Can You Beat the Market by Investing in Low PE Stocks?

In this Academic-Style Research we tested a valuation factor, low price-to-earnings (PE), on a global universe of stocks. PE is a valuation measure that tells you how many times the company’s earning you have to pay when you buy the stock at a certain point in time.

Hypothesis

Investing in companies with low price-to-earnings (PE) generates price outperformance.

Universe

A global universe of stocks from June 2006 to April 2017. Only included companies with a minimum market cap of US$500m (no micro caps) and more than US$3m in 3MADTO (no illiquid stocks). On average, the universe consisted of 3,200 stocks per quarter.

Methodology: Testing the relationship between low PE and return

We winsorized at +/- 3 standard deviations to exclude outliers. Divided the universe into deciles and added two additional groups: Top 15 and Bottom 15. We calculated the equal-weighted return for each group. The groups were reselected and rebalanced each quarter. All returns are presented in US dollar terms.

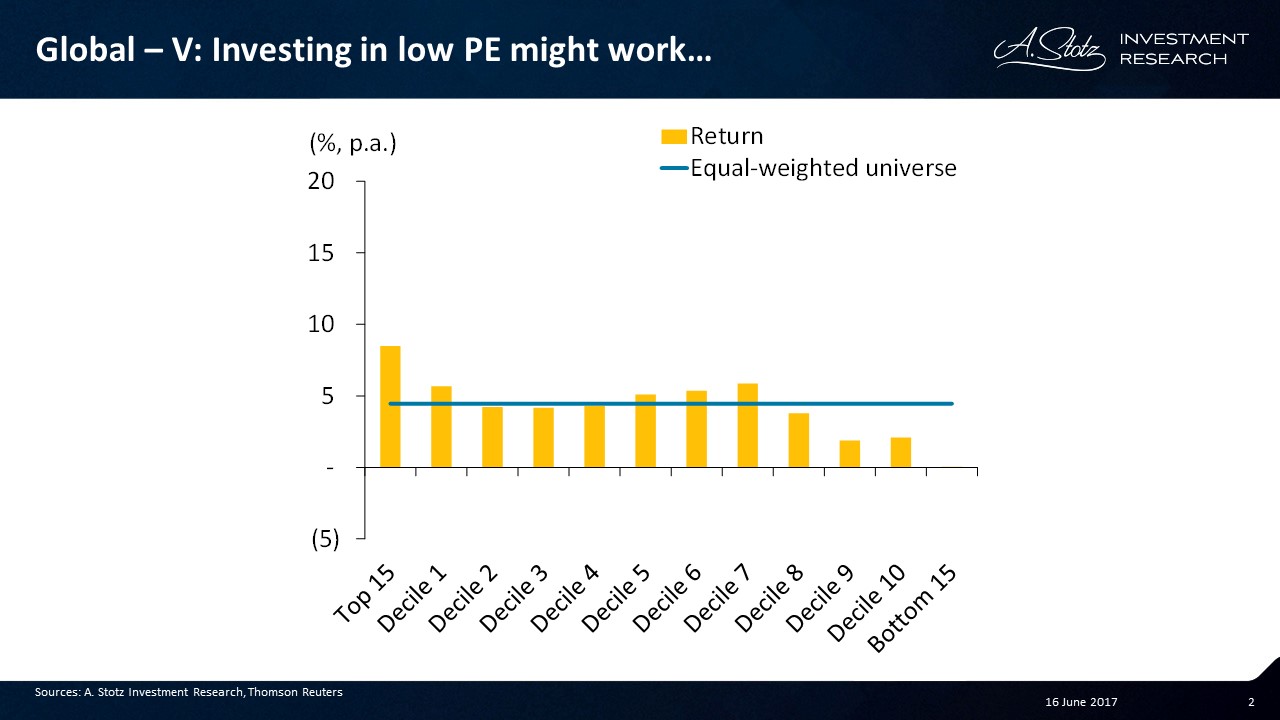

Investing in low PE might work…

On a decile basis, investing in low PE didn’t seem to have been the perfect strategy. Decile 1 returned better than the universe, but so did deciles 5-7 as well. The Top 15 including the lowest PE stocks returned the best, also the Bottom 15 showed the worst performance among the groups.

