A. Stotz All Weather Strategy – August 2021

The All Weather Strategy outperformed the traditional 60/40 portfolio in the past three months. Central banks let recovering Western economies run hot. Commodities to benefit from Western and Chinese recovery. We keep our target allocations unchanged.

The A. Stotz All Weather Strategy is Global, Long-term, and Diversified:

- Global – Invests globally, not only Thailand

- Long-term – Gains from long-term equity return, while trying to reduce a portion of losses during equity market downturns

- Diversified – Diversified globally across four asset classes

The All Weather Strategy is available in Thailand through FINNOMENA. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

Review

US has driven global equity

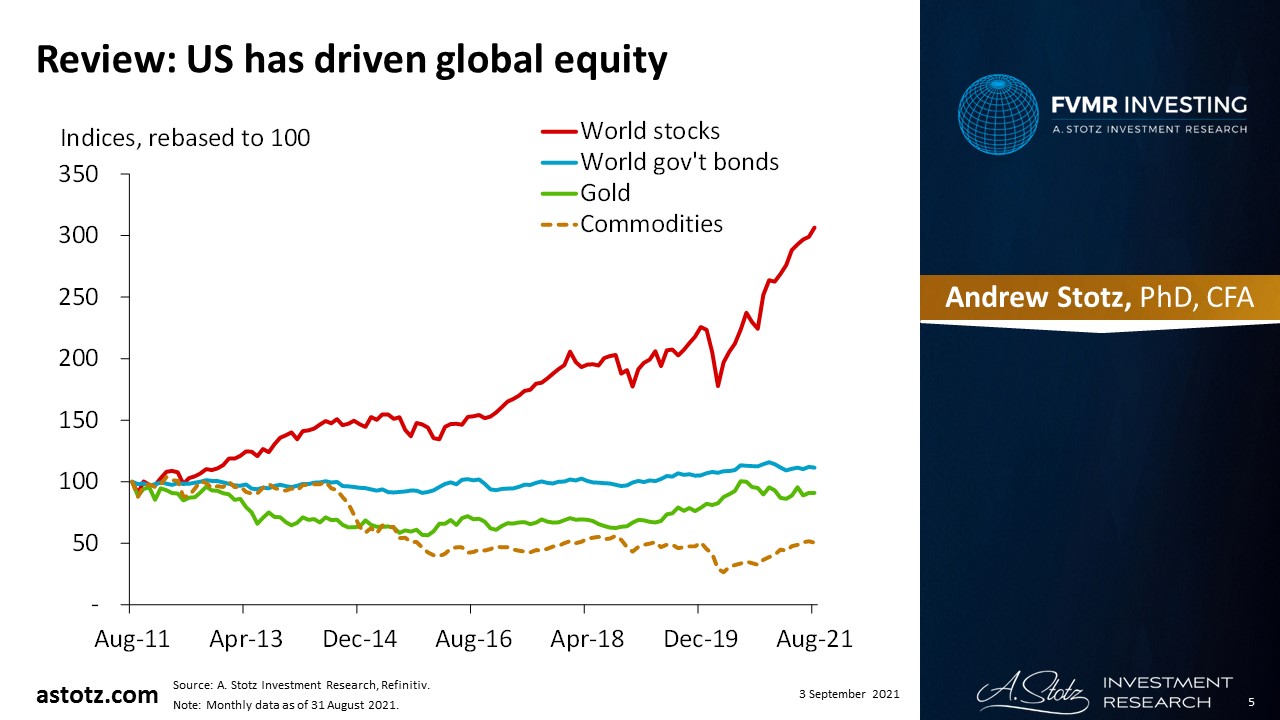

US equity was the best performer

- In our June revision, we switched our 25% equity allocations to the US and Developed Europe from Emerging markets and Asia Pacific ex Japan

- US equity was the best performer among all assets in the past three months

- A continued economic recovery has been confirmed by economic data, such as job numbers, inflation, and wage growth

Developed Europe was the second-best performing asset in the past three months

- Economic data shows recovery in the Eurozone as well

- Unemployment falls rapidly as countries open, and inflation reached a 10-year high in August

Right call to switch out of Asia Pacific ex Japan and Emerging markets

- Asia Pacific ex Japan and Emerging markets were the worst-performing equity

- Government-mandated shutdowns and mobility restrictions have led to weak economic activity in Asia and Emerging markets

- The Chinese government’s policy changes worsened sentiment towards Chinese stocks, which weighed on Emerging markets

Low bond target allocation at 5%

- We have a bond target allocation of 5% as they appeared less attractive relative to equity

- We’ve held only Thai government bonds, rather than a mix of global government and corporate bonds

- Bond return was flat as expected

Commodities were the third-best performer in the past three months

Gold has performed poorly year to date

- We have only a 5% allocation to gold

- Fed Chair Powell didn’t reveal anything new with regards to tapering in his speech at Jackson Hole, hence, no reason for gold to move on this event

- Gold closed August flat at US$1,813/oz t

Past 3 months: We allocated 25% to the three top performers

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

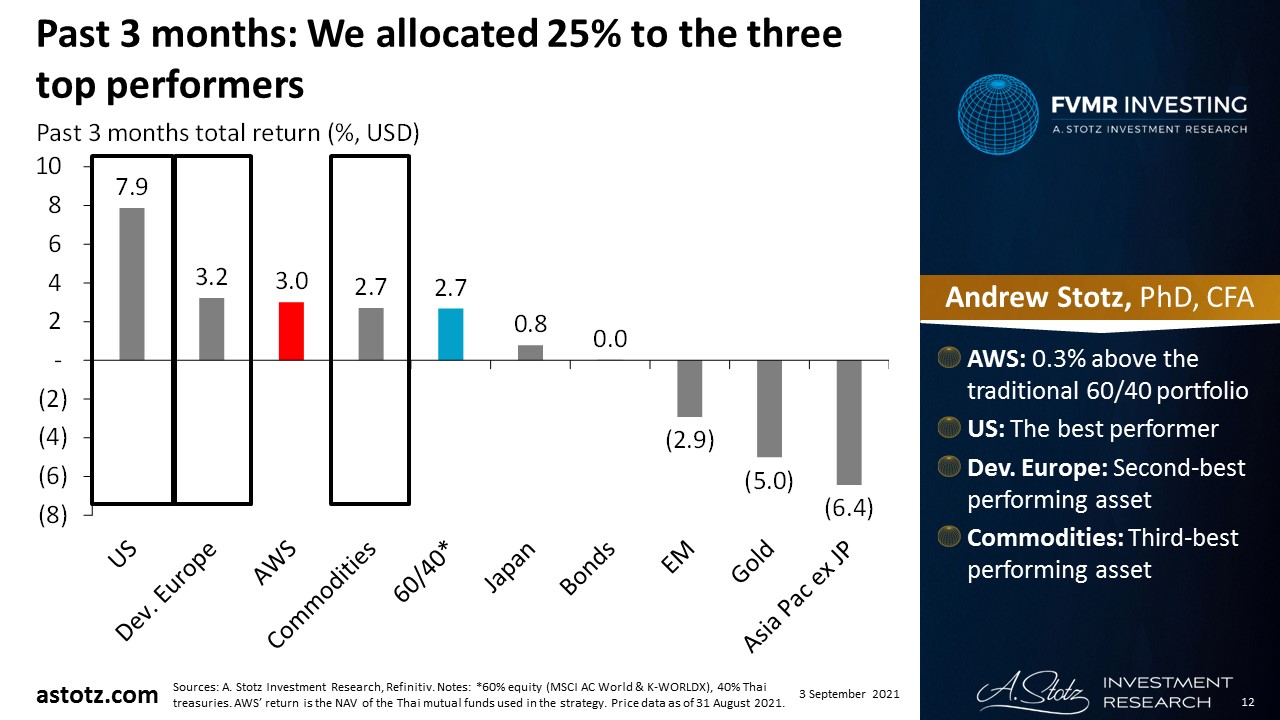

- AWS: 0.3% above the traditional 60/40 portfolio

- US: The best performer

- Dev. Europe: Second-best performing asset

- Commodities: Third-best performing asset

Since inception: Slightly below a traditional 60/40 portfolio but with lower drawdowns

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

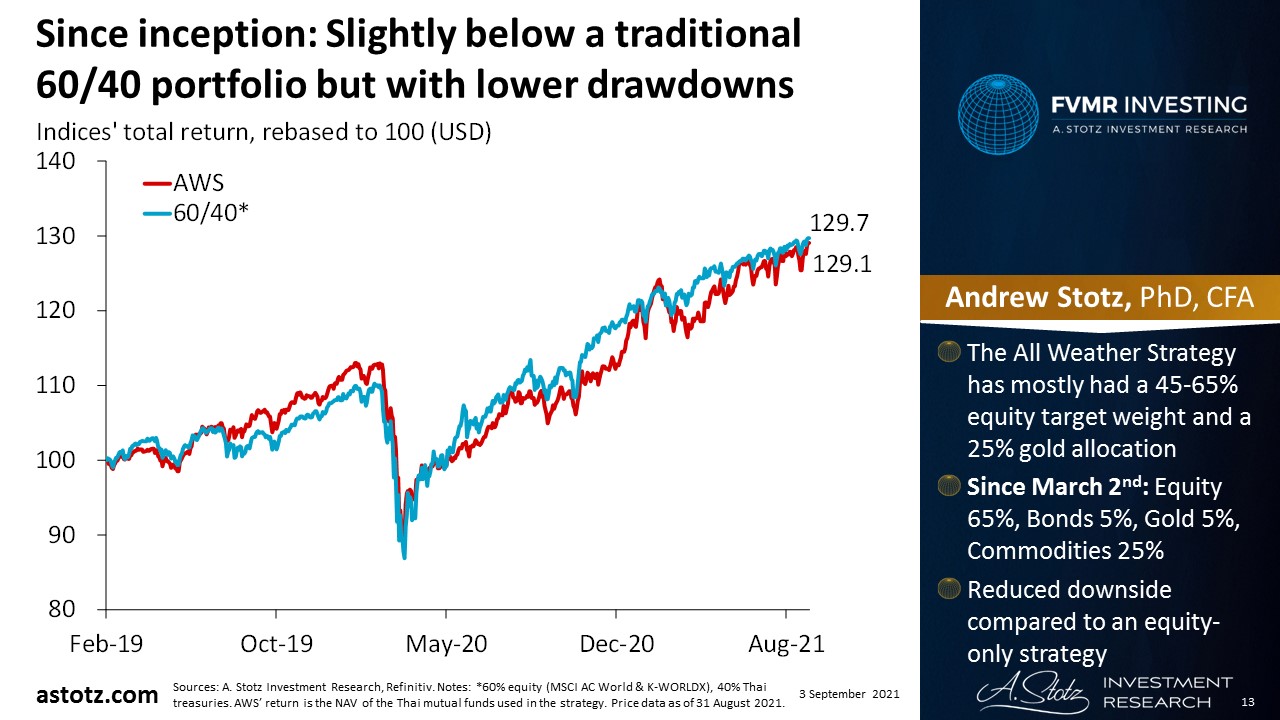

- The All Weather Strategy has mostly had a 45-65% equity target weight and a 25% gold allocation

