Strong equity rebound; Japan and Tech were the best performers. Performance review of our strategies in June 2023 – All Weather Inflation Guard was up 1.2%, All Weather Strategy was up 2.9%, All Weather Alpha Focus was up 2.3%. Global outlook that guides our asset allocation.

Read More

Shandong Humon Smelting Company Limited (002237 SZ): Profitable Growth rank of 8 was up compared to the prior period’s 9th rank. This is below average performance compared to 840 large Materials companies worldwide.

Read More

US core inflation lower than expected. The service sector holds up the economy. Bankruptcies peak at the end of a recession. Extremely low earnings yield for S&P 500. The top 1% is recovering.

Read More

What’s the difference between “perfect” and “that will work?” We use them interchangeably all the time. In this episode, Bill and Andrew discuss what “perfect” means and why it’s standing in the way of innovation and improvement at work and at home.

Read More

In this episode of Investment Strategy Made Simple (ISMS), Andrew and Larry discuss two chapters of Larry’s book Investment Mistakes Even Smart Investors Make and How to Avoid Them. In this seventh episode, they talk about mistake number 11: Do you let the price paid affect your decision to continue to hold an asset? And mistake number 12: Are you subject to the fallacy of the hot streak?

Read More

Triveni Turbine Limited (TRIV IN): Profitable Growth rank of 2 was same compared to the prior period’s 2nd rank. This is World Class performance compared to 770 small Industrials companies worldwide.

Read More

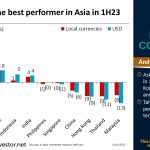

Asian markets were down in 1H23 except for Taiwan, Korea, Vietnam, Indonesia, and India. Taiwan was the strongest performer in USD and local terms.

Read More

In June 2023, we published 16 new episodes of the My Worst Investment Ever podcast and one blog post. Listen to all of them here.

Read More

80% of YouTube ads are subject to refunds. Bankruptcies on the rise in the US. T-Bills return the same as equities. Time to buy some bling? REMINDER: Stocks are still best in the long run.

Read More

Dr. Deming encouraged lifelong learning for everyone, but particularly for managers and leaders. In this episode, David and Andrew talk about Deming’s fourth point in his list for The Role of the Manager of People After the Transformation.

Read MoreAS SEEN ON: