Learning Valuation: KCE Electronics

Disclaimer:

This example was created on January 23, 2016. This is NOT a valuation, forecast, rating, or recommendation; rather, it is a teaching example. What follows is NOT investment advice; rather, it is a teaching example. It is intended only as academic information to those who want to learn about valuation. It should not be construed as the basis for any valuation or investment. The information in this presentation came from various sources which we believe are reliable, though we do not guarantee the accuracy, adequacy or completeness of such information. We hope you enjoy learning about valuation as much as we do!

Background

Founded in 1982, KCE Electronics Public Company Limited, with its five subsidiaries, develops, manufactures and distributes PCBs and inks for circuit boards and recycles chemicals used in making PCBs.

KCE is a producer of printed circuit boards (PCB), which are used in almost every computer device to connect electronic components using conductive tracks. Currently, more than 70% of its revenue comes from the automotive sector.

KCE operates three plants located in Ayutthaya, Bang Pu and Lat Krabang with total capacity of more than 280,000 square meters per month.

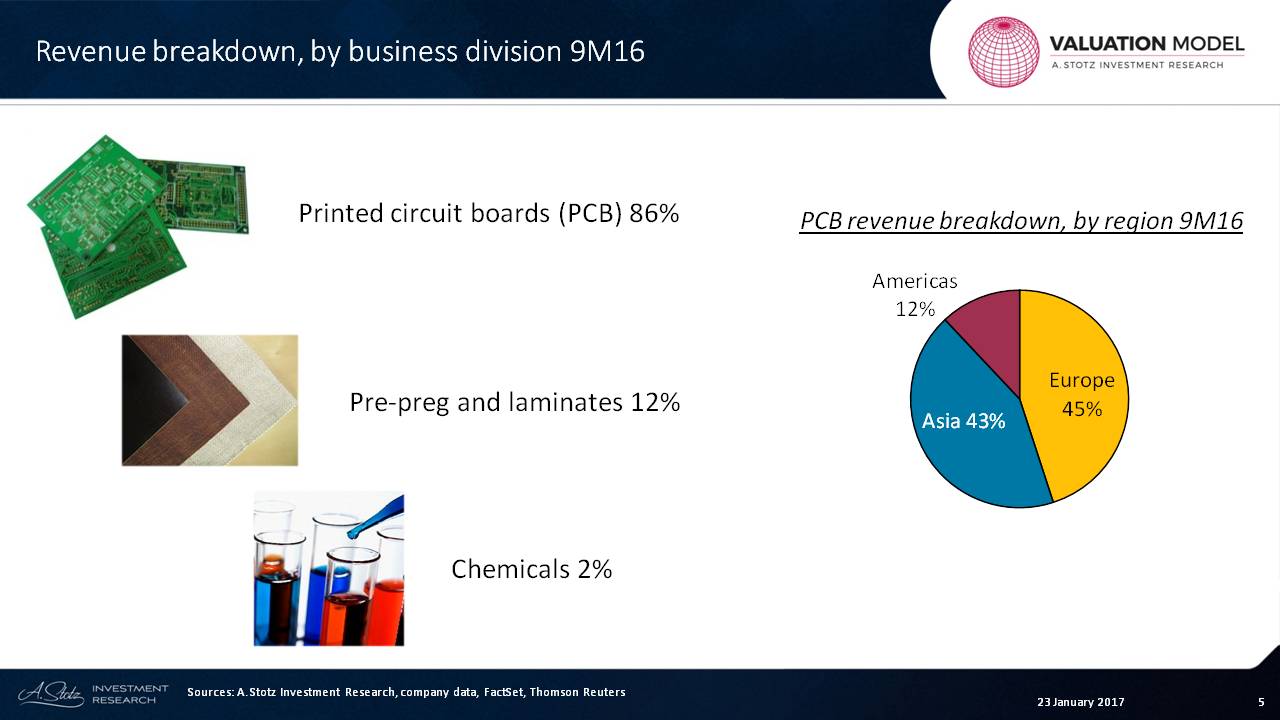

The company also exports products, with 45% of revenue coming from Europe, 43% from Asia and only 12% from Americas. It’s “Americas,” so a portion of that is the US. So if the new president, Donald Trump, says, “I am not going to import anything. I want to put huge taxes on it,” this company probably wouldn’t be that badly hurt. KCE’s sales offices are located in the Americas, Europe, Mexico, Japan, Korea, China and Singapore.

KCE’s sales offices are located in the Americas, Europe, Mexico, Japan, Korea, China and Singapore.

Revenue breakdown by business division as of the first nine months in 2016: Printed circuit boards (PCB) are 86% of revenue; pre-preg and laminates, 12%; and chemicals, 2%.

