A. Stotz All Weather Strategies – March 2023

The All Weather Strategy is available in Thailand through FINNOMENA. If you’re interested in our allocation strategy, you can also join the Become a Better Investor Community. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

What happened in world markets in March 2023

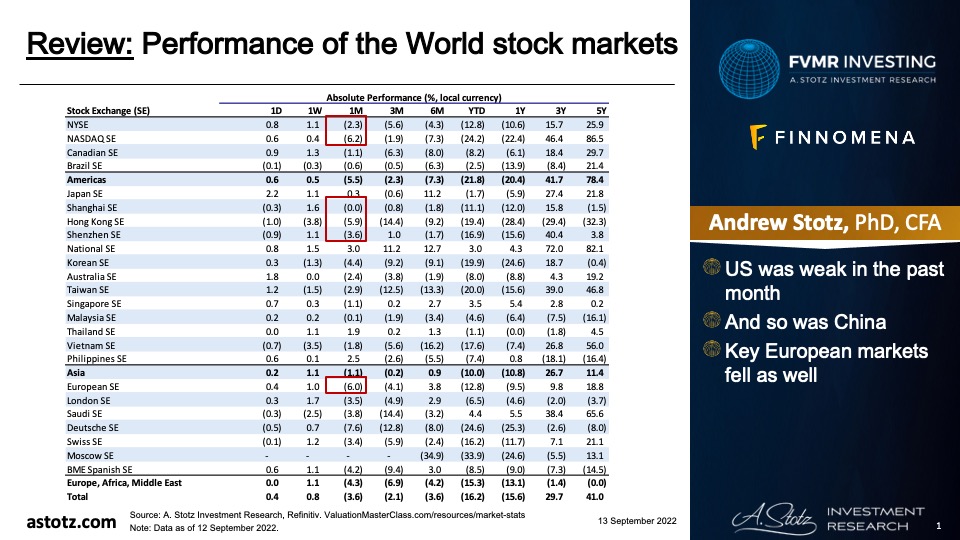

Performance of the World stock markets

- Tech-heavy NASDAQ rebounded strongly

- Hong Kong was up, while mainland China was slightly down

- Europe was up modestly

Find the updated Performance of the World stock markets here.

