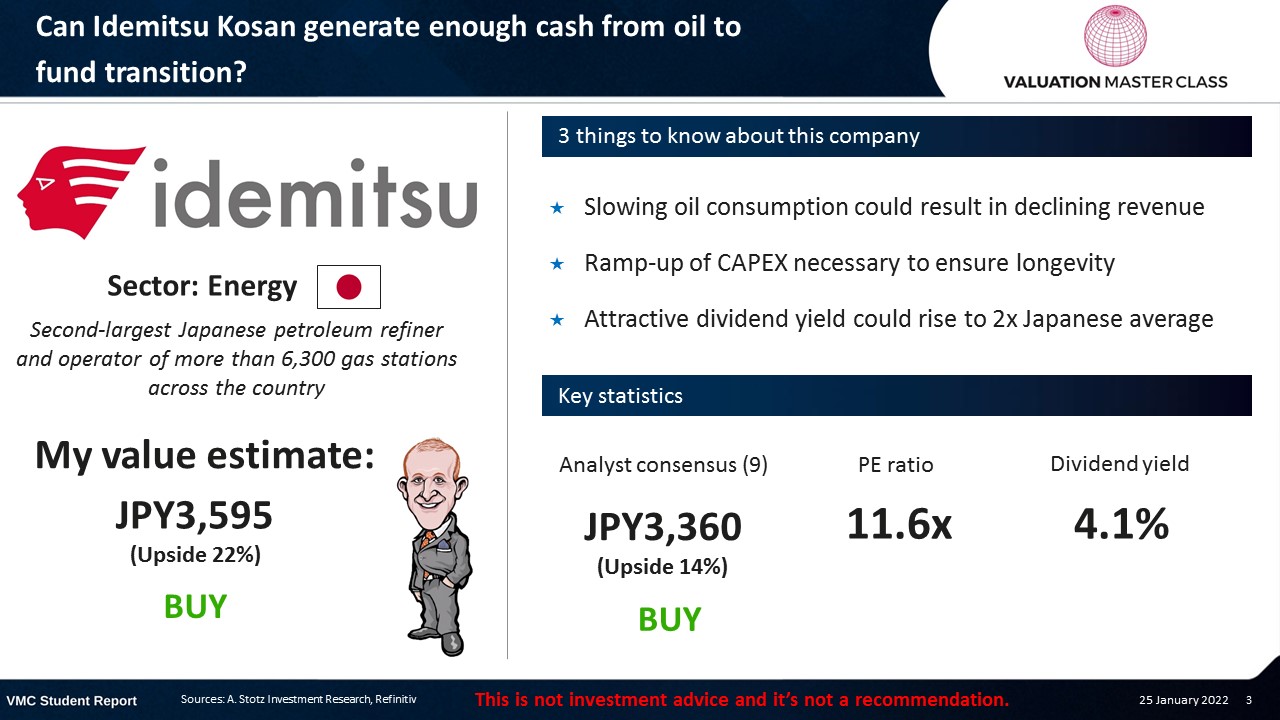

Can Idemitsu Kosan Generate Enough Cash From Oil to Fund Transition?

The post was originally published here.

Highlights:

- Slowing oil consumption could result in declining revenue

- Ramp-up of CAPEX necessary to ensure longevity

- Attractive dividend yield could rise to 2x Japanese average

Download the full report as a PDF

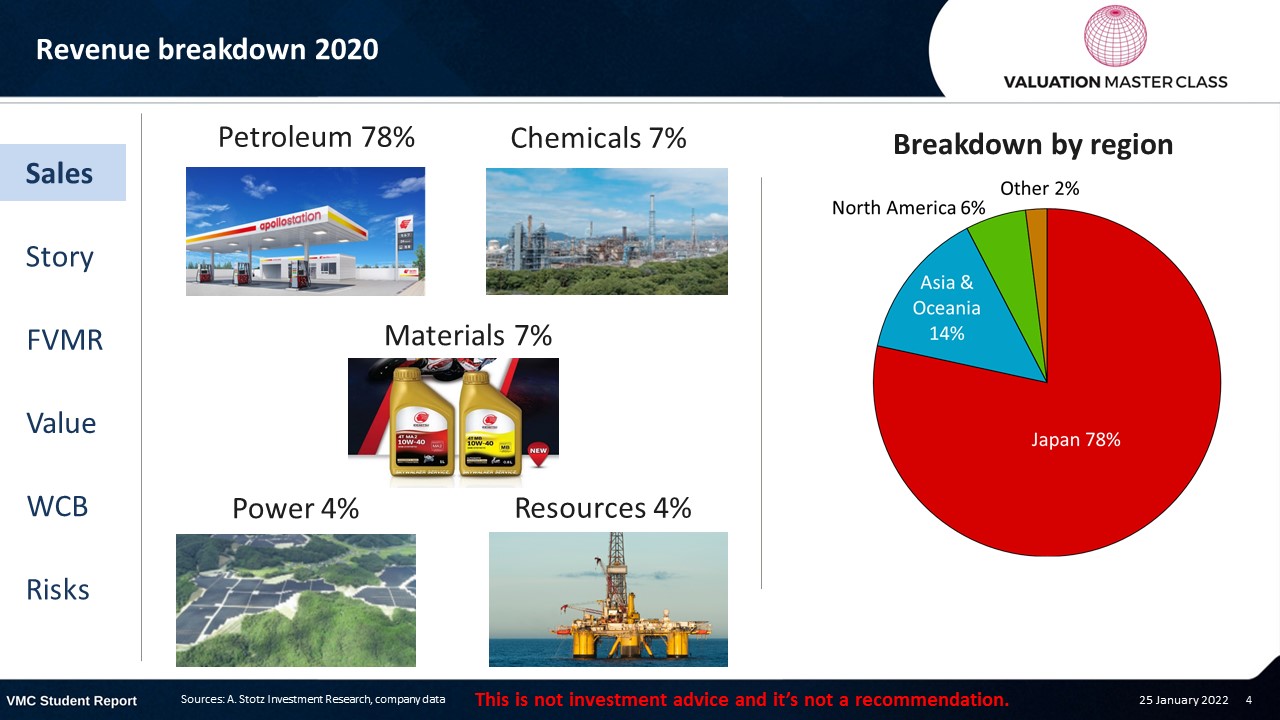

Idemitsu Kosan’s revenue breakdown 2020

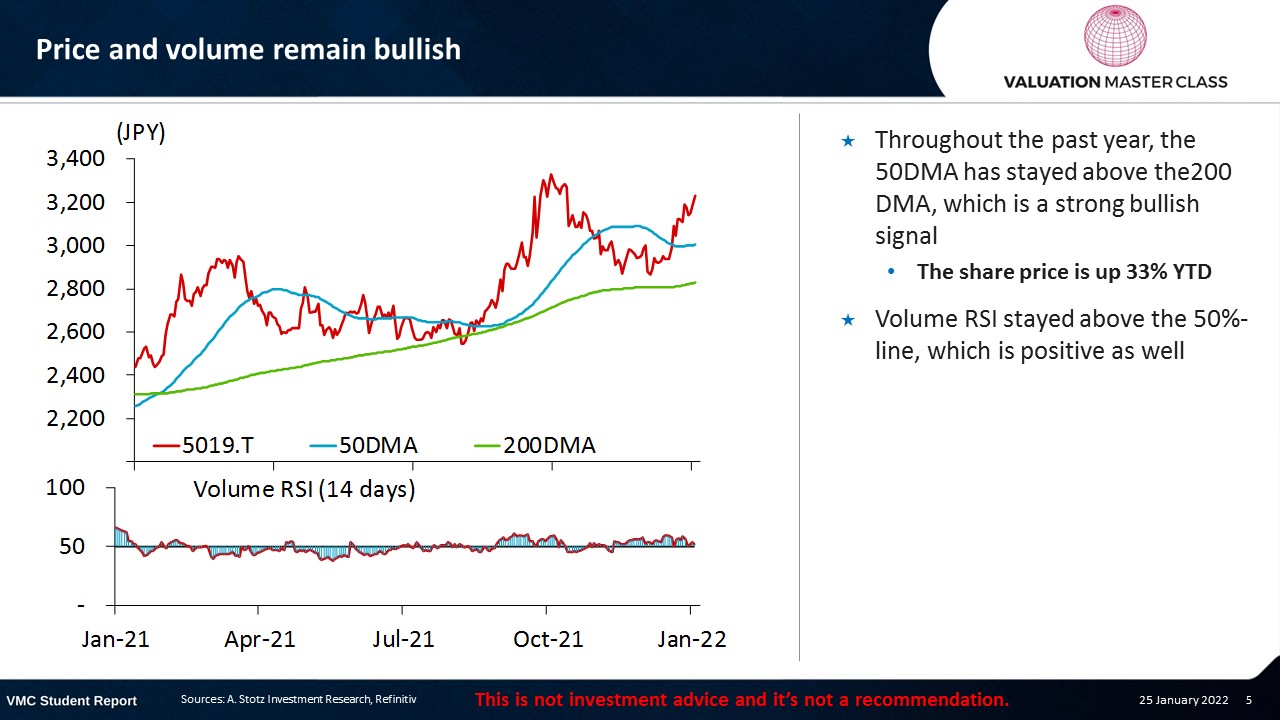

Price and volume remain bullish

- Throughout the past year, the 50DMA has stayed above the200 DMA, which is a strong bullish signal