Forecasting

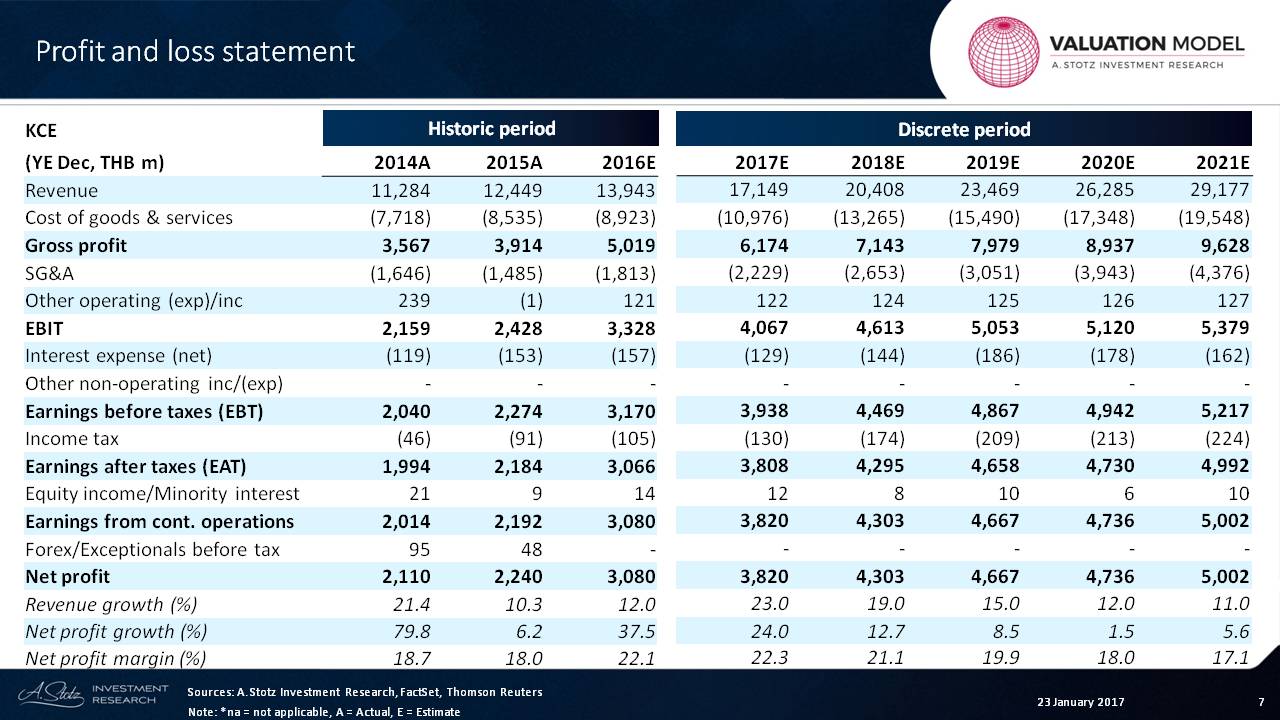

What we can see from this forecasting section is that we are expecting strong growth based upon the last three quarters or so, and then for that to level out at about 10%.

The growth is very volatile, and we’re expecting that it’s going to come down over time.

Why is that?

It’s because the margins are massive right now. You can see a 22% margin, which we think over time will start to decrease.

That’s one of the mistakes that analysts often make. When a company is making a high margin, they forecast a high margin going forward. That’s the concept of “recency bias,” where analysts carry forward whatever is recent.

I always try to bring it down if it has been really high or bring it up if it has been really low.

