A. Stotz All Weather Strategies – February 2023

The All Weather Strategy is available in Thailand through FINNOMENA. If you’re interested in our allocation strategy, you can also join the Become a Better Investor Community. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

What happened in world markets in February 2023

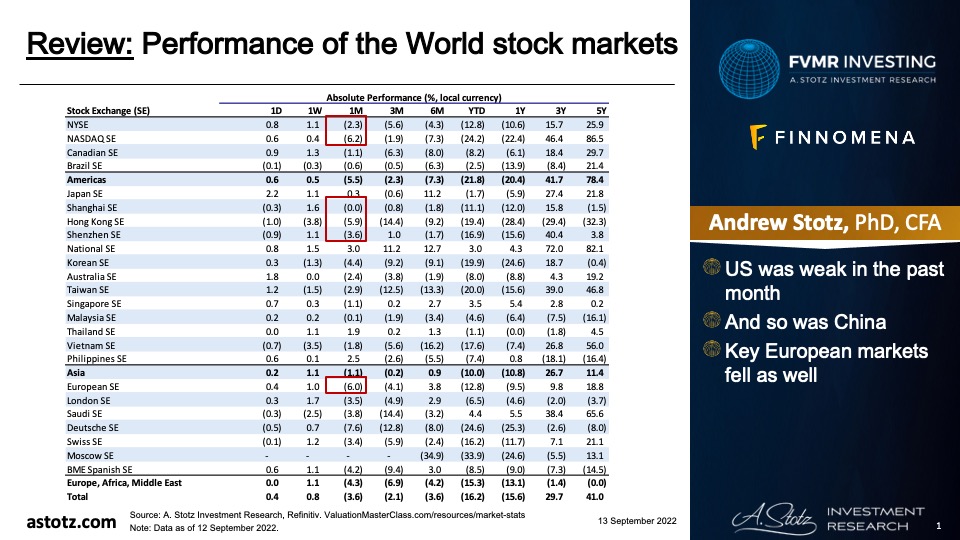

Performance of the World stock markets

- US retreated

- China A was flat, while Hong Kong saw a massive drop

- Europe was one of the few places with a positive return in February

Find the updated Performance of the World stock markets here.

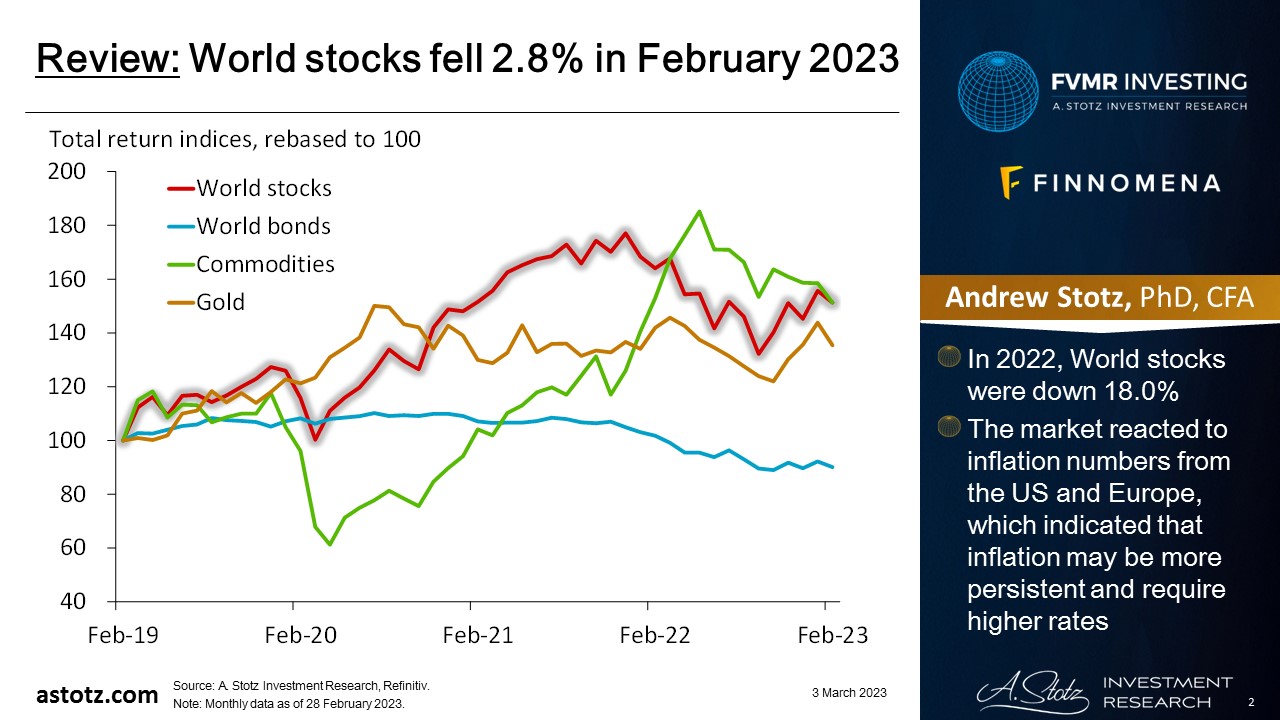

World stocks fell 2.8% in February 2023

- In 2022, World stocks were down 18.0%

- The market reacted to inflation numbers from the US and Europe, which indicated that inflation may be more persistent and require higher rates

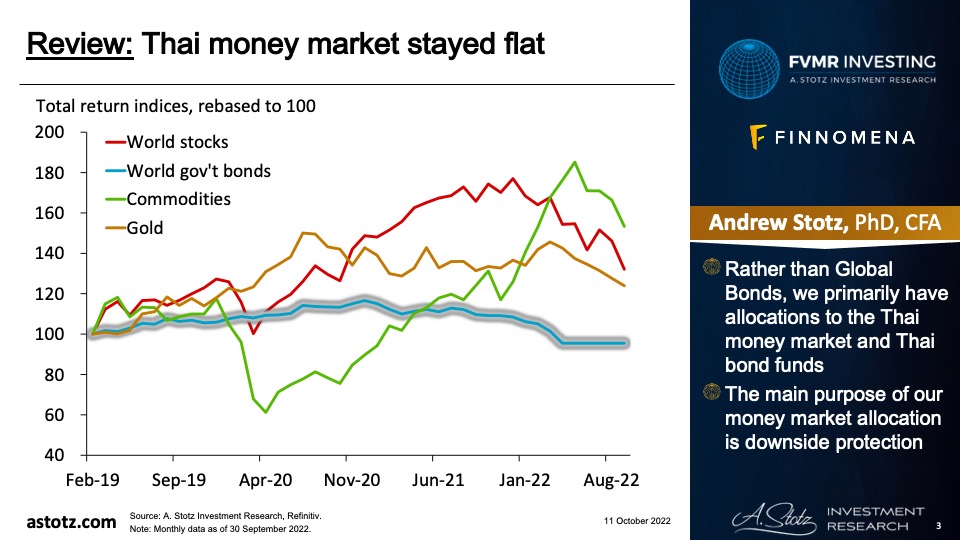

Global bonds were down in February

- In AWS and AWAF, rather than global bonds, we had a 25% target allocation to the Thai money market, which was flat as expected