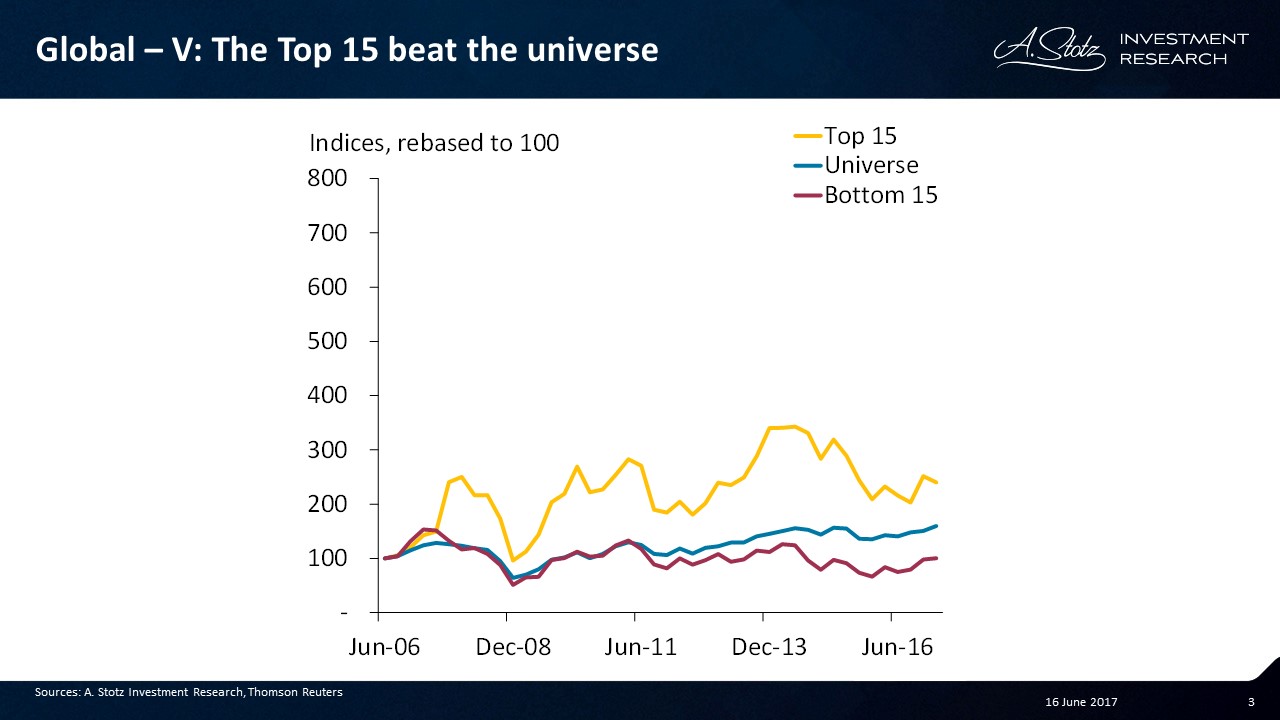

The Top 15 beat the universe

The Top 15 beat the universe since inception and the Bottom 15 underperformed almost the whole time period.

