A. Stotz All Weather Strategies – January 2023

Executive summary

- Central bankers appear to be raising rates into a recession to stifle inflation; stagflation would be the worst outcome

- Demand for necessities (food and energy), inflation, and supply-chain disruptions can drive commodities higher

- We see opportunities to allocate to specific sectors and markets within equity

- Bonds and gold to protect capital

- Risks: Global recession, collapsing energy prices, weak China

The All Weather Strategy is available in Thailand through FINNOMENA. If you’re interested in our allocation strategy, you can also join the Become a Better Investor Community. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

What happened in world markets in January 2023

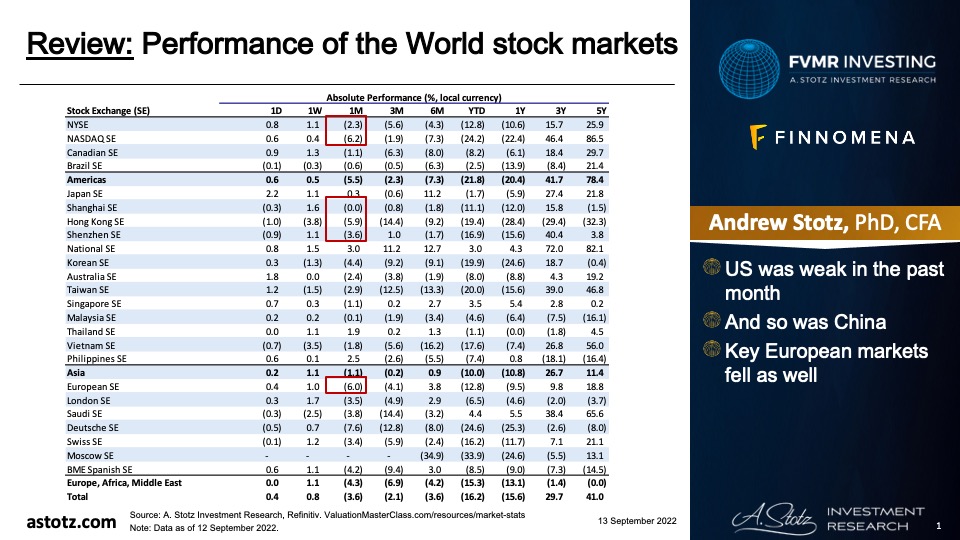

Performance of the World stock markets

- Broad market recovery in January 2023

- NASDAQ saw double-digit returns in the US

- China was up, Hong Kong up by 10%

- The European market recovered strongly

Find the updated Performance of the World stock markets here.

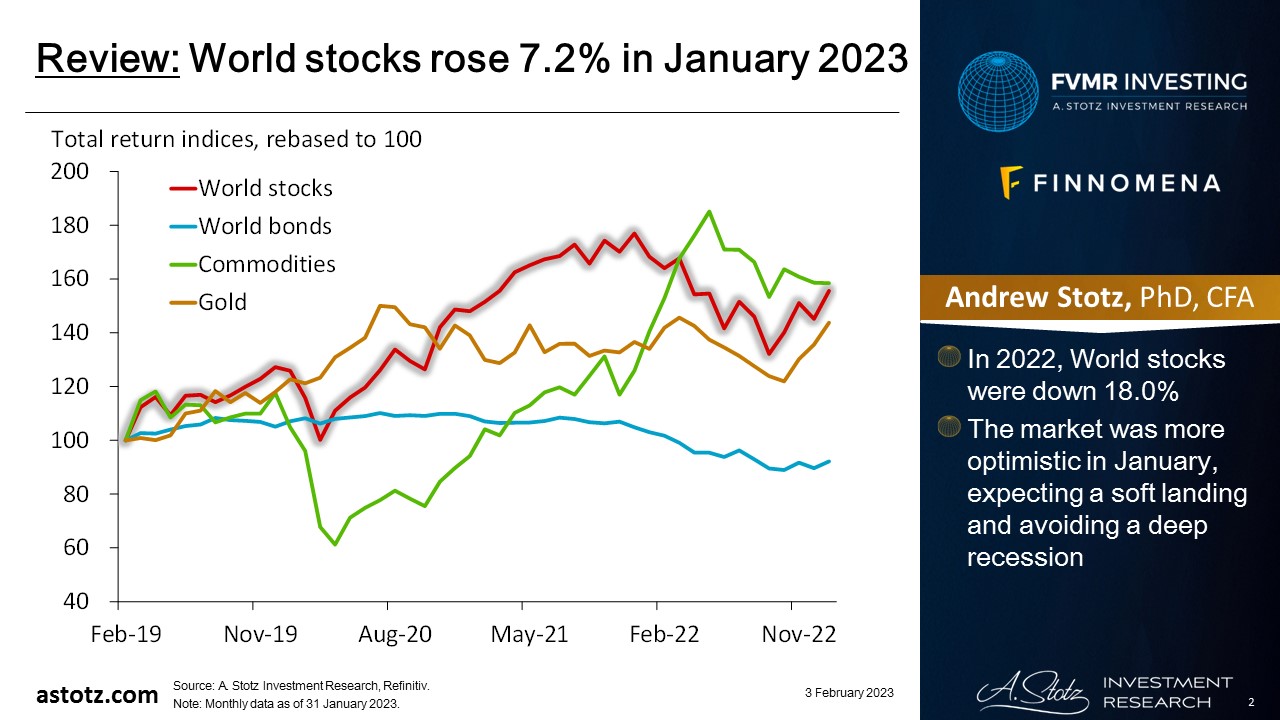

World stocks rose 7.2% in January 2023

- In 2022, World stocks were down 18.0%

- The market was more optimistic in January, expecting a soft landing and avoiding a deep recession

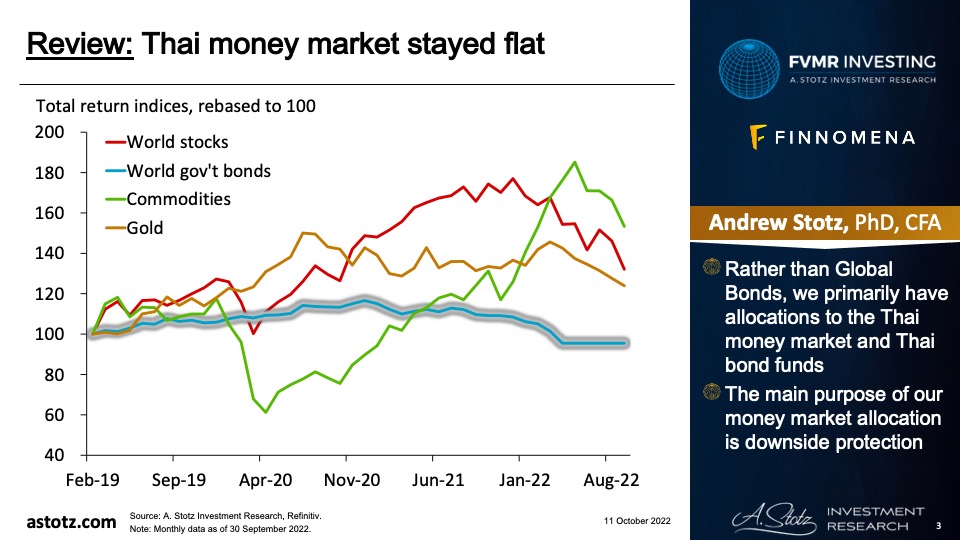

Global bonds were up in January 2023

- Rather than global bonds, we have target allocations to the Thai money market, which was flat as expected

- The main purpose of our money market allocation is downside protection

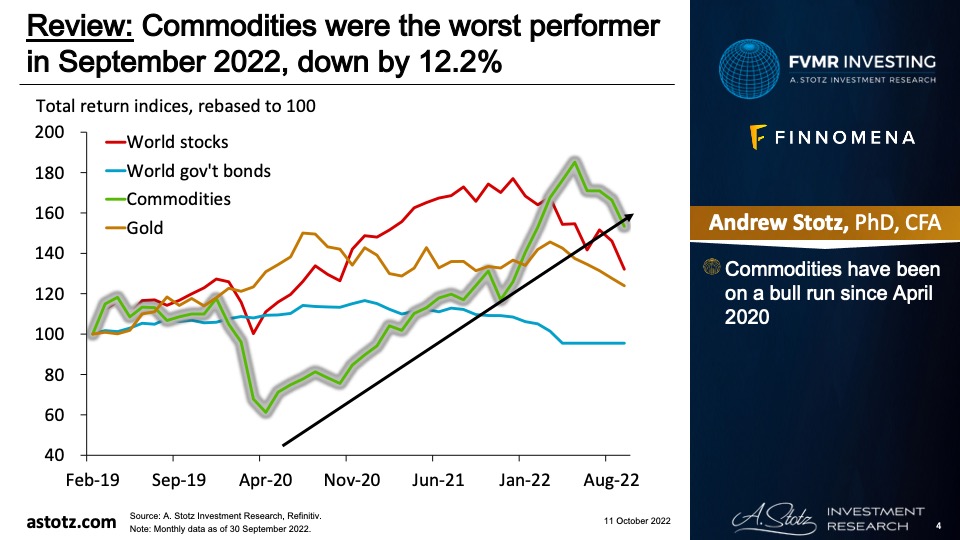

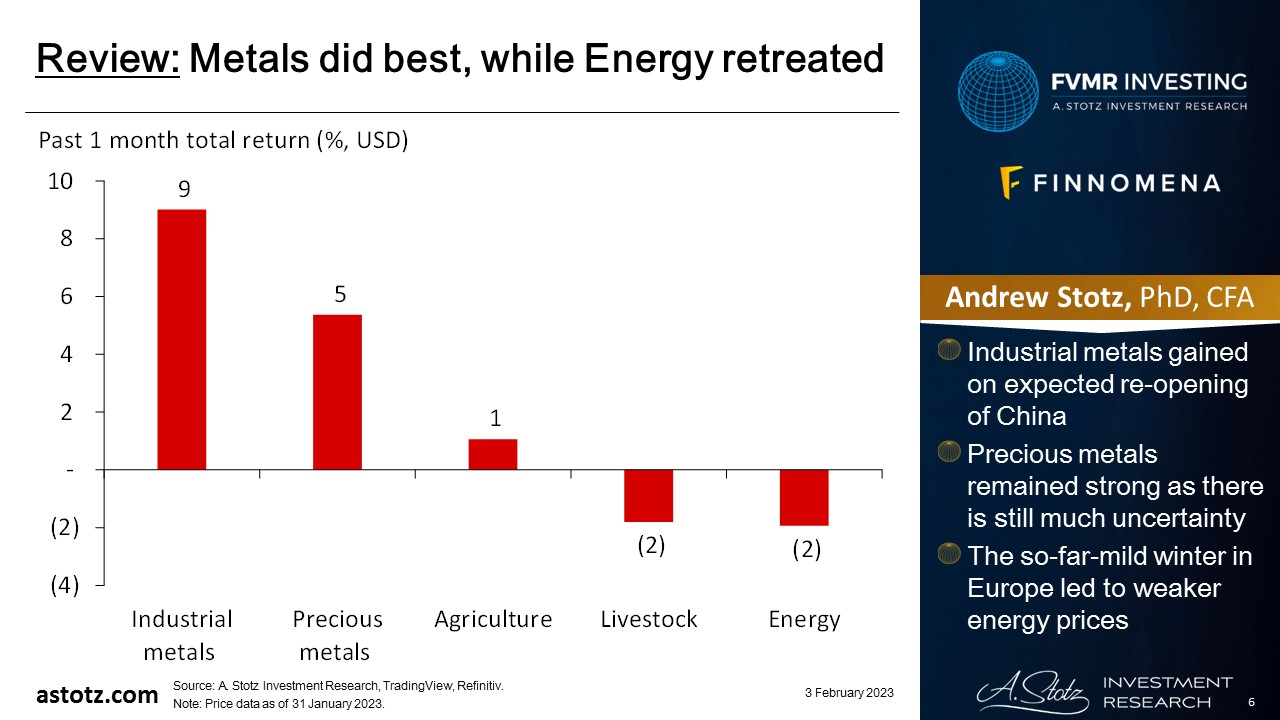

Commodities underperformed in January 2023 and lost 0.8%

WTI oil closed January 2023 at US$79/bbl

Metals did best, while Energy retreated

- Industrial metals gained on expected re-opening of China

- Precious metals remained strong as there is still much uncertainty

- The so-far-mild winter in Europe led to weaker energy prices

Gold was up by 3.6% in January 2023

- Gold closed the month at US$1,928/oz

- Uncertainty remains high in the markets, which has led to continued momentum in gold

All currencies weakened against gold in January 2023

- Typically, a stronger US$ means a lower gold price in US$ and vice versa

2022 was an awful year for a stock + bond portfolio

5/5

Combined stocks and bonds together, and Yale’s Bob Shiller, via the Financial Times, says 2022 was the worst year for investors since 1871!

Note only three years in the last 150 in the lower left quadrant.https://t.co/7Wfoc0mmyc pic.twitter.com/k1ze8Sy6yF

— Jim Bianco biancoresearch.eth (@biancoresearch) December 31, 2022

- Looking at the returns of stocks and bonds, 2022 was the worst year since 1871

While the American mortgage rate has retreated, it’s still at levels not seen for a decade

The 30-year US mortgage rate has moved from 7.08% to 6.13% over the last 11 weeks, the largest 11-week decline (-95 bps) in rates since January 2009. pic.twitter.com/tSxePBy6US

— Charlie Bilello (@charliebilello) January 26, 2023

- People are reminded what it feels like to have to pay interest on their loans

- As of Jan 31, 2023, it has fallen only to 6.13%

The most expected recession in history

The most expected recession in history?

Yep, probably.

I am hearing that’s exactly the reason why it’s not going to happen.

So let me ask you.

Everybody expects the sun to rise from East tomorrow.

Does that imply there is a higher chance it rises from West instead? pic.twitter.com/kH9FjtKdZe

— Alf (@MacroAlf) January 10, 2023

- Some say the recession won’t happen just because it’s highly anticipated

- Alf points out a flaw in this line of thinking

We’ve heard about soft landing before

In late 2007, the Fed and major US banks were predicting a soft landing. pic.twitter.com/o94TVxmLnC

— Alf (@MacroAlf) January 29, 2023

- A reminder that even when a soft landing seems likely, it can change rapidly

- In 2007, Fed Chair Bernanke, said that the subprime mortgage market was contained

What happens in the US matters for the rest of the world

Remember the last time the US went into a recession and the Rest of the Worlds developed and emerging markets experienced prosperity and growth?

Yea… pic.twitter.com/msoGosNXsx

— Santiago Capital (@SantiagoAuFund) January 26, 2023

- Typically, a US recession means the world will follow

- That’s why much focus is spent on what’s going on “over there.”

US inflation continued to fall

US CPI has moved down from a peak of 9.1% last June to 6.5% in December.

What’s driving that decline? Lower rates of inflation in New/Used Cars, Gasoline, Apparel, Medical Care, Food at Home, Gas Utilities, and Fuel Oil. pic.twitter.com/be5eDz1Jh7

— Charlie Bilello (@charliebilello) January 12, 2023

- Lower prices for cars, fuel, apparel, medical care, and food at home were the main items that saw deflation or lower inflation rates

US equity risk premium is at a decade low

Worth noting that this is THE worst implied risk compensation in equities since 2007 pic.twitter.com/15PuUxmXRe

— AndreasStenoLarsen (@AndreasSteno) January 31, 2023

- The return on stocks, measured as earnings yield, is just slightly above the risk-free rate

- Hence, you don’t get very well compensated for taking on equity risk

Key takeaways

- 2022 was exceptionally bad for a mixed stocks and bond portfolio

- Market participants highly anticipate a recession, the question is, “Does that mean it won’t appear?”