- The main purpose of our money market allocation is downside protection

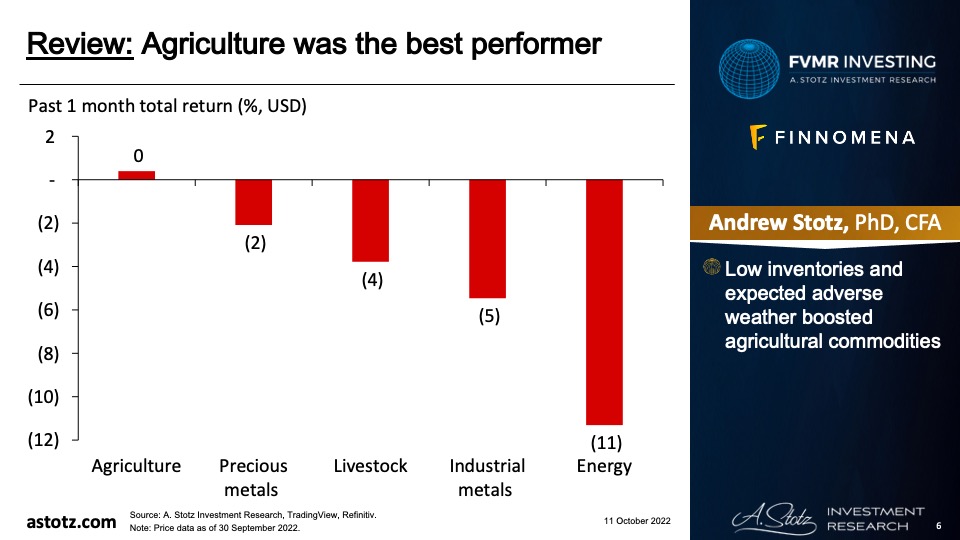

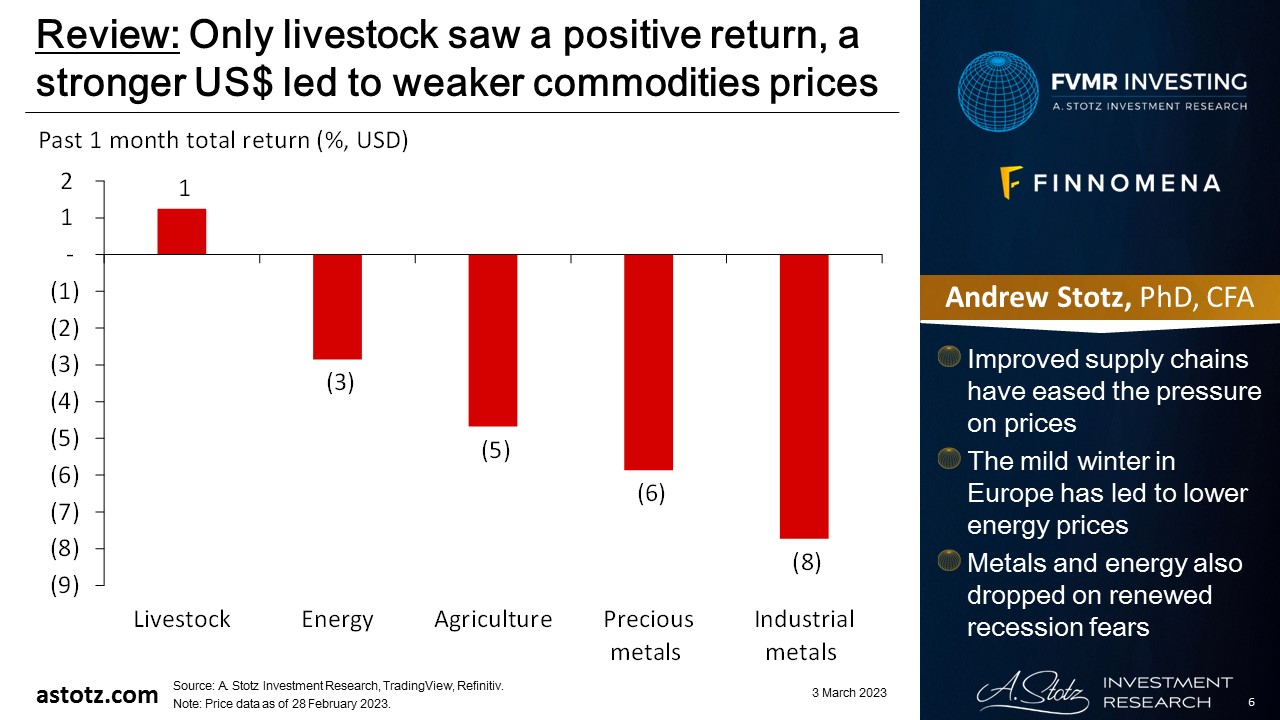

Commodities underperformed in February 2023 and lost 4.5%

WTI oil closed February 2023 at US$77/bbl

Only livestock saw a positive return, a stronger US$ led to weaker commodities prices

- Improved supply chains have eased the pressure on prices

- The mild winter in Europe has led to lower energy prices

- Metals and energy also dropped on renewed recession fears

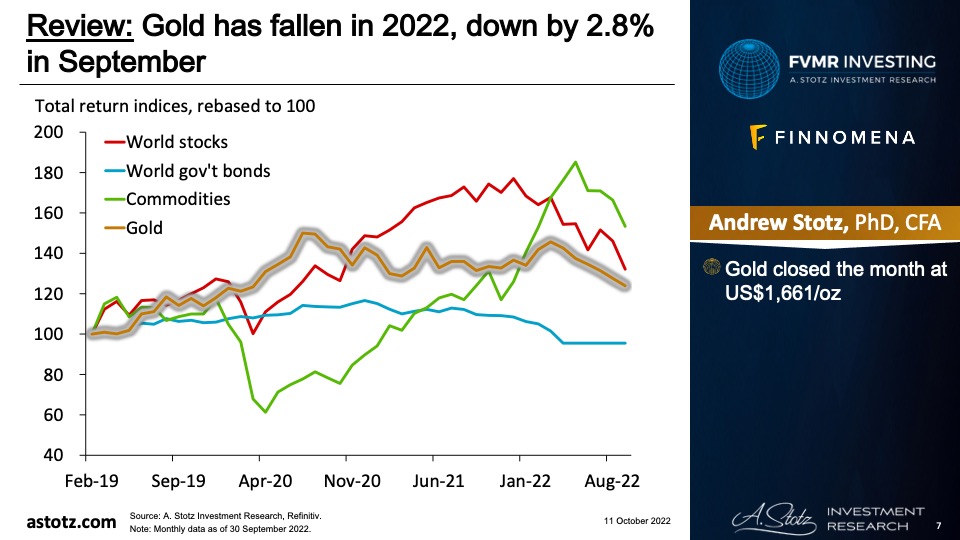

Gold fell by 4.9% in February 2023

- Gold closed the month at US$1,827/oz

- Fed’s “higher rates for longer” communication has punished gold, as higher rates often pushes down gold price

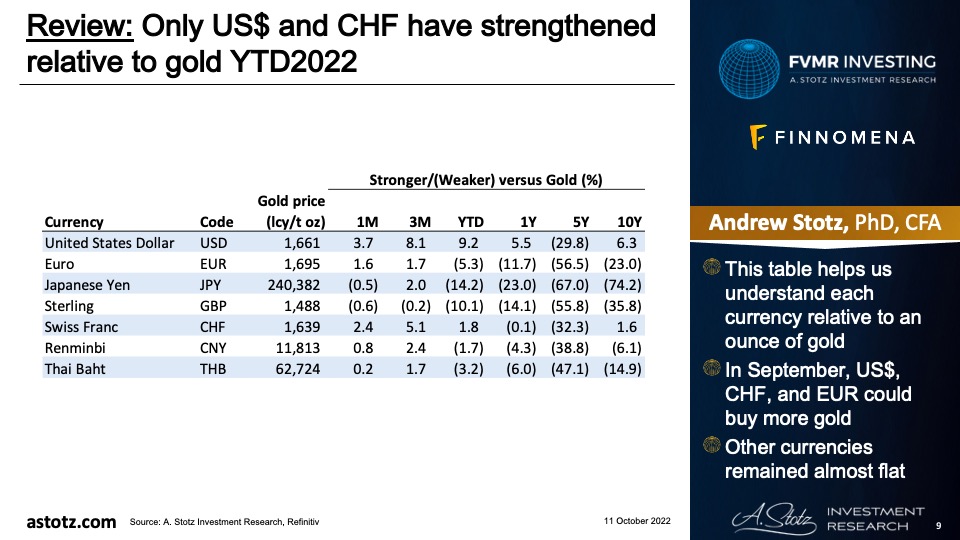

All currencies except THB strengthened against gold in February 2023

- Typically, a stronger US$ means a lower gold price in US$ and vice versa

Fed started February with a 0.25% hike

After today’s 25 bps rate hike, the Fed Funds Rate has moved above Core PCE (the Fed’s preferred measure of inflation). Since 2008, the only other period w/ a Fed Funds Rate above Core PCE: Oct 2018 – Sep 2019. That ended with Fed rate cuts in 2019 & a move back to easy money. pic.twitter.com/rlampX2lnL

— Charlie Bilello (@charliebilello) February 1, 2023

Inflation in some European nations came in high, driving up bond yields

Inflation is still coming in hot in Europe, rising to a new record in France this month & unexpectedly re-accelerating in Spain. Money markets are fully pricing in a 4% ECB terminal rate by February 2024, & German 2-year yields are the highest since 2008. https://t.co/xyLoz5LcqH pic.twitter.com/Vu9c49KFcc

— Lisa Abramowicz (@lisaabramowicz1) February 28, 2023

Earnings expectations have turned negative

Earnings slide? The 2023 growth estimate has now flipped into negative territory (-1.1%). This will likely get worse before it gets better. Typically, the estimate comes down by around 800 bps during the year, so that implies earnings growth of around -5% for 2023. pic.twitter.com/YRRO9xAWPJ

— Jurrien Timmer (@TimmerFidelity) February 7, 2023

Interest payments are reaching new heights for the US government

New #s out today with GDP. Annual interest expense on Fed debt: $853 billion. Each year, every year. Next up: $1 trillion-plus.

If nothing else, this is what will stop the Fed. Powell doesn’t have Volcker’s toolbox. pic.twitter.com/TVbWNErCa6

— Brien Lundin (@Brien_Lundin) January 26, 2023

Bonds were terrible in 2022 and they weren’t great before the 1980s either

What is most interesting in this chart is not the 2022 bonds return, but the fact that between 1900 and 1981 bonds had negative real return 👇 60/40 anyone? (FT) pic.twitter.com/C9KfgdsZp9

— Michael A. Arouet (@MichaelAArouet) February 28, 2023

Seems like European natural gas prices are normalizing

European natural gas futures dropped to a 17-month low 📉 📉

⚠️ Risks of a gas supply shortage this winter has disappeared amid high inventories and a steady flow of LNG

🌡️ Milder weather and industrial demand destruction are reducing gas consumptionhttps://t.co/1C2AsT90R9 pic.twitter.com/4dAQejANB8— Stephen Stapczynski (@SStapczynski) February 9, 2023

Stronger US$ pushed down gold price

Metal commodity.

Gold prices edged down to $1’808.55 🔻-0.18%, near their lowest levels since late December.

On stronger dollar and after US economic data last week raised worries that the Federal Reserve could hike interest rates further. pic.twitter.com/gFk9sEqXBA— Arth Ben (@ArthurBenta) February 27, 2023

Stronger US$ led to underperformance of Emerging markets

A stronger dollar and higher rates in the US are encouraging outflows from EM debt pic.twitter.com/THLfezGaaf

