Learning Valuation: TPC Power Holding

Disclaimer:

This example was created on January 23, 2016. This is NOT a valuation, forecast, rating, or recommendation; rather, it is a teaching example. What follows is NOT investment advice; rather, it is a teaching example. It is intended only as academic information to those who want to learn about valuation. It should not be construed as the basis for any valuation or investment. The information in this presentation came from various sources which we believe are reliable, though we do not guarantee the accuracy, adequacy or completeness of such information. We hope you enjoy learning about valuation as much as we do!

Background

TPC Power Holding Public Company Limited is a Thai power producer that focuses on electricity generation and distribution from biomass. It plans to expand to other renewable energy sources as well.

TPCH has investments in seven main subsidiaries and holds majority stakes in six of them, all in Thailand.

TPCH owns the largest biomass power plant group in Thailand. Its main revenues come from dividends and servicing fees from shares in its subsidiaries, as well as income from providing supporting services to them.

TPCH sells and distributes the energy generated through PPAs and similar contracts. Within two years, the company is set to start up a hydro production plant in Laos (80MW) and two more biogas plants.

Basically, TPCH is a holding company but its only holdings are its subsidiary assets, which are the power plants.

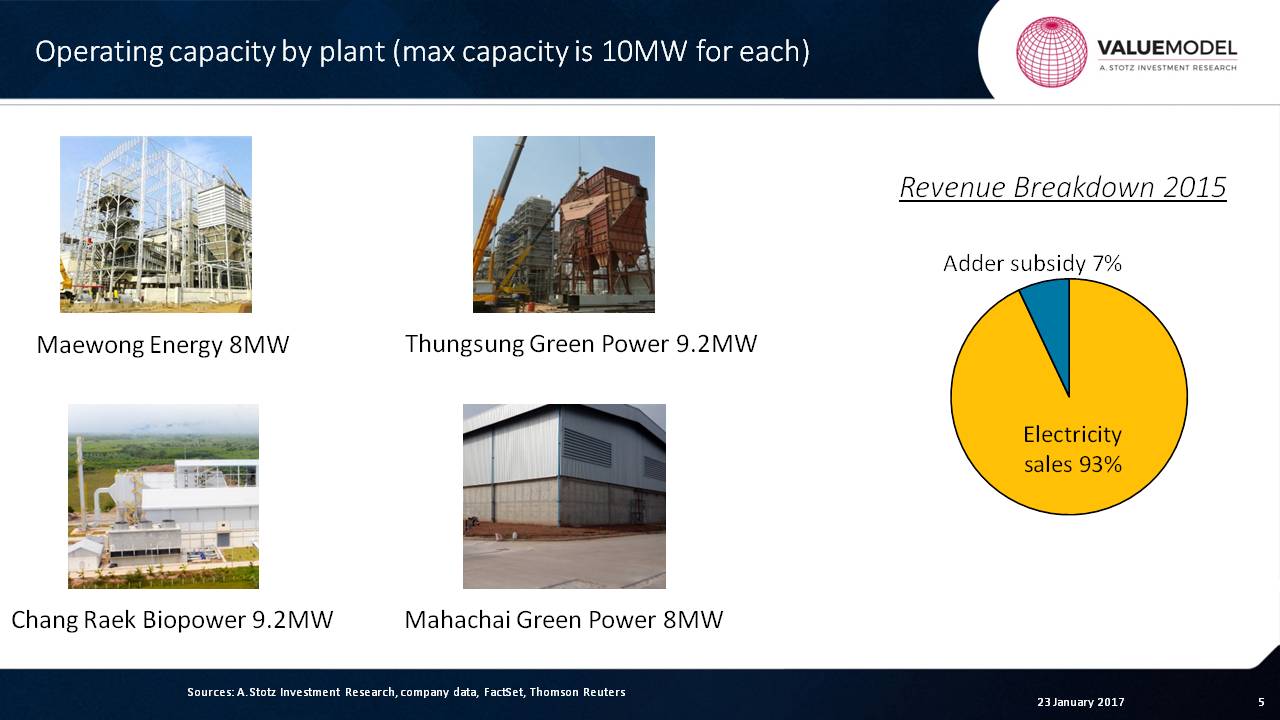

So if we go forward, we can see the operating capacity by plant: They’ve got the Maewong plant with 8 MW; the Thungsung Green Power at 9 MW; the Chang Raek Biopower plant at 9.2 MW and the Mahachai Green Power plant at 8 MW.

Next, we can see that the main revenue coming in is from electricity sales. “Adder subsidy” accounts for the government’s subsidy for the biomass industry.

Forecast

Let’s look at this company, and we can get a picture of what’s going on here.

