A. Stotz All Weather Strategies – July 2023

The All Weather Strategy is available in Thailand through FINNOMENA. If you’re interested in our allocation strategy, you can also join the Become a Better Investor Community. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

What happened in world markets in July 2023

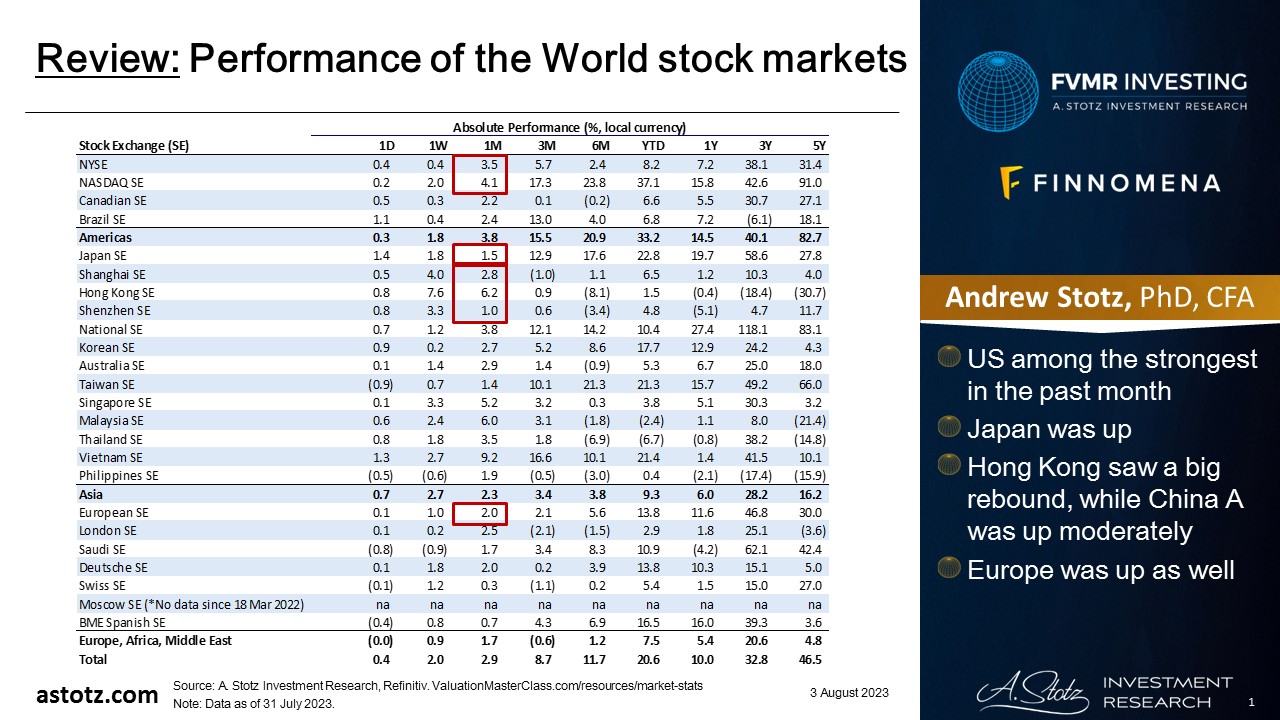

Performance of the World stock markets

- US among the strongest in the past month

- Japan was up

- Hong Kong saw a big rebound, while China A was up moderately

- Europe was up as well

Find the updated Performance of the World stock markets here.