— Markets & Mayhem (@Mayhem4Markets) February 25, 2023

Key takeaways

- Fed announced a further 0.25% rate hike

- Inflation remained high

- Interest payments become a heavier burden for the US government budget

- Natural gas prices in Europe normalized

- A stronger US$ hit gold and Emerging markets

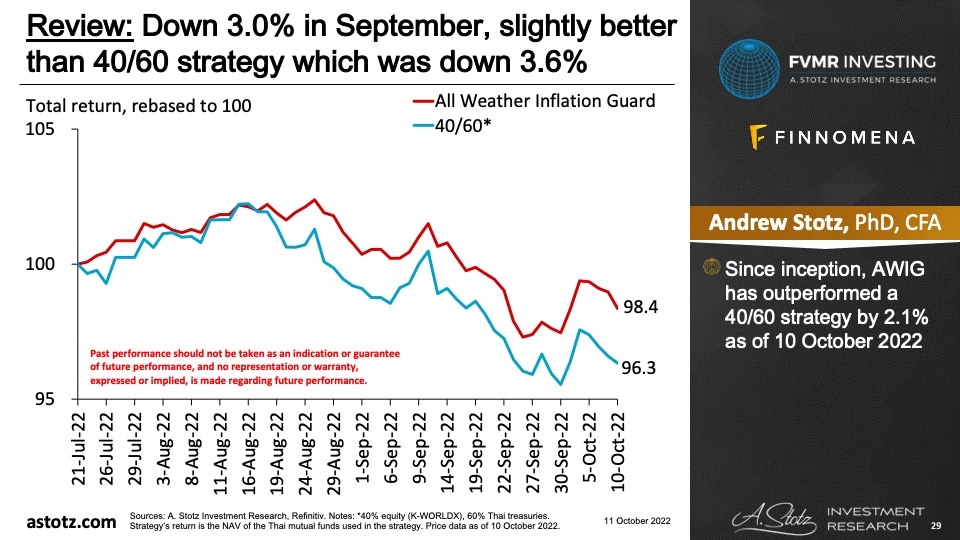

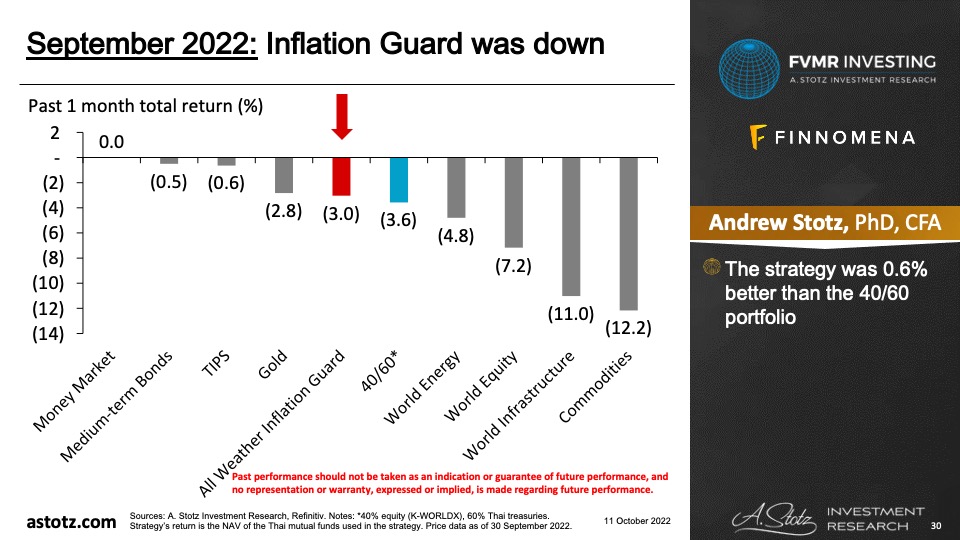

Performance review: All Weather Inflation Guard

All Weather Inflation Guard was down 0.7%

- The strategy has experienced less volatility though

The strategy was 0.6% above the 40/60 portfolio

- Though the strategy fell by 0.7% as markets dropped

- Bonds held up well

- Only energy did well of our tilts

- The world equity fund outperformed the MSCI AC World index

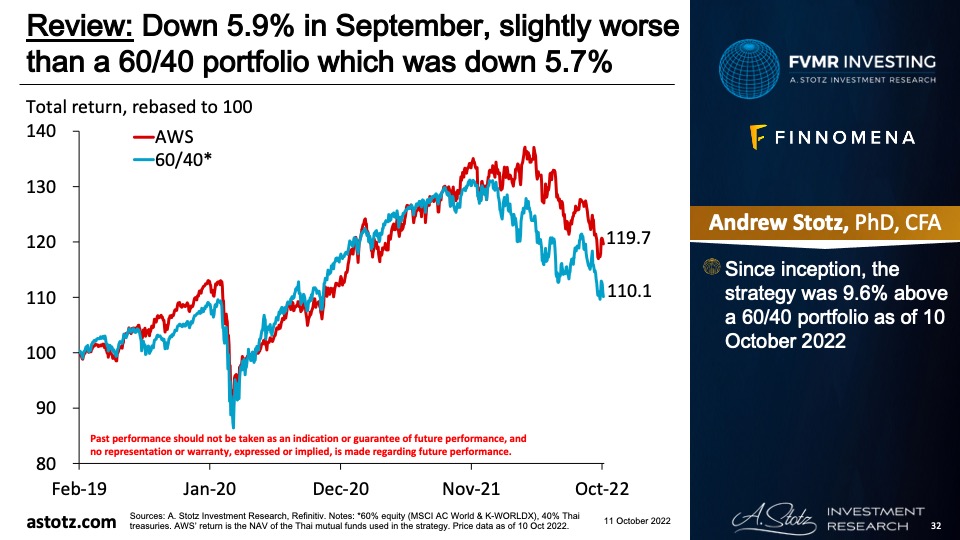

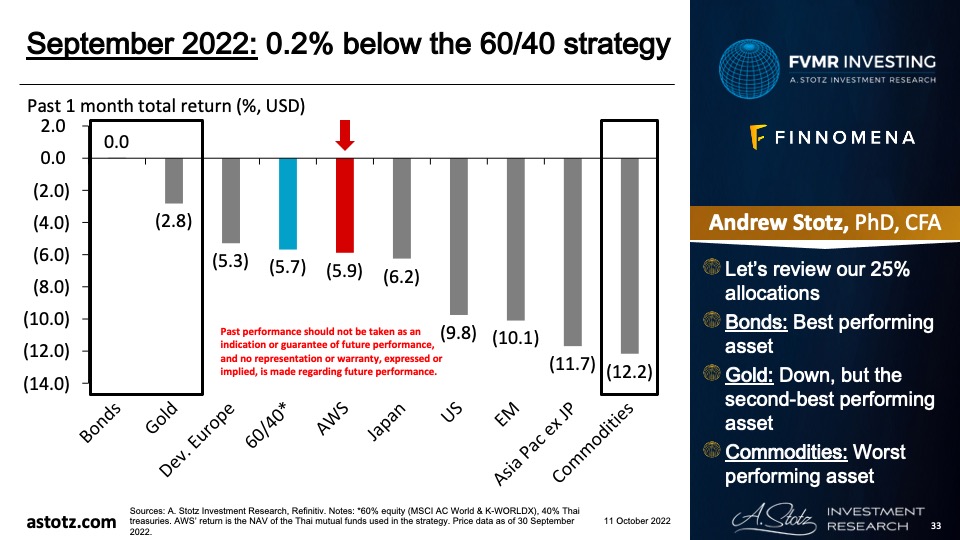

Performance review: All Weather Strategy

All Weather Strategy was down 3.0%

The strategy was 1.3% below the 60/40 portfolio

- Our 25% allocations to commodities and goldy were the major cause of underperformance in February 2023

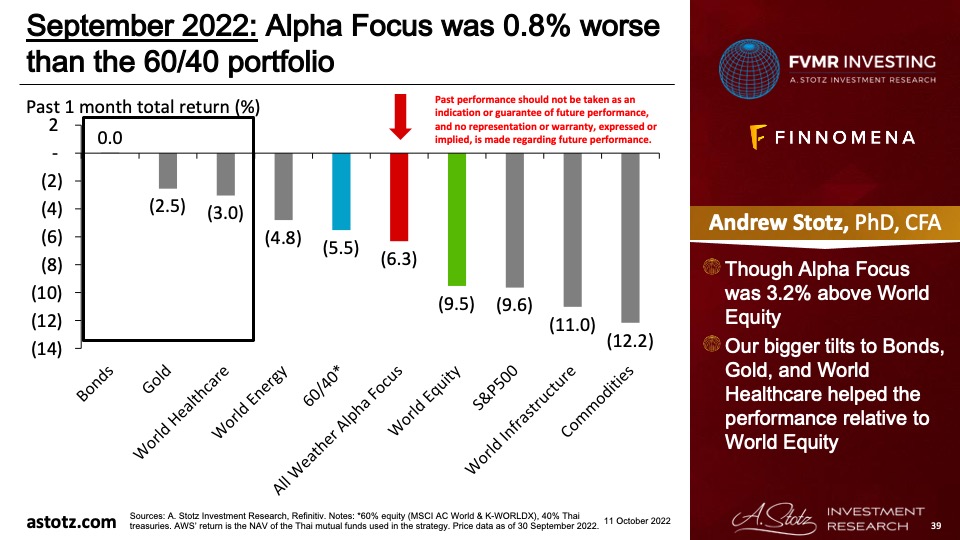

Performance review: All Weather Alpha Focus

All Weather Alpha Focus was down 1.8%

Since inception, the strategy was 5.8% above World equity as of 28 February 2023

The strategy was on par with the 60/40 portfolio

- The strategy was 1.5% above World Equity

- Our 22% tilts World energy and India helped the performance relative to World equity

Global outlook that guides our asset allocation

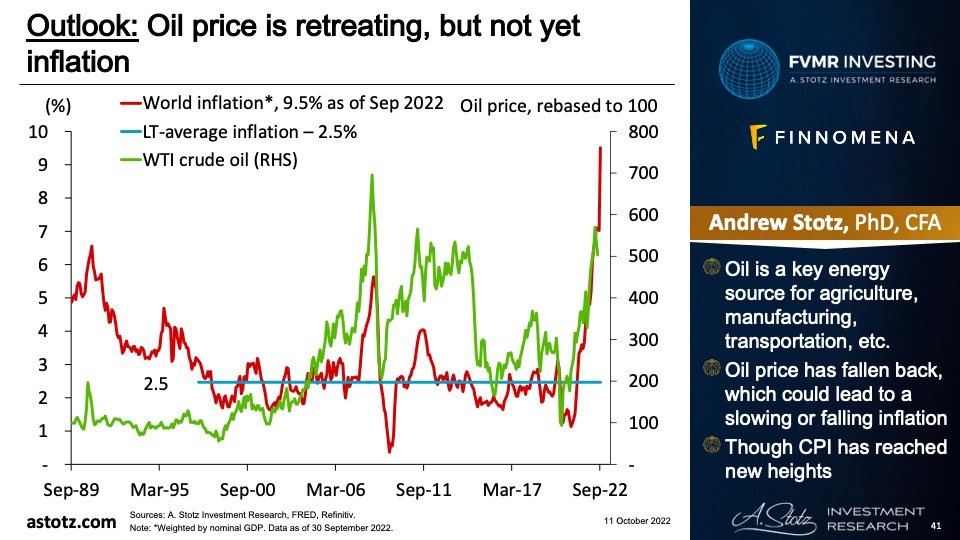

Oil price has retreated, but not yet global inflation

- Oil is a key energy source for agriculture, manufacturing, transportation, etc.