- Since March 2nd: Equity 65%, Bonds 5%, Gold 5%, Commodities 25%

- Reduced downside compared to an equity-only strategy

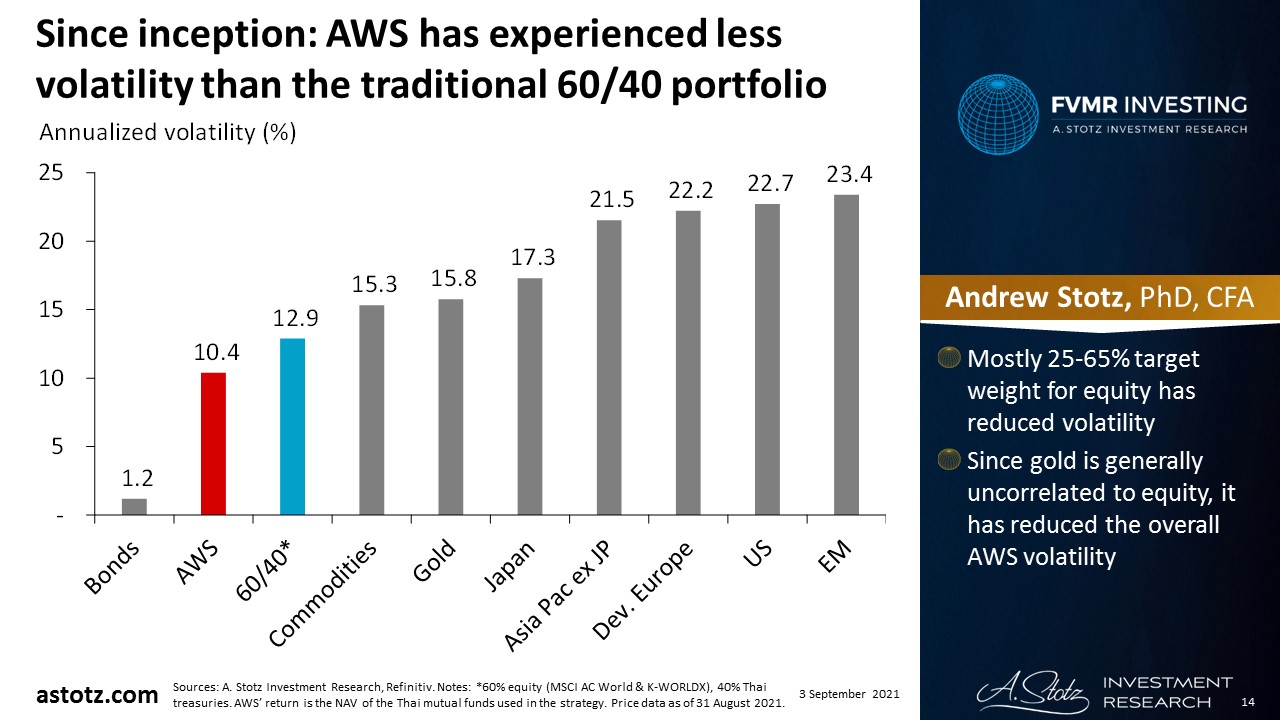

Since inception: AWS has experienced less volatility than the traditional 60/40 portfolio

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- Mostly 25-65% target weight for equity has reduced volatility

- Since gold is generally uncorrelated to equity, it has reduced the overall strategy’s volatility

