.

Let’s just look within the sectors and we can see that the volatility in the energy sector over the last three months has been crushing. Fifty-two percent is a very high level of volatility. And then, the consumer staple companies are where the lowest volatility has been at 18.6% over the last year.

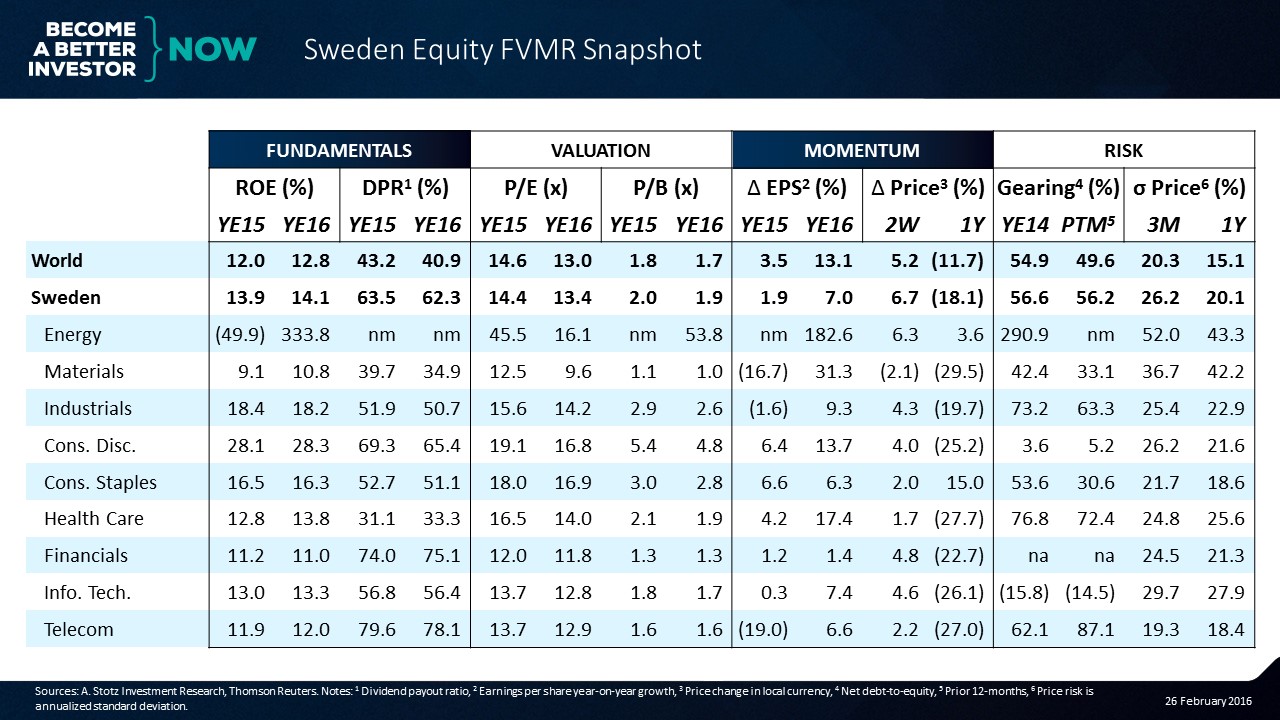

Sweden in Your Hand

With our Sweden Equity FVMR Snapshot, you’ll get a weekly update like the one below covering the Swedish stock market.

You’re going to understand fundamentals, valuation, momentum, and risk, and the way we look at them.

After signing up, YOU will:

-

Always be up to date: Every week you will receive the updated Sweden Equity FVMR Snapshot

-

Know all the numbers: One page covers Fundamentals, Valuation, Momentum, and Risk (FVMR)

-

Be professional: Use the same information as institutional investors and fund managers

-

Not have to do anything else to stay informed: After signing up you will receive a one-page PDF every Monday

The Sweden Equity FVMR Snapshot is free for everyone signing up within a limited time period. Sign up now to not miss out on getting it for free.

NOTE: You’ll have to fill in the form below to receive the Sweden Equity FVMR Snapshot even if you’re already subscribing to other Equity FVMR Snapshots and/or is a founding member that get our newsletter.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.