- Oil price has fallen back, which could lead to a slowing or falling inflation

- Though CPI globally is stubborn to fall

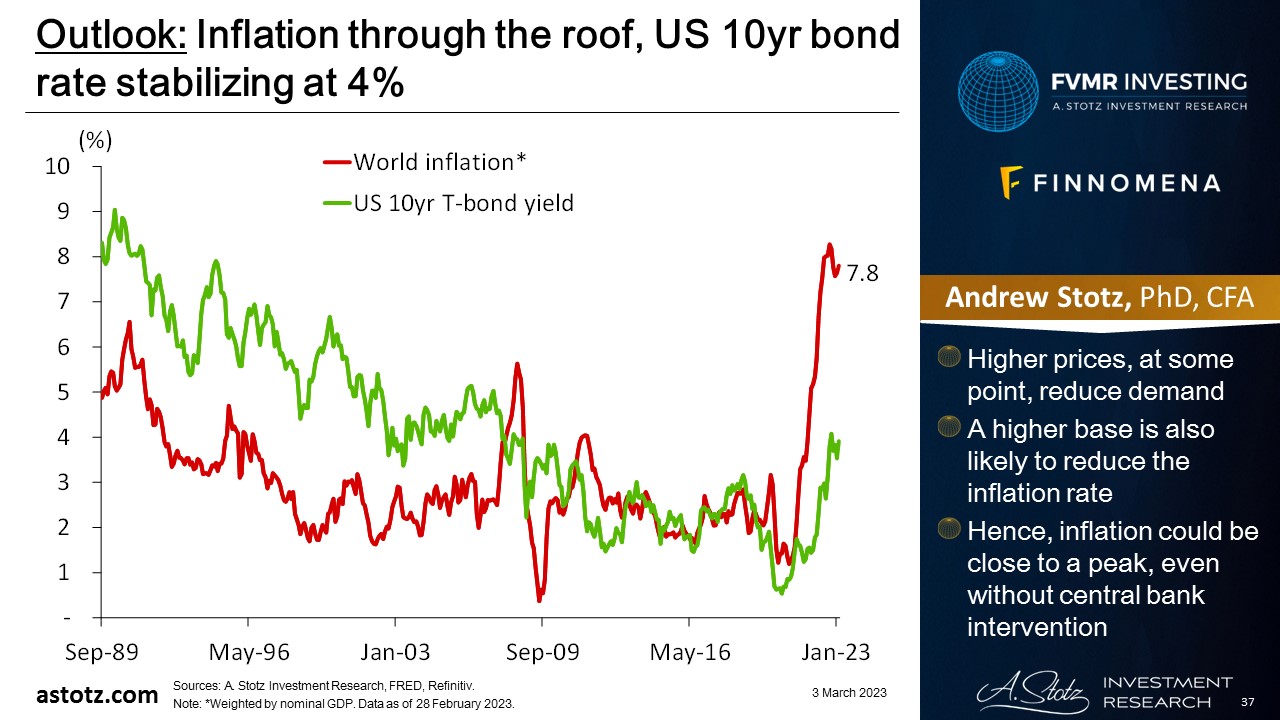

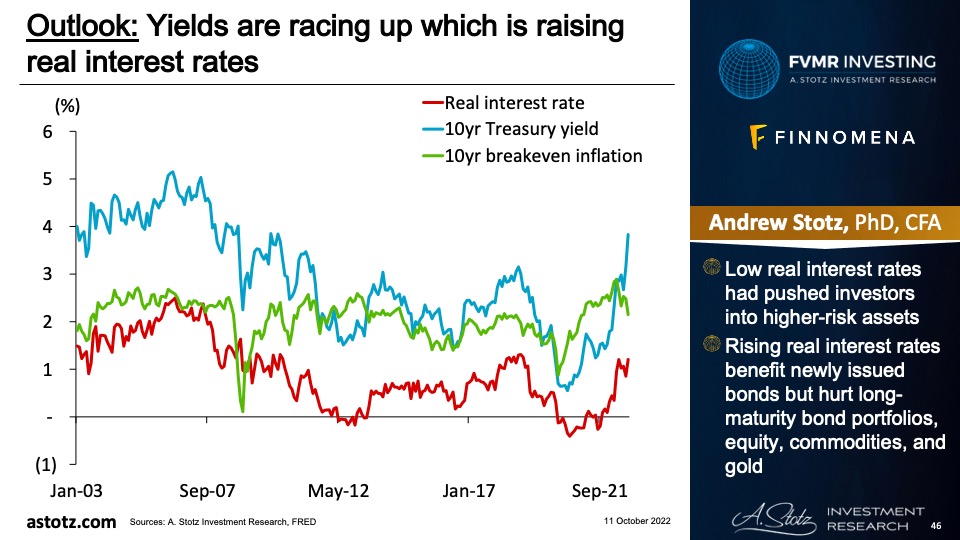

Inflation through the roof, US 10yr bond rate stabilizing at 4%

- Higher prices, at some point, reduce demand

- A higher base is also likely to reduce the inflation rate

- Hence, inflation could be close to a peak, even without central bank intervention

The 3m gov’t bond yield has risen to 5.1% from 2.1% a year ago

- Still, global inflation has raced up significantly more

- Expect central banks to continue raising rates, though at a slower pace, as they haven’t yet stifled inflation

US CPI is past its peak

Euro area inflation has slowed as well

- Though recent data from US, France, and Spain suggests that inflation is not dropping as fast as before

- This has led to a more positive outlook on Europe

The battle against inflation isn’t over

- High inflation will likely persist for a while

- In the long run, equity is the best hedge against inflation, as companies have to adapt to survive

- And as consumers and companies turn more optimistic (or at least less pessimistic), we are increasing our equity allocations

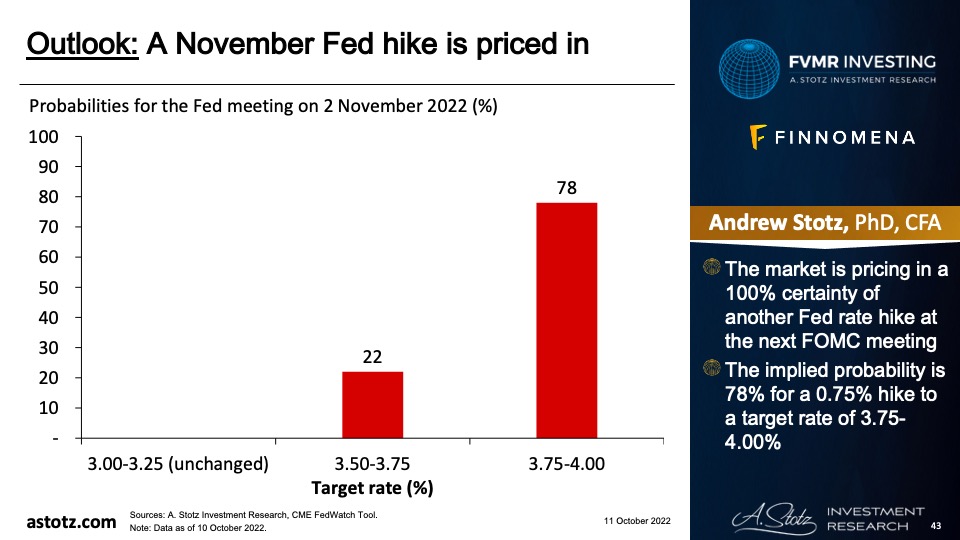

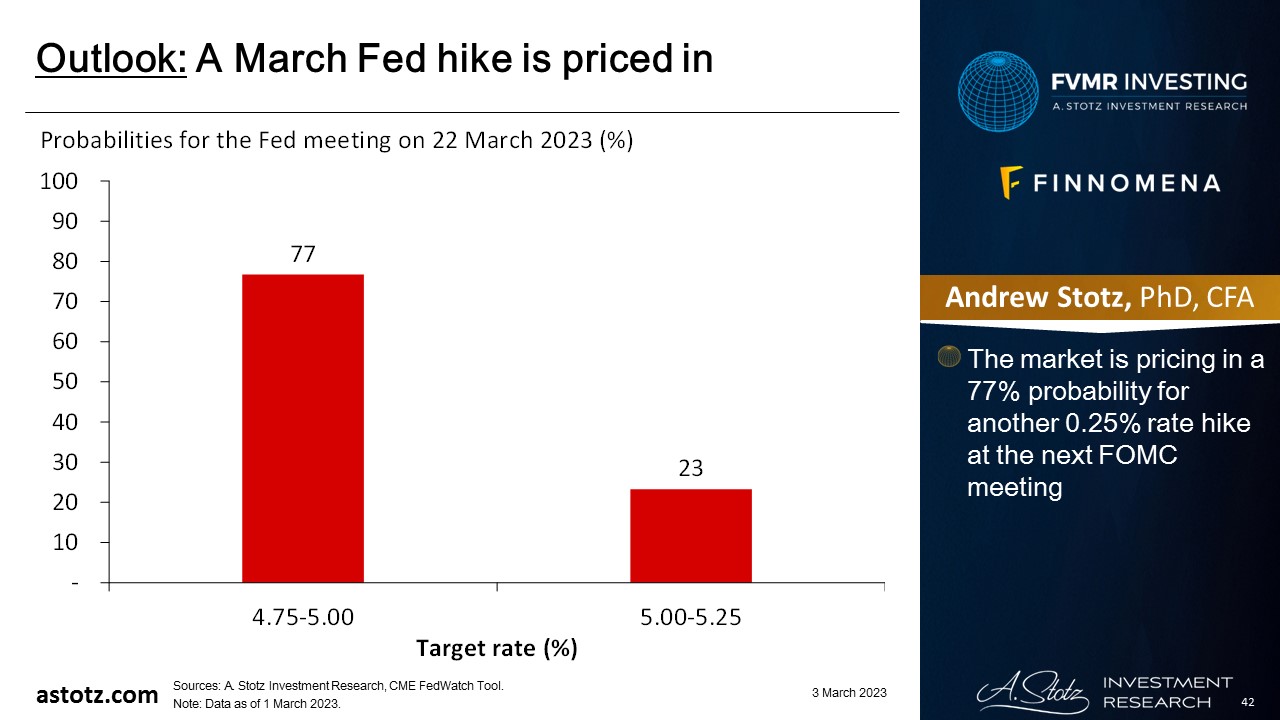

A March Fed hike is priced in

- The market is pricing in a 77% probability for another 0.25% rate hike at the next FOMC meeting