Assets

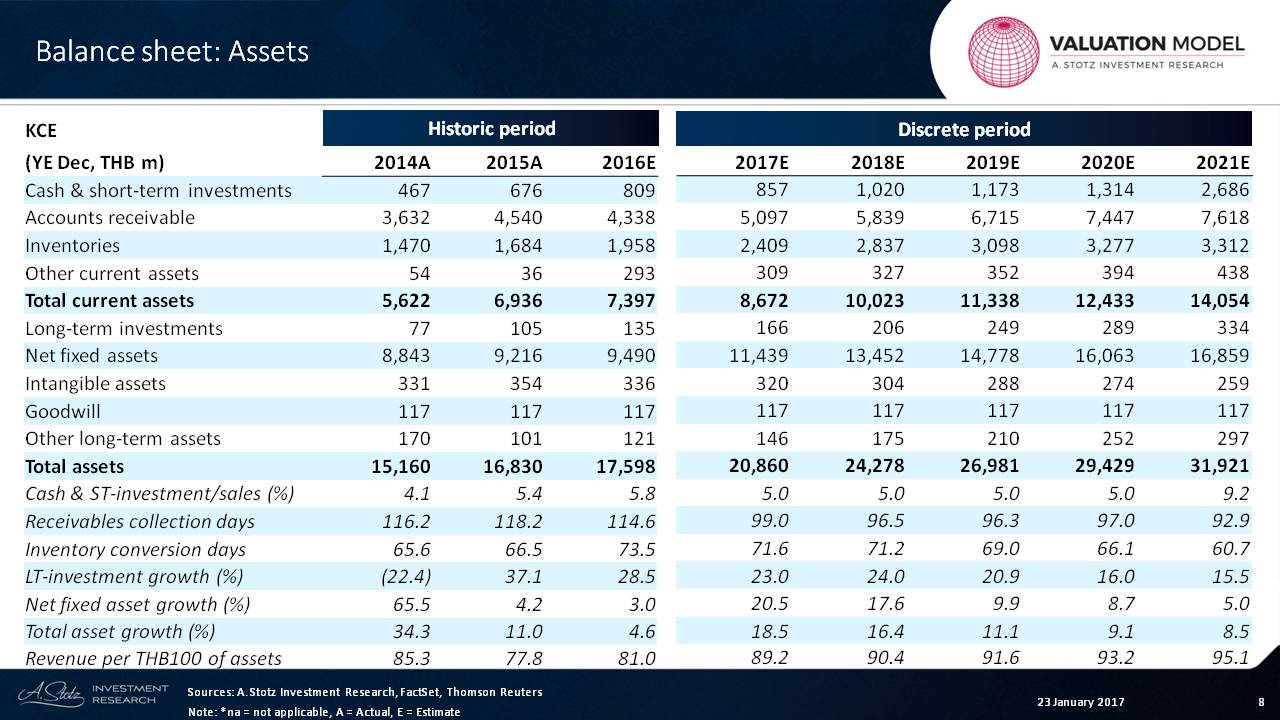

Next, let’s look at the amount of asset growth.

We can see that the company made a big investment, and then that asset growth has slowed. That’s good for now, but eventually they’ll have to raise investment in order to grow revenue.

The main thing that we want to look at is the revenue per THB100 of assets, and we can see that that will improve a little bit over time as they slow their asset growth.

The company’s dividend payout ratio is about 40%, which will increase over time to about 50% during the discrete period.

Cash Flow

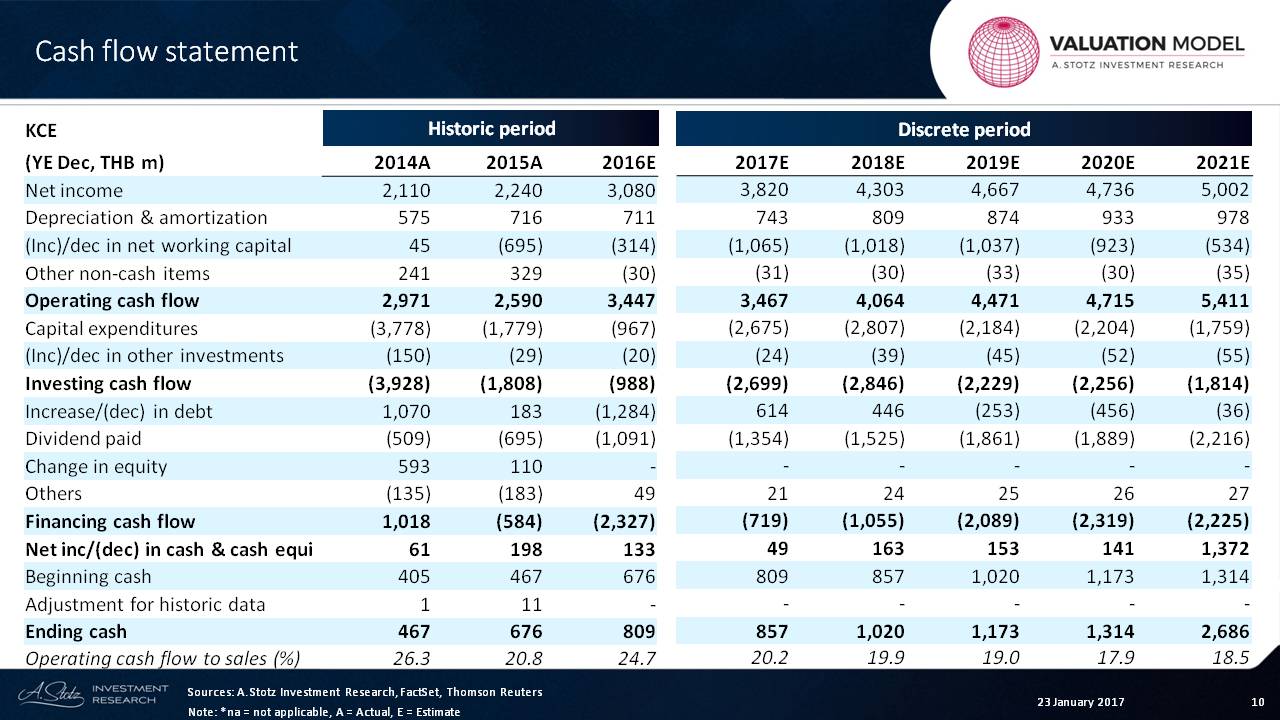

The next thing we look at is the cash flow of the company, and we can see that the investing cash flow is exceeding the operating cash flow ─ good news ─ so they don’t have to invest all that, which gives us room to pay a lot of dividends over the next five years or so.

Operating cash flow as a percent of sales varies, but let’s say it’s going to be 18% to 20% in the future.