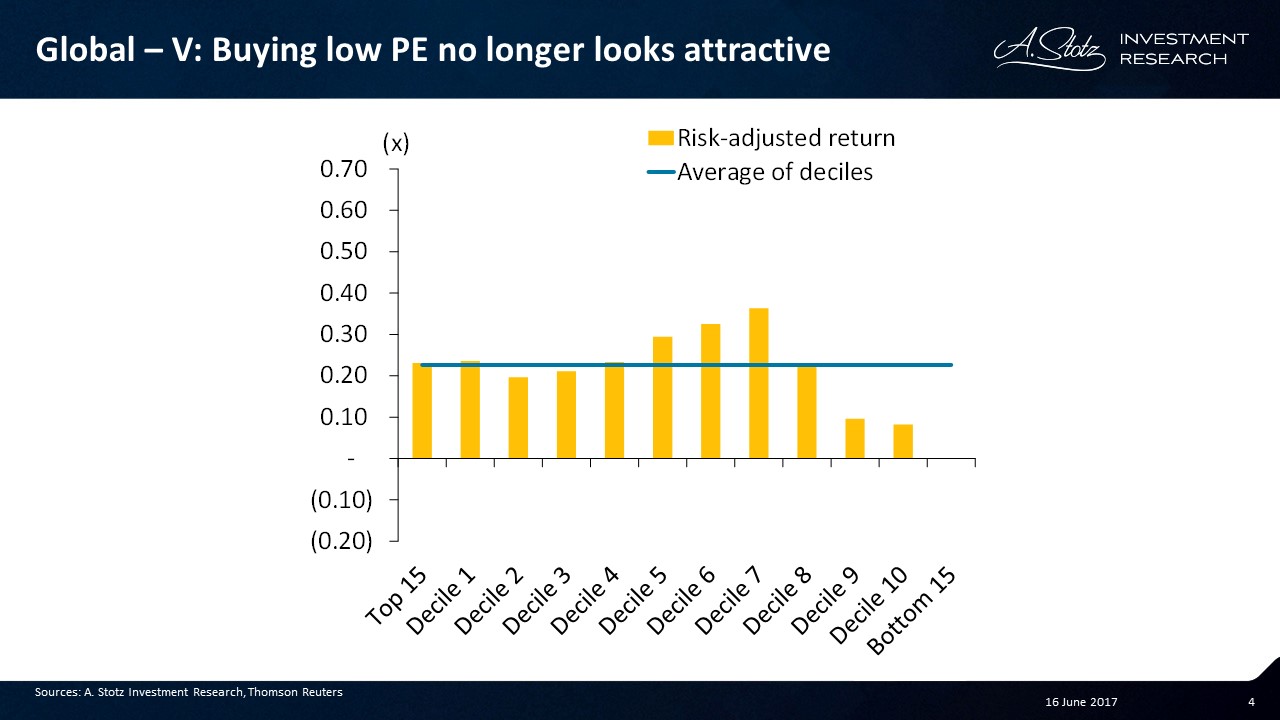

Adjusting for risk, buying low PE no longer looks attractive

Adjusting for risk, the results do not look good. The Top 15 only generated an average risk-adjusted return. Only deciles 5-7 had a risk-adjusted return better than the average.

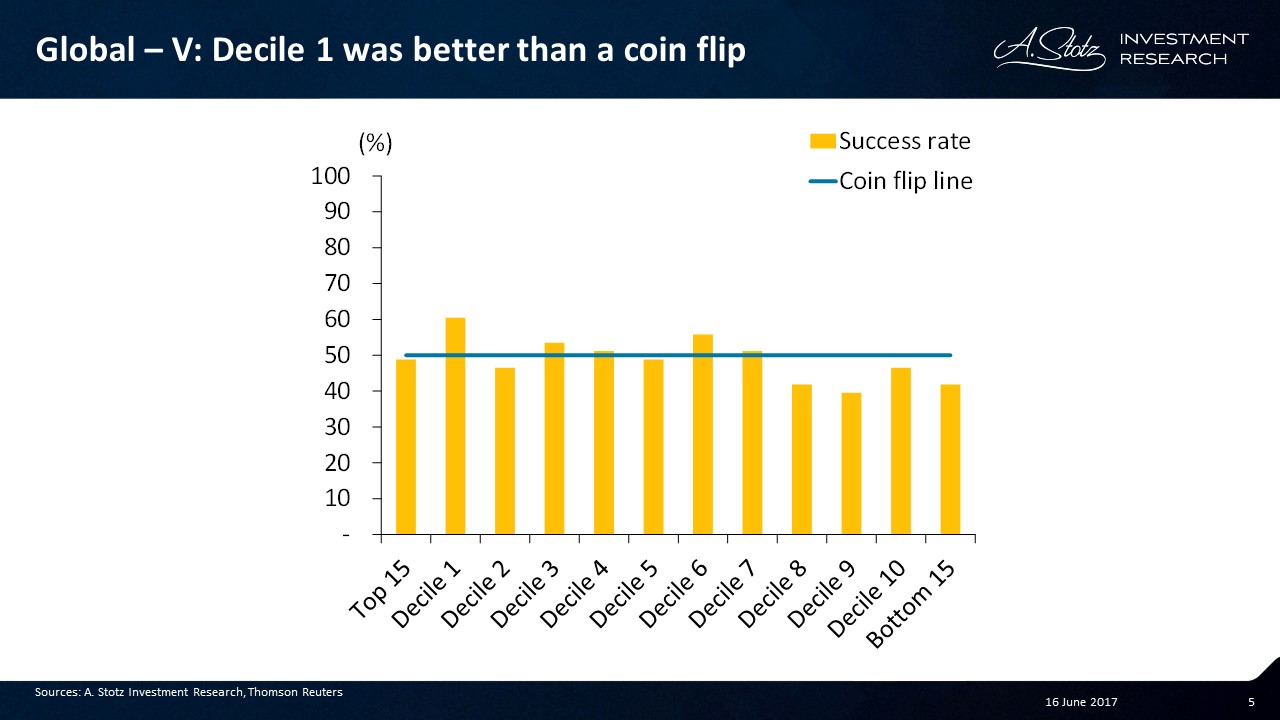

Decile 1 was better than a coin flip

A successful quarter is when that group of stocks returned more than the equal-weighted universe. The success rate is given by the number of successful quarters divided by the total number of quarters. Decile 1 had the highest success rate at about 60%.