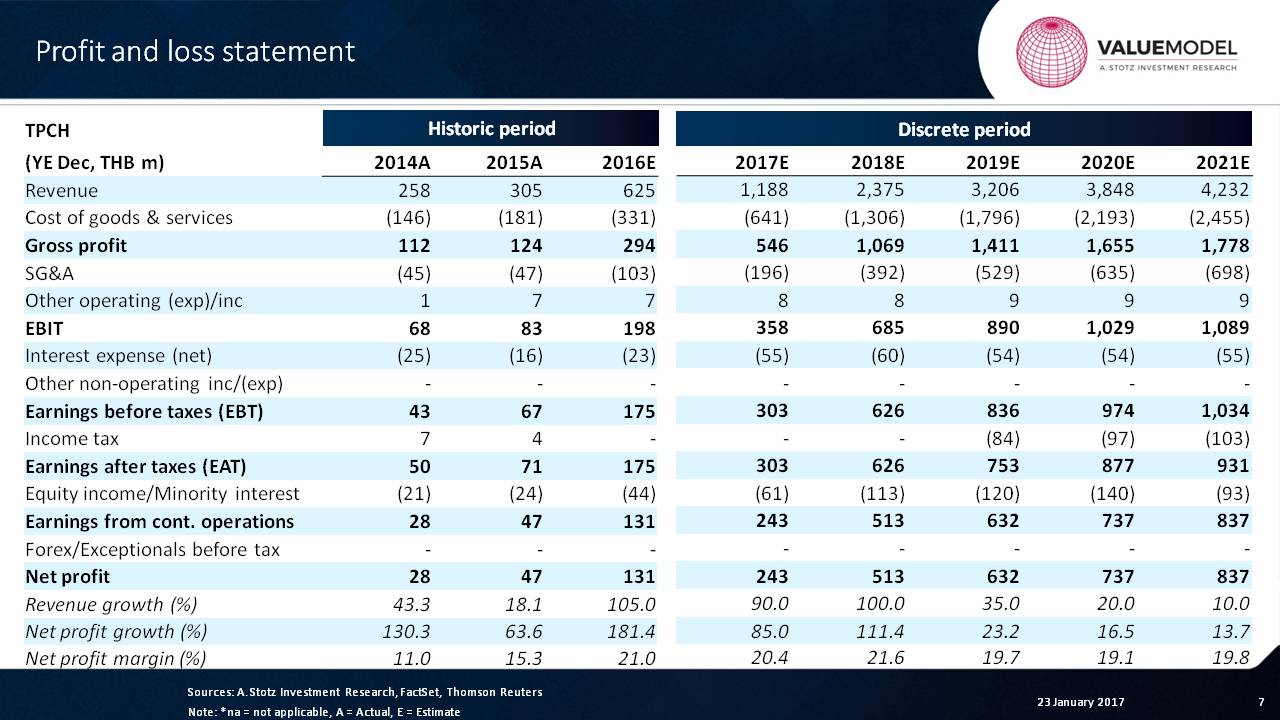

The first thing is we can see that the growth in the company has started to expand enormously, because the company is expanding quite quickly with new plants coming online.

So the growth in this company can be really strong in the next couple of years and then, eventually, start to slow down.

Right now, the profit margin is getting high and, of course, they’re getting economies of scale as they add more facilities, because the parent company is servicing all the subsidiaries. So the overhead cost of the parent company can be spread over a wider group of subsidiaries.

Assets

Now, let’s talk about what’s going on with the balance sheet.

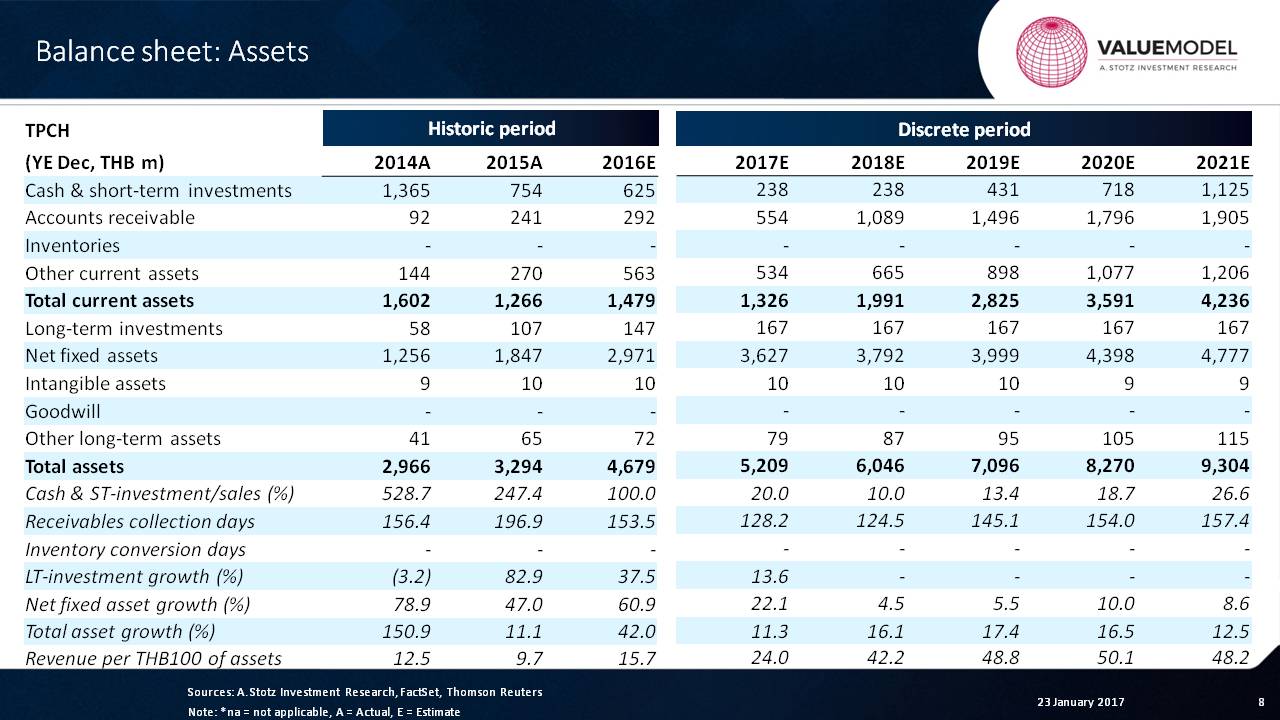

Here we can see that the growth in net fixed assets has been pretty massive. It’s going to slow down a bit, and then it will eventually slow down more as they get bigger.

They’re still going to add more plants, but this is the main portion of the time when they are adding facilities. As a result of that, we can see that they’re getting more and more revenue per asset in the future.

Liabilities and Equity

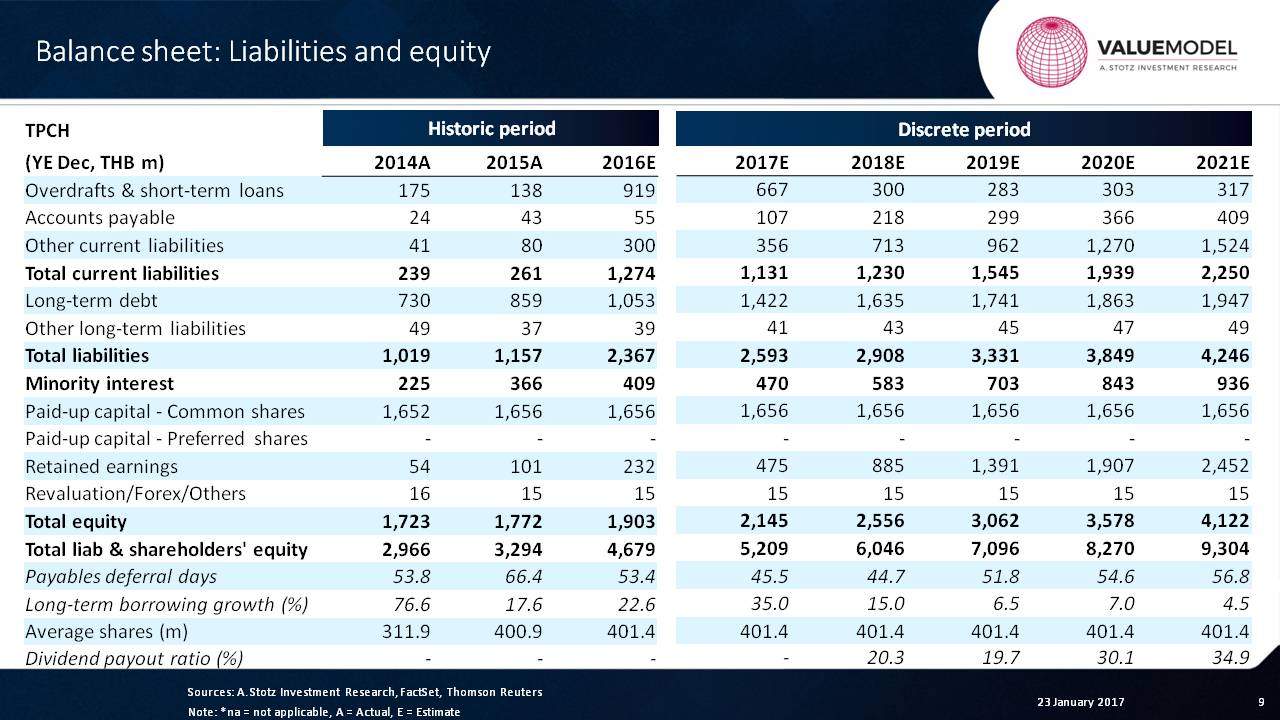

If we look at this company’s structure right now, it’s got short-term borrowings that just jumped up to about 900 million baht, but their profitability is going to feed that. In addition, they’ve been issuing some long-term debt, and we expect that that will probably continue.

The key thing here is that as they make more and more profit, that’s going to drive up retained earnings, and that will be part of how they finance this business.

We’re expecting the dividend payout ratio to be about 20%, to increase to 30%, and then to 35%.

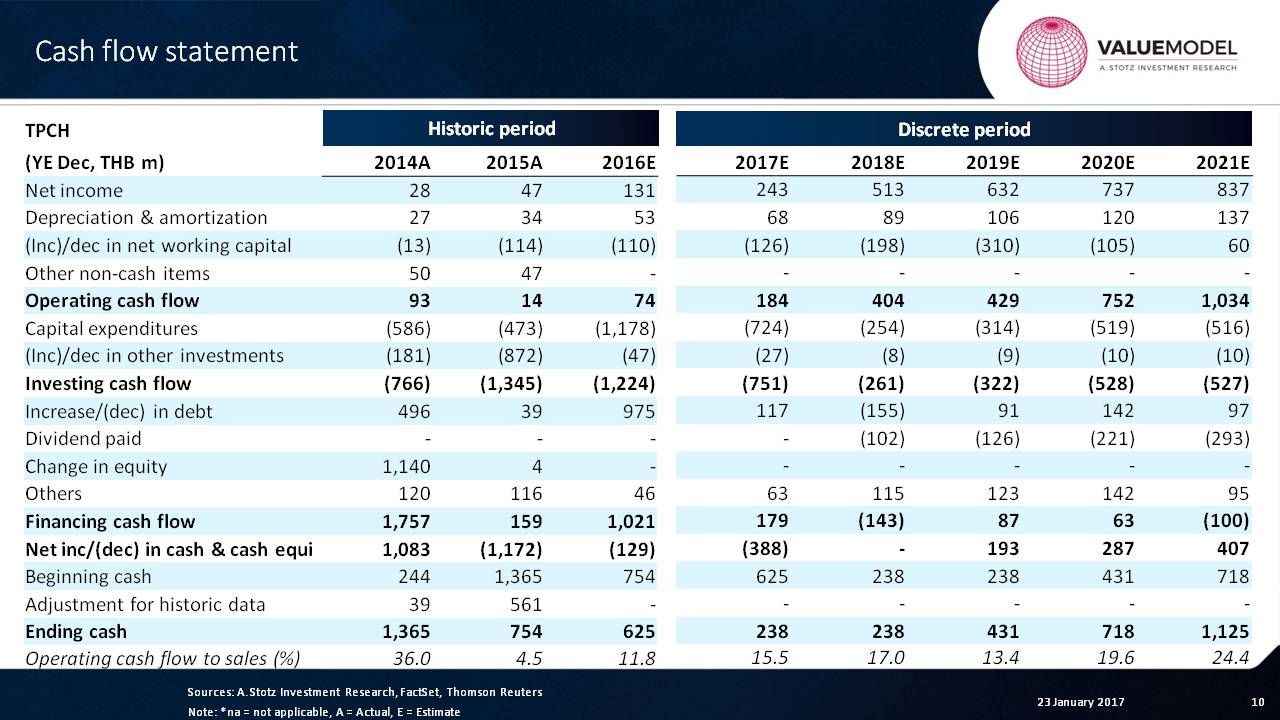

Cash Flow

If we look at the cash flow, we can see that the amount of CAPEX has been pretty large here but starting to slow in our forecast. The result is that they’ve been in a big investing period.

When you compare that investing to the amount of operating cash flow, it’s pretty low. But what we’re going to see soon is that the operating cash flow at this point is going to cover the amount of investment, based upon our projections.

Of course, if they’ve got massive opportunities, it may be that they increase the amount of investment allocated at this time, but this gives you an idea of how a company moves from a negative free cash flow basis to a positive one. And, of course, all that means is that the company can start paying out dividends, which we can see right here.

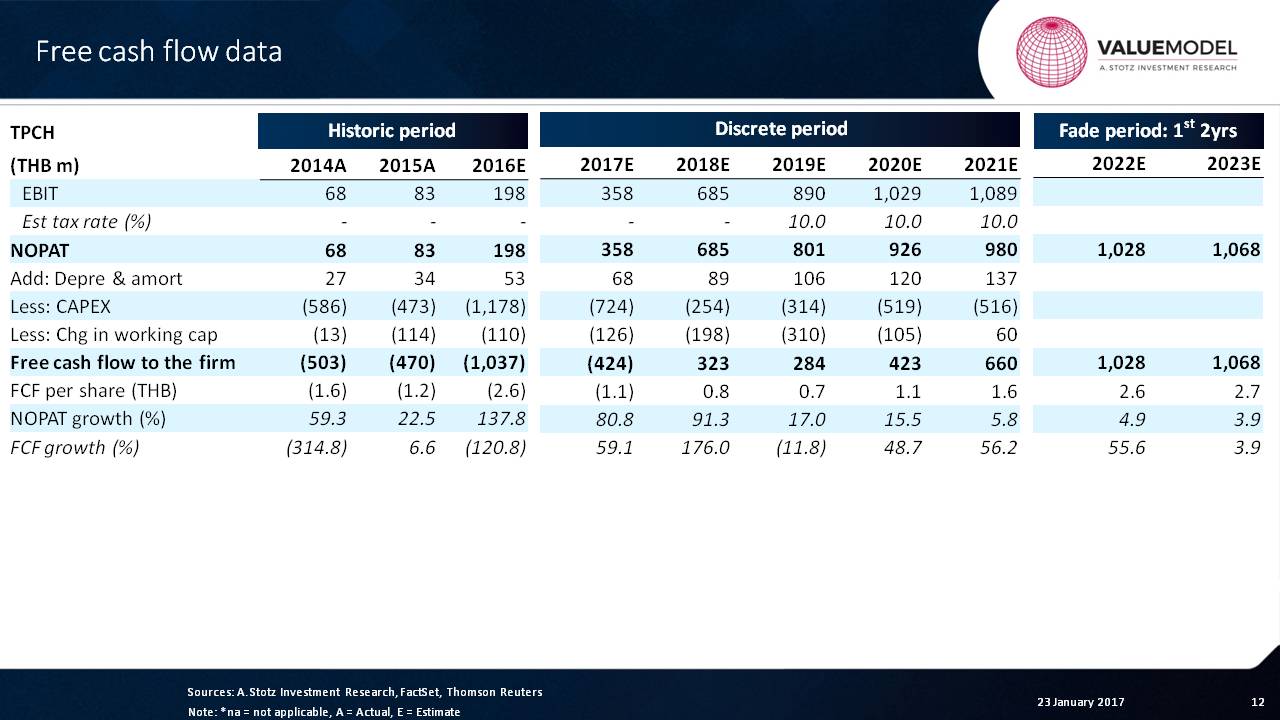

Free Cash Flow

Next, let’s move into valuation and let’s look at what’s happening with the EBIT and what’s called “net operating profit after taxes” (NOPAT).

It’s very small. As the company ramps up, it gets bigger and bigger and bigger. Eventually, the company will have to pay some taxes, but they’re going to get a lot of tax holidays due to the fact that they’re green energy.

And if we see the amount of free cash flow to the firm ─ of course, free cash flow to the firm is investment related to CAPEX and investment related to working capital ─ what we can see is that that free cash flow to the firm is very negative in these years but eventually starts to get positive as they generate more and more NOPAT.