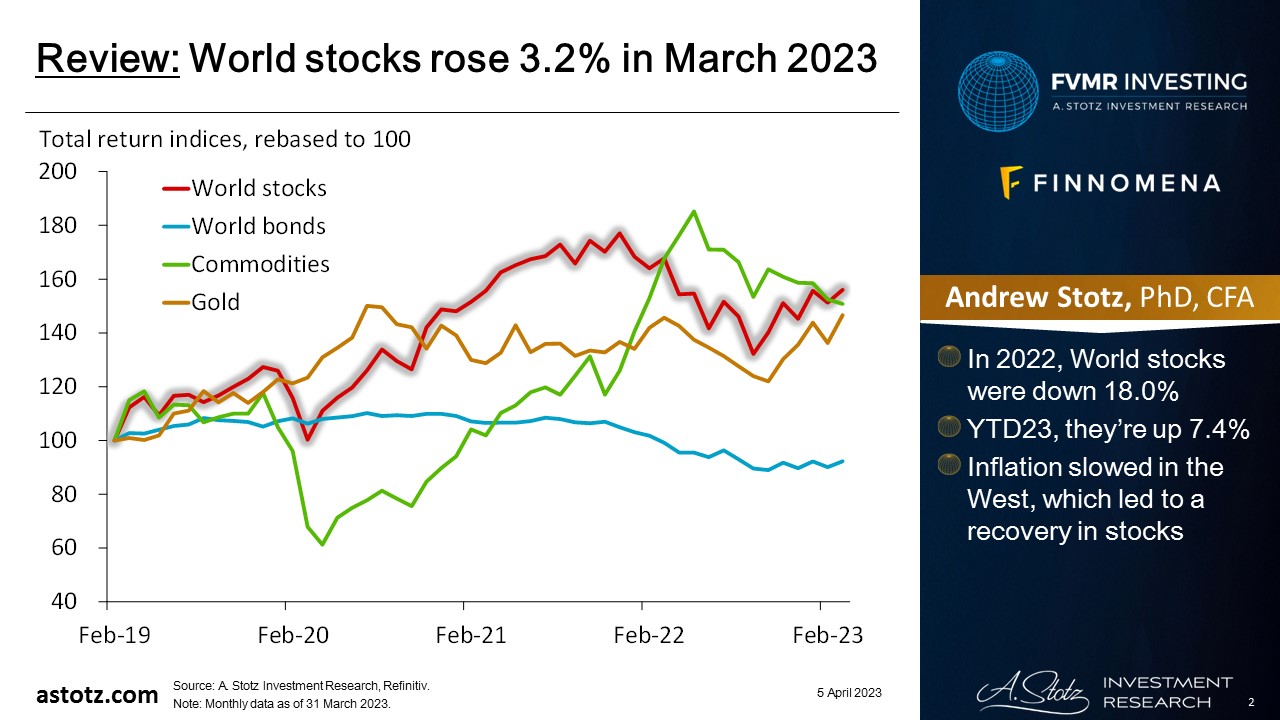

World stocks rose 3.2% in March 2023

- In 2022, World stocks were down 18.0%

- YTD23, they’re up 7.4%

- Inflation slowed in the West, which led to a recovery in stocks

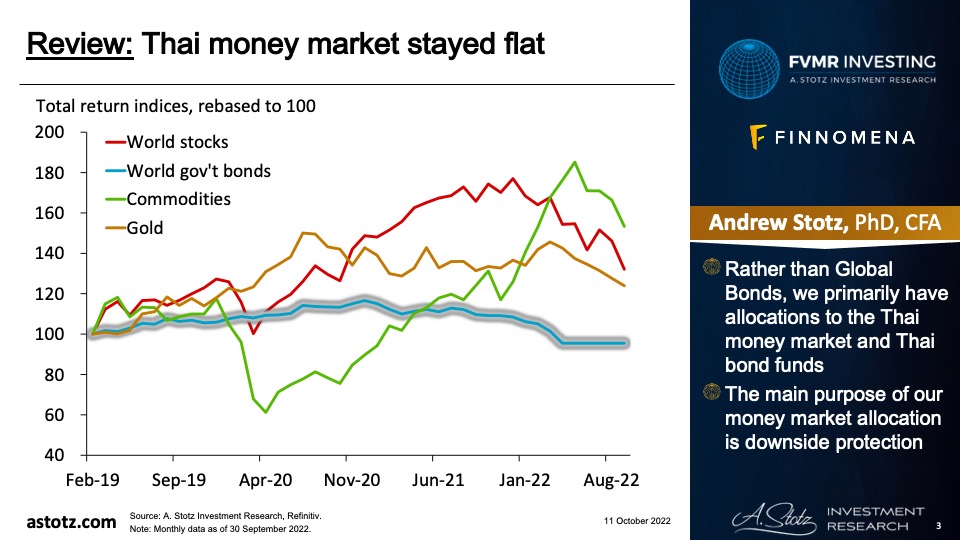

Global bonds were up in March

- Rather than global bonds, we had a target allocation to the Thai money market, which was flat as expected