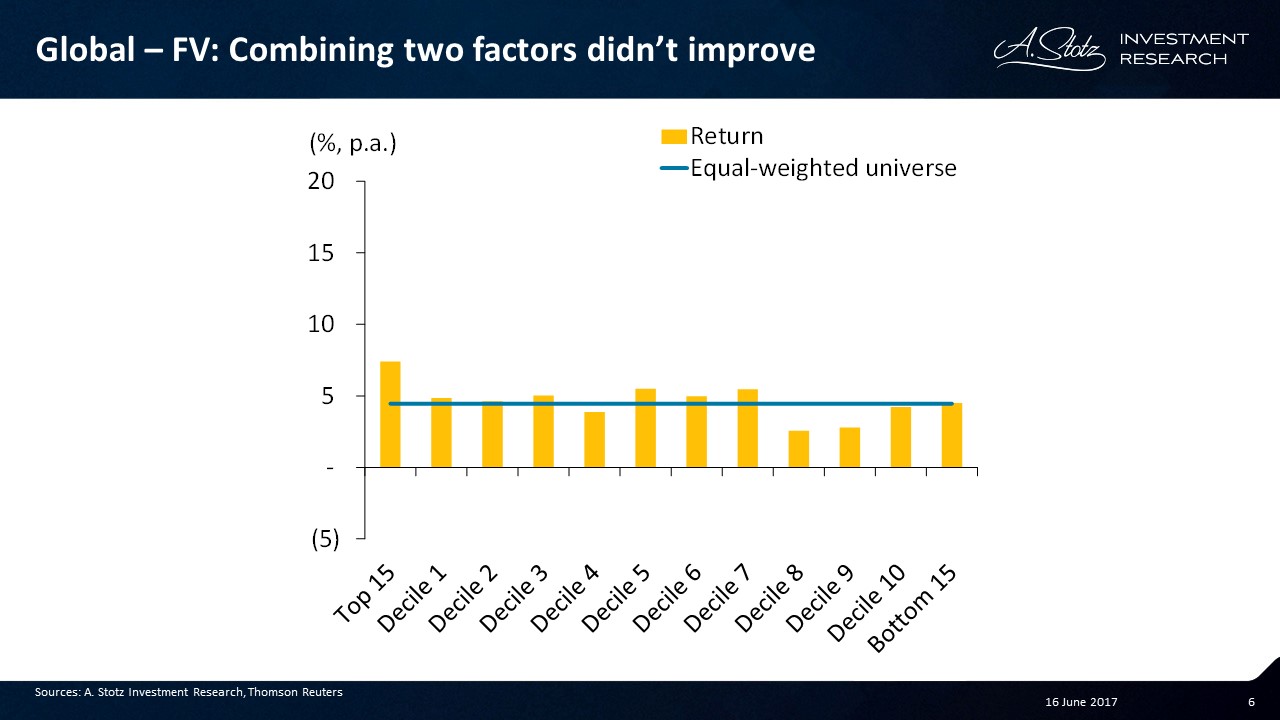

Let’s combine this Valuation factor with a Fundamental factor

Now we’ve combined high asset turnover improvement (Fundamental factor) and low PE (Valuation factor). Check out Can Change in Asset Turnover Predict Future Return? if you want to see how the Fundamental factor did on its own.

Top 15 generated the best return and Decile 1 returned better than the universe, but it wasn’t the best decile.