World stocks gained 3.7% in July 2023

- In 2022, World stocks were down 18.0%

- YTD23, they’re up 18.5%

- The market seems to expect a soft landing

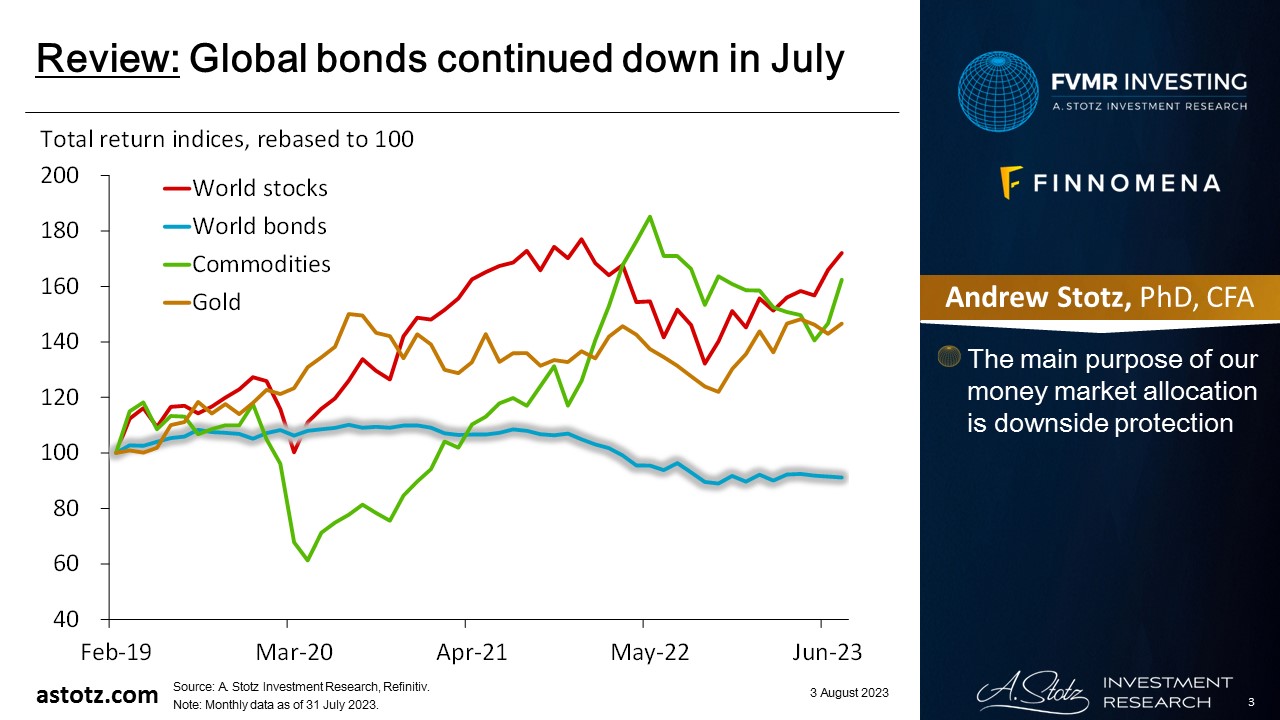

Global bonds continued down in July

- The main purpose of our money market allocation is downside protection

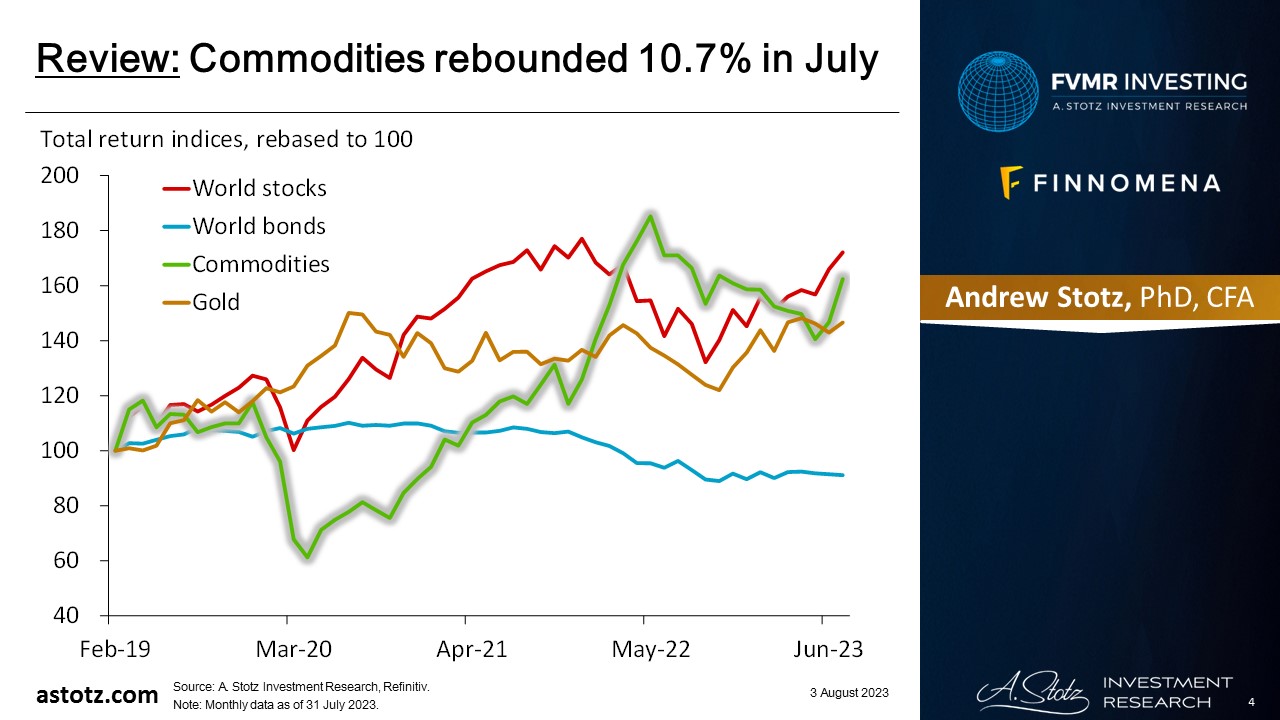

Commodities rebounded 10.7% in July

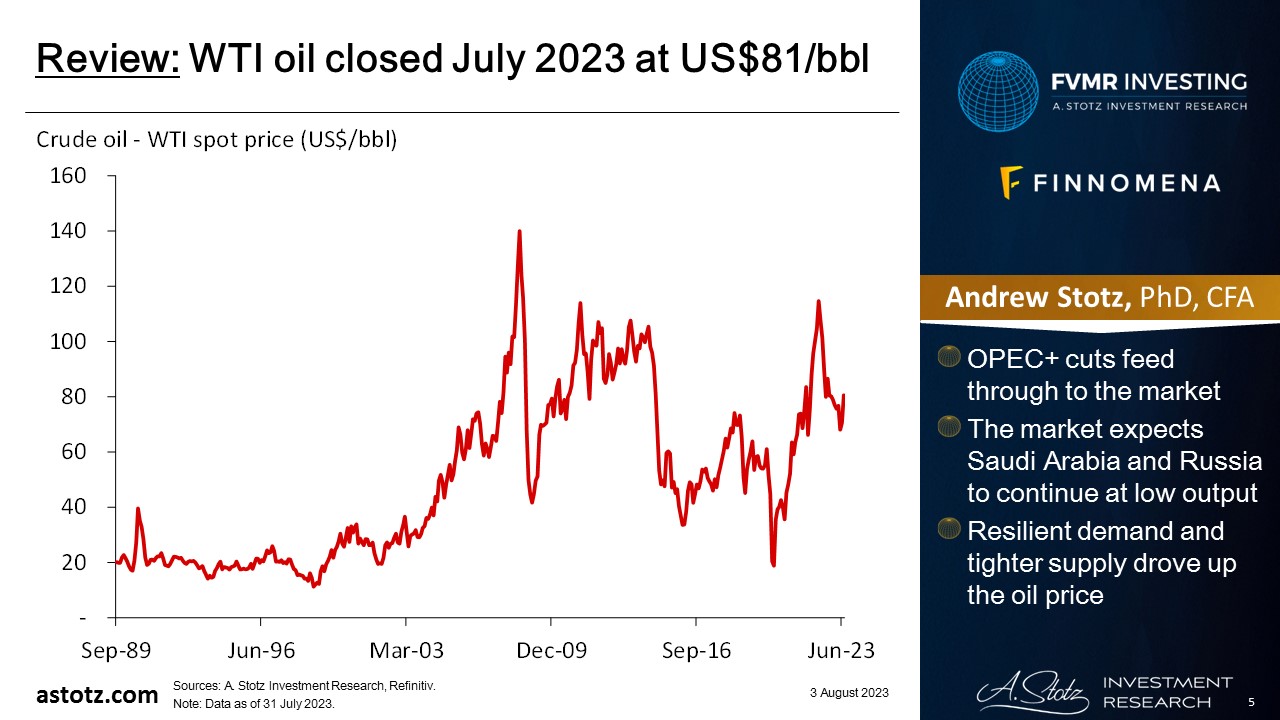

WTI oil closed July 2023 at US$81/bbl

- OPEC+ cuts feed through to the market

- The market expects Saudi Arabia and Russia to continue at low output

- Resilient demand and tighter supply drove up the oil price

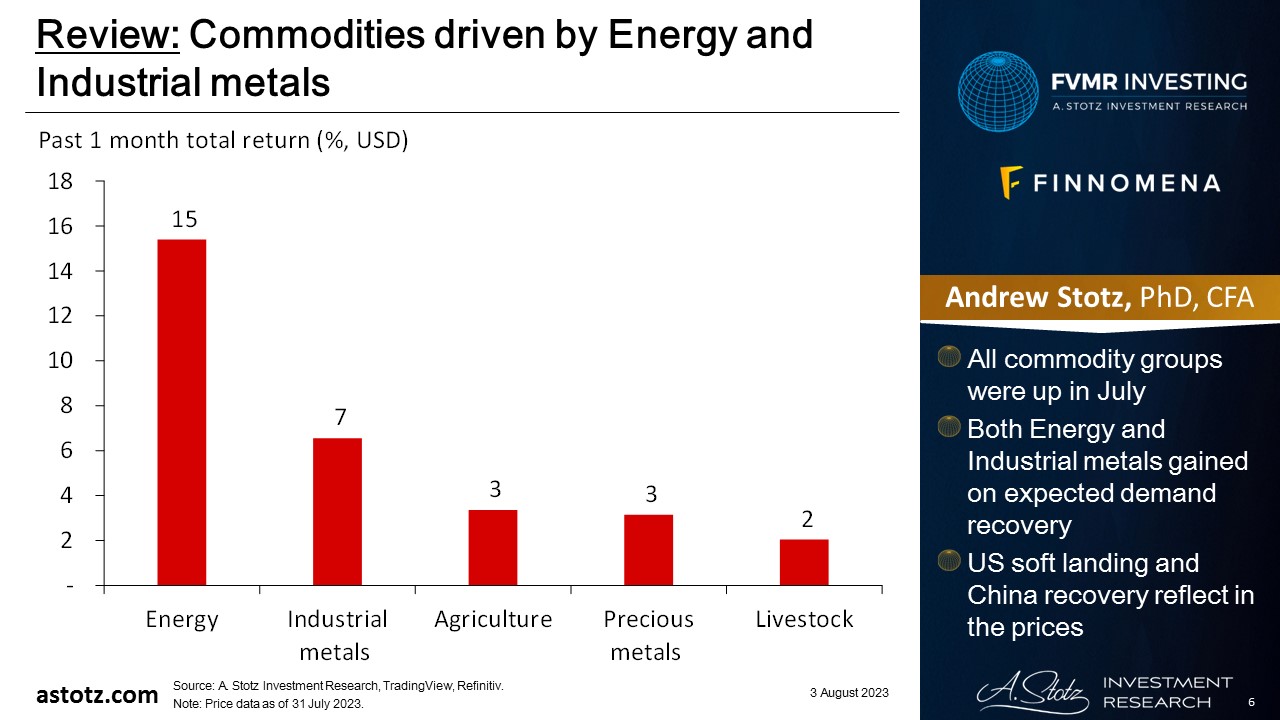

Commodities driven by Energy and Industrial metals

- All commodity groups were up in July

- Both Energy and Industrial metals gained on expected demand recovery

- US soft landing and China recovery reflect in the prices

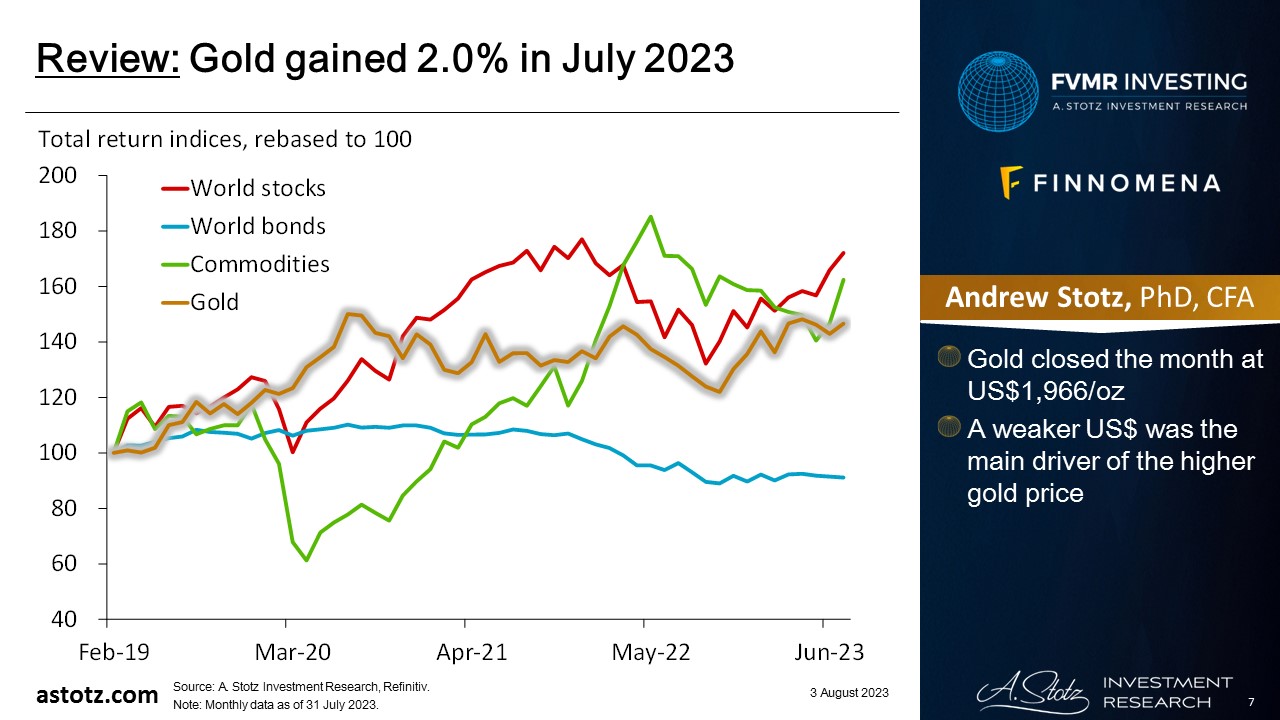

Gold gained 2.0% in July 2023

- Gold closed the month at US$1,966/oz

- A weaker US$ was the main driver of the higher gold price

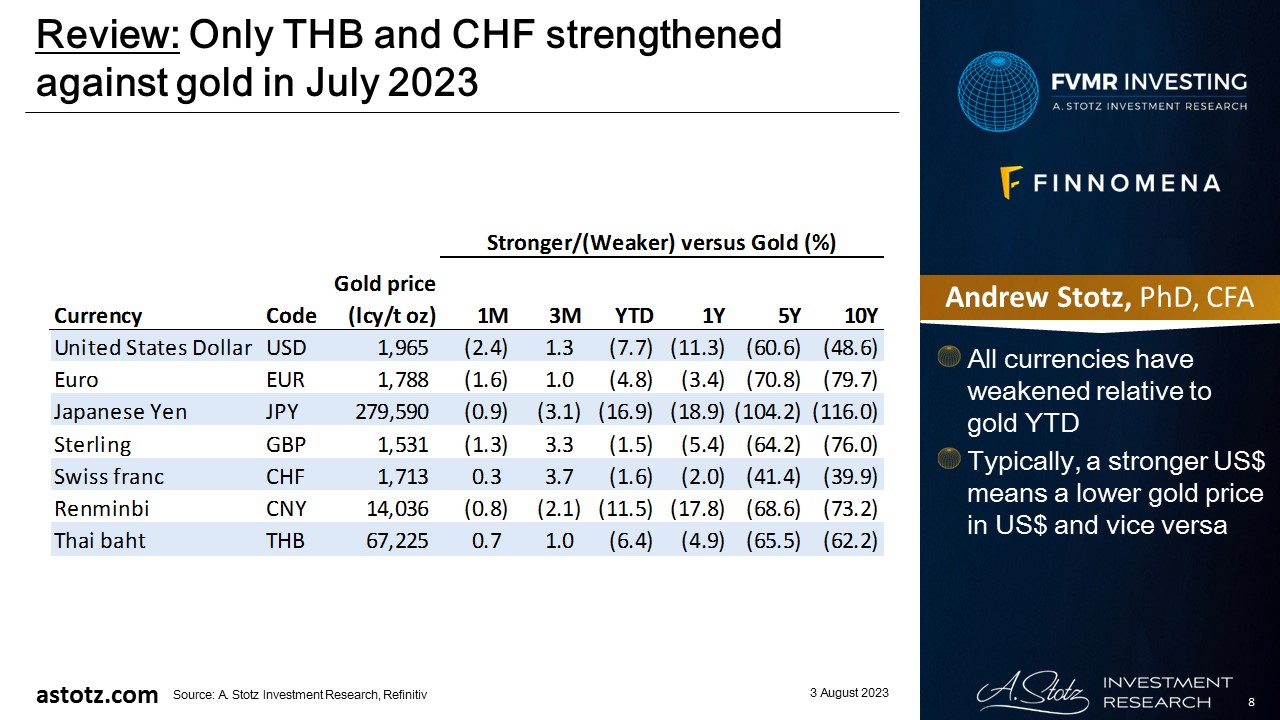

Only THB and CHF strengthened against gold in July 2023

- All currencies have weakened relative to gold YTD

- Typically, a stronger US$ means a lower gold price in US$ and vice versa

This bear market is different

S&P 500 peak in January 2022 vs. peaks in October 2007 and March 2000… pic.twitter.com/hzEqhDeAxU

— Charlie Bilello (@charliebilello) July 14, 2023

- It looks different when comparing the current bear market to Dotcom and GFC

- It’s worth remembering Sir John Templeton’s words: “The four most dangerous words in investing are: ‘This time it’s different’”

Fed hiked another 0.25% at the July FOMC meeting

BREAKING! The #FederalReserve hikes rates to 5.50%.

Taking the cumulative rate hike in this cycle to 5.25%.

From this angle, this is the biggest tightening cycle in over 40 years.

From here, the #FOMC ‘Will Continue to Assess Additional Information’ pic.twitter.com/73aMPTGod6— jeroen blokland (@jsblokland) July 26, 2023

