Do Not Avoid Risk, Manage It

What is risk?

An essential part of investing is risk management; in the long run risk management often matters more than picking the highest performing assets at certain points in time. So, what is risk?

On the one hand, risk is the possibility of losing something of value; in investing, this is often losing monetary value. Risk is also about taking action in an environment of uncertainty. While risk and uncertainty may appear to be the same, the two are often separated. Uncertainty is unmeasurable and uncontrollable, while risk is quantifiable and can, therefore, be managed.

In our effort to be as general as possible in our definition of investment risk, we define it as permanent loss of capital, i.e., you end up with your capital being of less value at the end of your investment horizon. The size of the loss is also relevant, e.g., if you lose 5% of your invested capital compared to losing all of your wealth, it affects you in different ways. A 5% loss is likely to be manageable, while losing all your wealth may lead to complete ruin or even death.

Another broad definition of investment risk is to not meet your investing goals, so-called shortfall risk–may it be financial independence at the age of 40, a comfortable retirement at 65, or something else.

In the world of finance, the relationship between risk and return is a central idea; if you take on more risk, you’re expected to have the chance to earn a higher return.

Different types of risk in investing

Investment risk can be general or asset-specific. In this post, we’ll look at some common risks when investing in stocks, bonds, gold, and commodities. This is not a complete list of risks involved, but a few we believe you should be aware of and consider.

The broadest type of investing risk

The broadest type of risk, which is unavoidable, is the so-called market risk. This is a risk that you can’t get rid of if you want to invest in a certain type of asset. If you, for example, invest in a passive equity fund that owns all stocks in the market, you still bear the risk of the equity market.

Risks driven by politicians and central bankers

As you narrow down the universe to specific regions or countries or specific assets, the risk drivers may differ. For example, when you invest in stocks or bonds in a specific country, you expose yourself to political risk and currency risk related to that country. Political decisions can lead to a change in legislation that affects you and your investments, and it can also affect the exchange rate. Lower-yielding assets such as bonds are more sensitive to changes in the exchange rate; a currency that depreciates significantly against your home currency can wipe put your whole profit.

Another risk that is driven by politicians and central bankers and affects you is inflation risk. Inflation reduces your purchasing power, and a minimum goal for your investments is to keep up with inflation to not lose purchasing power over time. Historically, hard assets and precious metals such as gold have been used to protect yourself from inflation. However, stocks should be fine to protect against inflation as well, as businesses can adjust their prices in line with inflation. Lastly, nowadays, some bonds are protected against inflation, e.g., Treasury Inflation-Protected Securities (TIPS).

The other party may fail to deliver on their promise

When investing, you normally bear counterparty risk, e.g., that the other party fails to deliver on their promise. When investing in debt, credit, or default risk is a risk that the borrower will fail on the promise to pay you interest and return your principal.

Illiquidity can eat your returns as well

With most investments, you may expose yourself to liquidity risk, i.e., that it is hard or takes a long time to buy or sell an asset. Some stocks have very low trading volume; hence, it can be hard to buy or sell a sufficient number of shares within a reasonable time. Other investments, such as bonds, might have reduced liquidity due to high par values; hence, there are fewer investors that have a sufficient amount of money to participate in the market.

This latter type of issue can be dealt with through mutual funds and ETFs. Though, mutual funds may only allow investments and redemptions once a month or less and an ETF can, like a stock, have low trading volume; hence, you may still expose yourself to liquidity risk. Liquidity is an issue as it usually leads to higher spreads, and you may also move the price by your own trading as you buy or sell a large part of the daily turnover in the instrument.

Diversify across and within asset classes to reduce overall portfolio risk

The last risk, we’d like to highlight in this post is concentration risk, which means that you hold one or very few assets in your portfolio. First, you might want to allocate money to different asset classes, so your portfolio includes stocks, bonds, gold, and commodities. Many investors also like to add real estate to the portfolio; however, for the average investor that owns the property they live in the allocation to real estate is already likely sufficient or too high.

Then within each asset class, there’s concentration risk, e.g., only investing in a specific stock or sector within the stock market. Throughout the years, many studies have shown that it’s not uncommon for investors to only hold one or a few stocks in their brokerage accounts. Those investors bear a significant amount of company-specific risk, e.g., exposed to poor decisions made by management in that specific company or changes in the market environment that only impacts that specific company or companies of that type.

How to measure investment risk

Volatility measured as the standard deviation of returns is the most common risk measure in finance. There are numerous financial theories and hypotheses based on the assumption that risk is volatility. However, in real life, volatility is hardly a risk in itself. Think about it yourself, if the price of the asset you own increases, is that a risk?