- The share price is up 33% YTD

- Volume RSI stayed above the 50%-line, which is positive as well

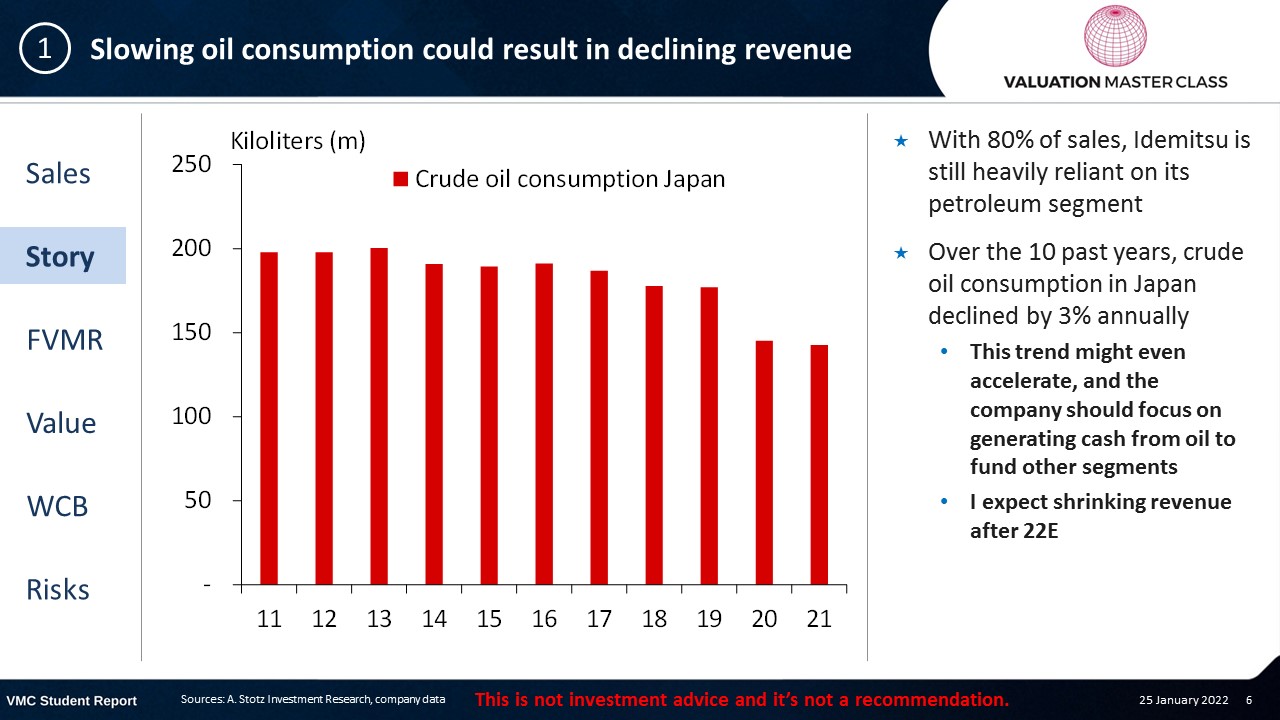

Slowing oil consumption could result in declining revenue

- With 80% of sales, Idemitsu is still heavily reliant on its petroleum segment

- Over the 10 past years, crude oil consumption in Japan declined by 3% annually

- This trend might even accelerate, and the company should focus on generating cash from oil to fund other segments