ECB hiked 0.25% too

#ECB raises all rates by 25bps as expected. Deposit rate to 3.75%, highest since Apr2001, Main refinancing rate to 4.25%, highest since 2008. It’s 9th consecutive hike in a cycle that started exactly one year ago. APP Portfolio declining at measured & predictable pace so balance… pic.twitter.com/L4uR2XzfnY

— Holger Zschaepitz (@Schuldensuehner) July 27, 2023

US core inflation continues to fall

BREAKING: June PCE inflation, the Fed’s “preferred” inflation metric, falls to 3.0%, below expectations of 3.1%.

Core PCE inflation fell to 4.1%, below expectations of 4.2%.

PCE inflation is now at its lowest since April 2021.

The Fed may finally have inflation under control.

— The Kobeissi Letter (@KobeissiLetter) July 28, 2023

Very low earnings yield for S&P 500; hence, high valuation

Long-term investors should not touch the market even with a ten-foot pole

Earnings yield is only at 2.8%

Current valuations have marked iconic tops, like 1929 and 1966 pic.twitter.com/mLlFDgrqHN

— Game of Trades (@GameofTrades_) July 1, 2023

Americans failing to pay their credit card bills

🇺🇸 US credit card delinquency rates in Global Financial Crisis territory!

H/t: Apollo pic.twitter.com/yLBJLjP1hX

— Alex Joosten (@joosteninvestor) July 8, 2023

Key takeaways

- This bear market is different (or is it?)

- Fed hiked another 0.25% at July meeting

- ECB hiked 0.25% too

- US core inflation continues to fall

- Very low earnings yield for S&P 500

- Americans fail to pay their credit card bills

Performance review: All Weather Inflation Guard

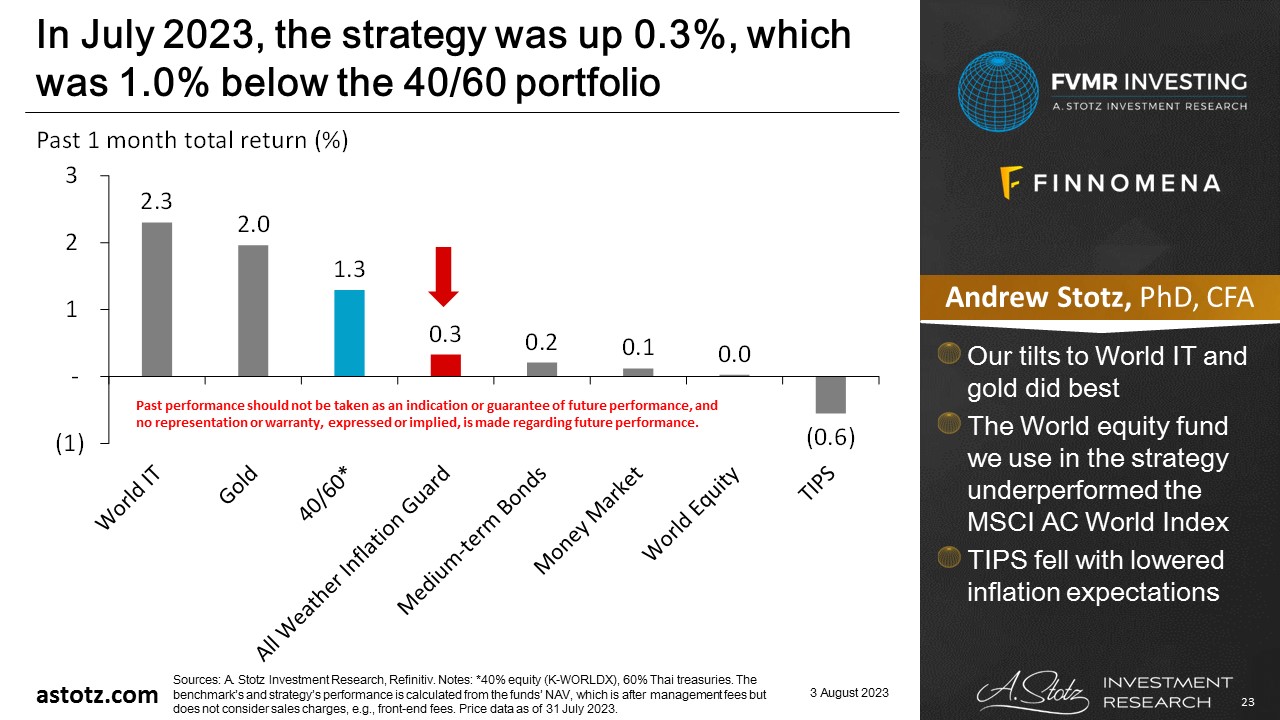

All Weather Inflation Guard was up 0.3%

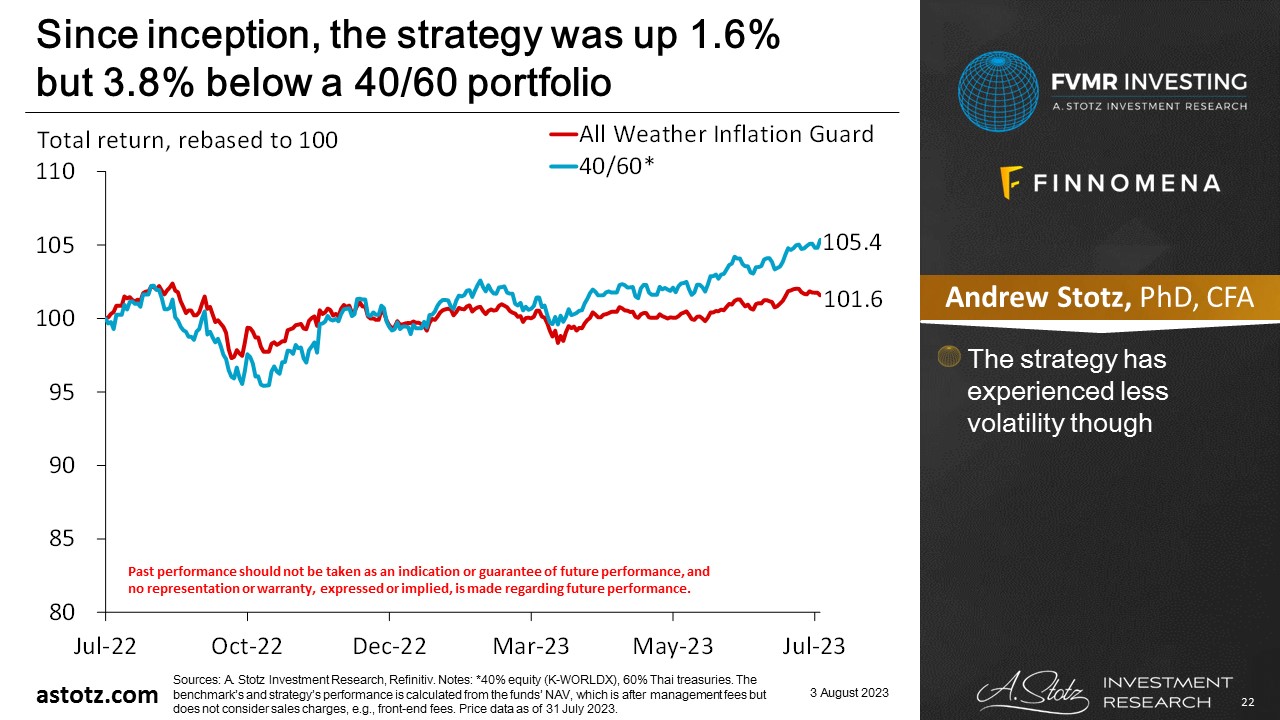

Since inception, the strategy was up 1.6% but 3.8% below a 40/60 portfolio

- The strategy has experienced less volatility though

In July 2023, the strategy was up 0.3%, which was 1.0% below the 40/60 portfolio

- Our tilts to World IT and gold did best

- The World equity fund we use in the strategy underperformed the MSCI AC World Index