- History could be repeat as there was a soft-landing narrative before the Global Financial Crisis too

- US equity risk premium at a decade low, so, you are not well compensated for the risk

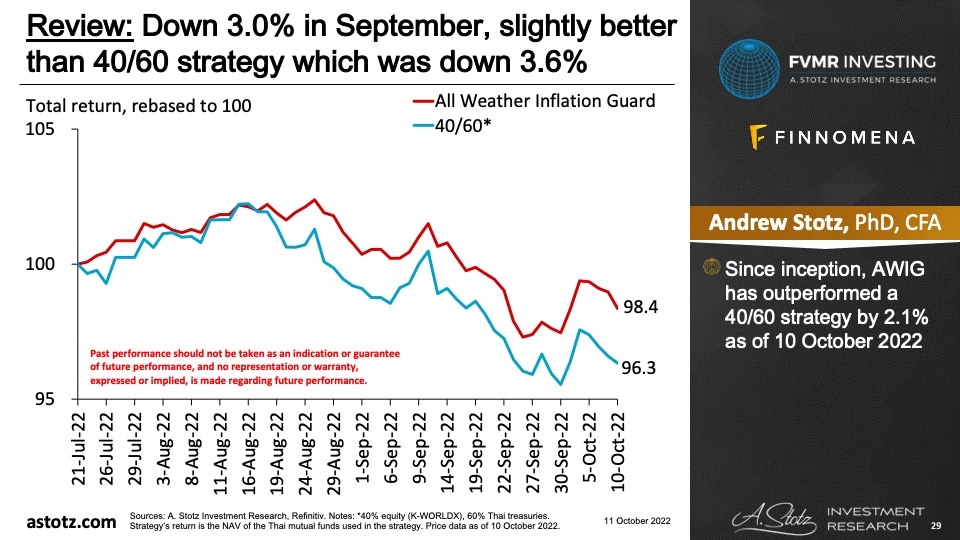

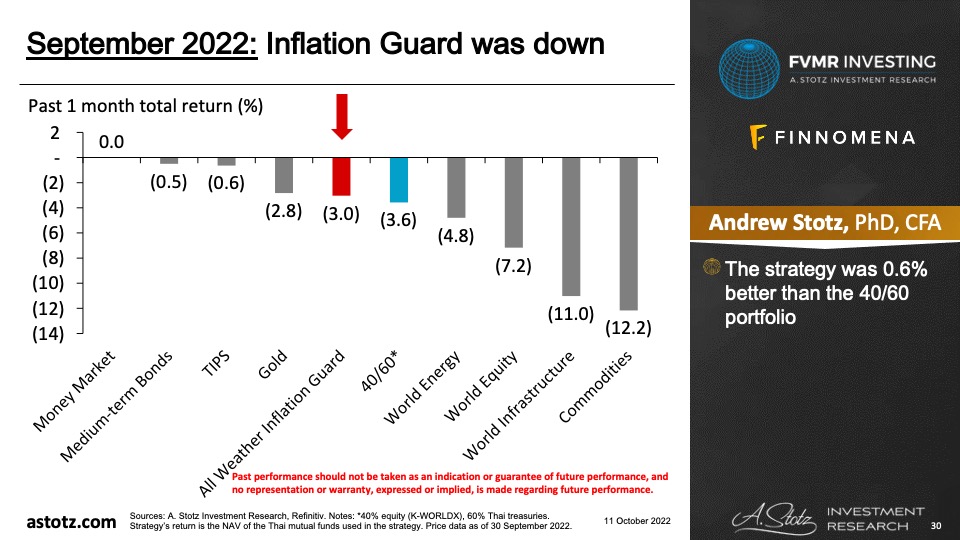

Performance review: All Weather Inflation Guard

All Weather Inflation Guard rose by 0.9%

- Since inception, the strategy is up 0.6% and has underperformed a 40/60 strategy by 1.3%

- The strategy has experienced less volatility though

The strategy was 1.7% below the 40/60 portfolio

- Though the strategy rose by 0.9% in January 2023 as markets rebounded

- Our allocations to healthcare, commodities, and energy dragged on the performance

- The world equity fund lagged the MSCI AC World index

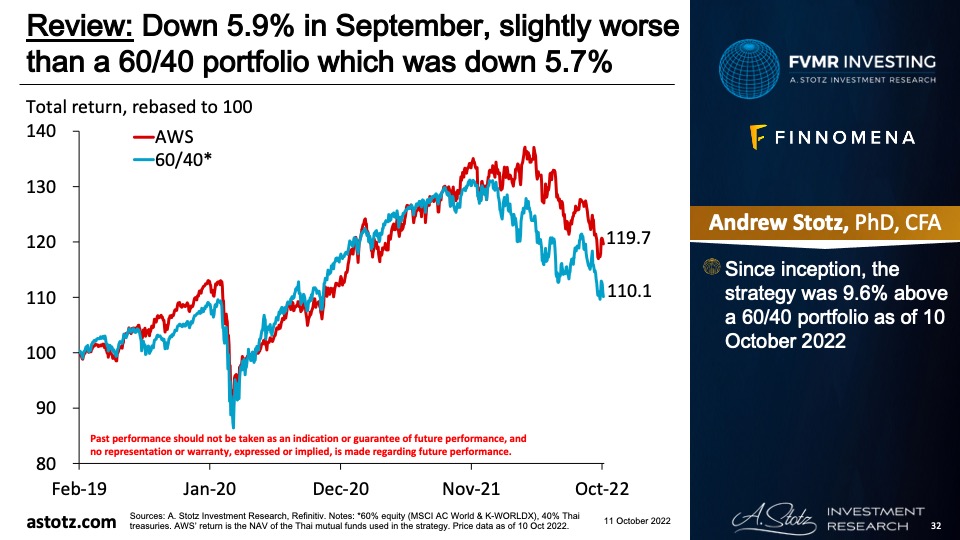

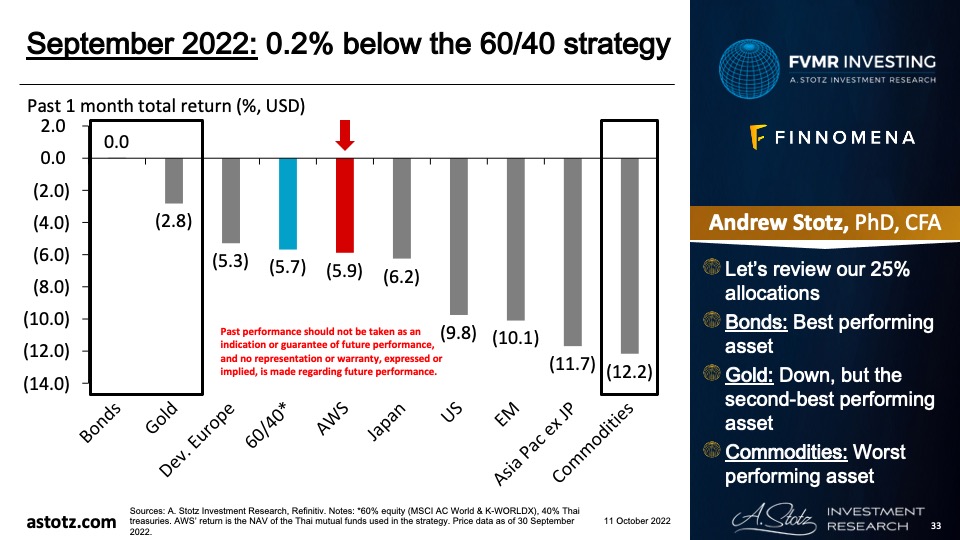

Performance review: All Weather Strategy

All Weather Strategy rose by 2.2%

- Since inception, the strategy was 6.0% above a 60/40 portfolio by the end of January 2023

The strategy was 1.7% below the 60/40 portfolio

- Our low 25% allocation to equity was a major cause of underperformance in January 2023