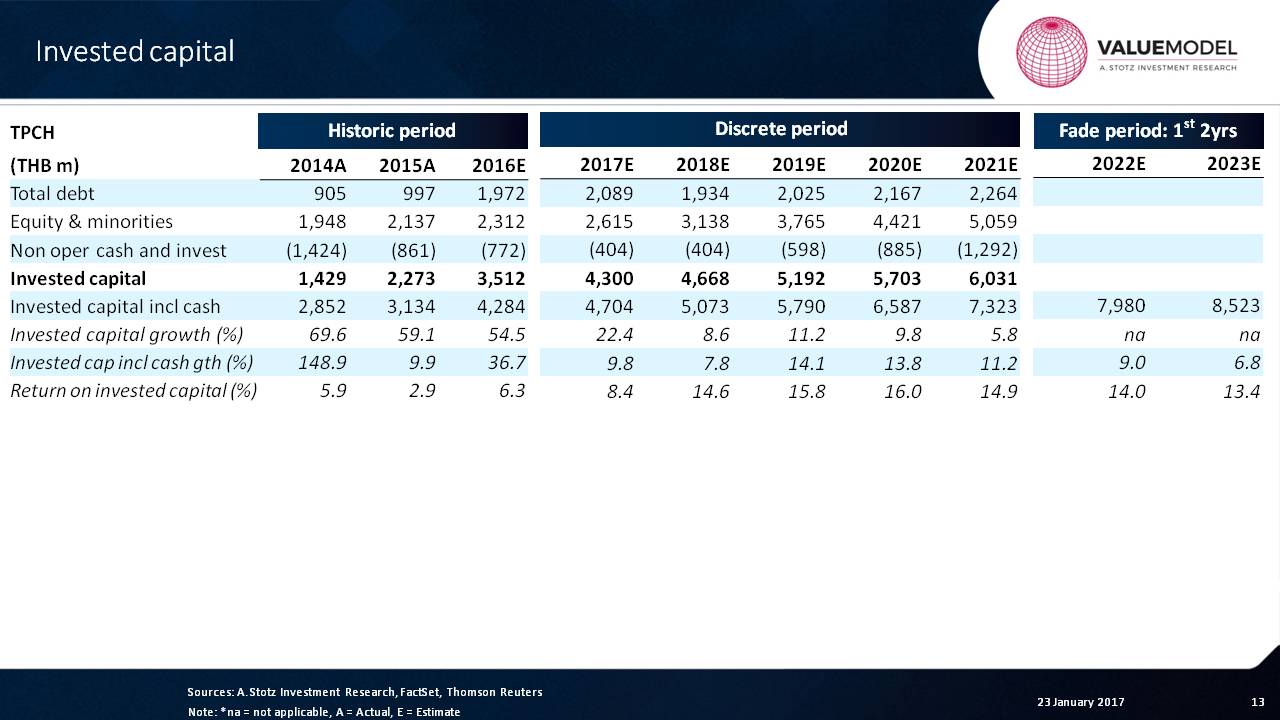

Invested Capital

This business has been expanding. It’s basically doubled over that period of time, and it eventually will grow but at a slower pace. It will take until after 2021 before they double their invested capital here.

We can also see that the return on invested capital has started to rise and should continue to be very strong in future years. The thing to remember is that this business is a very stable business with government contracts.