- TIPS fell with lowered inflation expectations

Performance review: All Weather Strategy

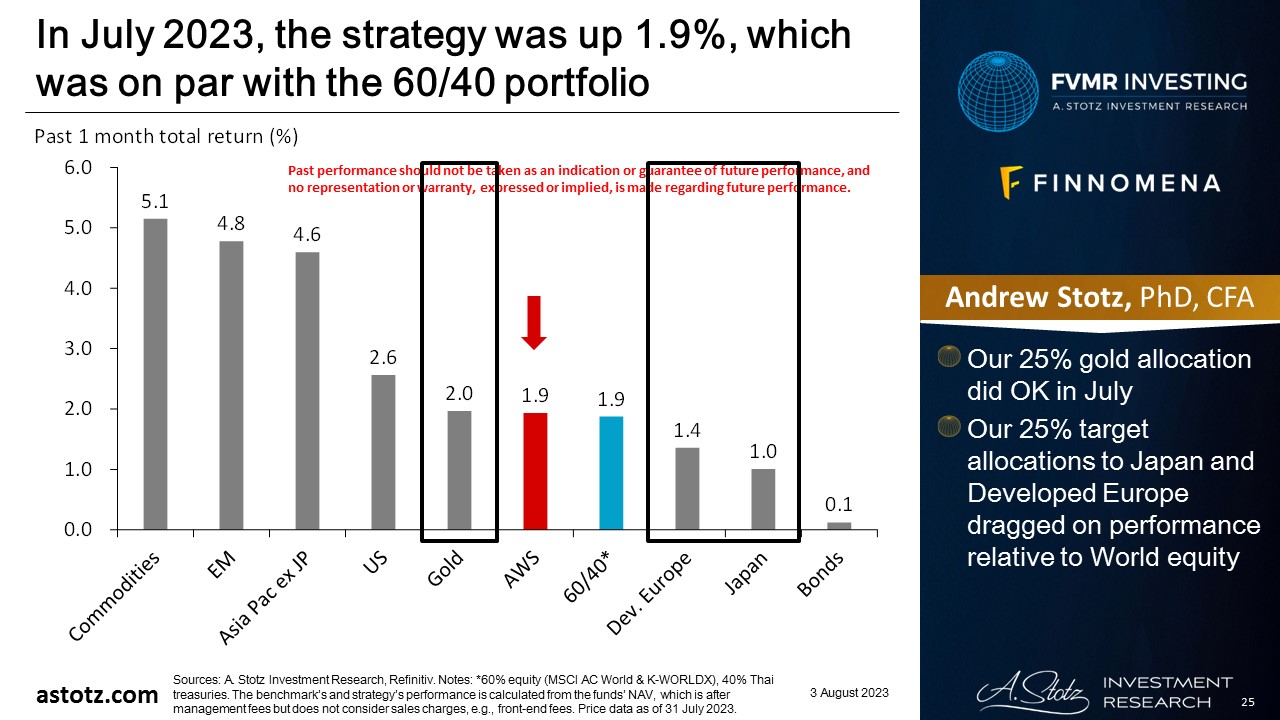

All Weather Strategy was up 1.9%

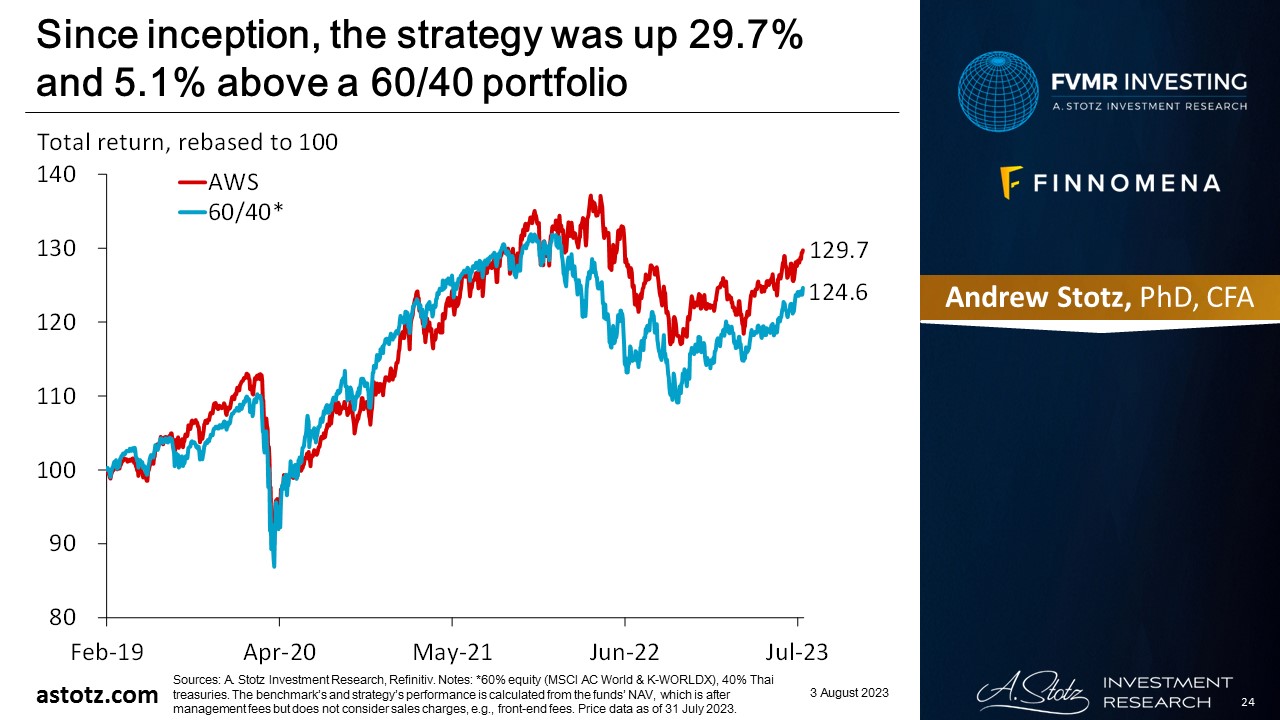

Since inception, the strategy was up 29.7% and 5.1% above a 60/40 portfolio

In July 2023, the strategy was up 1.9%, which was on par with the 60/40 portfolio

- Our 25% gold allocation did OK in July

- Our 25% target allocations to Japan and Developed Europe dragged on performance relative to World equity