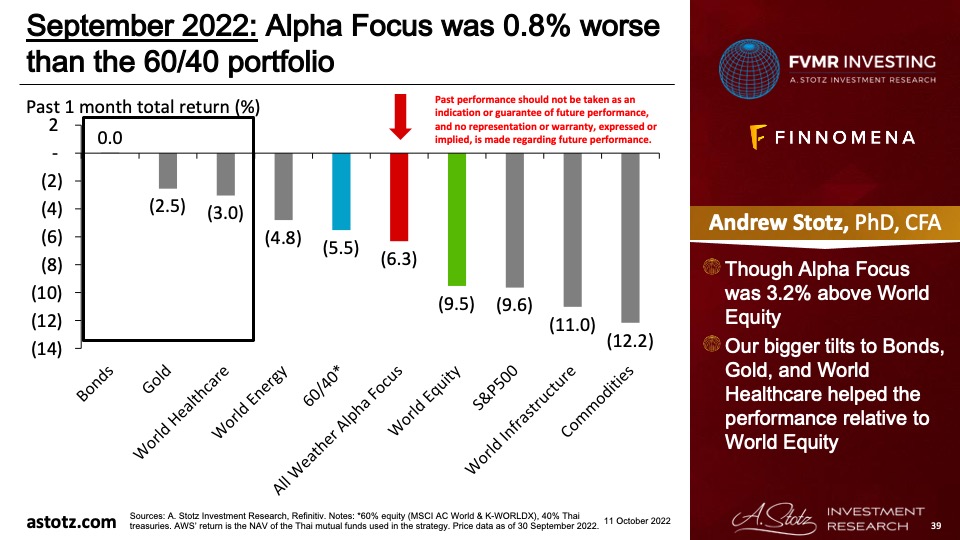

Performance review: All Weather Alpha Focus

All Weather Alpha Focus rose by 1.1%

- Since inception, the strategy was 1.1% below the 60/40 portfolio as of 31 January 2023

The strategy has done better than World equity since inception

- Since inception, the strategy was 4.7% above World equity as of 31 January 2023

The strategy was 2.5% below the 60/40 portfolio

- The strategy was 5.5% below World Equity

- Our 22% tilt to India, Commodities, and World Energy led to the underperformance

Global outlook that guides our asset allocation

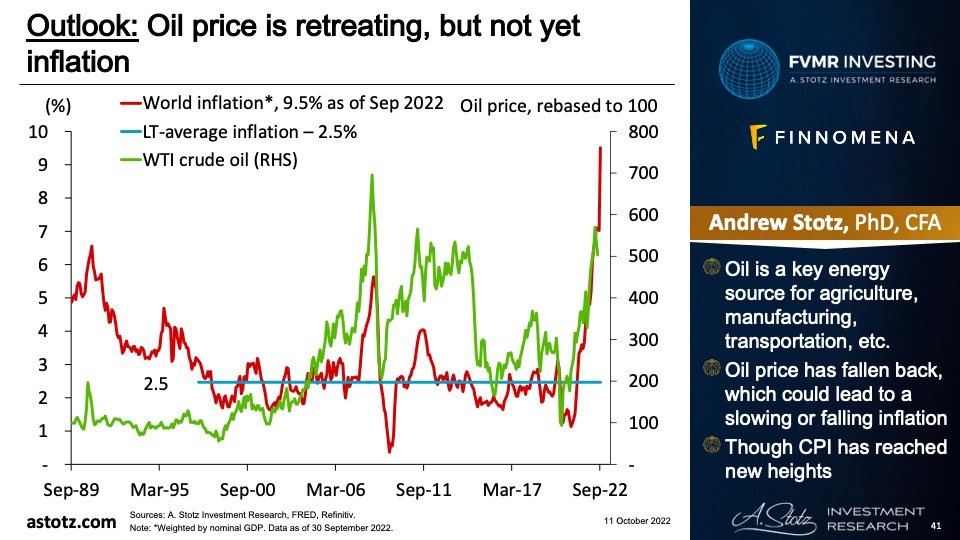

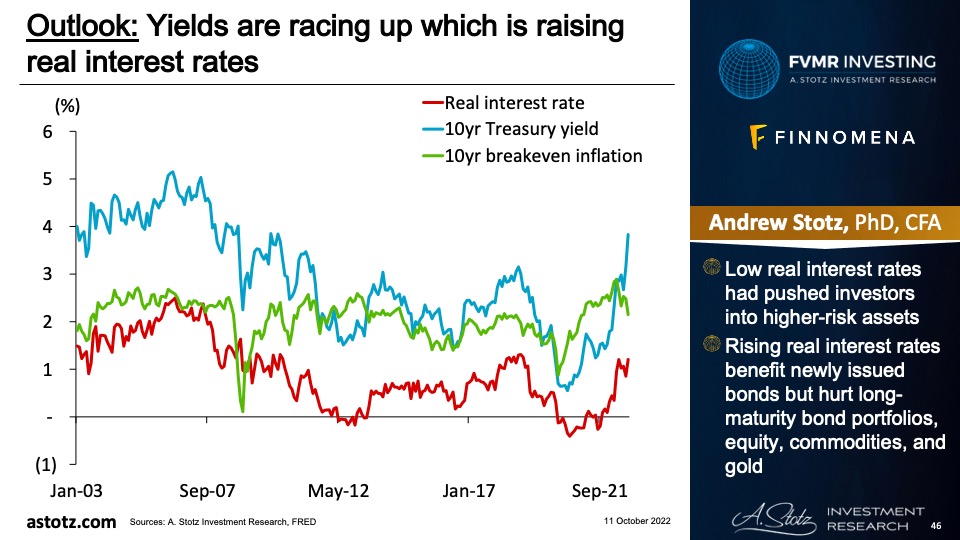

Inflation through the roof, but US 10yr bond rate has been cooling off

- Higher prices, at some point, reduce demand

- A higher base is also likely to reduce the inflation rate

- Hence, inflation could be close to a peak, even without central bank intervention

The 3m gov’t bond yield has risen to 5.0% from 1.7% a year ago

- Still, global inflation has raced up significantly more

- Expect central banks to continue raising rates, though at a slower pace, as they haven’t yet stifled inflation

US CPI appears to be peaking

- If no significant oil price moves from here, it could be the peak for US CPI

- But the feed through of high oil prices could keep food and everything else high, meaning no extreme fall in US CPI over the next few months