- I expect shrinking revenue after 22E

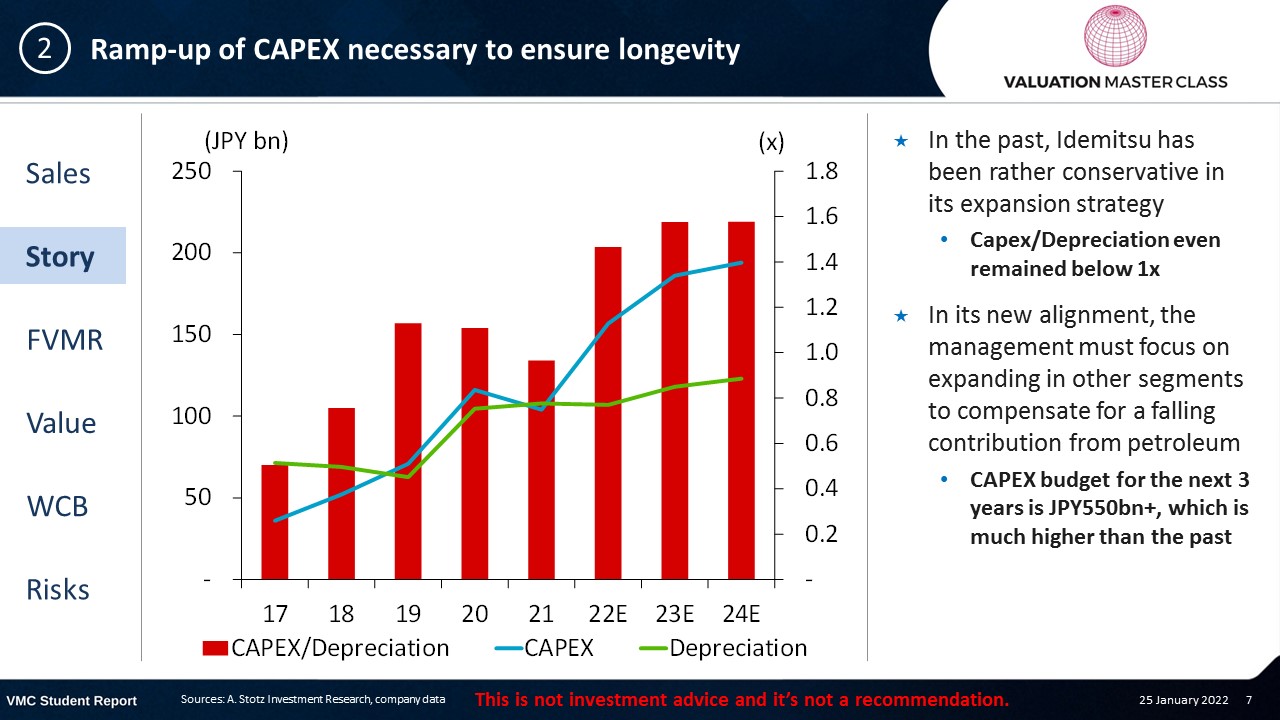

Ramp-up of CAPEX necessary to ensure longevity

- In the past, Idemitsu has been rather conservative in its expansion strategy

- Capex/Depreciation even remained below 1x

- In its new alignment, the management must focus on expanding in other segments to compensate for a falling contribution from petroleum

- CAPEX budget for the next 3 years is JPY550bn+, which is much higher than the past