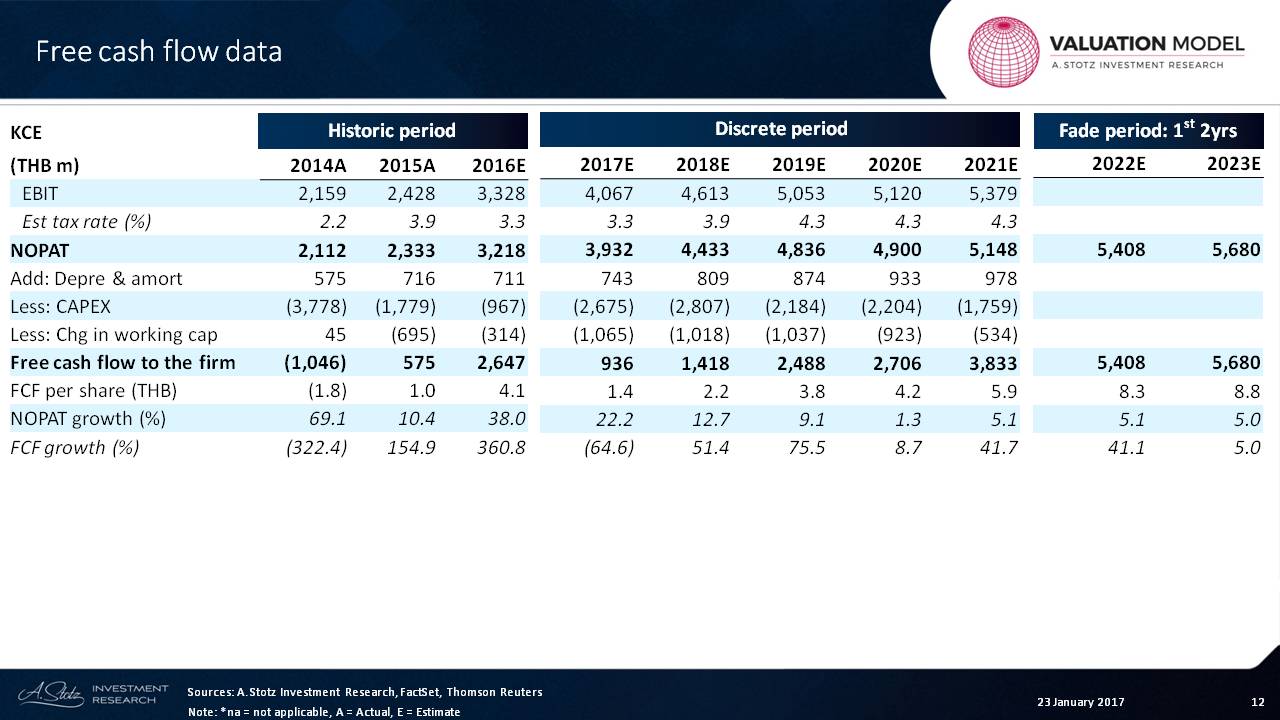

Free Cash Flow

Now, let’s talk about valuation.

When we talk about valuation, the first thing we want to understand is the net operating profit after tax (NOPAT) of the firm.

Looking at adding back depreciation, taking away the CAPEX and changing working capital, we end up with the free cash flow to the firm. The free cash flow to the firm was massive, and this will grow over time.