Euro area inflation has slowed down as well

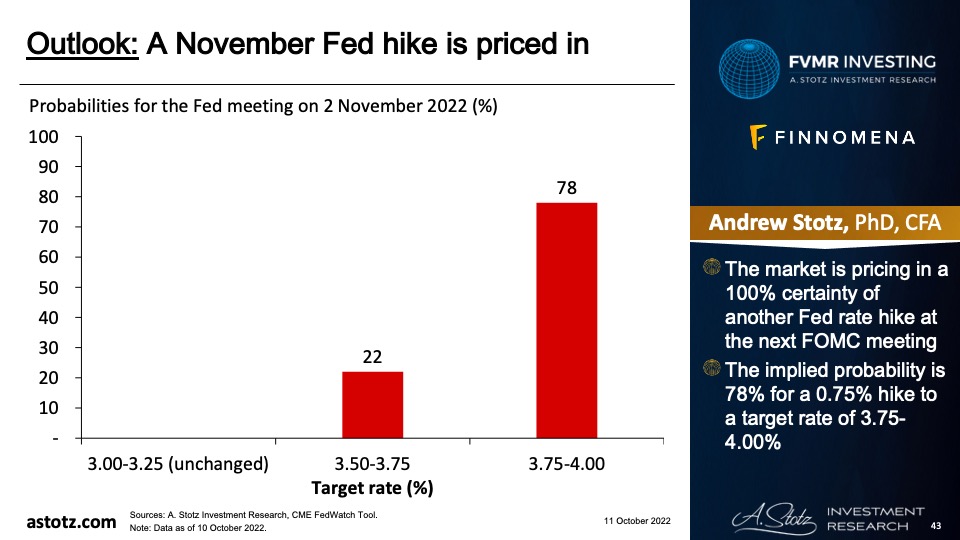

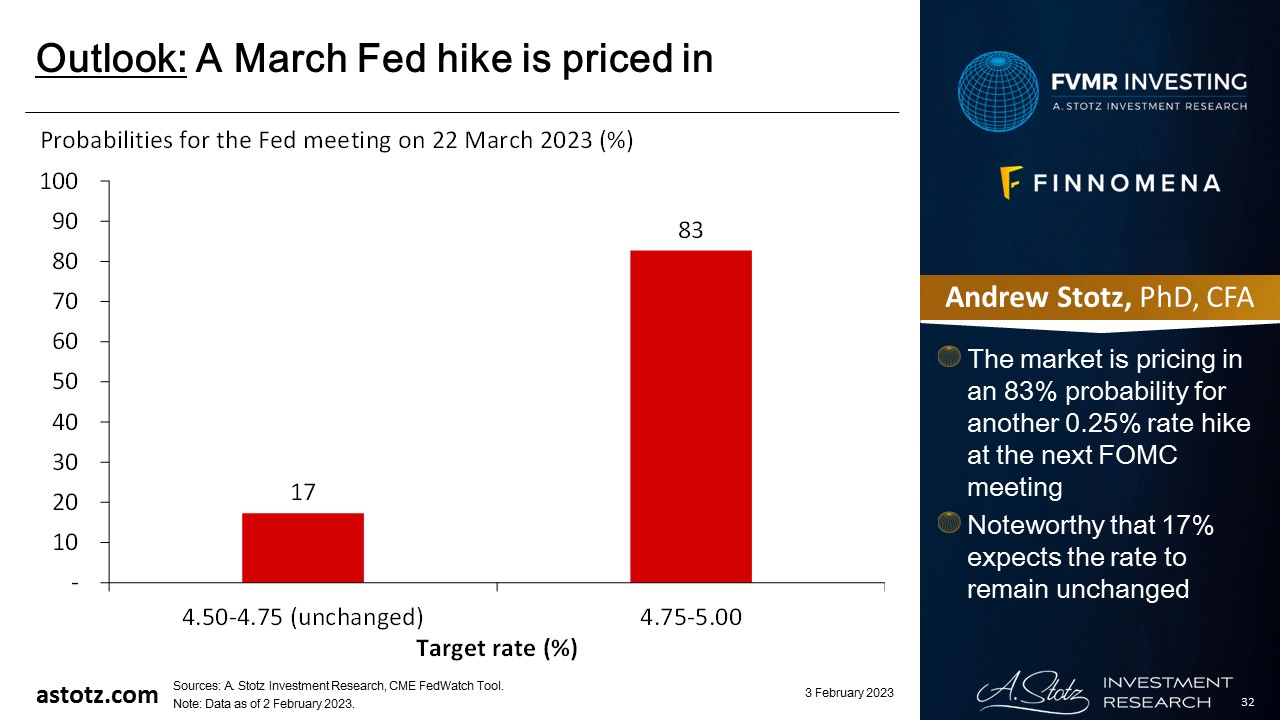

A March Fed hike is priced in

- The market is pricing in an 83% probability for another 0.25% rate hike at the next FOMC meeting

- Noteworthy that 17% expects the rate to remain unchanged

The fastest and most aggressive rate-hike cycle by the Fed since the 1980s

- After the 0.25%-hike on 1 February 2023, the current rate-hike cycle became the most aggressive since the 1980s

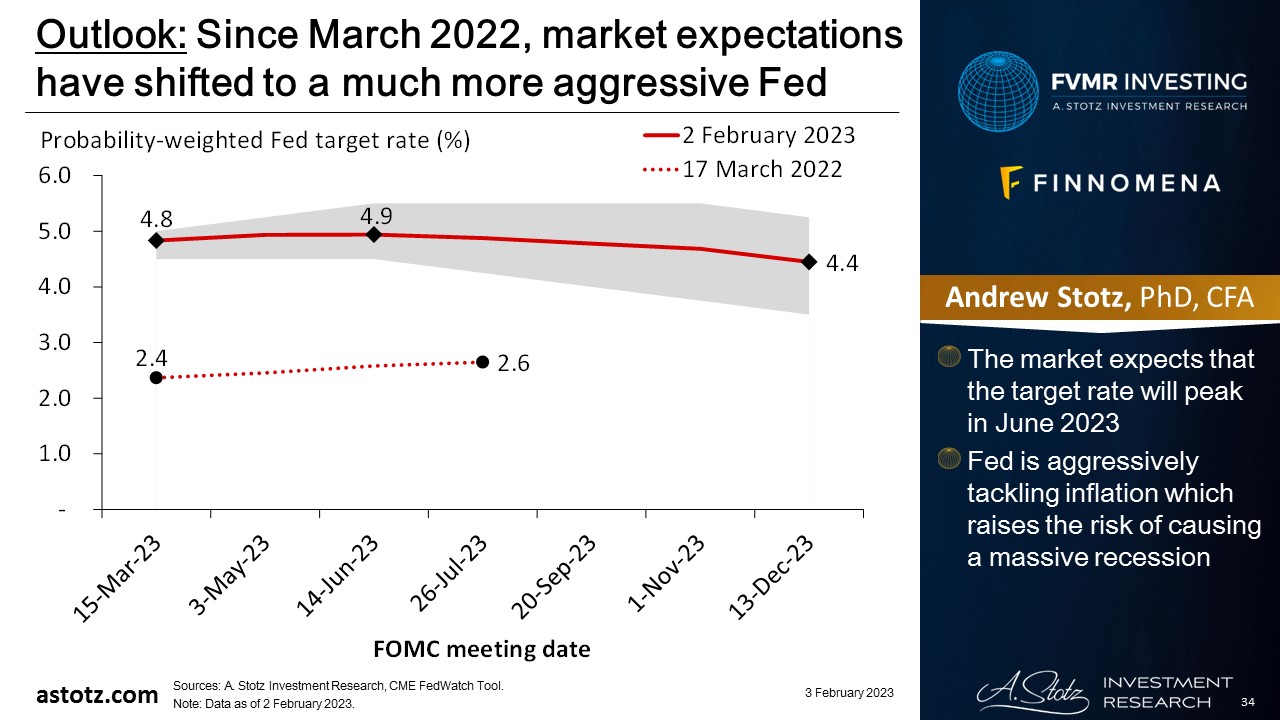

Since March 2022, market expectations have shifted to a much more aggressive Fed

- The market expects that the target rate will peak in June 2023

- Fed is aggressively tackling inflation which raises the risk of causing a massive recession