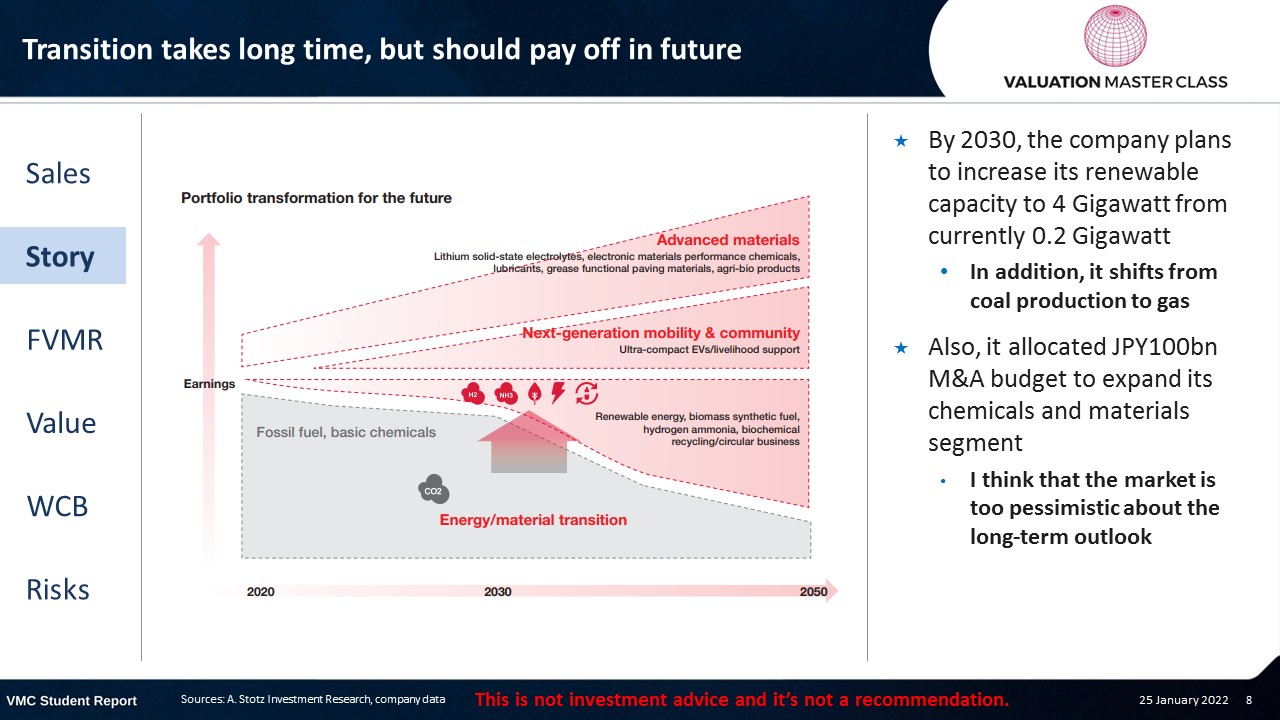

Transition takes long time, but should pay off in future

- By 2030, the company plans to increase its renewable capacity to 4 Gigawatt from currently 0.2 Gigawatt

- In addition, it shifts from coal production to gas

- Also, it allocated JPY100bn M&A budget to expand its chemicals and materials segment

- I think that the market is too pessimistic about the long-term outlook

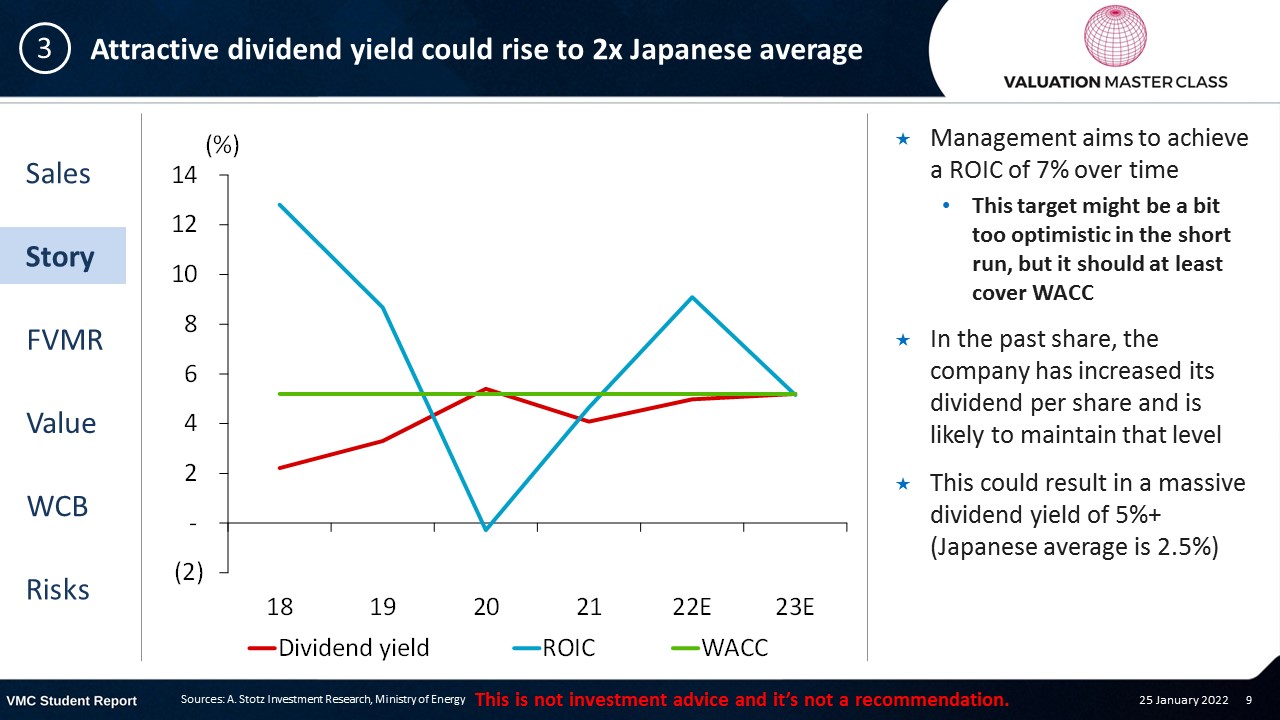

Attractive dividend yield could rise to 2x Japanese average

- Management aims to achieve a ROIC of 7% over time

- This target might be a bit too optimistic in the short run, but it should at least cover WACC

- In the past share, the company has increased its dividend per share and is likely to maintain that level

- This could result in a massive dividend yield of 5%+ (Japanese average is 2.5%)