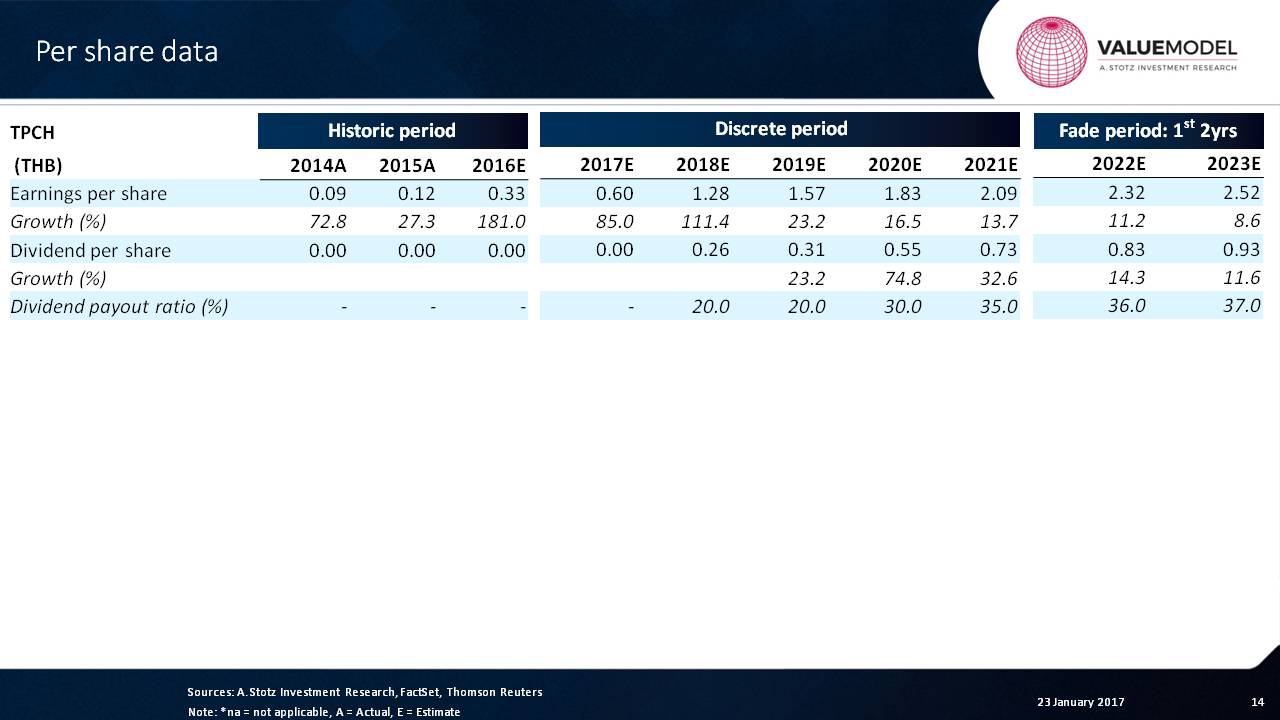

If we look at the earnings per share, it’s been positive. Now it’s starting to jump, and we’re going to see that the dividend payout ratio is rising. Since it is, we’re going to see the dividends per share go from nothing in this period of time to start growing incredibly fast. So we can see very fast growth there in dividends per share.

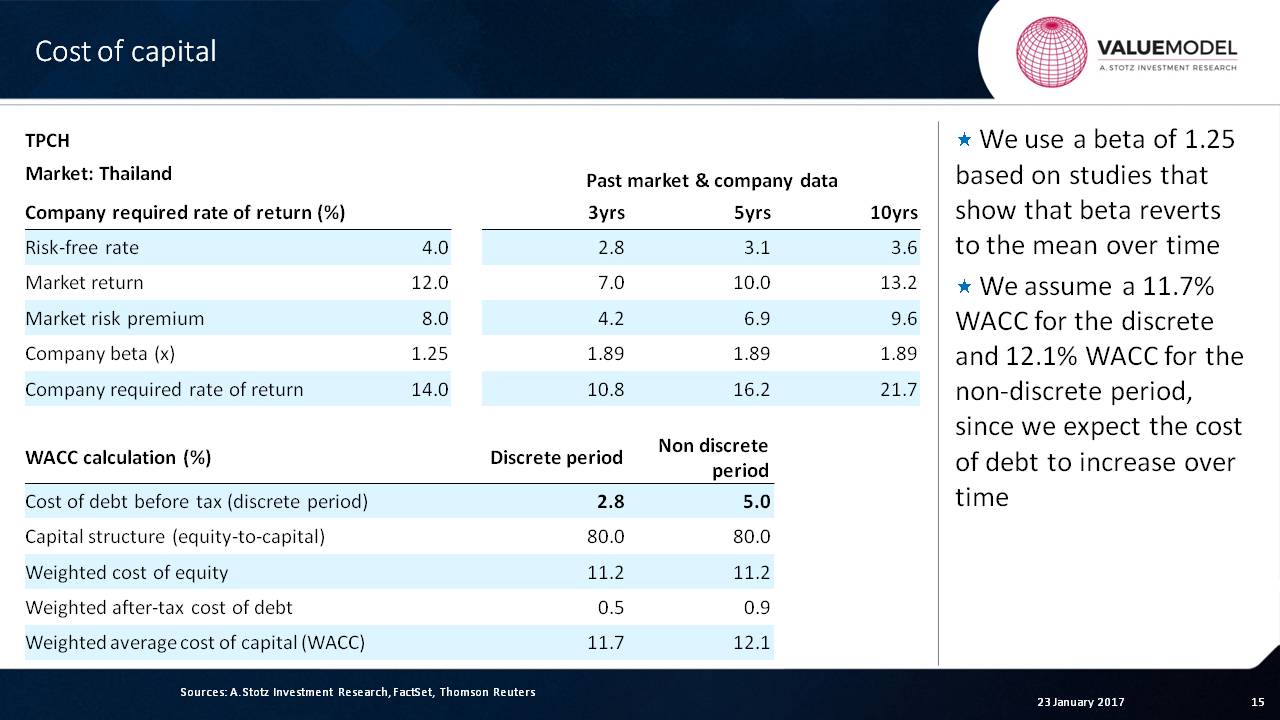

Cost of Capital

This company over the years has been pretty volatile. But the truth is that this volatility should fall over time as its revenue streams come in. And these are very steady revenue streams.

So we’re going to bring the beta down to 1.25 ─ this is our market information for Thailand ─ and that gives us a required rate of return of 14%.

Now, the company finances about 80% of its capital structure as equity. So if we want to calculate the weighted cost of capital with a debt level of 2.8% and a debt level of 5.0%, it will rise over time as we can see. But the cost of equity is higher, of course, than the cost of capital.