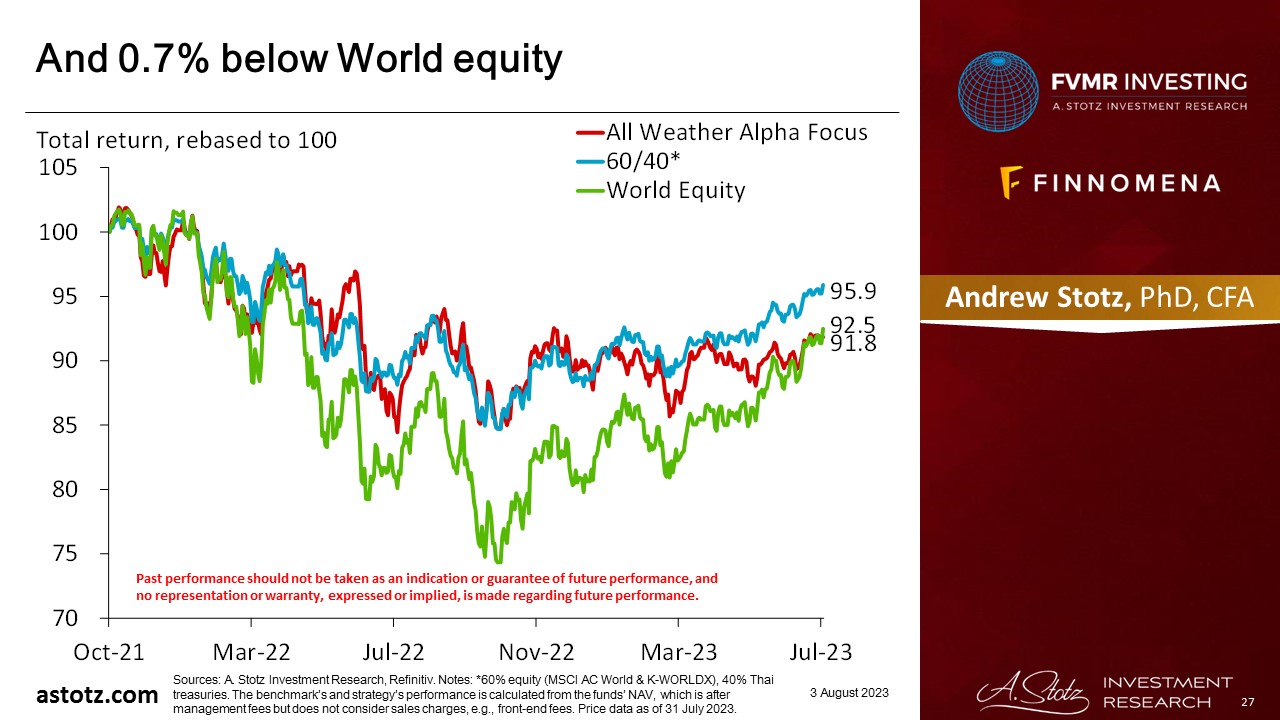

Performance review: All Weather Alpha Focus

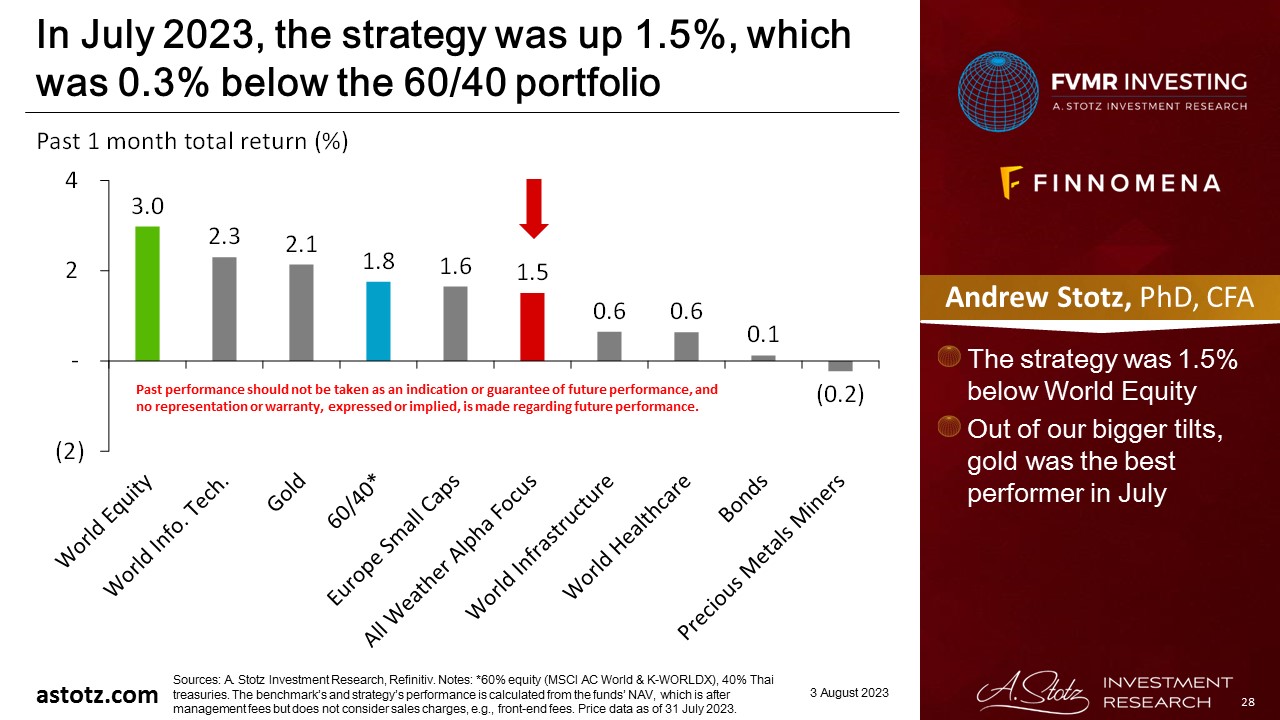

All Weather Alpha Focus was up 1.5%

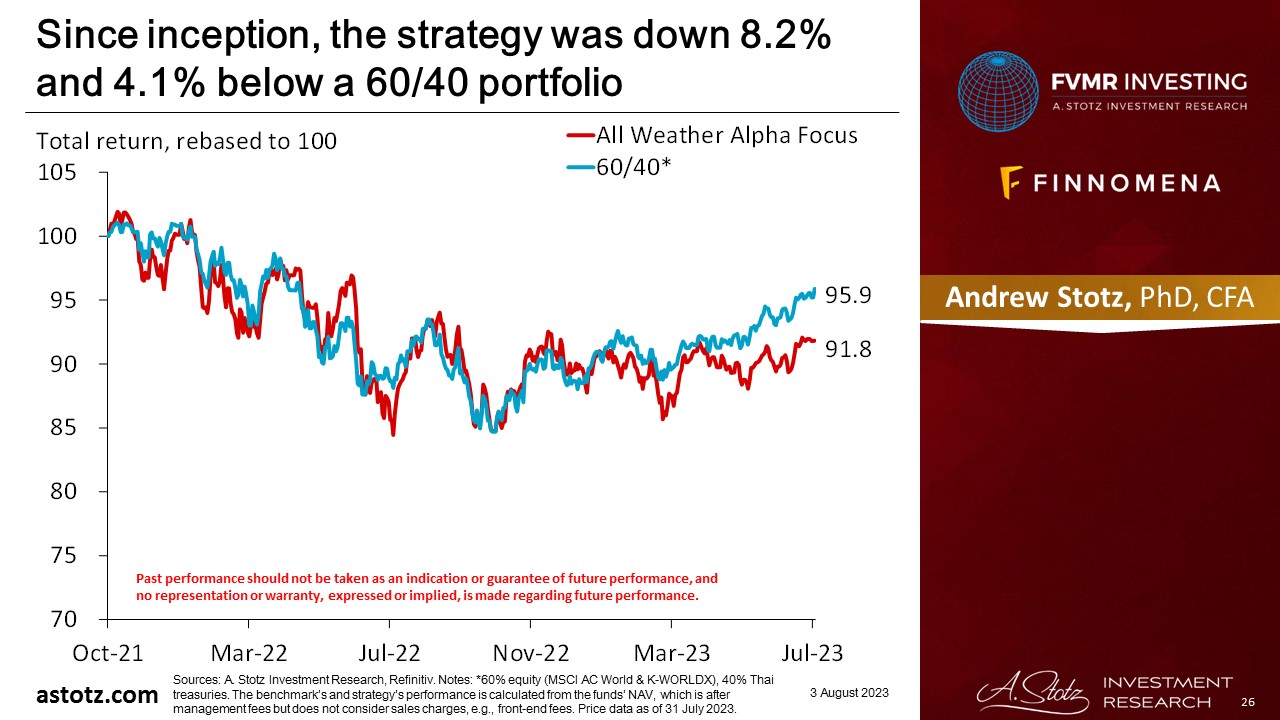

Since inception, the strategy was down 8.2% and 4.1% below a 60/40 portfolio

And 0.7% below World equity

In July 2023, the strategy was up 1.5%, which was 0.3% below the 60/40 portfolio

- The strategy was 1.5% below World Equity

- Out of our bigger tilts, gold was the best performer in July

Global outlook that guides our asset allocation

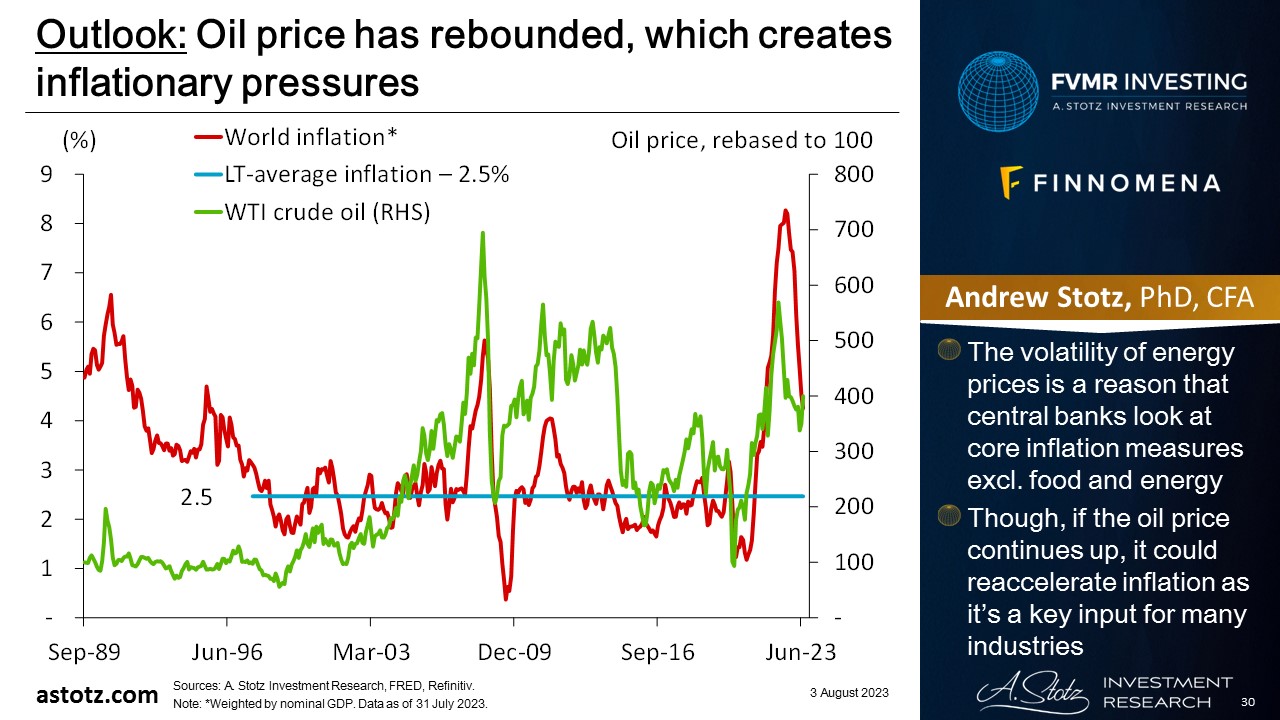

Oil price has rebounded, which creates inflationary pressures

- The volatility of energy prices is a reason that central banks look at core inflation measures excl. food and energy

- Though, if the oil price continues up, it could reaccelerate inflation as it’s a key input for many industries

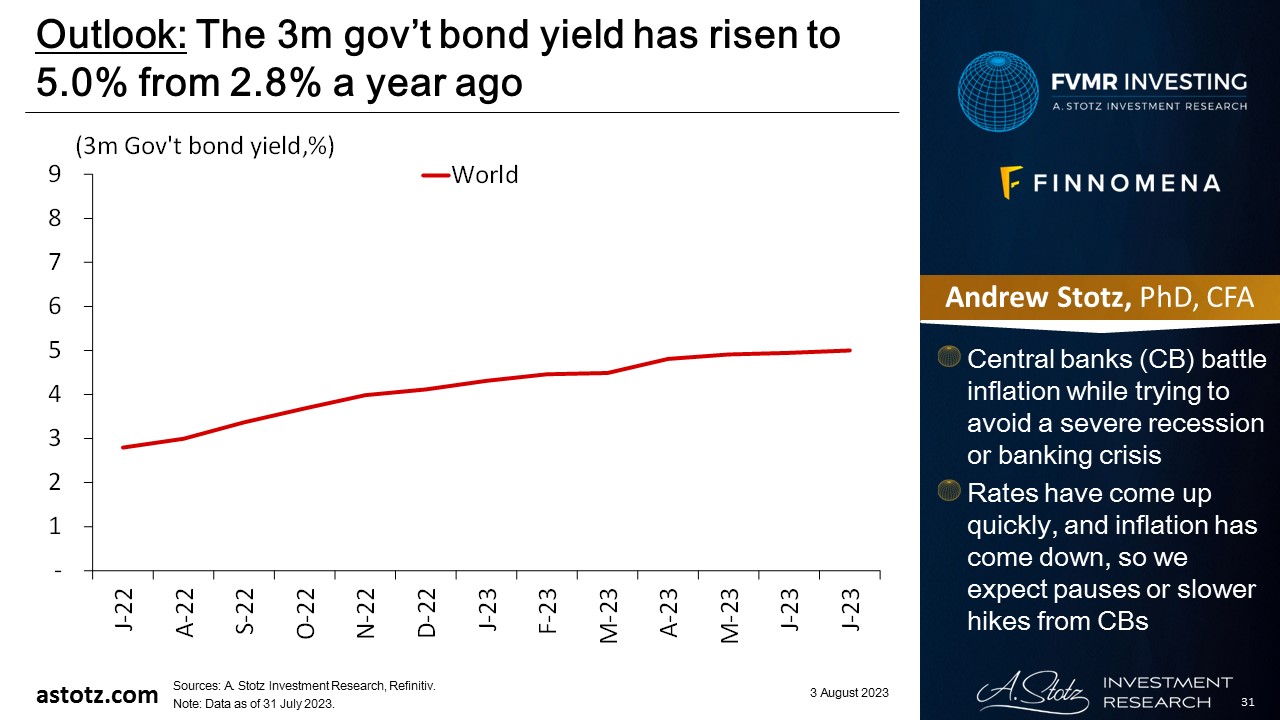

The 3m gov’t bond yield has risen to 5.0% from 2.8% a year ago

- Central banks (CB) battle inflation while trying to avoid a severe recession or banking crisis