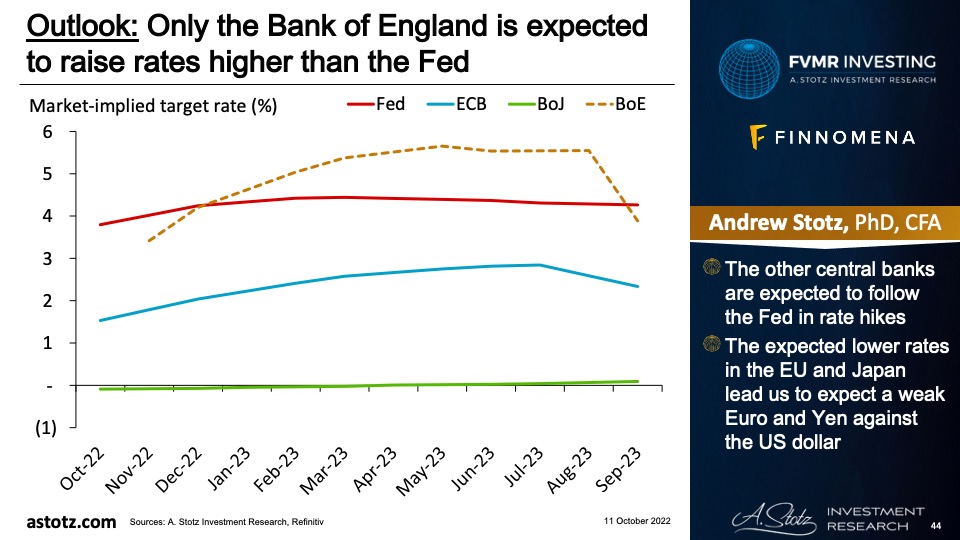

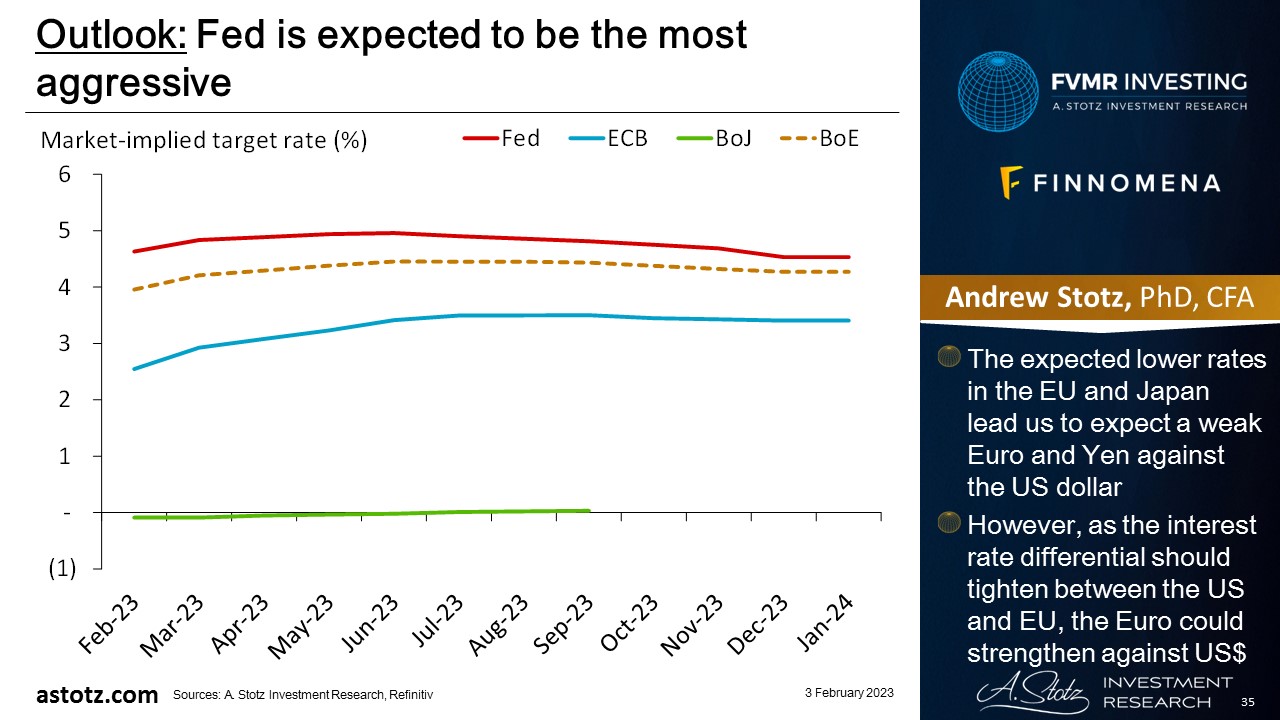

Fed is expected to be the most aggressive

- The expected lower rates in the EU and Japan lead us to expect a weak Euro and Yen against the US dollar

- However, as the interest rate differential should tighten between the US and EU, the Euro could strengthen against US$

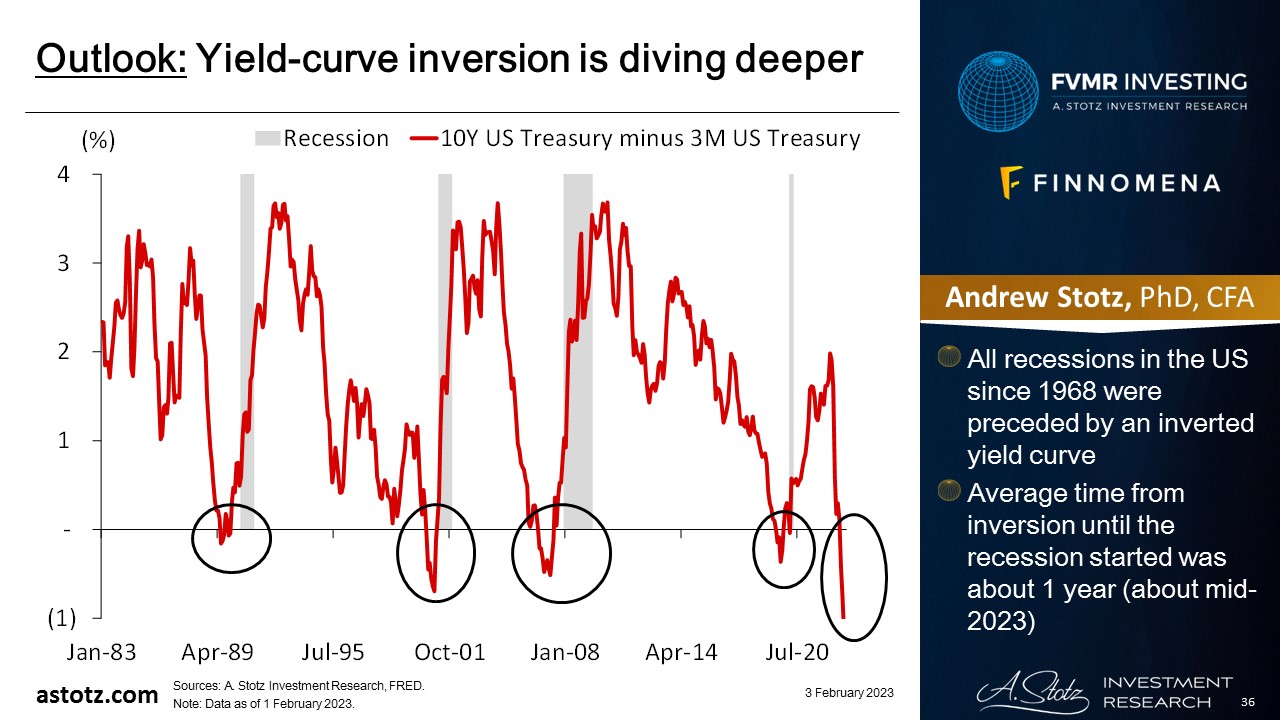

Yield-curve inversion is diving deeper

- All recessions in the US since 1968 were preceded by an inverted yield curve

- Average time from inversion until the recession started was about 1 year (about mid-2023)

Valuations have come down, primarily due to price fall, but bounced in January

- World stocks’ valuation is now around its long-term average

- While the consensus net margin has come down a bit, the downward revision is likely not enough

