US ROE 3 Percentage Points above World Average

US Equity FVMR Snapshot

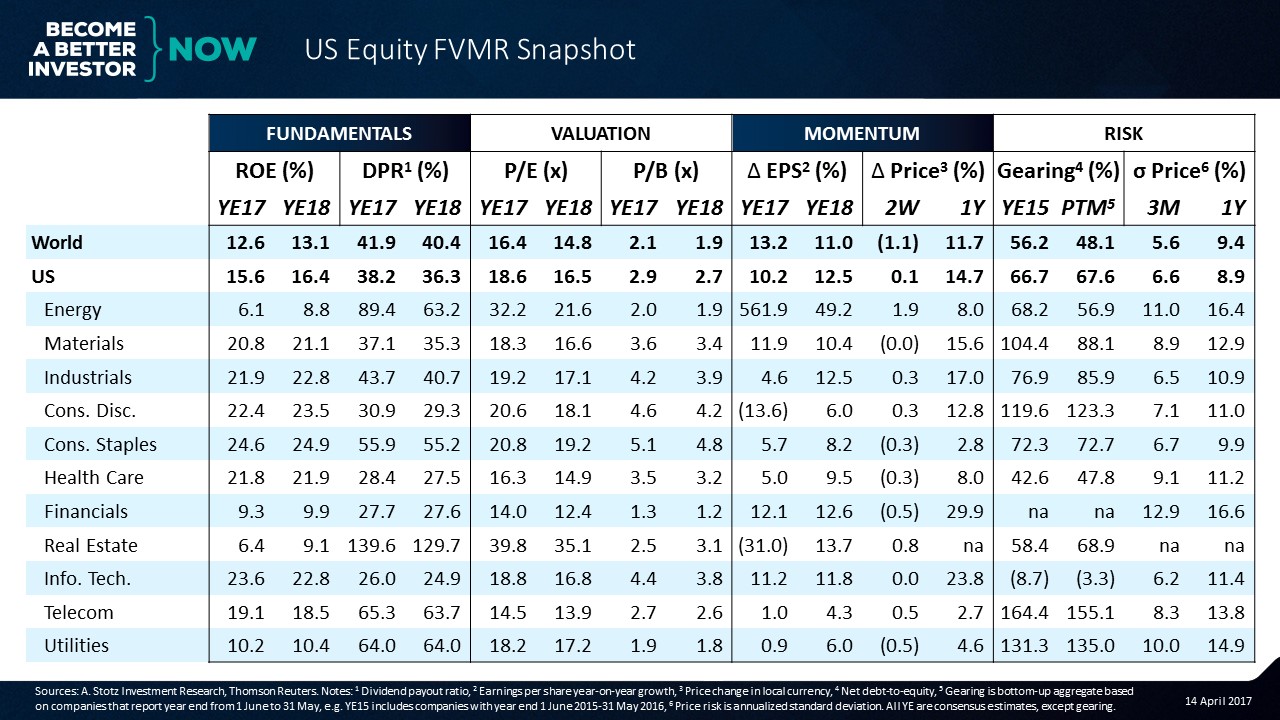

Fundamentals: US ROE 3 percentage points above world average

The first thing is just to understand what’s happening across the world versus the U.S.

We can see an ROE of about 13% across the world and a very impressive 16% ROE in the U.S.

With that good ROE, it doesn’t necessarily make sense to pay out a lot of dividends. Right now, U.S. companies are paying out about 37% of their profits as dividends.

Valuation: US somewhat expensive

If we look at the PE ratio, what we see is that the world is trading at 16x; and the U.S., about 19x.

Though the U.S. has a very high ROE relative to the rest of the world, what we can see is that you pay for that in the PE. And PE is relatively high, if we look at it relative to the long-term past.

Now, the next thing we can look at is the price-to-book ratio to understand the valuation. We can see about a 2x price-to-book for the world versus almost a 3x price-to-book for the U.S.

So on a price-to-book basis, the U.S. is still a bit expensive.

Momentum: US EPS expected between 10-12.5%

If we look at growth, we can see an expected 10% growth rate for 2017 and then a 12.5% expected growth rate the following year. Analysts tend to be optimistic, and we can see that they are right here.

Across the broad world, I’d say that growth estimates sit at about 11% for 2018.

I would say that the U.S. expectations for growth are mostly in line with the rest of the world, but you’re going to get a higher ROE and be paying a higher price-to-book and PE valuation.

That would tell me that the U.S. is a bit expensive at this point.

Now, if we look at the change in price over the last year, remember that the world includes the U.S. So if the world includes the U.S., it’s heavily weighted in that overall index as well.

What we can see is that 11.7% is how much price change there was over the past year worldwide, with the U.S. at about 15%. That actually means that if we could look at the world-ex U.S., it would be lower than the 11.7.

Risk: US higher than world in gearing

The gearing in the U.S. is a little bit high relative to the rest of the world at about 67%. That’s driven by a couple of sectors that are really high in the U.S.

If we look at price volatility though, it’s about in line.

The US market, by sector

We can see that the consumer staples sector has about a 25% ROE ─ impressive! In fact, these sectors all have more than 20% ROE. So a very impressive performance in the U.S.!

The U.S. ROE is being dragged down by energy companies because of lower oil prices, however, and we can see financials, real estate and utilities are almost always going to be lower because they’re regulated entities.

Overall, it looks pretty amazing.

If we go and look at the PE ratio for these sectors, we can see that with the energy sector, though ROE is low at 6%, PE is about 32x. That valuation is massive compared to other sectors.

Why?

Because this is a cyclical industry, and with oil prices rising, we’re seeing that there’s going to be a rise in earnings. So what looks like a high PE can actually be cheap for a cyclical industry like energy.

If we look at some of the other industries here, we can see that some of them are really expensive, such as the real estate industry.

We look at real estate on a price-to-book basis, because right now we can see that the earnings have collapsed for the real estate sector.

On a price-to-book basis, you get a more stable number and you’re talking about 2.5x to 3x.

With the market right now, analysts are expecting that this is going to recover.

Let’s just see if we can find a relatively cheap sector for a high ROE.

What we can see is that healthcare is trading at about 15x for a 22% ROE, and we can see information technology trading at about 17x for a 24% ROE.

That’s not bad. Those are interesting and good sectors.

If we look at price change right now, financials has been roaring back along with information technology.

Let’s look at gearing and understand the risk level. Some of these industries naturally have a pretty high level of gearing. We can see telecoms and utilities as examples.

Information technology just sits on a lot of cash on those balance sheets. They’re an asset-light type of business, so we don’t see any sizable amount of debt.

Sector volatility

Finally, if we want to look at the volatility of these sectors, let’s look at one-year volatility. And, of course, the volatility of the markets is a little bit lower because there are all kinds of stocks from all kinds of countries in the world and in the U.S.

But if you want to look at these sectors, that is an apples to apples comparison. And we can see that the most volatility is in the energy and financials sectors.

The lowest volatility is in the consumer staples sector and in the industrial sector.

Consumer staples are low volatility partially by nature. These are the things that you have to buy, as opposed to discretionary items like a car or a washing machine, which you have discretion over buying.

Consumer staples are things like food and coffee.

If you want us to look at your country, just leave a message in the comments below.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.