- Rates have come up quickly, and inflation has come down, so we expect pauses or slower hikes from CBs

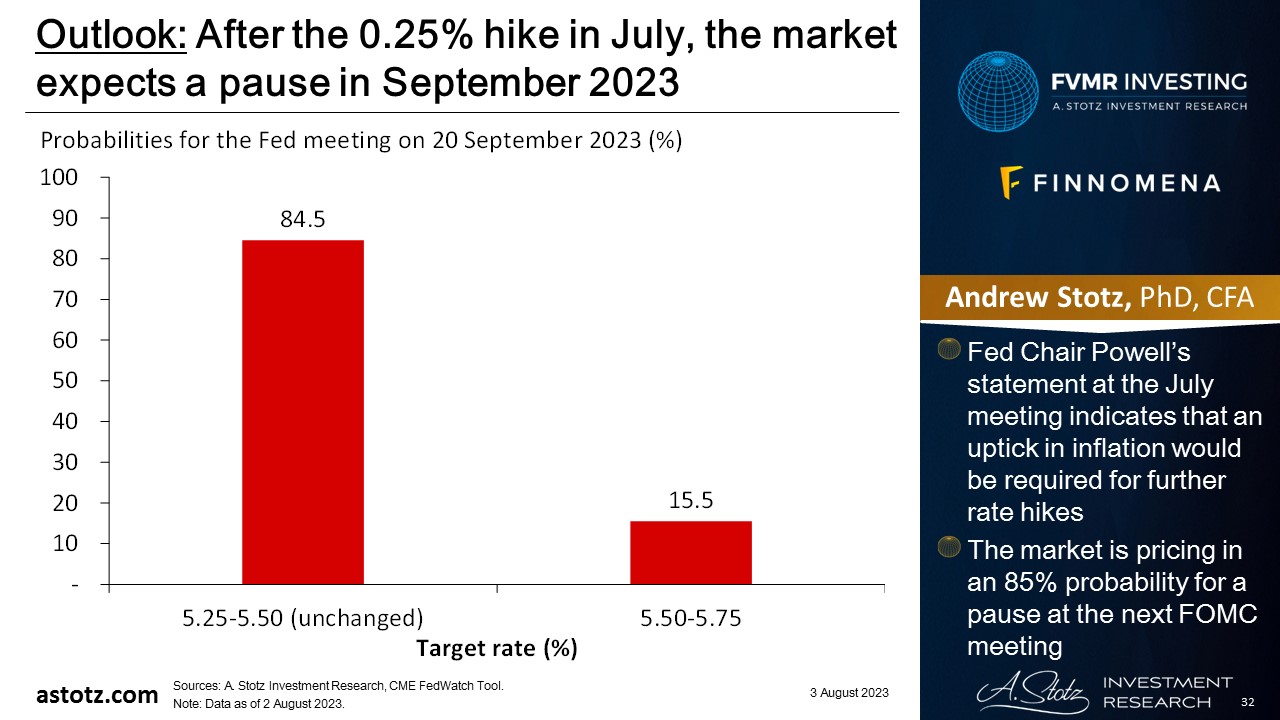

After the 0.25% hike in July, the market expects a pause in September 2023

- Fed Chair Powell’s statement at the July meeting indicates that an uptick in inflation would be required for further rate hikes

- The market is pricing in an 85% probability for a pause at the next FOMC meeting

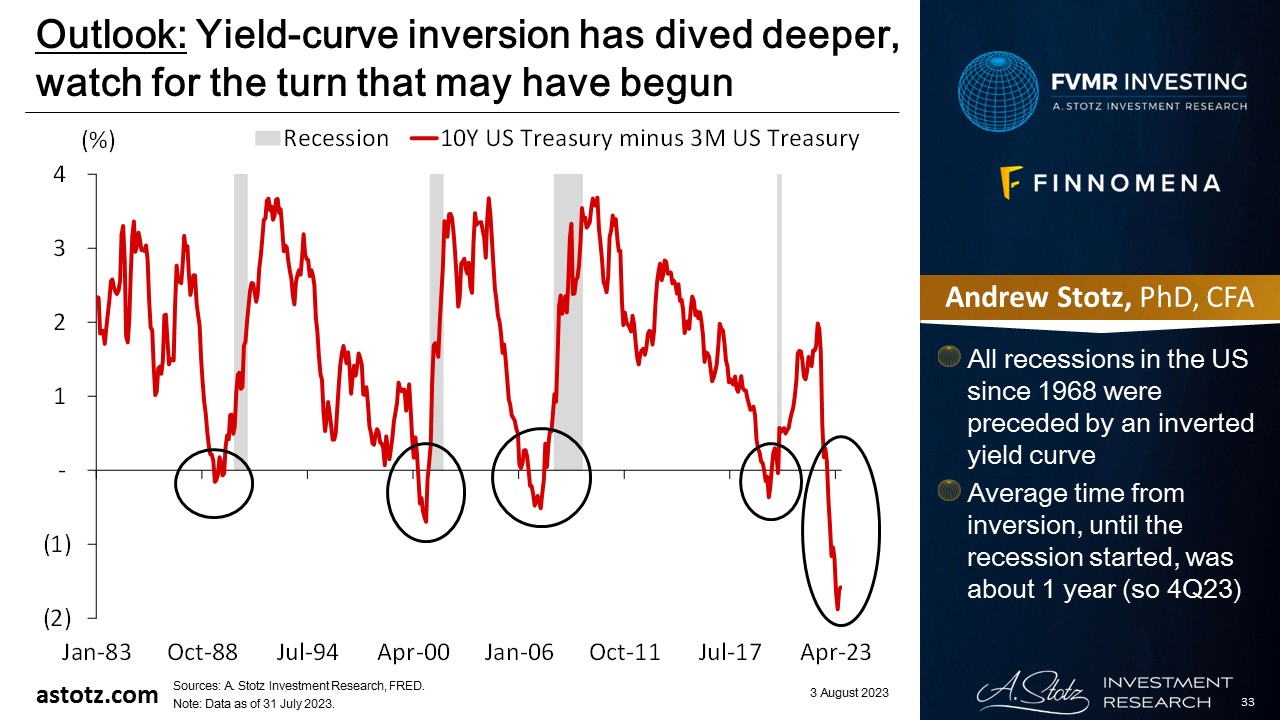

Yield-curve inversion has dived deeper, watch for the turn that may have begun

- All recessions in the US since 1968 were preceded by an inverted yield curve

- Average time from inversion, until the recession started, was about 1 year (so 4Q23)

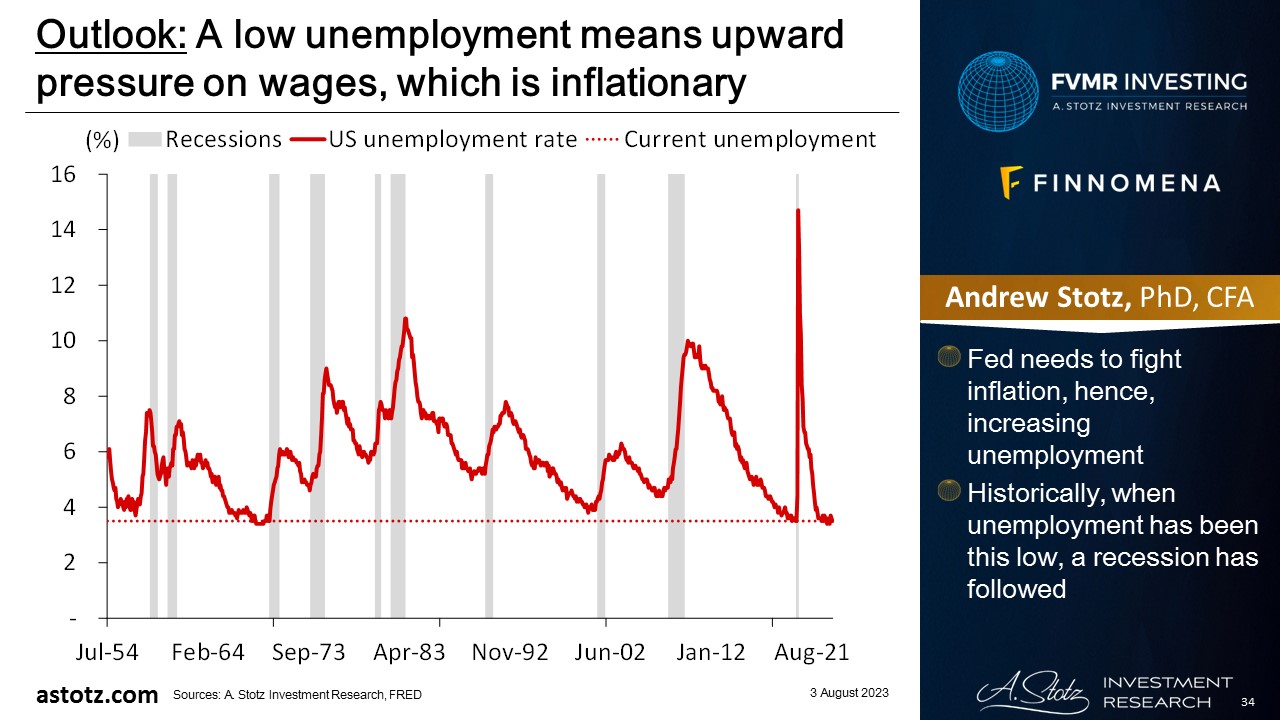

A low unemployment means upward pressure on wages, which is inflationary

- Fed needs to fight inflation, hence, increasing unemployment

- Historically, when unemployment has been this low, a recession has followed

Valuations have risen, as price has rebounded YTD

- World stocks’ valuation is now above its long-term average

- The consensus net margin has come down a bit, and analysts have revised it down again recently