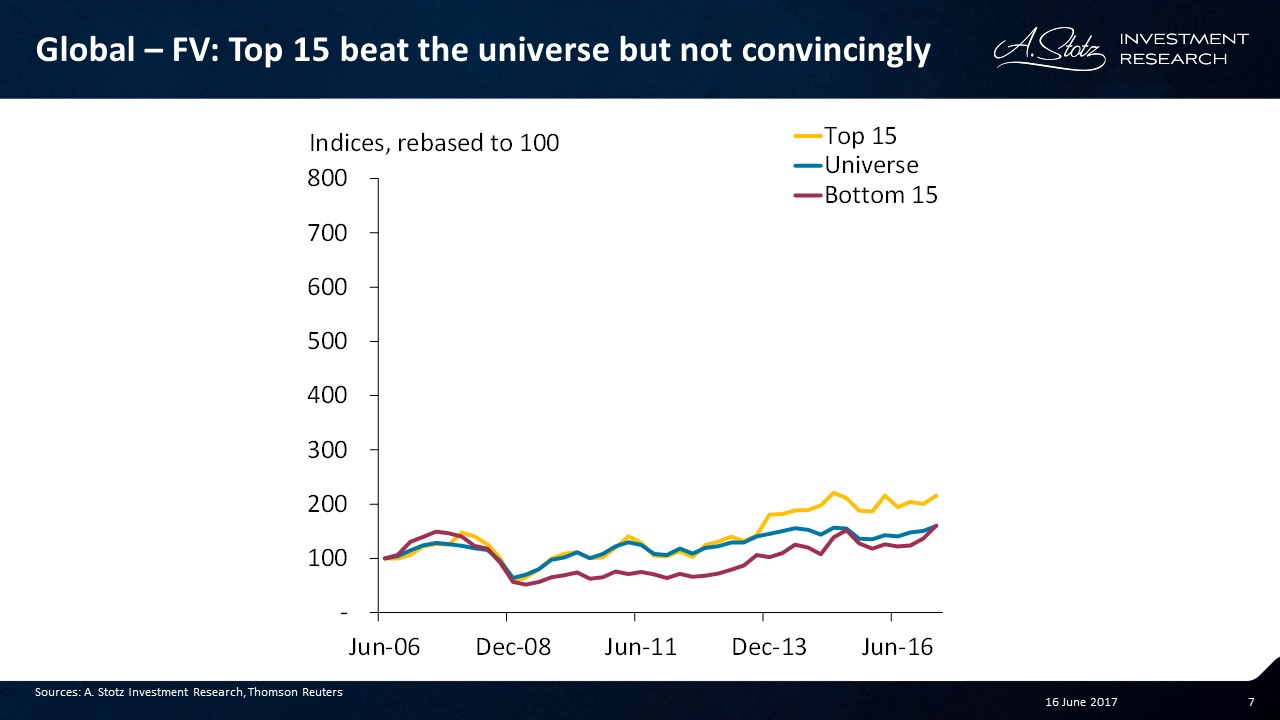

Top 15 beat the universe but not convincingly

The Top 15 started mainly started to outperform the universe after 2013. The Bottom 15 underperformed most of the time, but picked up on the universe recently.