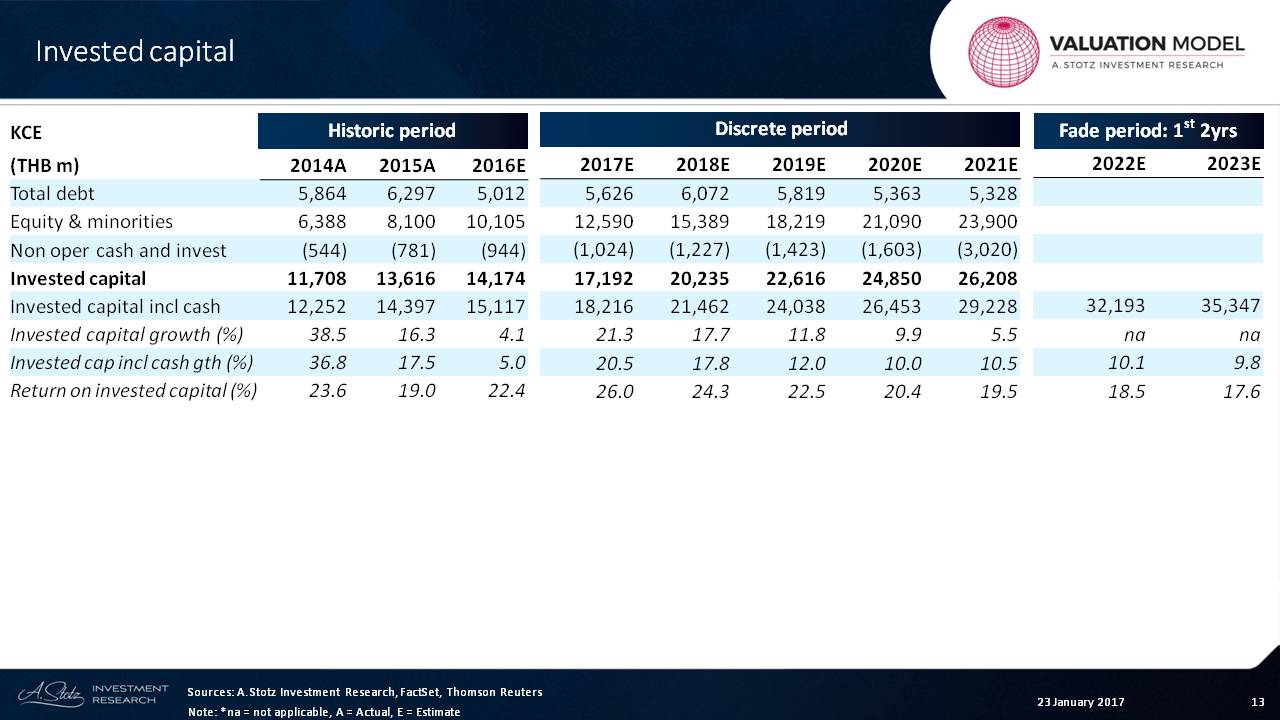

Invested Capital

The next thing we do is look at the return on invested capital, which has been about 20-some percent, and we’re forecasting it to be very high before coming down. And that is the item that we are fading down over time.

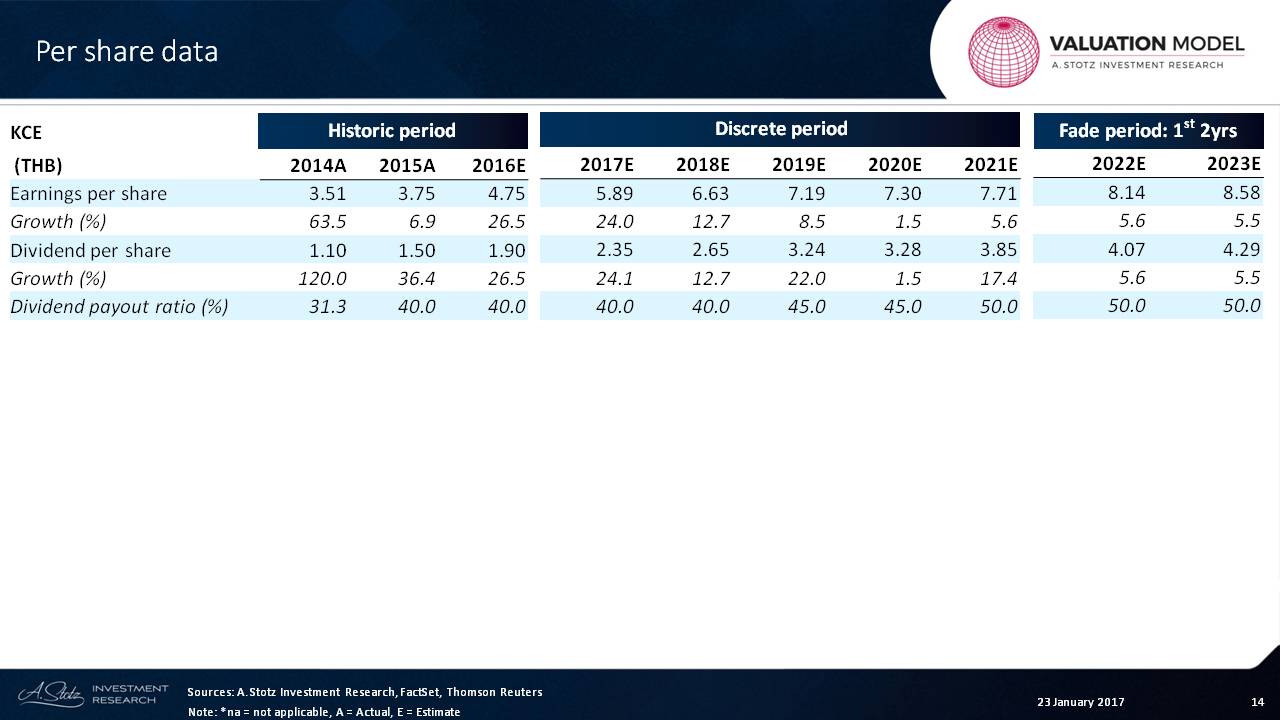

Per Share

For the dividend discount model, we need to understand the EPS, and we can see growth in EPS ─ 26%, 24%, 12% ─ and then it gets down to single digits. And that will fade down over time.

As far as the dividend growth, it is going to exceed the earnings growth, and that’s because the dividend payout ratio will be rising over time according to our estimates.