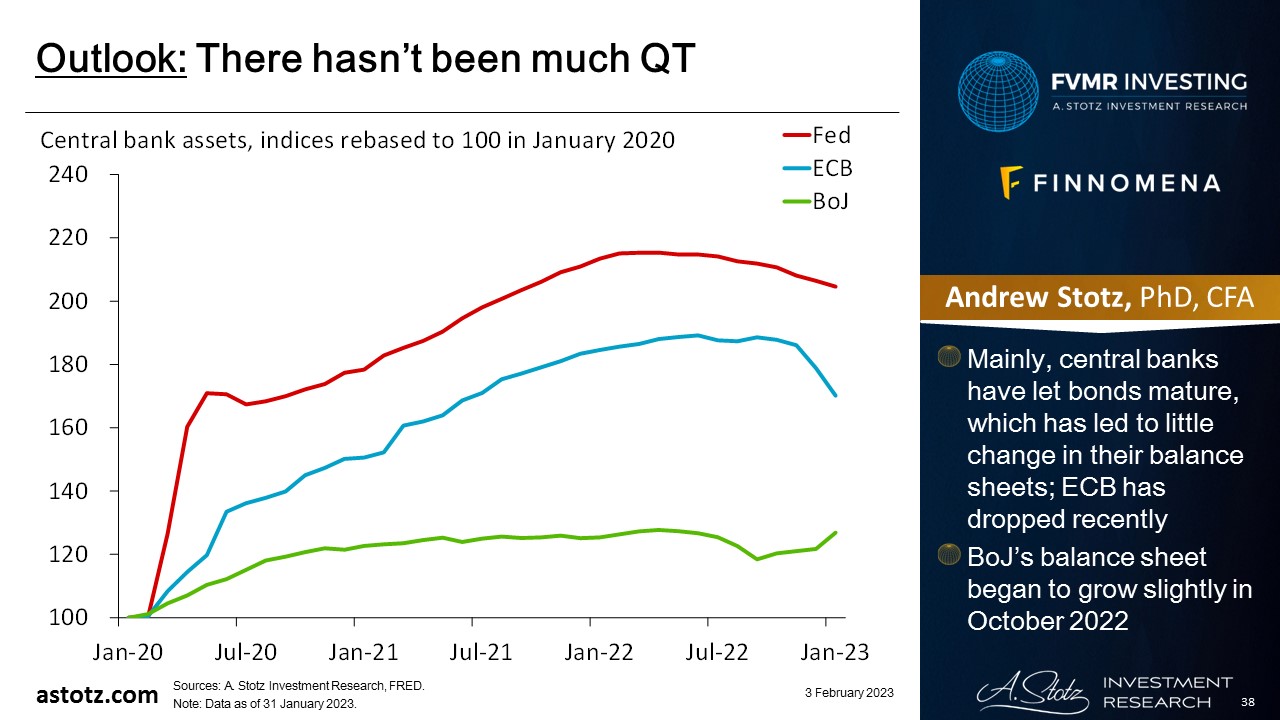

There hasn’t been much QT

- Mainly, central banks have let bonds mature, which has led to little change in their balance sheets; ECB has dropped recently

- BoJ’s balance sheet began to grow slightly in October 2022

For the past year, we’ve said that we think the course will eventually be reversed

- We still think central bankers and politicians will change course and return to accommodative policies as soon as something “breaks”

- And we do think central bankers are going to break things

Central banks may kill growth but not inflation, and we’ll get stagflation

- Stagflation is typically bad for both stocks and bonds

- Commodities have typically done well during inflationary times and have been resilient during stagflation

- Gold has historically fared well during stagflation

We see opportunities to allocate to specific sectors and markets within equity

- Overall, equities are likely to suffer from aggressive rate hikes and withdrawn liquidity

- Likely earnings downgrades to come, which is also bad for equities

- Despite that, we see opportunities to allocate to specific sectors and countries

Bonds are typically a safe place to be, even though 2022 was exceptionally bad

- In recessions, safer assets like government bonds are typically performing well

- Though with high inflation, low yields could still lead to negative real returns

- We typically don’t allocate to bonds to speculate on the upside but rather use it as a way to protect capital over time

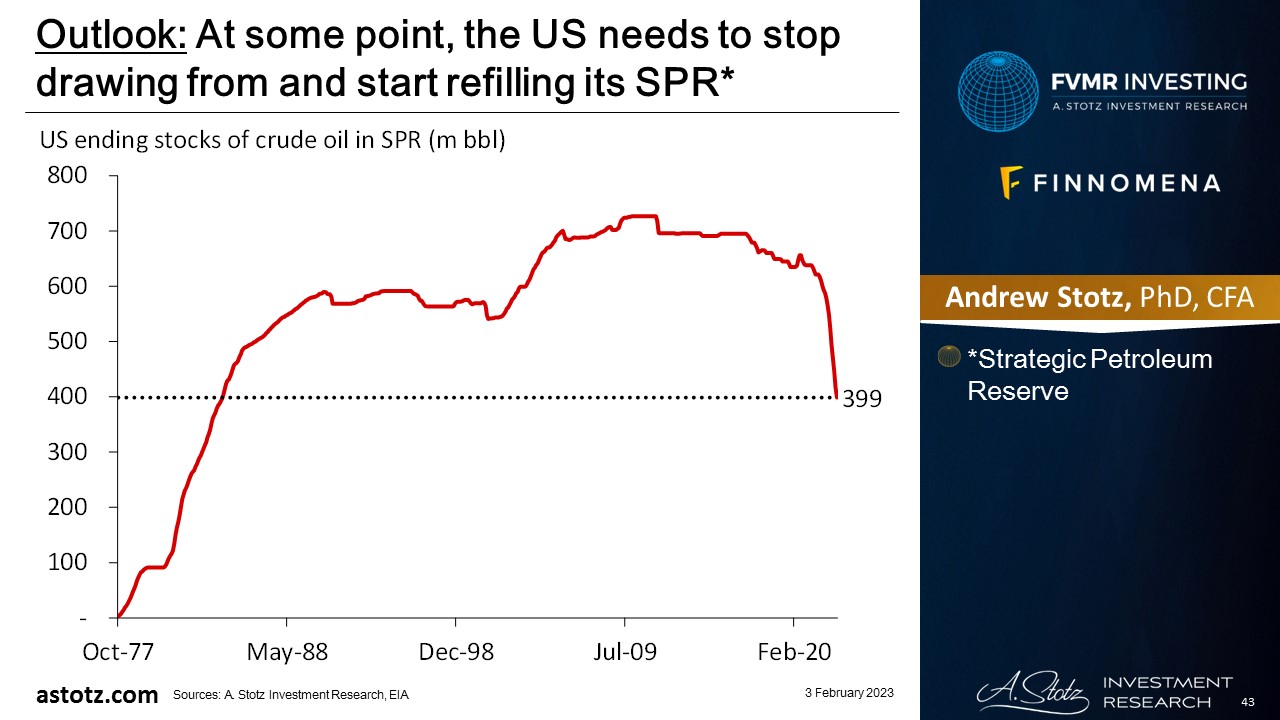

At some point, the US needs to stop drawing from and start refilling its SPR*

- *Strategic Petroleum Reserve

Fundamental support for energy prices

- OPEC+ keeps missing its output targets, and the cartel has announced to cut production and support oil price

- Geopolitical conflicts and wars could lead to further supply shocks

- Energy prices can also remain high due to past underinvestment in new projects

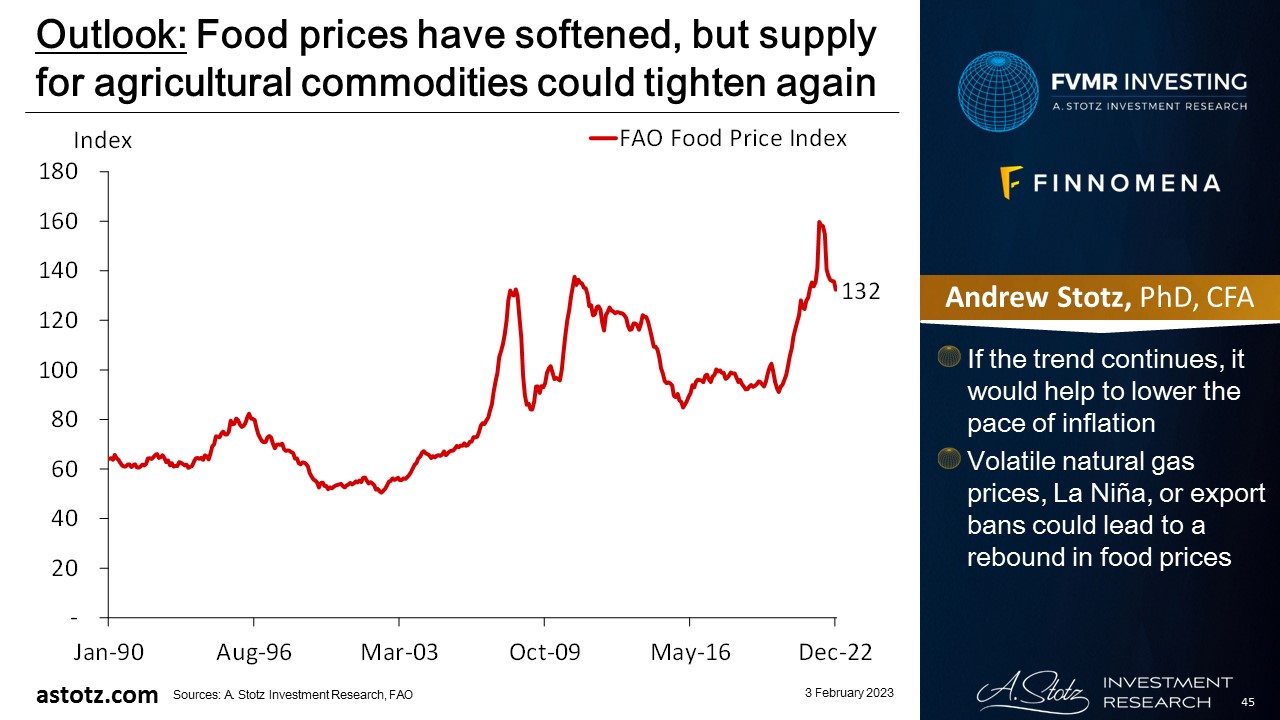

Food prices have softened, but supply for agricultural commodities could tighten again