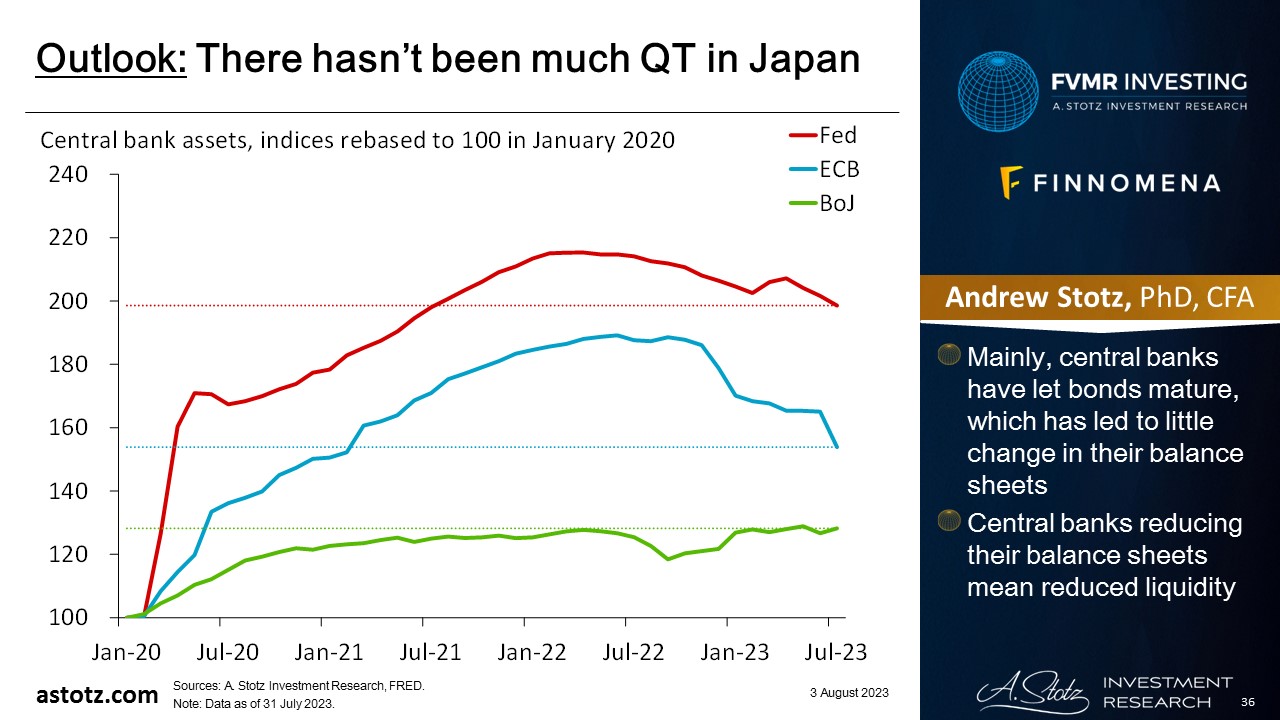

There hasn’t been much QT in Japan

- Mainly, central banks have let bonds mature, which has led to little change in their balance sheets

- Central banks reducing their balance sheets mean reduced liquidity

For the past year, we’ve said that we think the course will eventually be reversed

- We still think central bankers and politicians will change course and return to accommodative policies as soon as something “breaks”

- And we do think central bankers are going to break things

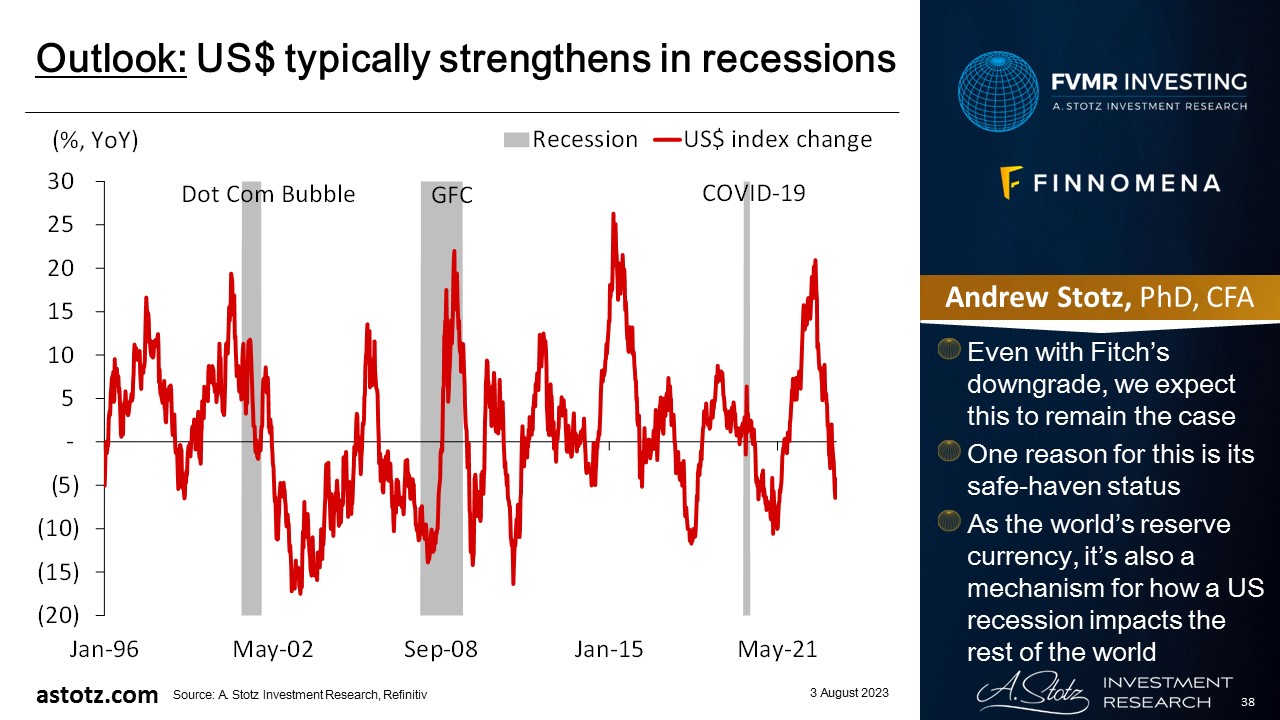

US$ typically strengthens in recessions

- Even with Fitch’s downgrade, we expect this to remain the case

- One reason for this is its safe-haven status

- As the world’s reserve currency, it’s also a mechanism for how a US recession impacts the rest of the world

Bonds are typically a safe place to be

- In recessions, safer assets like government bonds typically have performed well

- Though with high inflation, low yields could still lead to negative real returns

- We generally don’t allocate to bonds to speculate on the upside but rather use it to protect capital over time