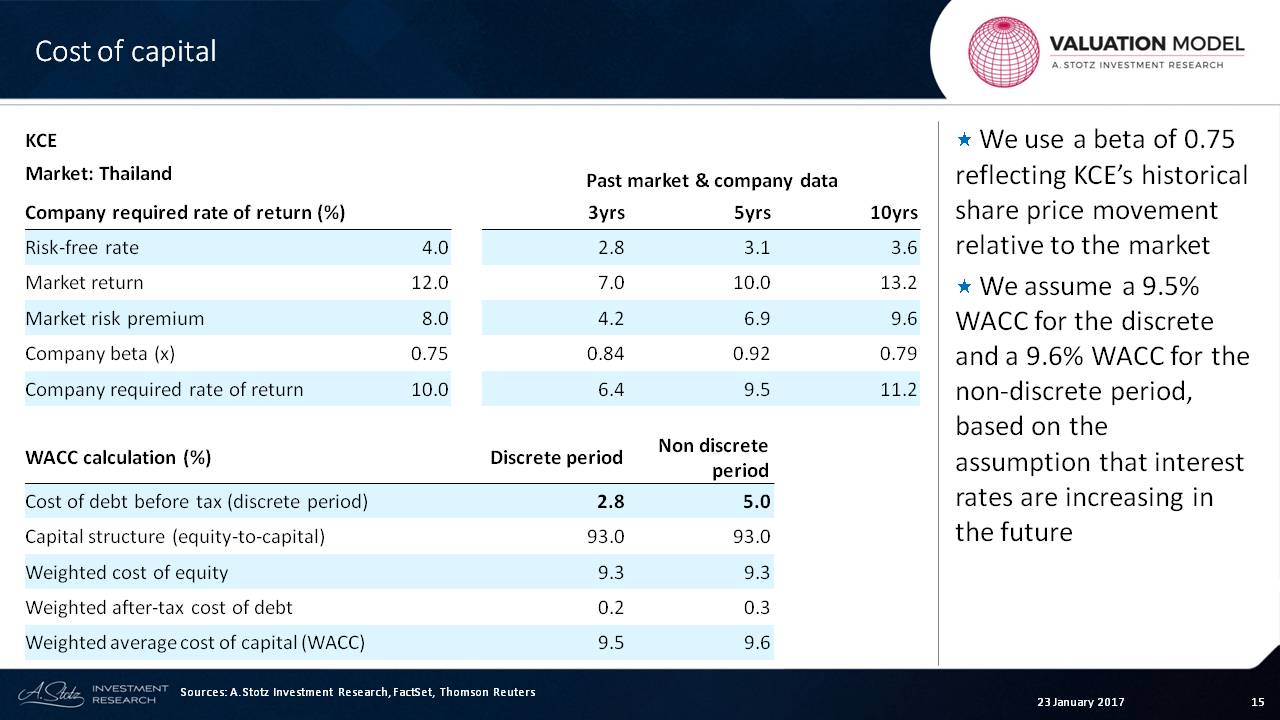

Cost of Capital

Let’s continue on to look at the cost of capital and how we get to that calculation.

We know that Thailand’s risk-free rate is 4% ─ that’s what we’re using ─ and the market premium is 8%. Therefore, the market return is 12%. Those are our assumptions for the country.

Let’s just look at this company over the years and say that it’s a low-risk company as far as volatility.

I didn’t mean to say “low risk.” What I meant to say was “low volatility” because, to me, the measure of beta is not really a measure of risk. It’s a measure of volatility.

What we can also see is that the cost of debt right now is pretty low at 2.8%. And we think that that’s going to rise over time.

The company is mainly funded by equity, and that’s probably going to remain the same. And so, the result is that the cost of equity here ─ the 10% ─ is very close to the weighted average cost of capital.