Another way to measure risk is then to only look at downside volatility. In this case, you exclude the volatility on the upside, since that is something you want, and only measure the standard deviation on the downside. Losing less on the downside matters over the long run, as if you manage to reduce your losses, you have a larger principal on which you earn returns.

The final risk measure we’d like to mention is the maximum drawdown risk. Maximum drawdown is the fall in price from peak to trough. You may also want to look at not only the magnitude of the drawdown but also the length of it, or how long time it took until the previous peak was recovered. Maximum drawdown is interesting to look at over long periods and also to see how well a portfolio fared through a large market downturn.

Risk management in our All Weather Strategy

Our All Weather Strategy aims to capture as much of the long-term equity return as possible while at the same time capture less of the downside compared to an all-equity portfolio. We, therefore, invest in four different asset classes: stocks, bonds, gold, and commodities. So that we, for example, can reduce our equity exposure at times when stocks appear to be overvalued and increase our bond exposure to reduce volatility. Or increase our gold exposure in times of high inflation expectations or when trust in the financial system falls.

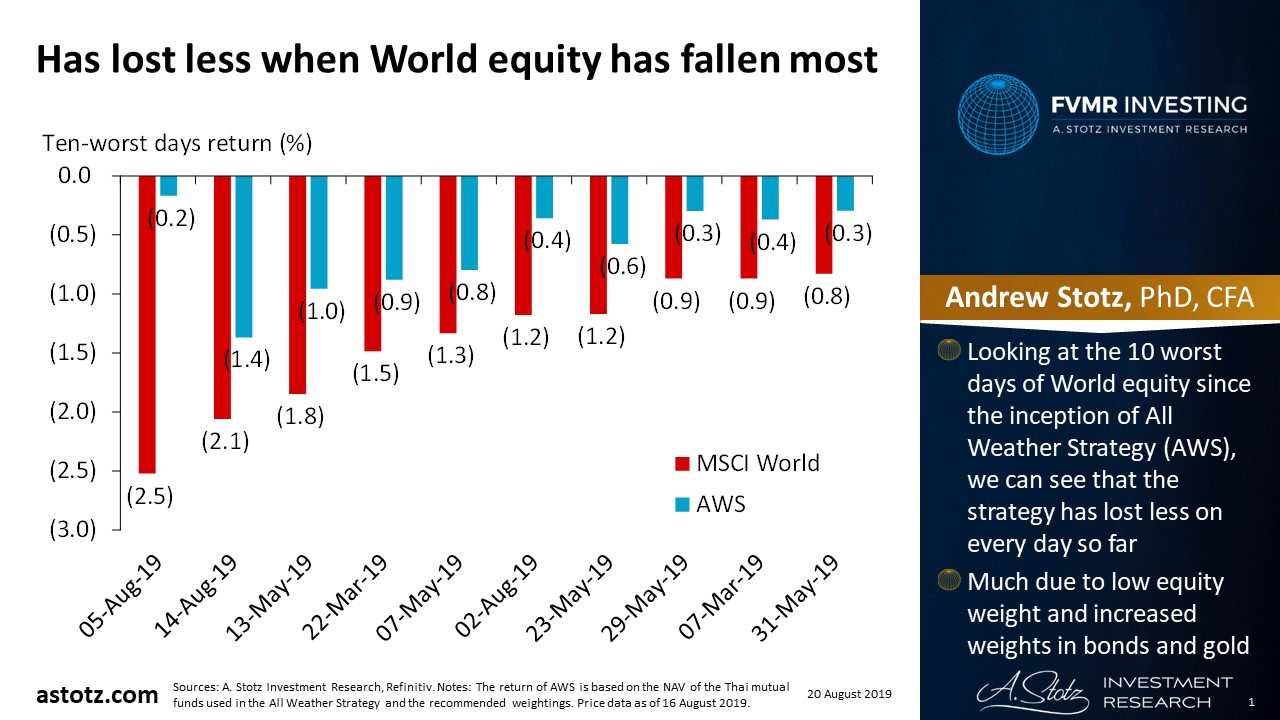

Looking at the 10 worst days for World equity, since inception of the All Weather Strategy, we can see that our strategy has lost less on all of these 10 days. This is partly due to reduced equity exposure, but also due to downside protection in terms of a relatively high bond allocation and also a high allocation to gold.

Do not avoid risk completely, manage it

To conclude, when digging deeper into risk and becoming aware of the many risks you expose yourself to when investing, keep in mind that one can also be too conservative. If you put your savings in the piggy bank instead of investing it, you may not have enough in the future. Instead of completely avoiding risk, make sure to manage it carefully.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.