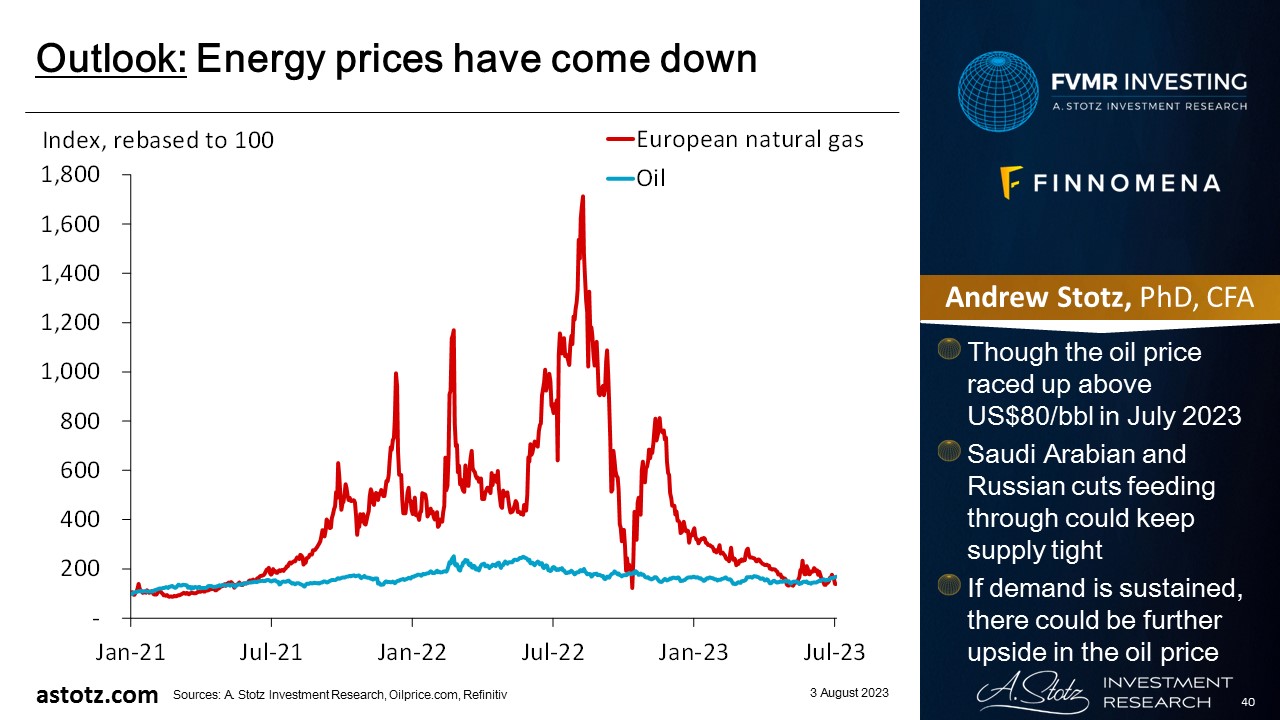

Energy prices have come down

- Though the oil price raced up above US$80/bbl in July 2023

- Saudi Arabian and Russian cuts feeding through could keep supply tight

- If demand is sustained, there could be further upside in the oil price

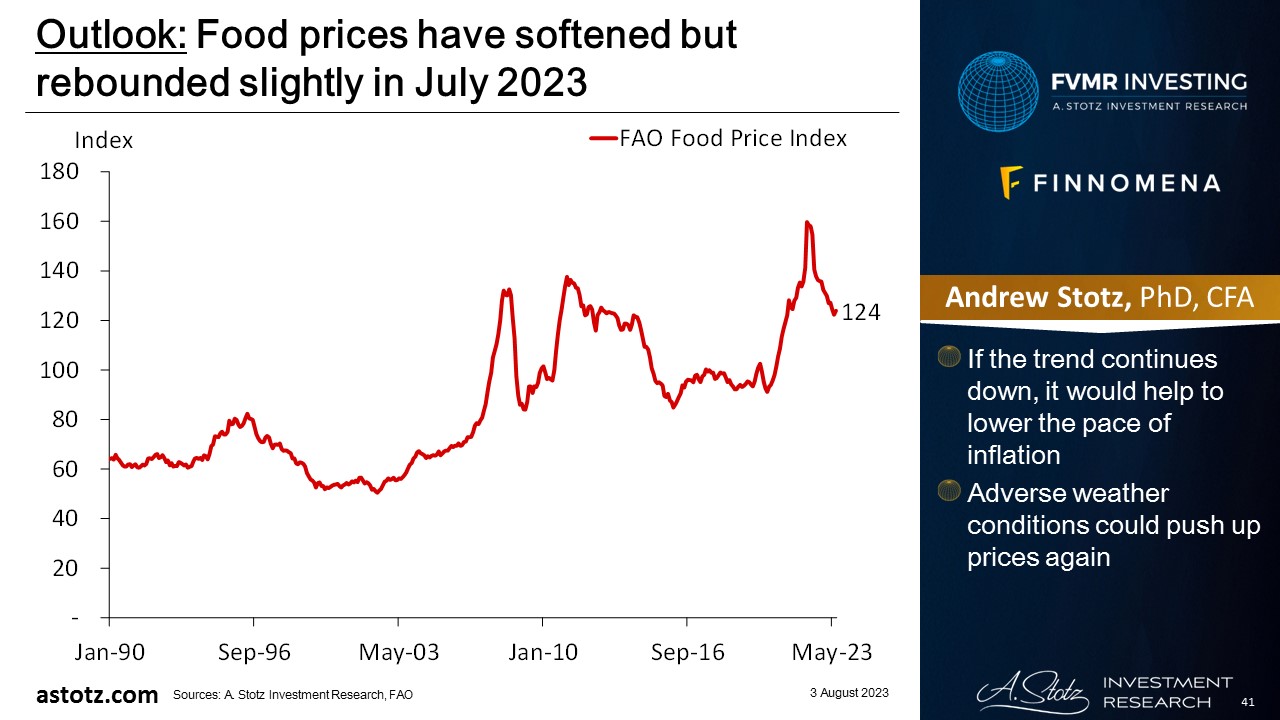

Food prices have softened but rebounded slightly in July 2023

- If the trend continues down, it would help to lower the pace of inflation

- Adverse weather conditions could push up prices again

Commodities have rebounded, but too early to call the turn

- The global economic growth outlook remains uncertain

- The main upside in commodities would come from a supply shock, adverse weather conditions, or significantly higher demand due to an improved growth outlook

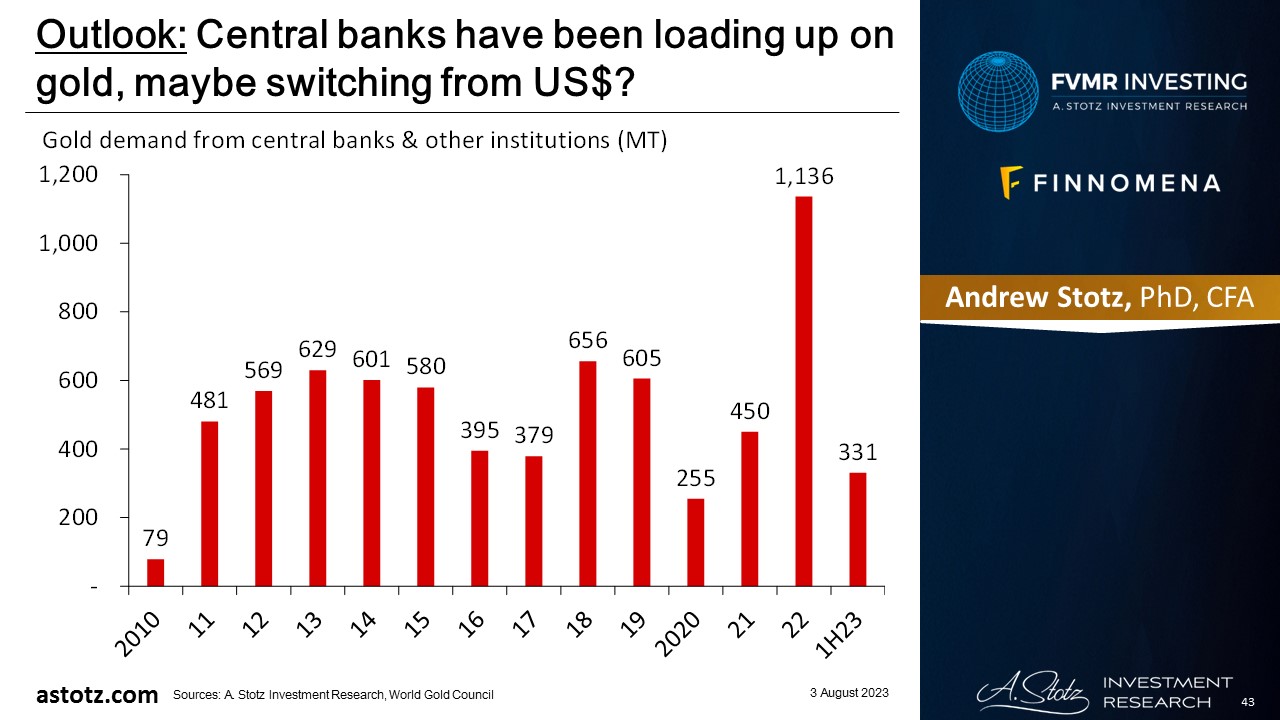

Central banks have been loading up on gold, maybe switching from US$?

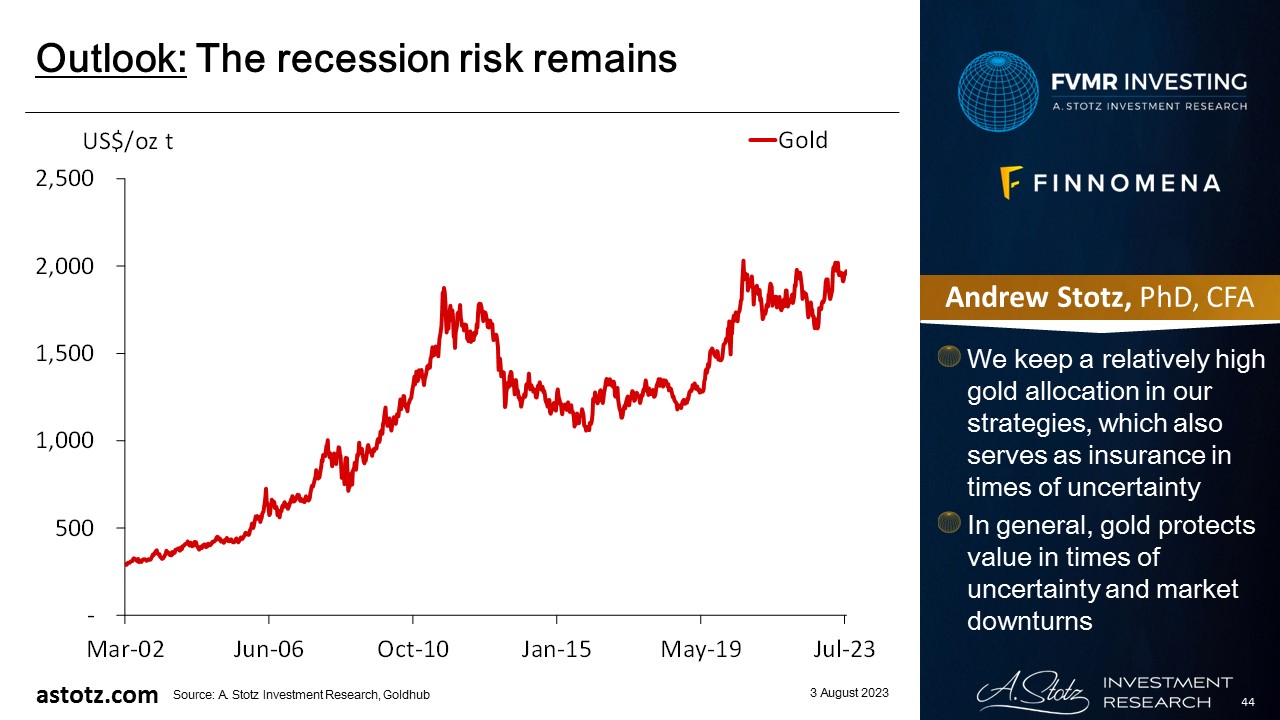

The recession risk remains

- We keep a relatively high gold allocation in our strategies, which also serves as insurance in times of uncertainty

- In general, gold protects value in times of uncertainty and market downturns

Risk: Inflation reaccelerates

- Central banks’ aggressive rate hikes and QT crash the stock markets

- If inflation reaccelerates, we could miss out on rising commodities prices

- Our high gold allocation could get hit by higher rates or improved market sentiment

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.