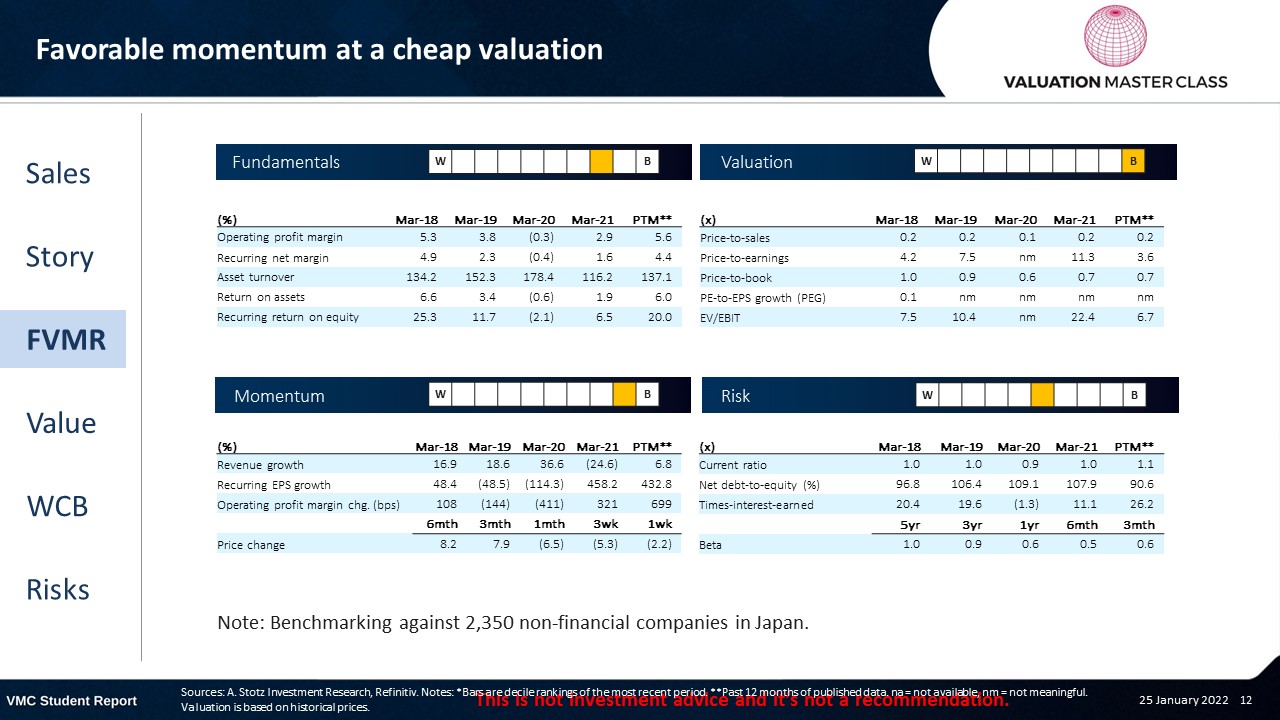

FVMR Scorecard – Idemitsu Kosan

- A stock’s attractiveness relative to stocks in that country or region

- Attractiveness is based on four elements

- Fundamentals, Valuation, Momentum, and Risk (FVMR)

- Scale from 1 (Best) to 10 (Worst)

Analysts see small upside, but remain cautious

- Currently, there is no catalyst in place, that would lead to excessive optimism

- Most analysts are still on HOLD

- Consensus expects a record revenue in 21E

- However, as oil price tends to normalize, the company is likely to face shrinking revenue in 22E and 23E

Get financial statements and assumptions in the full report

P&L – Idemitsu Kosan

- Strong bottom-line mainly driven by inflated oil prices worldwide

- The Japanese gov’t announced to release some of its oil reserve to prevent a further spike in price

Balance sheet – Idemitsu Kosan

- As of 2021, Idemitsu has a cash-to-assets ratio of 3%

- Low cash generation ability might result in conservative expansion plans

- Idemitsu has moderate high leverage

- Its net-debt to equity ratio stood at 0.9x in 2021

Ratios – Idemitsu Kosan

- Unlike other petroleum companies, Idemitsu has a very high efficiency

- Gross margin in 21E and 22E continues to stay on a high level, attributable to high oil price rather than efficiency gains