The fastest and most aggressive rate-hike cycle by the Fed since the 1980s

- After the 0.25%-hike on 1 February 2023, the current rate-hike cycle became the most aggressive since the 1980s

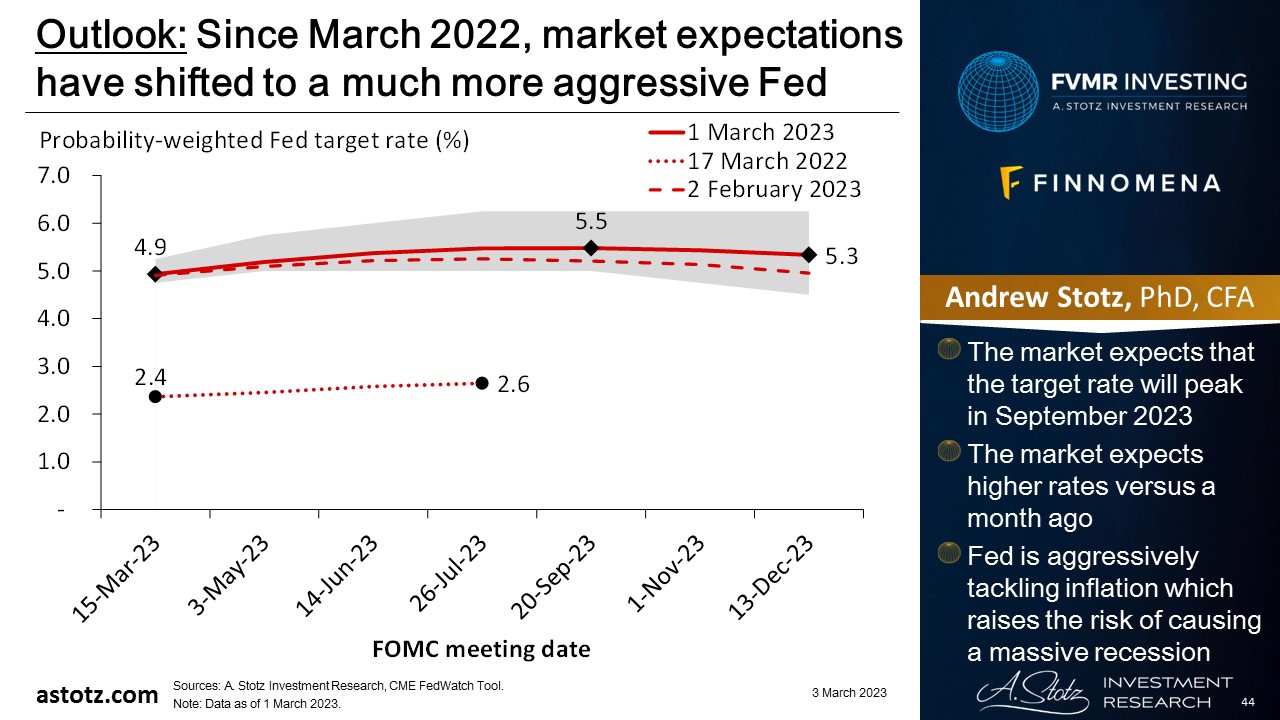

Since March 2022, market expectations have shifted to a much more aggressive Fed

- The market expects that the target rate will peak in September 2023

- The market expects higher rates versus a month ago

- Fed is aggressively tackling inflation which raises the risk of causing a massive recession

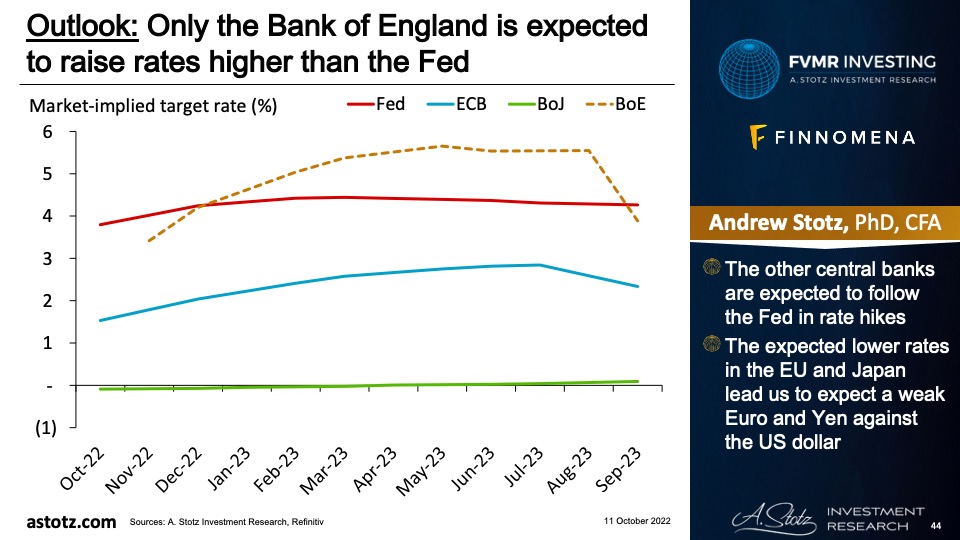

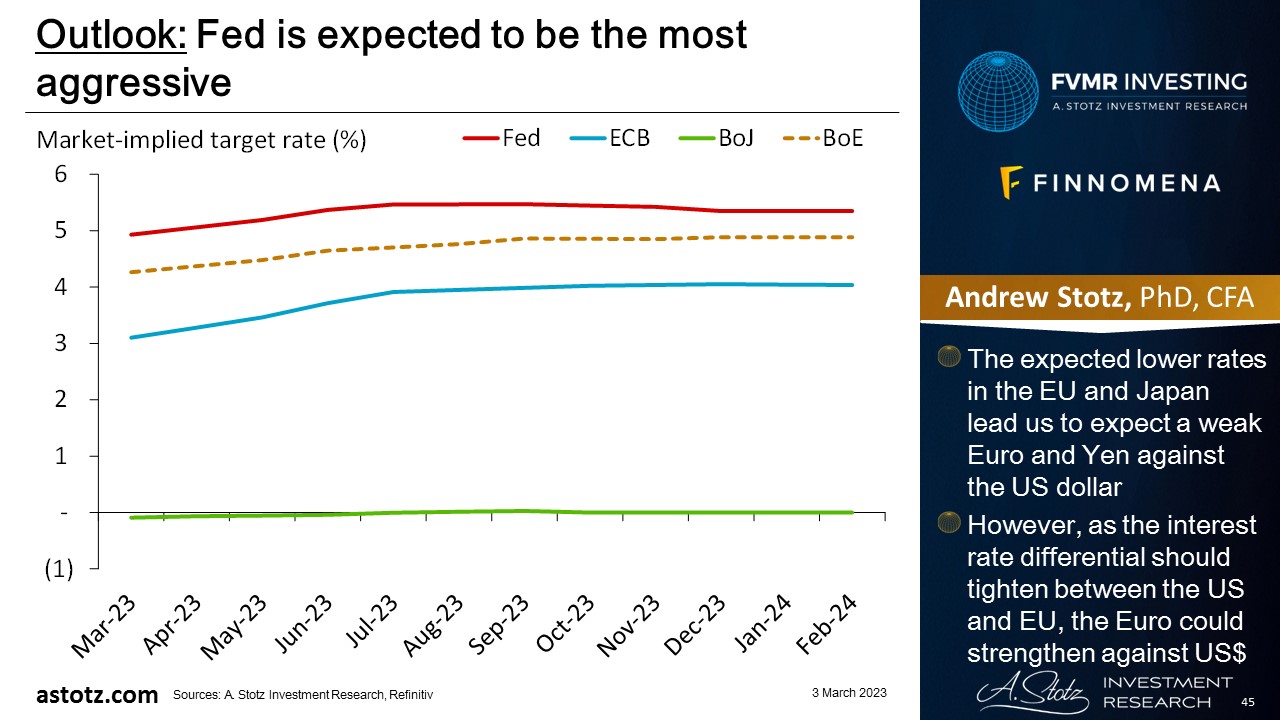

Fed is expected to be the most aggressive

- The expected lower rates in the EU and Japan lead us to expect a weak Euro and Yen against the US dollar

- However, as the interest rate differential should tighten between the US and EU, the Euro could strengthen against US$