- If the trend continues, it would help to lower the pace of inflation

- Volatile natural gas prices, La Niña, or export bans could lead to a rebound in food prices

Commodities have fundamental support

- Demand for necessities (food and energy), inflation, and supply-chain disruptions related and unrelated to the war in Ukraine are going to keep commodities prices high

- The re-opening of China could lead to increased demand for commodities

- Also, if we were to go into a stagflationary period, commodities could show resilient

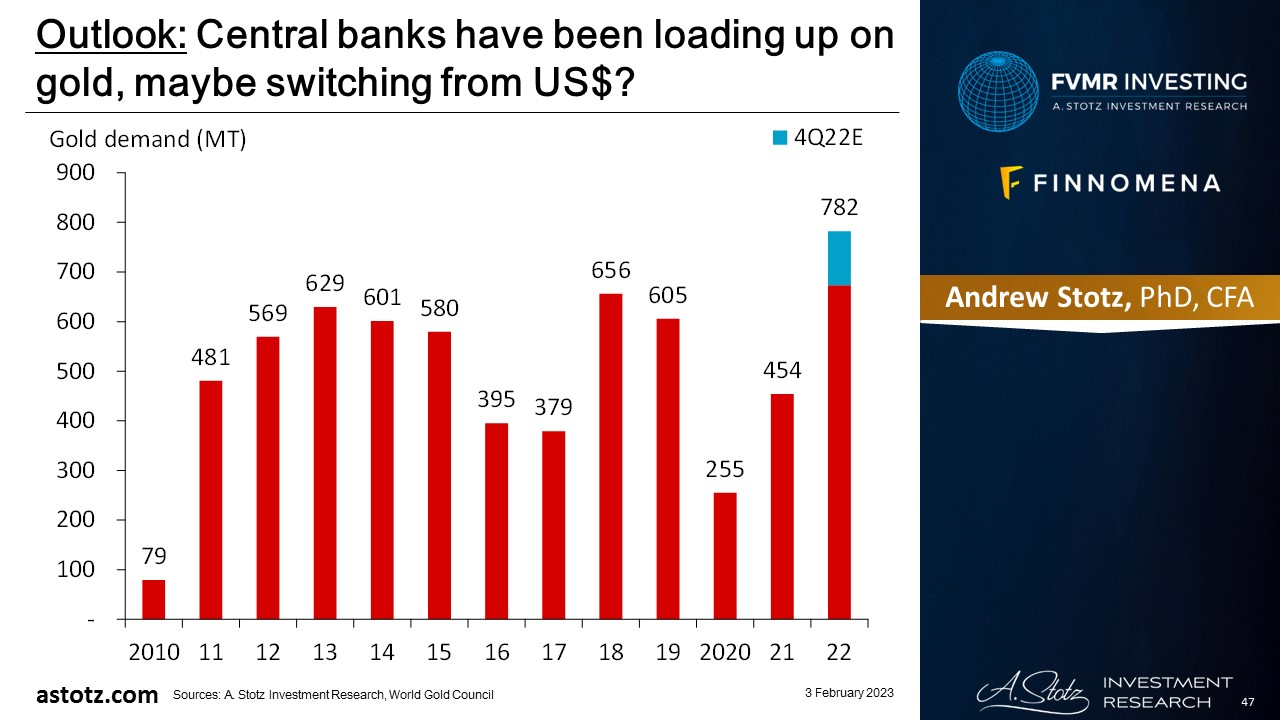

Central banks have been loading up on gold, maybe switching from US$?

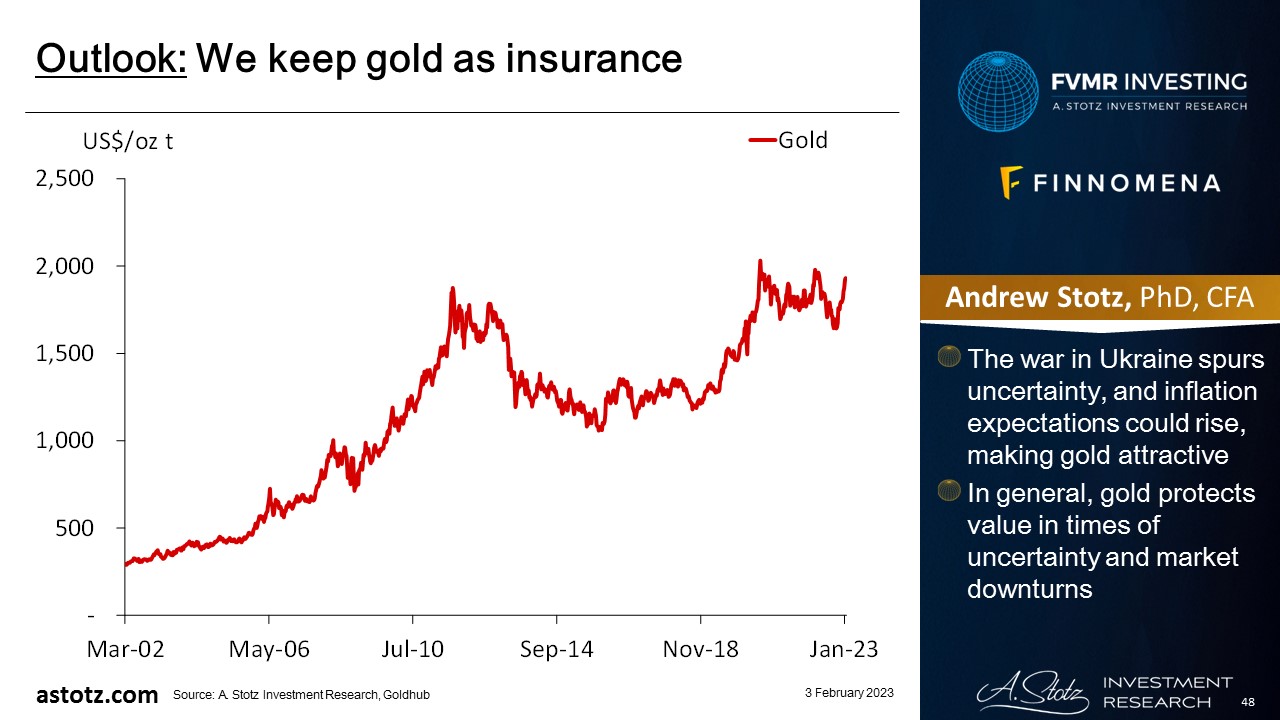

We keep gold as an insurance

- The war in Ukraine spurs uncertainty, and inflation expectations could rise, making gold attractive

- In general, gold protects value in times of uncertainty and market downturns

Risk: Inflation quickly gets under control

- Central banks’ aggressive rate hikes and QT crash the stock markets

- We’re underweight equity, so if central banks pivot and stocks go up, we’d miss the upside

- We are mainly exposed to Thai bonds; hence, BOT’s actions impact the most

- Weak Chinese economy could reduce commodities demand; hence, lower prices

- Other commodities could fall with energy prices, too, as it’s part of the production cost

Key takeaways

- Central bankers appear to be raising rates into a recession to stifle inflation; stagflation would be the worst outcome

- Demand for necessities (food and energy), inflation, and supply-chain disruptions can drive commodities higher

- We see opportunities to allocate to specific sectors and markets within equity

- Bonds and gold to protect capital

- Risks: Global recession, collapsing energy prices, weak China

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.