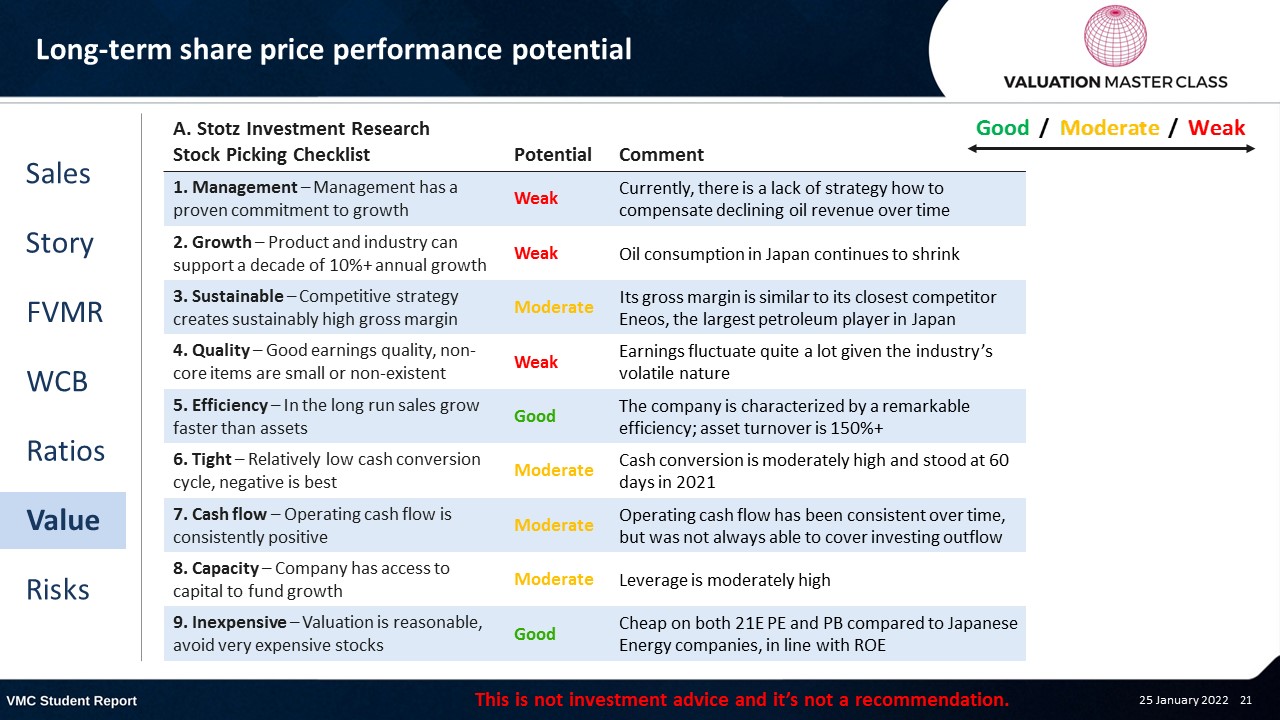

Long-term share price performance potential

Free cash flow – Idemitsu Kosan

- FCFF likely to remain volatile given abrupt changes in working capital

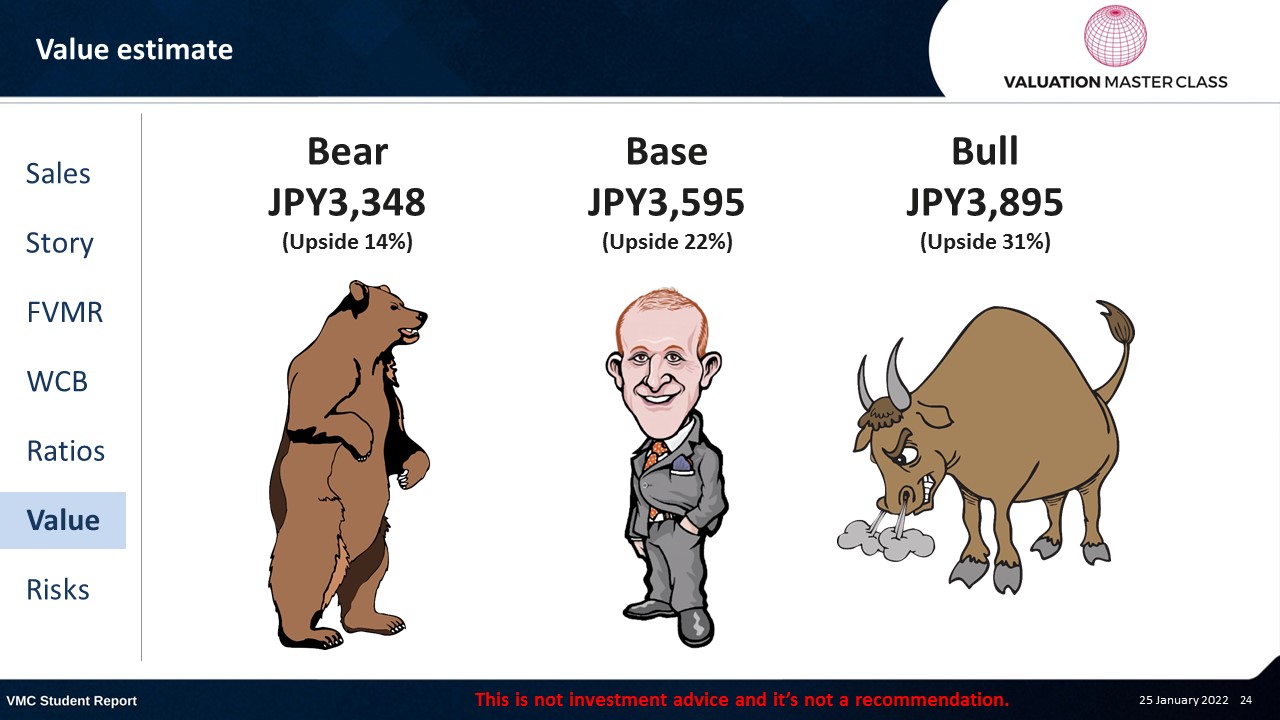

Value estimate – Idemitsu Kosan

- I expect a higher revenue drop in 23E and 24E than the consensus

- However, my long-term outlook is a bit more optimistic

- Idemitsu should be able to focus on its other segments to diversify away from oil

- Historically, Japan has a very low risk-free rate

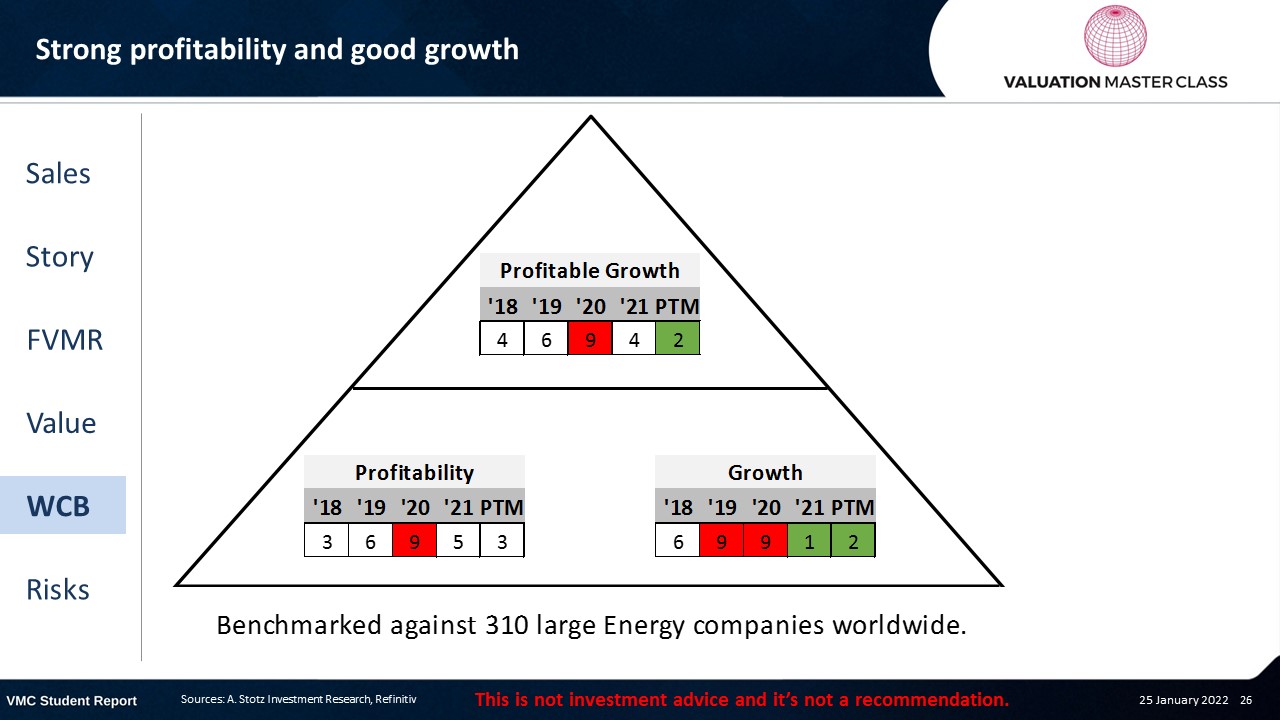

World Class Benchmarking Scorecard – Idemitsu Kosan

- Identifies a company’s competitive position relative to global peers

- Combined, composite rank of profitability and growth, called “Profitable Growth”

- Scale from 1 (Best) to 10 (Worst)

Key risk is high dependency on oil

- Adverse regulatory changes could accelerate phase-out of fossil fuels

- Failure to identify suitable expansion opportunities for non-oil business segments

- Lower than expected operating cash flows could hamper expansion plans as the company has not much cash reserves

Conclusions

- Petroleum segment strong in short run but does not ensure longevity

- Management’s plans to expand other segments should drive revenue growth in the long run

- A 5% dividend yield at cheap valuation might be already attractive enough

Download the full report as a PDF

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.