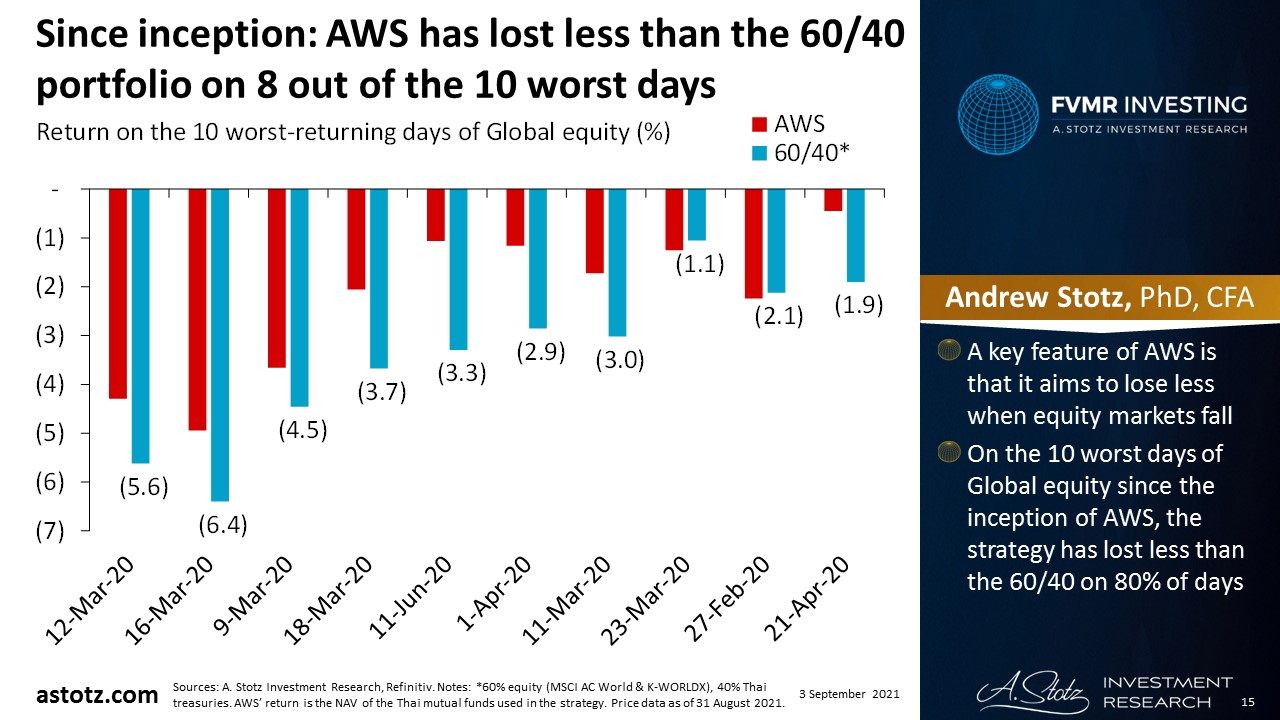

Since inception: The All Weather Strategy has lost less than the 60/40 portfolio on 8 out of the 10 worst days of world equity

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- A key feature of the All Weather Strategy is that it aims to lose less when equity markets fall

- On the 10 worst days of Global equity since the inception of the All Weather Strategy, the strategy has lost less than the 60/40 portfolio on 80% of days

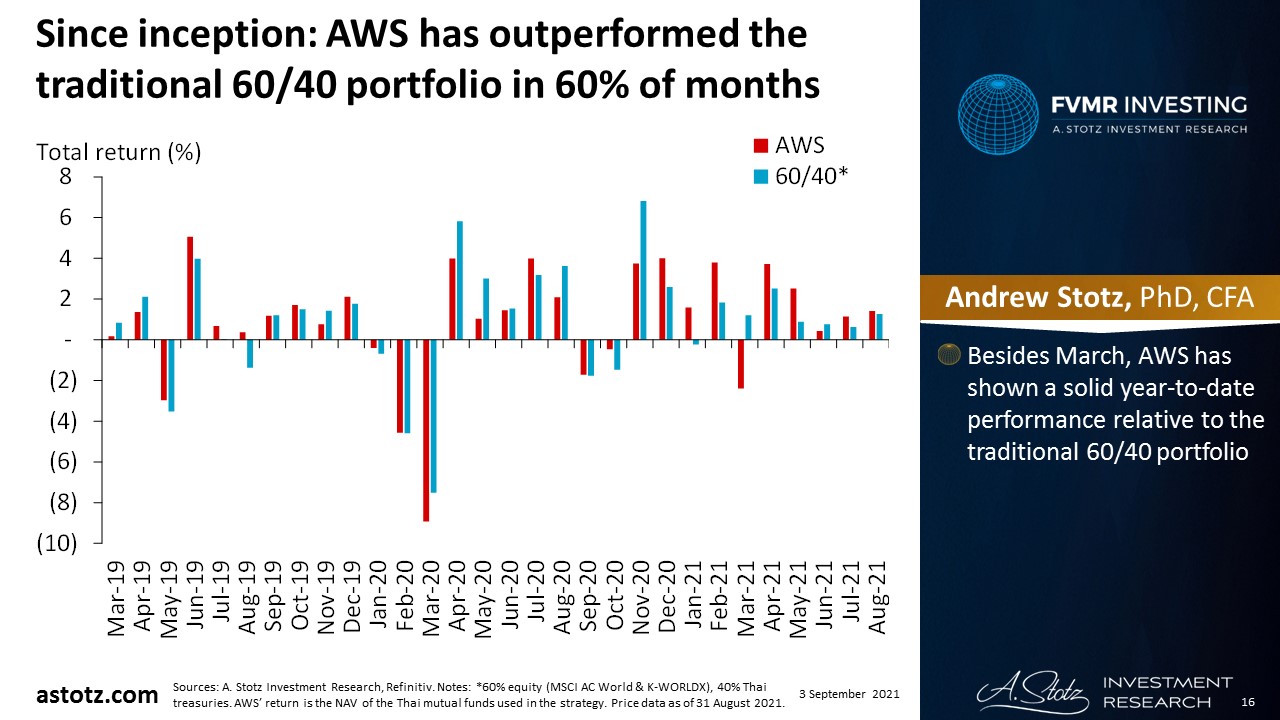

Since inception: The All Weather Strategy has outperformed the traditional 60/40 portfolio in 60% of the months