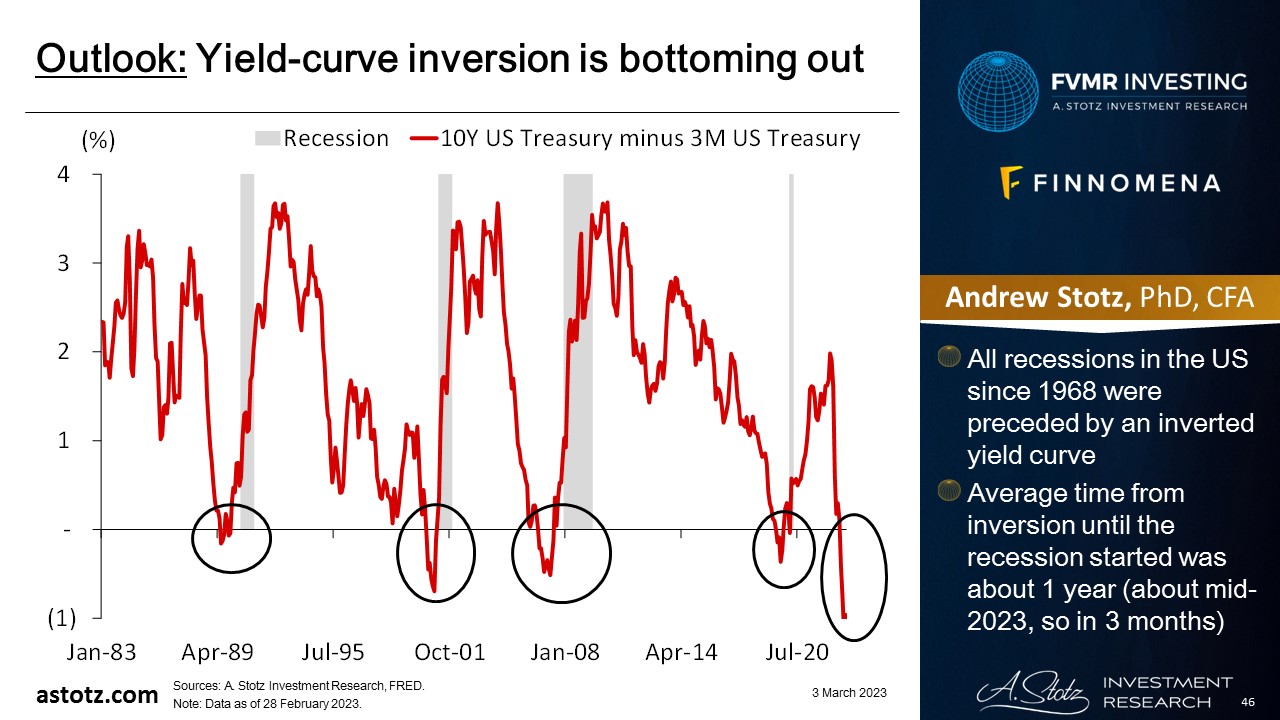

Yield-curve inversion is bottoming out

- All recessions in the US since 1968 were preceded by an inverted yield curve

- Average time from inversion until the recession started was about 1 year (about mid-2023, so in 3 months)

For the past year, we’ve said that we think the course will eventually be reversed

- We still think central bankers and politicians will change course and return to accommodative policies as soon as something “breaks”

- And we do think central bankers are going to break things

- If we are right, equity could get a boost

- If we are wrong, we could get stagflation

Bonds are typically a safe place to be, even though 2022 was exceptionally bad

- In recessions, safer assets like government bonds are typically performing well

- Though with high inflation, low yields could still lead to negative real returns

- We typically don’t allocate to bonds to speculate on the upside but rather use it as a way to protect capital over time