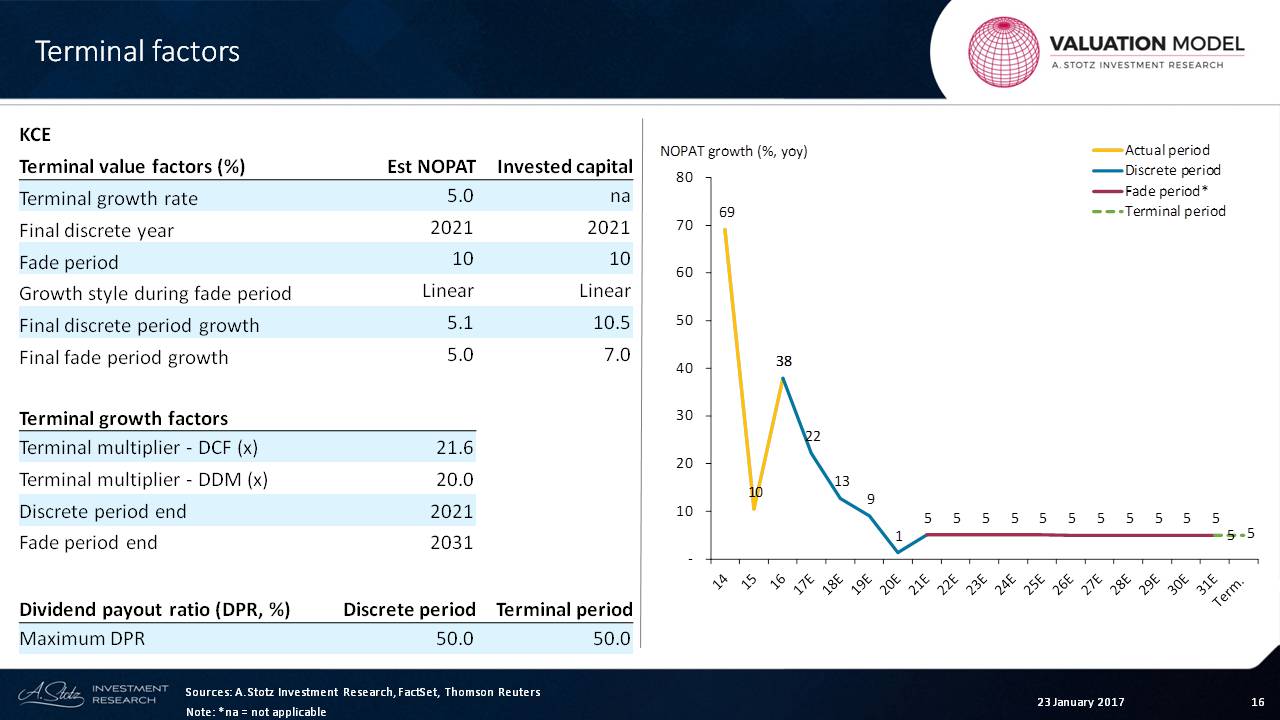

Terminal Factors

The company has had some pretty extreme growth. What we’re going to do is forecast that it’s going to come down.

This blue line is the discrete period. It means that the yellow line is what has already happened. And then we have our fade period.

The terminal growth right now is 5%. That’s the highest terminal growth we usually would give to a company. I would say that if we find that the terminal value is actually quite high in our valuation, we could bring that down to 3% or 4%.

What we can see is that the final fade period growth is 5%. That’s why everything is 5%, because it’s targeting 5% in that terminal period.

Normally, this would be coming down from 10% to 9% to 8% to 7% to 6% to 5%.

The next thing that we want to do is to understand the multiples.

These multiples are how we get our terminal value. They’re pretty high multiples, because we have a very high growth rate.

Remember that the terminal growth rate could never be higher than the growth rate of the overall economy, or else the company over time would become bigger than the economy, and that’s impossible.

Now, let’s go through it.

What I can see already is that 11% and 10% of the value is in the next five years. We can see that a lot of the value is in the terminal period.

We’ve seen some pretty high terminal growth that we’ve forecasted. So if we were going to adjust that, I would say that that would be something we could consider adjusting.

Again, this is a teaching example, so we try to understand the levers there.

It’s possible that if the terminal value came down, the value here would come down a bit.

But overall, what we can see is that from a DDM basis, the DDM usually underestimates relative to the price. But if we look at it on a free cash flow basis, we can see that the valuation is about in line with the current price.

Is it expensive?

No.

Is it cheap?

No.

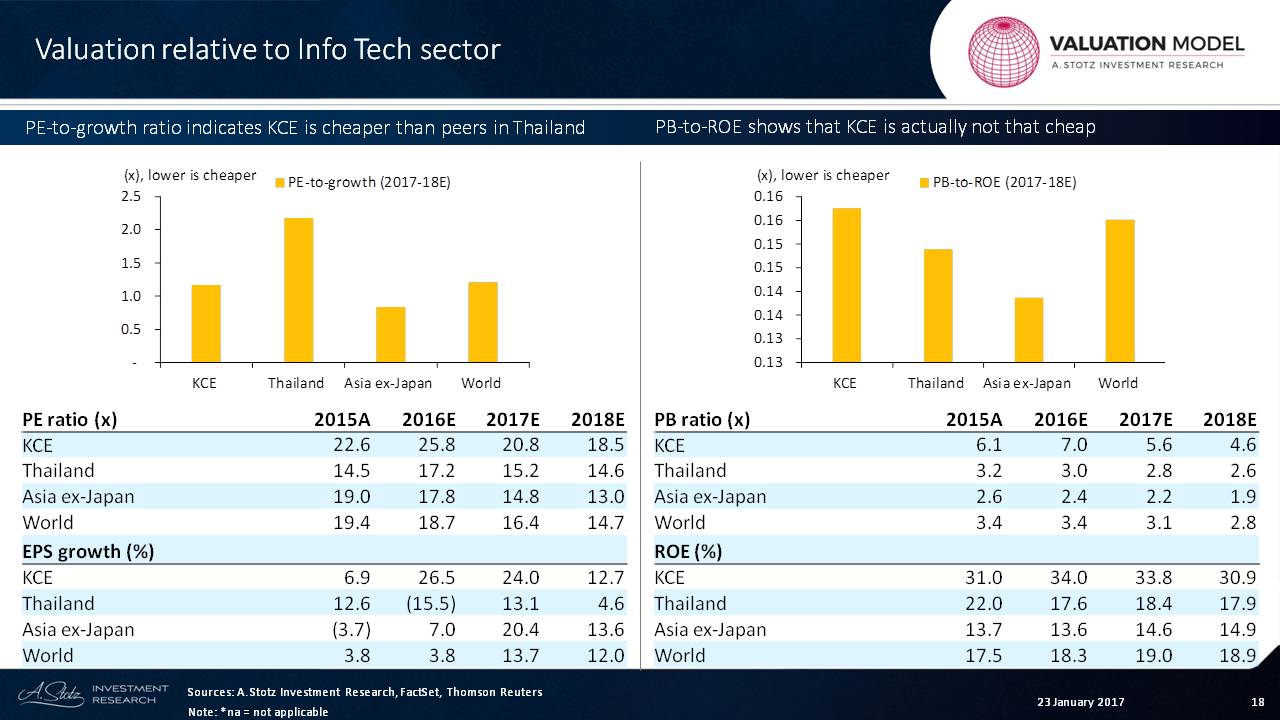

Relative Valuation

So let’s look at the valuation relative to the information technology sector. This is a relative valuation.