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

Besides March, AWS has shown a solid year-to-date performance relative to the traditional 60/40 portfolio

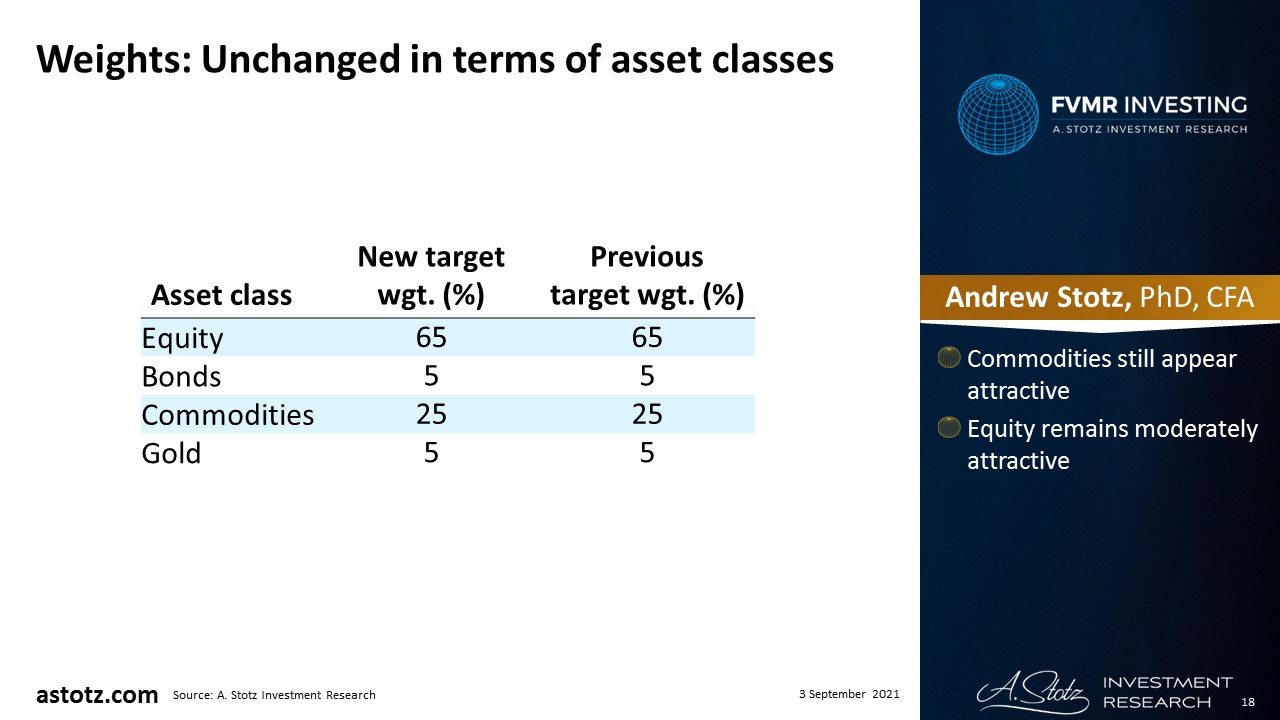

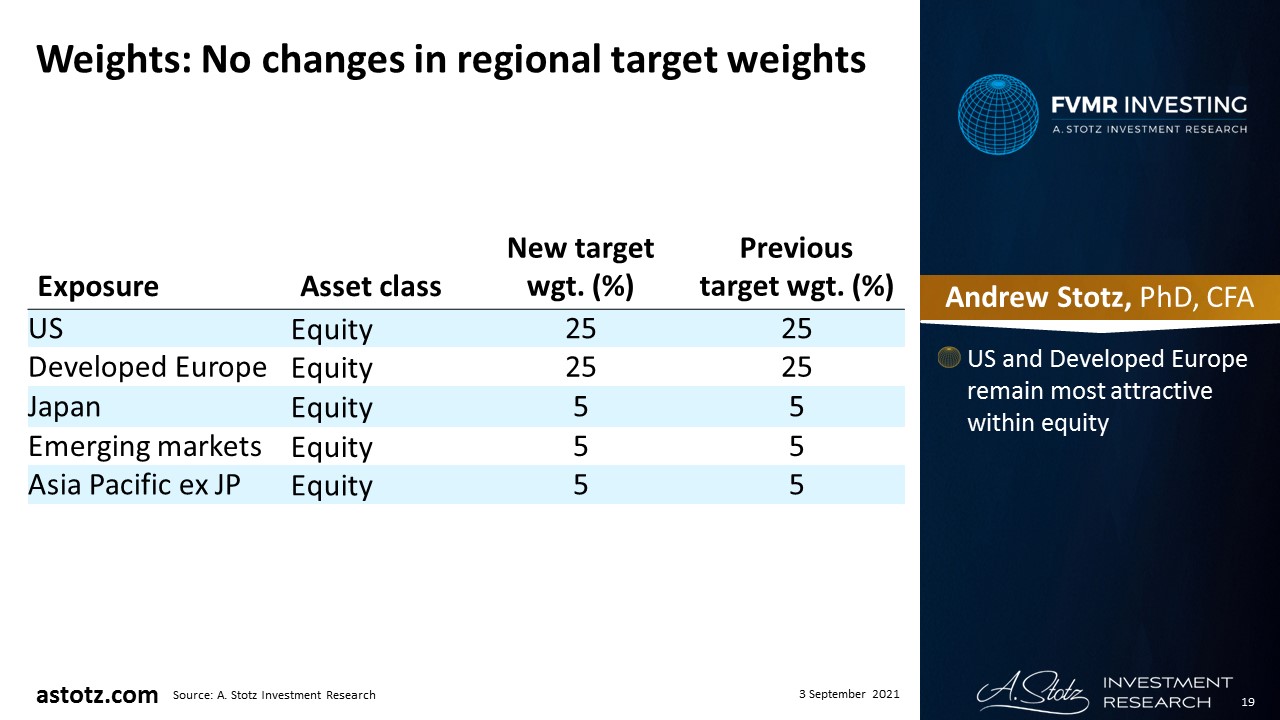

Weights: No change in target allocations

- Keep equity at 65% and commodities at 25%

- Keep bonds and gold at 5% each

- We keep US and Developed Europe at 25%

Unchanged in terms of asset classes

- Commodities still appear attractive

- Equity remains moderately attractive

No changes in regional target weights

- US and Developed Europe remain most attractive within equity

Outlook

Ride the US momentum

- The US continues to post strong economic data, and Fed Chair Powell hasn’t signaled any change in his tapering plans

- This should be positive for US equity; we keep a 25% target allocation

- Though the US equity market is highly valued, we’ll ride the momentum

US inflation won’t be transitory

- American businesses find it hard to fill job openings due to high unemployment compensations from government stimulus

- Which has caused wage inflation

- Inflation continues, and unlike money-printing Powell, we don’t think it will be transitory

- We see this as a risk to the US market in the longer term

European recovery story remains intact

- Similar to the Fed, ECB also pushed eventual tapering decisions to the future

- Liquidity to support European markets

- Unlike the US, the Eurozone has yet to see growth in wages