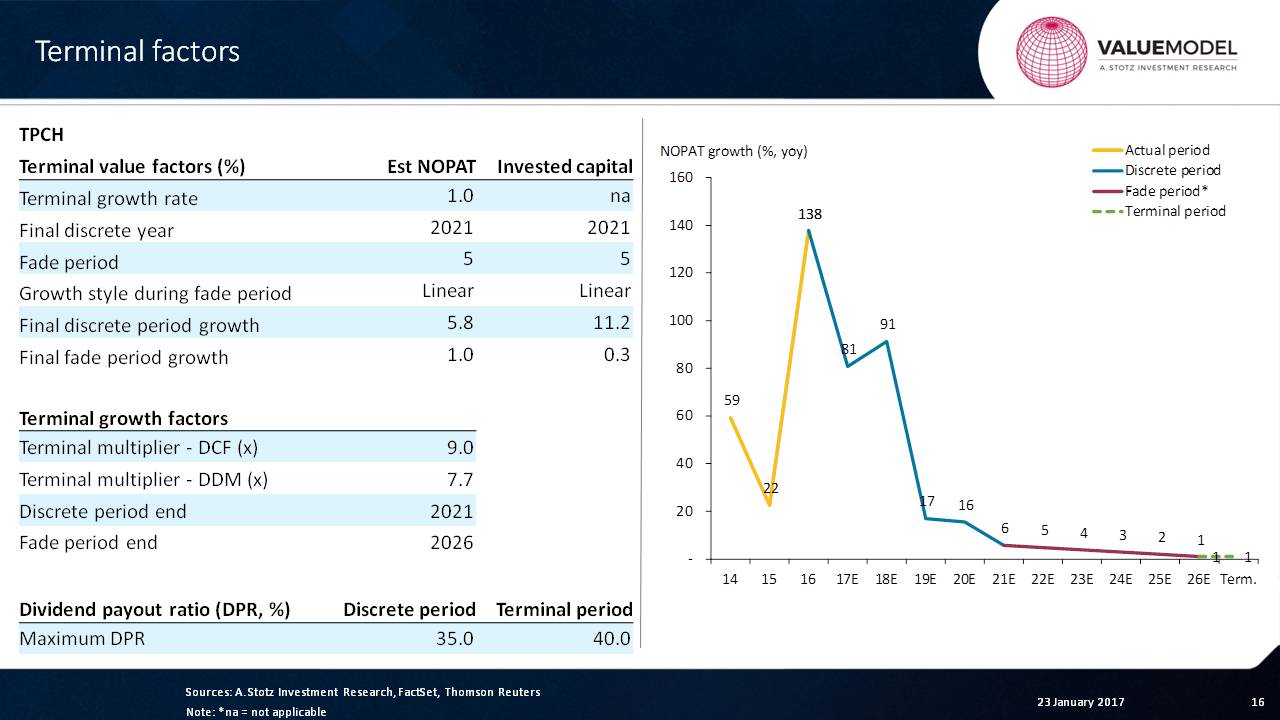

Terminal Factors

Next, let’s take a look at our terminal growth assumption, which is very conservative at 1%. It’s conservative because most of the value of this company really is coming in the future period, so we have to be careful not to put too much value on that terminal value, because if we were to value the last or the next couple of years, the cash flow actually is pretty low.

If we go back and look at that free cash flow calculation, which was right here, we can see that free cash flow has actually been negative and is only starting to rise.

If we value only this discrete period right here, the value of this company is going to be tiny. Actually, this is part of the discrete period.

So the value of this discrete period is going to be tiny. That means that a lot of value is put into the fade and the terminal period, so we have to be very careful when we’re selecting the terminal growth rate.

What we can see from this is that the multiples that were valued in this company at that terminal period are about 8x to 9x, which is pretty reasonable.

We can see here that we have a fade period that’s about five years, and that fades down the NOPAT growth.

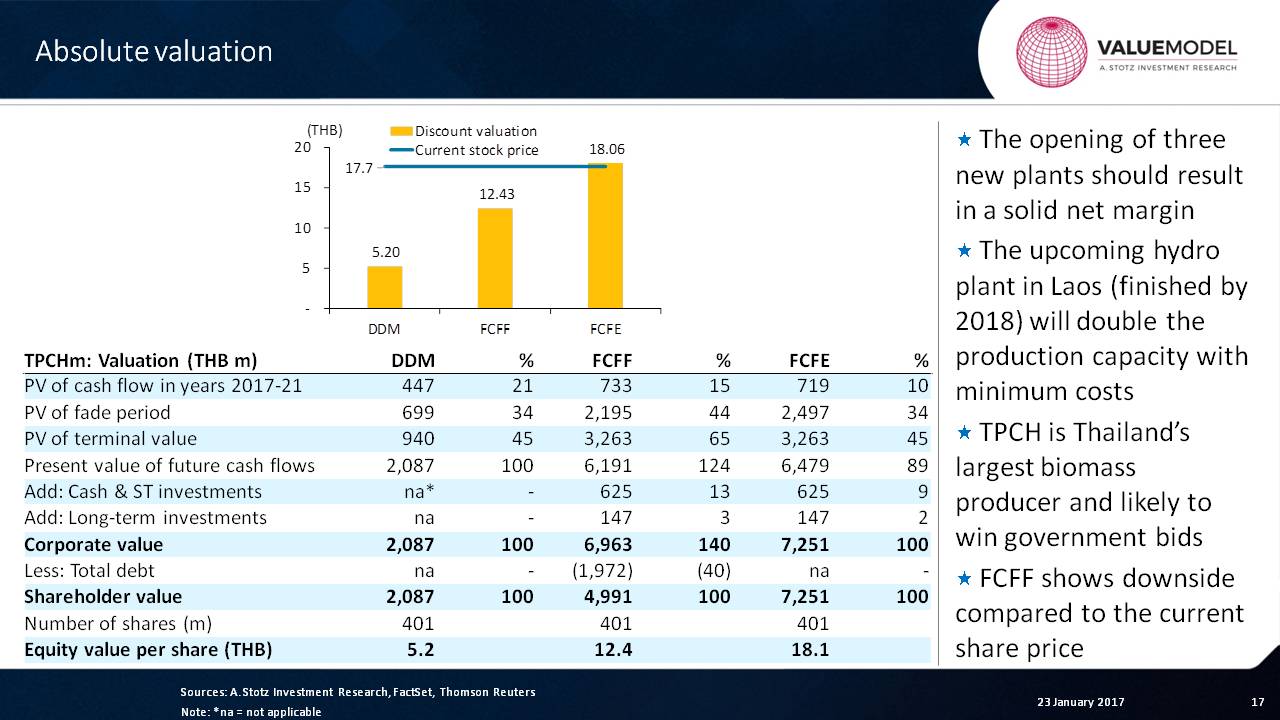

Absolute Valuation

And if we continue with those assumptions, what we can see is that, on a DDM basis, it’s valued at about 5x. On a free cash flow to the firm at about 12x; and on a free cash flow to equity at about 18x.