What we can see is that the PE of the company is about 20x, and the company has an EPS growth rate that’s pretty significant.

That 20x is higher than the market, so it’s a little bit more expensive. But the growth also is higher than the market. So the PE-to-growth ratio is about 1.0 right now.

Lower is cheaper, so it’s basically cheaper than the alternatives in Thailand. And it’s a little bit more expensive than the alternatives in the rest of Asia.

If we look at the other side, less volatile is the PB-to-ROE ratio, and we can see that price -to-book (PB) is a little bit high relative to Thailand ─ almost double the amount. But the ROE is almost double the amount also.

So if we look at them together, what we can see is that, right now, it’s a little bit expensive relative to Thailand and Asia ex-Japan.

I wouldn’t say that this looks like an overvalued stock but it looks like it’s a little bit expensive from a multiples perspective.

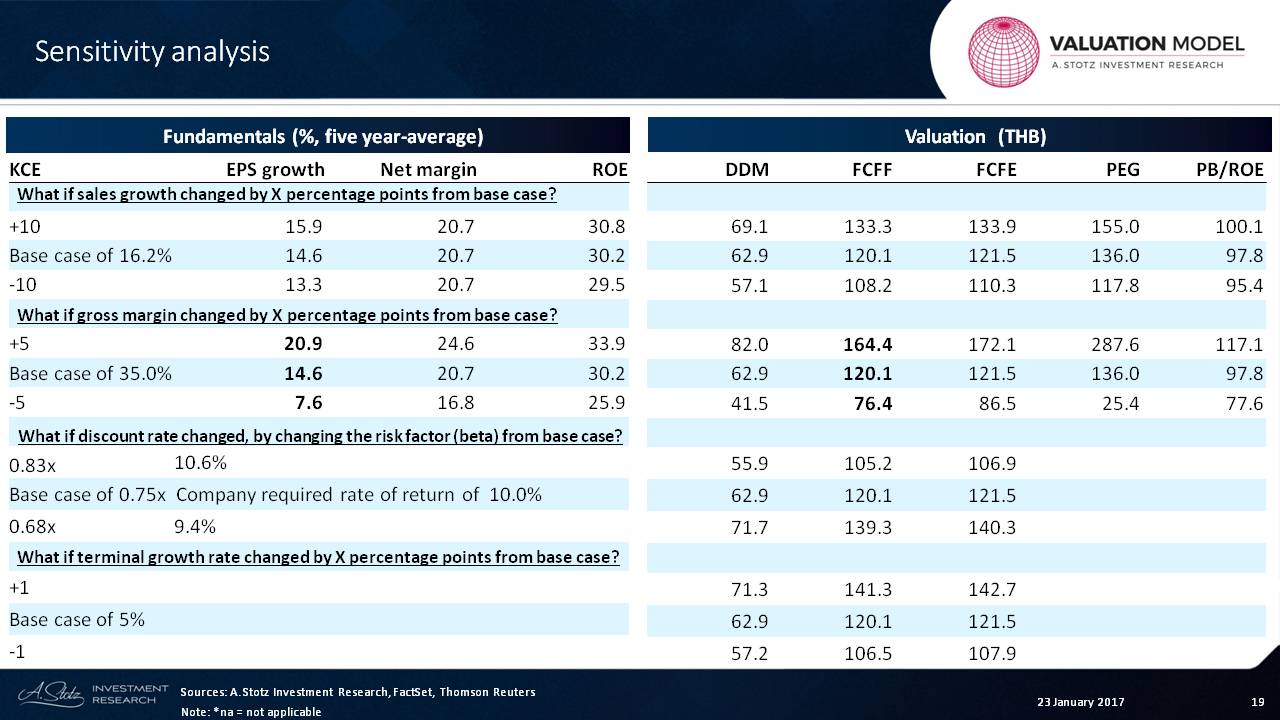

Sensitivity Analysis

Now, let’s take a look at the sensitivity.

Remember that we look at four factors: sales growth, margin change, discount rate, and terminal growth rate.

What we’re doing is looking at base case and then plus or minus. Let’s just take a look at gross margin, and we can see that the gross margin tends to be the most important for most companies.

So if we add 5% ─ that’s a 40% gross margin ─ then the EPS growth would go from 15% to 21%. And if that went down to a 30% margin, that would go down to 7.6%.

If we look at it from a free cash flow perspective, that small change in that EPS growth is just one year, but that will carry on for many years going forward.

So that gives us an idea of KCE. I hope you can learn from this.

If you have any questions or comments or experiences with it, leave them below… we want to talk to YOU.