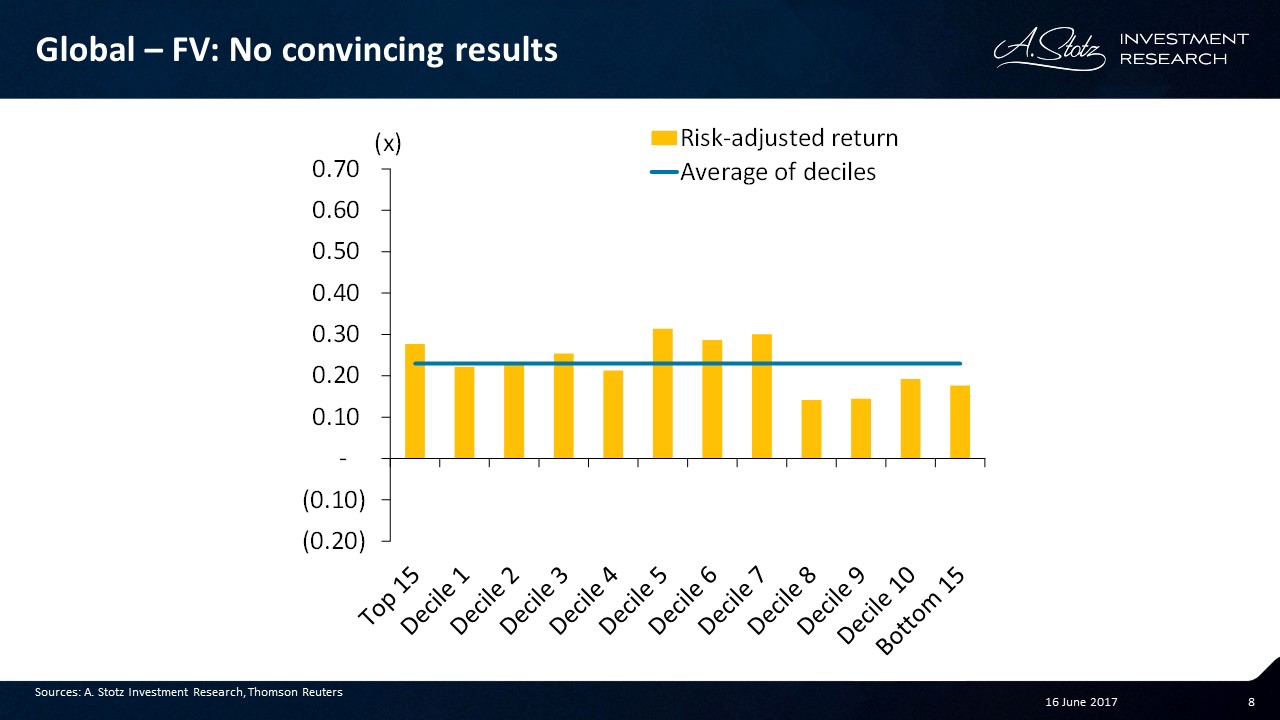

No convincing results for this combination

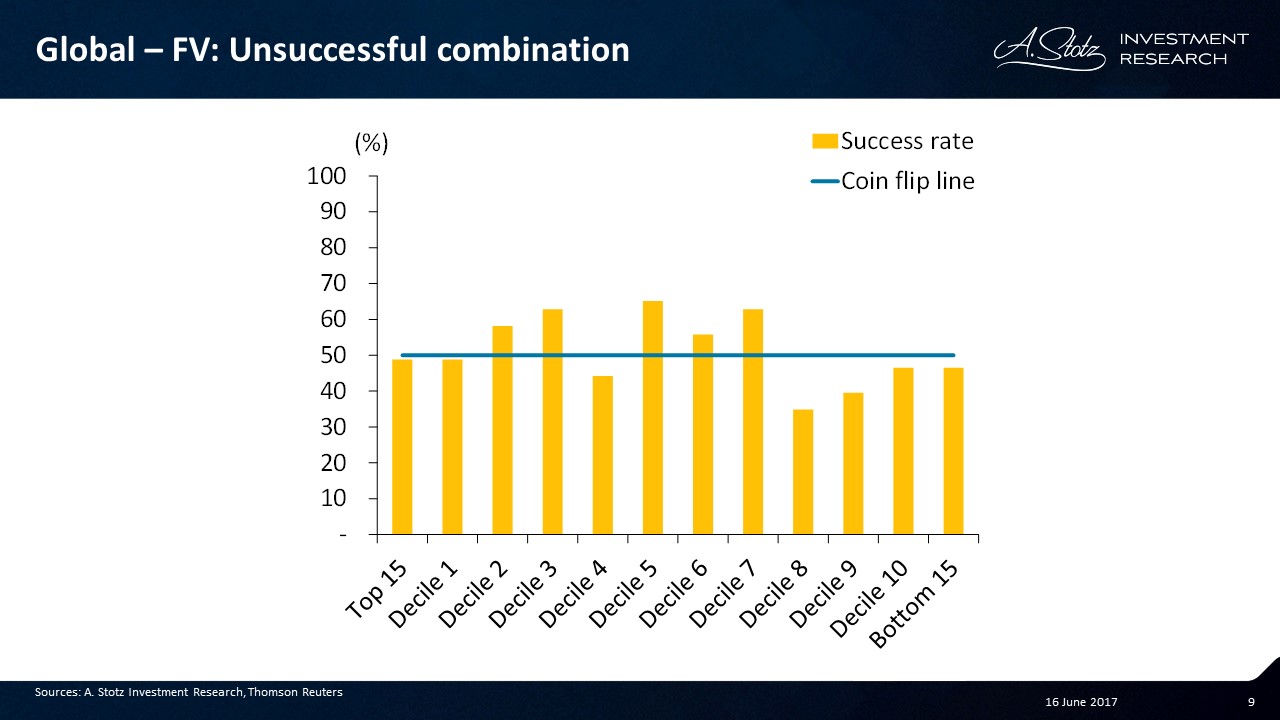

The combination was unsuccessful

Looking at the success rate, Top 15 and Decile 1 aren’t convincing.

What you have learned

A low PE strategy worked somewhat globally for the Top 15 and Decile 1. On a risk-adjusted return basis it did not beat the universe though. The combination of F+V (high asset turnover improvement and low PE) worked better for Top 15, but not a convincing investment strategy.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.