So what should be the actual value of this company?

That’s a great question. Actually, we may not be able to perfectly answer this, but let’s go through some of the information.

The first thing we can see is that free cash flow to the firm puts a lot of value on that terminal value. We can also look at it another way by saying that the present value of that cash flow in the discrete period is 21%, 15% and 10% right here.

So free cash flow to equity is really strong, but it’s putting all the value into the fade and into the terminal period.

This gives us some idea of the way the company looks. Overall, it appears that the stock price is above, at least, these two and in line with this one.

So is it cheap or expensive?

That’s the question that we’re trying to answer.

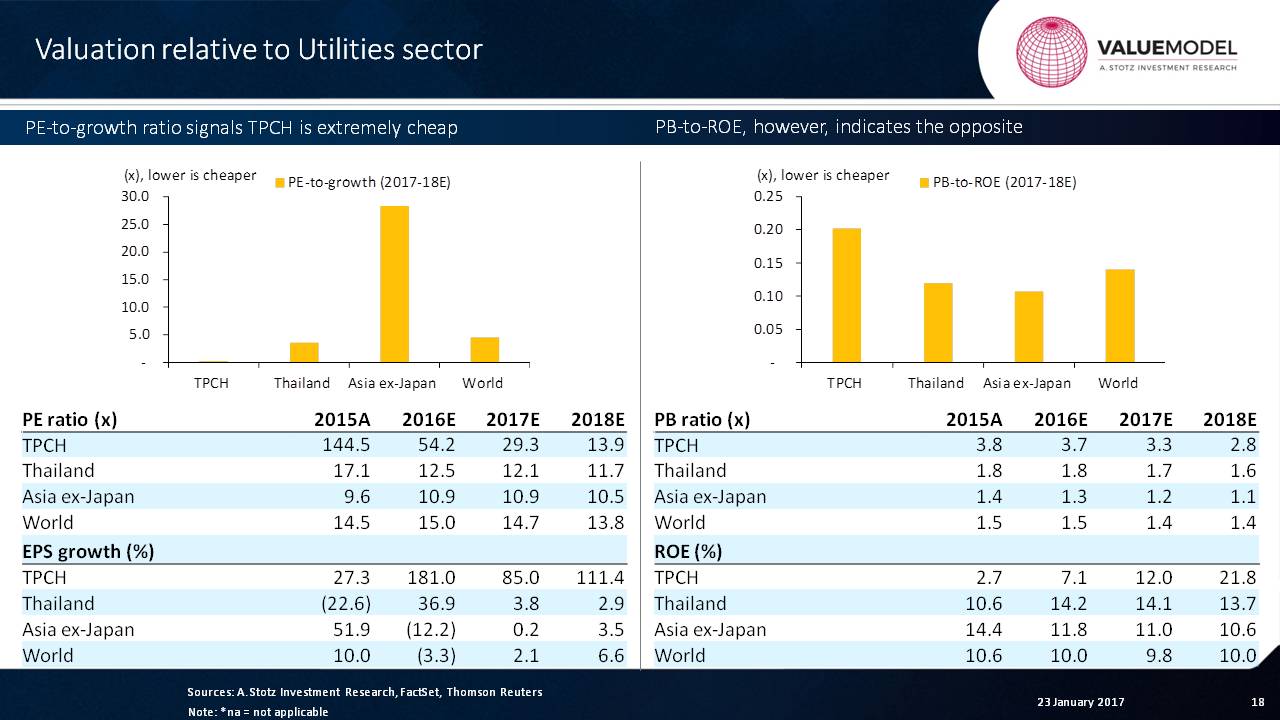

Relative Valuation

We’re going to see this company relative to the utility sector.

The first thing we want to do is look at the PE ratio, and we can see that the company is accelerating its growth quite fast ─ earnings growth at 111%.

Is that an exceptional item?

No, that’s real, because the facilities are coming online.

So really, we’re looking at PE-to-growth over a period of two years. But the truth is that the PE-to-growth ratio may be more reasonable, if we look at it over three or four years, something like that.

At this point, this company looks super cheap.

Now, if we go to the price-to-book ratio, we’ve got the same issue here. The ROE of the company is going from 3% to 7%, to 12% and then onto 22%.

Again, if we’re going to take the average of these two years, it’s going to appear that this company is overvalued relative to its peers in Thailand, Asia, and globally.

The truth is, if we were to use that same ratio using only 2018, we may find that that would make it cheap relative to the others.

Sensitivity Analysis

Now, if we just look at the sensitivity for a bit, what we can see here is that the sensitivity can be pretty high when we look at the gross margin. A 5-percentage point change in gross margin can cause this jump in EPS growth.

And what we can see on this side is that the value of the company could be 12x, 9x or 16x, depending on what’s happening.

We can also see that we can change the required rate of return to 14% to 15% or from 14% to 13%, and that will have a small impact on the free cash flow valuation of the business.

There you have it. That is TPCH. What you can see is that it’s hard to perfectly value a company that’s putting new facilities into their business.

From this, you would say, “Well, it looks a little bit expensive.” But if we were to look at the revenue and profits that are coming, it appears that maybe the company is cheap.

Keep on learning!

Have you got any questions?

Just leave a comment and we’ll try to answer it.

Have a great day!