- UK has lifted the final COVID-restrictions, and the Eurozone has high vaccination rates

New virus variants don’t appear to stop the re-opening of Western economies

- Amidst the spread of new variants of the coronavirus, due to high vaccination rates, Western countries appear to allow a continued re-opening

“Common prosperity” makes China investors equally poor

- The revival of China’s “common prosperity” could lead to further crackdowns on Chinese businesses, which we think leads to continued negative sentiment towards Chinese stocks

- China’s heavy weight in the Emerging markets and Asia Pacific ex Japan indices is likely to drag down performance

COVID measures constrain Asia

- Expanded COVID lockdowns in Japan and upcoming elections increases uncertainty, which is generally bad for equities

- Other Asian countries maintain COVID restrictions, which is likely to keep the economic recovery muted

Bonds to remain weak

- As we’re expecting rising inflation, we expect bonds to underperform

- This is reflected in our 5% target allocation

Commodities upcycle to continue

- Continued economic recovery in the West and China to support commodities prices

- Taliban takeover in Afghanistan could push up oil prices as it could stir up conflicts between large oil-producing nations in the region

- Poor weather conditions limiting the supply of key agricultural commodities could lead to even higher prices

Unexciting near-term outlook for gold

- In the longer term, as the inflation narrative spreads, it could lead to expectations of negative real rates