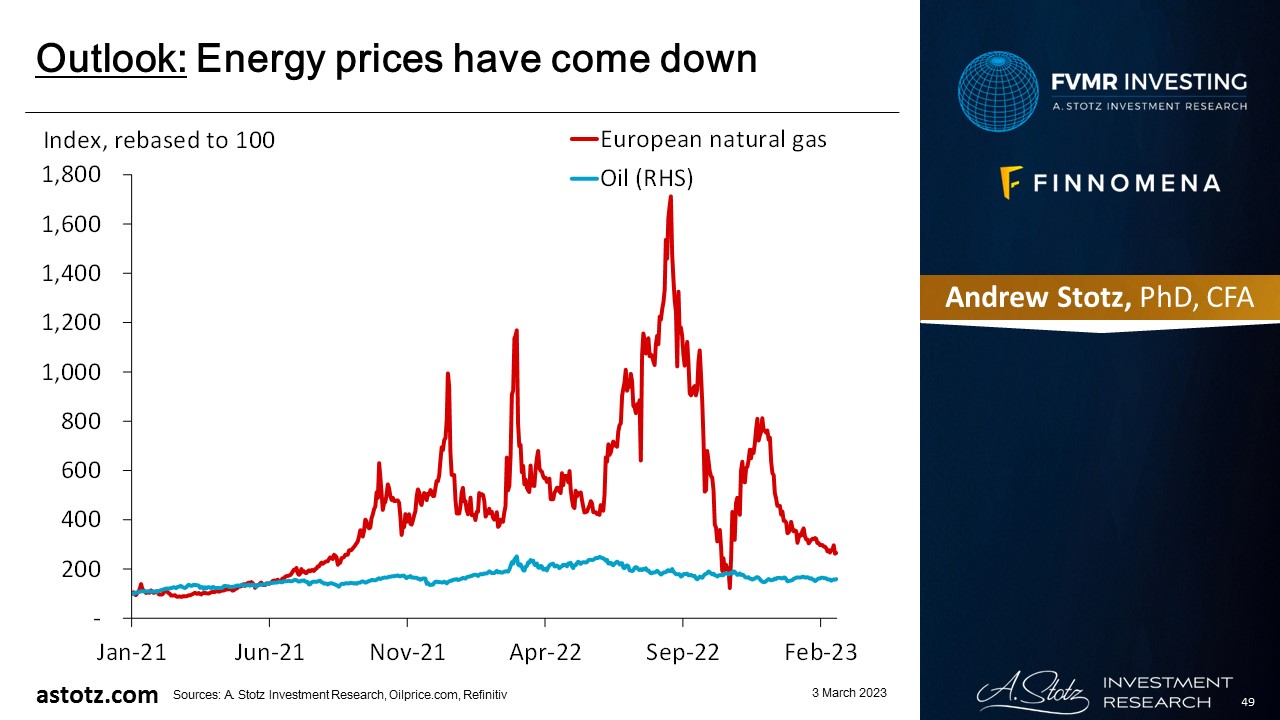

Energy prices have come down

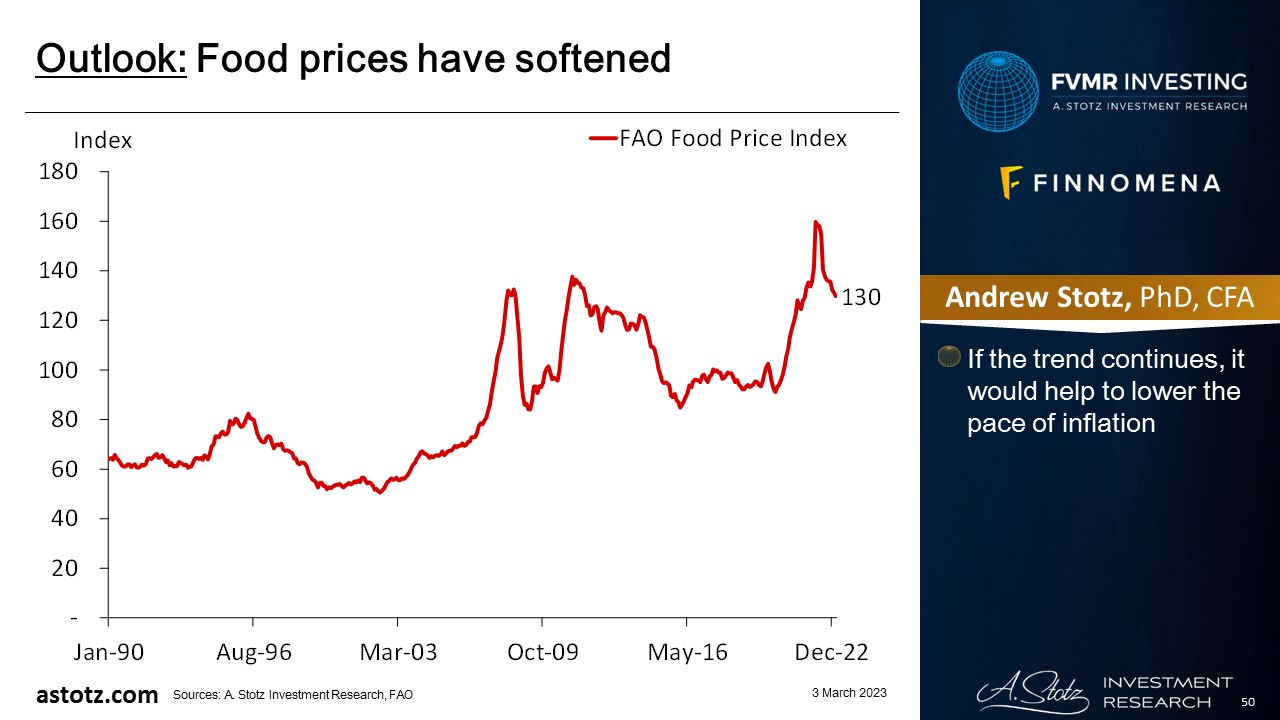

Food prices have softened

- If the trend continues, it would help to lower the pace of inflation

Commodities have lost momentum as energy prices eased due to a mild winter

- We don’t see a clear catalyst for energy prices to go significantly higher, but we think they can remain high, which supports profits for energy companies

- The main upside in commodities would come from a supply shock, adverse weather conditions, or significantly higher demand from, for example, the China reopening

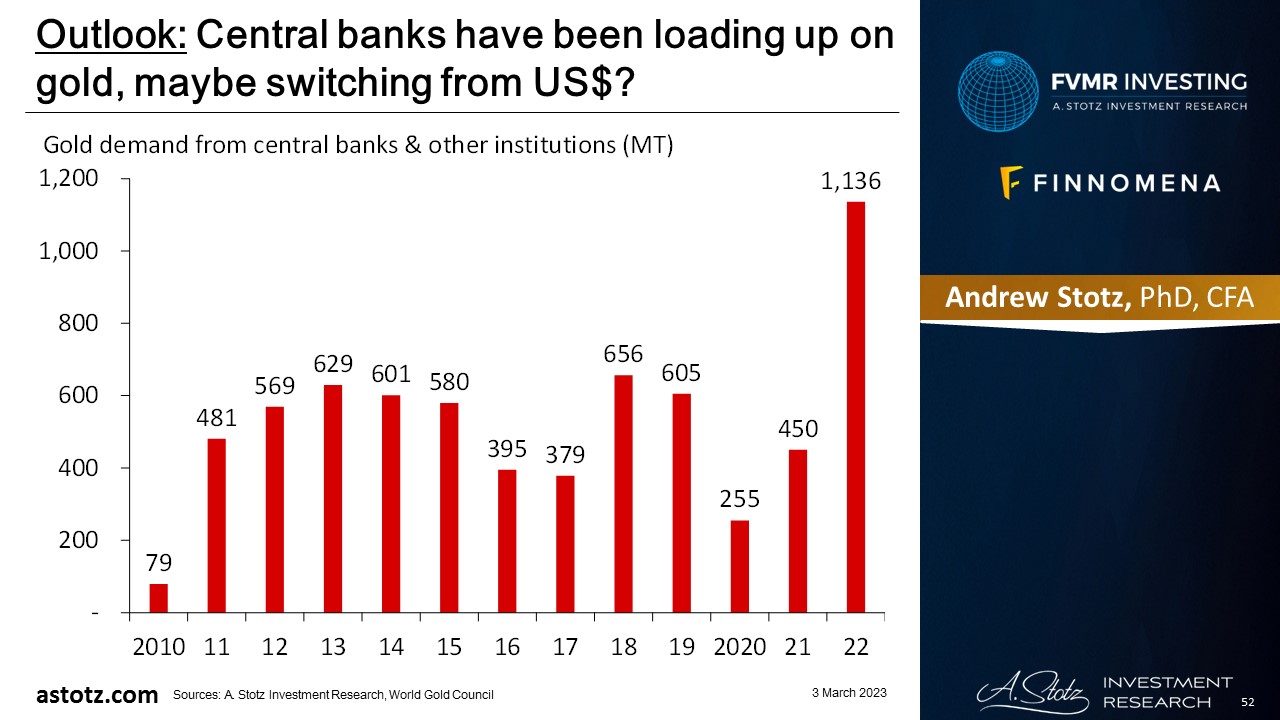

Central banks have been loading up on gold, maybe switching from US$?

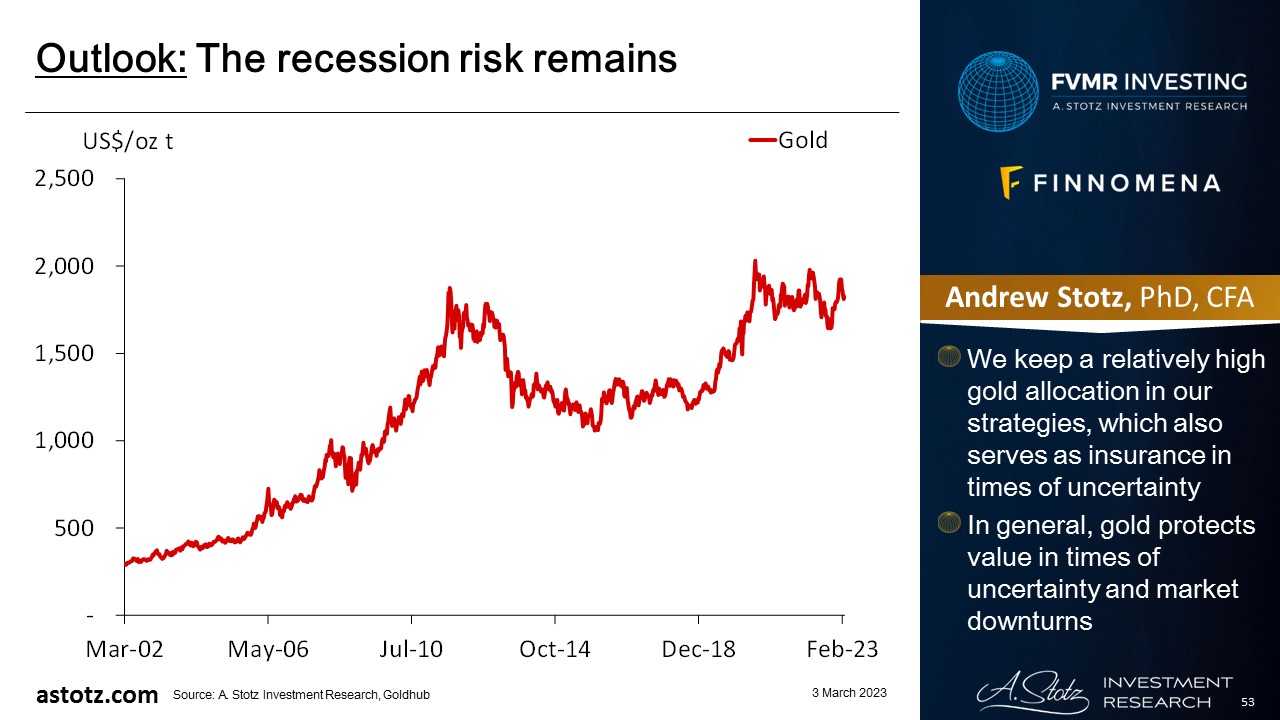

The recession risk remains

- We keep a relatively high gold allocation in our strategies, which also serves as insurance in times of uncertainty

- In general, gold protects value in times of uncertainty and market downturns

Risk: Inflation reaccelerates

- Central banks’ aggressive rate hikes and QT crash the stock markets

- We’re overweight Europe and Japan equity, so if these markets underperform, it will hurt our strategy’s performance

- Collapsing energy prices would be damaging to our tilt to World energy

- Our high gold allocation could get hit by higher rates or improved market sentiment

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.