- Supportive of the gold price

- Neither Fed nor ECB has changed their communication with regards to tapering, which keeps the market’s inflation expectations unchanged

- No push for gold in either direction

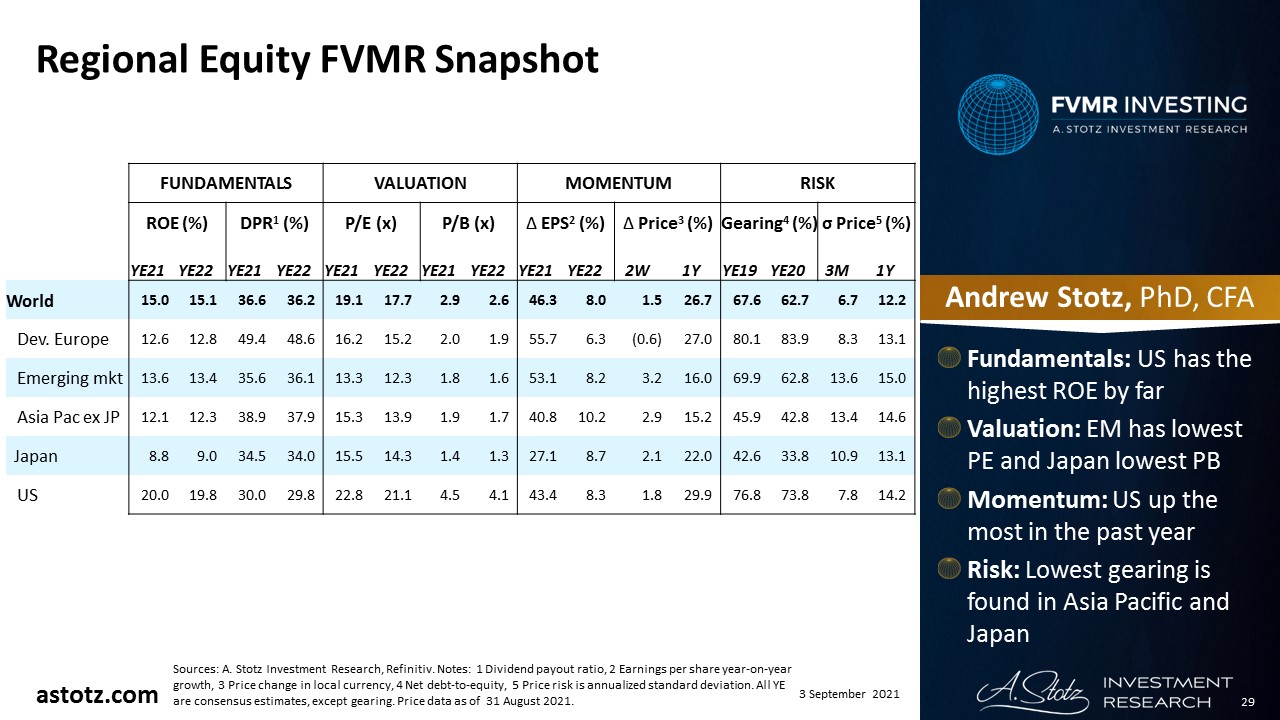

Regional Equity FVMR Snapshot

- Fundamentals: US has the highest ROE by far

- Valuation: Emerging markets have the lowest PE and Japan lowest PB

- Momentum: US is up the most in the past one year

- Risk: Lowest gearing is found in Asia Pacific and Japan

Risks

Inflation turns out transitory

- The All Weather Strategy is positioned to benefit from rising inflation

- There’s a risk that inflation is transitory, which could hurt our performance

- Besides, return expectations in inflationary environments are based upon corresponding rising interest rates

- But the Fed and ECB are expected to keep rates low at least until late 2022

New variants of the coronavirus lead to new lockdowns

- If governments in countries with high vaccination rates return to lockdowns to battle new mutations of the virus, it would be negative for those equity markets

China sentiment turns and vaccination rates ramp up in Emerging markets

- If the market was to have no longer to worry about a Chinese government crackdown, we could see a turn in Chinese stocks

- Faster vaccine rollouts or other measures that lead to re-opening expectations of Emerging economies could boost Emerging markets and Asian stocks

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.