- The main purpose of our money market allocation is downside protection

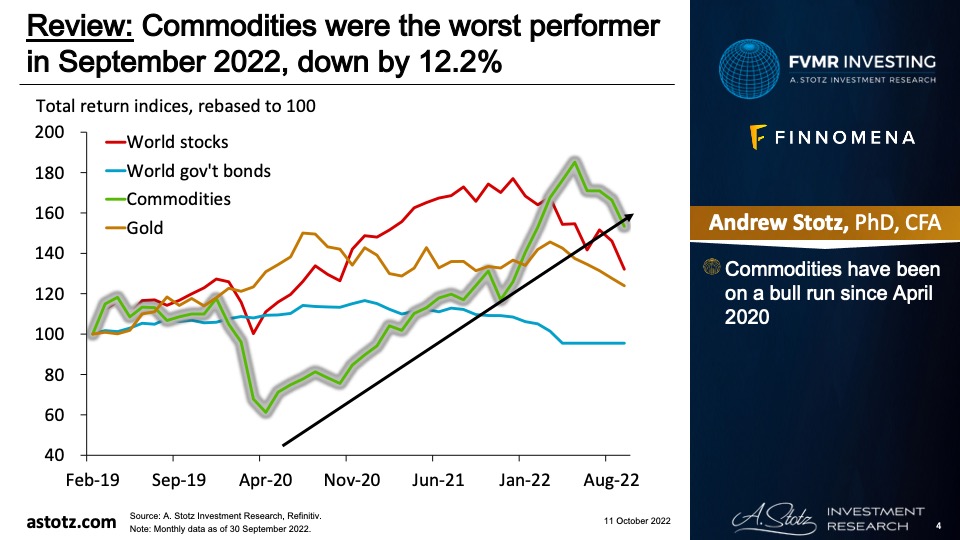

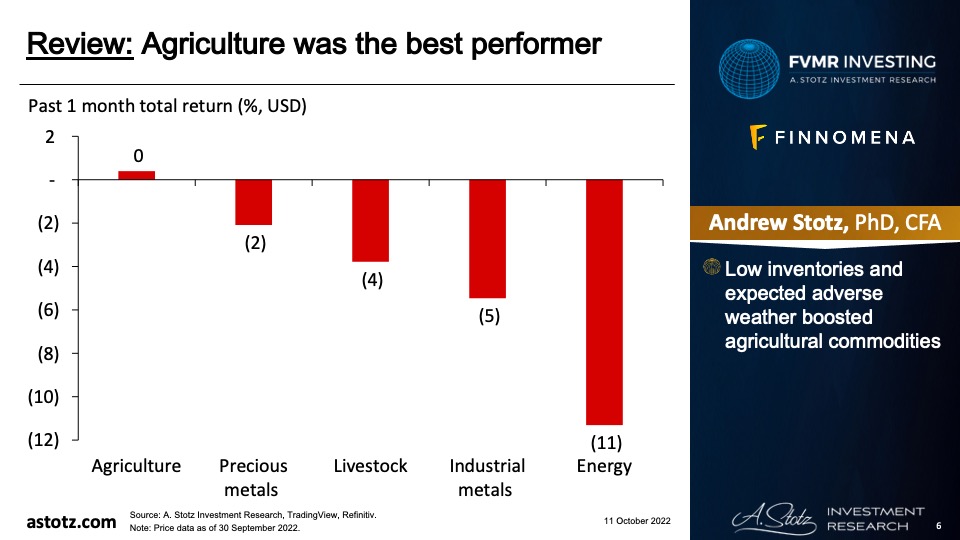

Commodities underperformed in March 2023, still up by 0.3%

WTI oil closed March 2023 at US$76/bbl

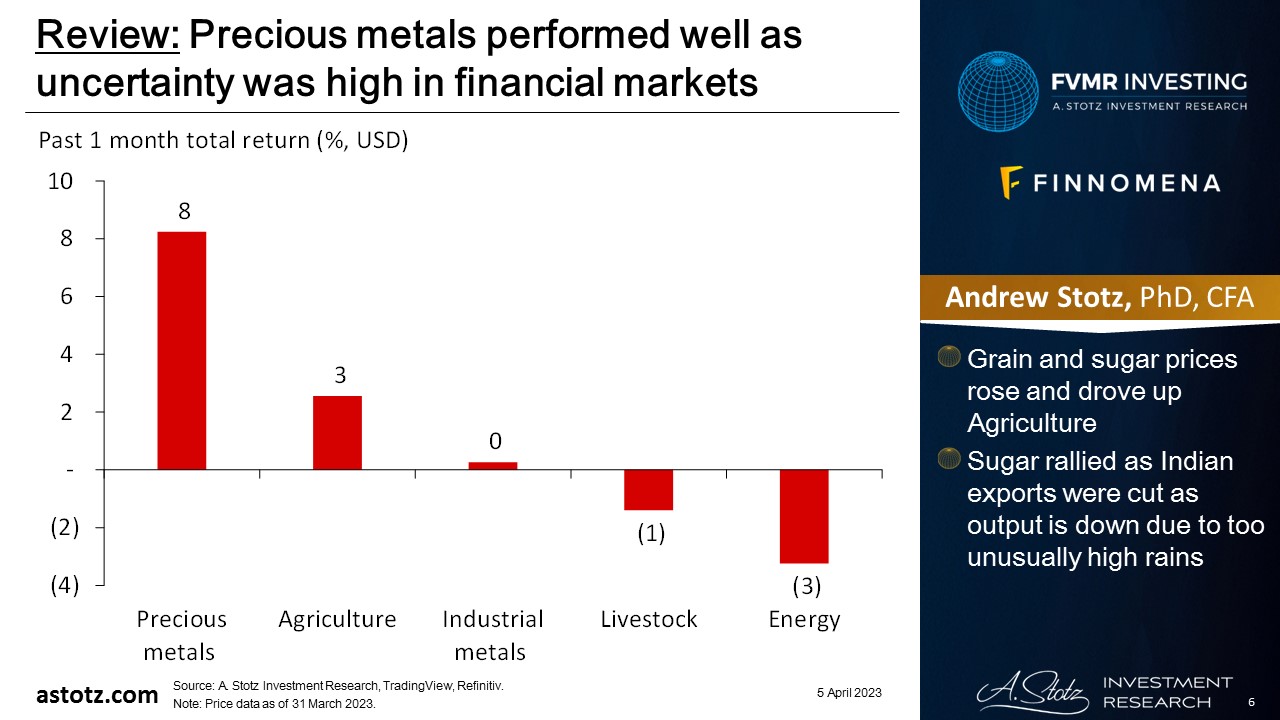

Precious metals performed well as uncertainty was high in financial markets

- Grain and sugar prices rose and drove up Agriculture

- Sugar rallied as Indian exports were cut as output is down due to too unusually high rains

Gold was the best performer in March 2023, up by 7.9%

- Gold closed the month at US$1,969/oz

- Heightened uncertainty in the market led investors to safe havens like gold

All currencies weakened by 4%+ against gold in March 2023

- Typically, a stronger US$ means a lower gold price in US$ and vice versa

US bonds have had a massive drawdown

The US Bond Market now has been in a drawdown for 31 months, by far the longest drawdown in history. pic.twitter.com/eulI5Qfy6u

— Charlie Bilello (@charliebilello) March 2, 2023

Silicon Valley Bank failed, and the regulator seems to have too

SVB demonstrates we don’t need more bank regulation, just regulators actually doing there job and not focusing on things like climate risk. Here’s simple chart showing failure of regulators. Where was FDIC, where was Cal bank regulators? Allowing this mismatch to occur? pic.twitter.com/pcGfYSdPB1

— Larry Swedroe (@larryswedroe) March 13, 2023

The Fed’s balance sheet grew again to save the banks

The US Federal Reserve Bank (Fed) just printed $300 billion out of thin air last week to bail out the banks. What a joke and a voodoo economics.

This is not free market or even capitalism.

If developing nations want $300 billion, they have to sell their sovereignty to the IMF… pic.twitter.com/G6efRJsI7O

— S.L. Kanthan (@Kanthan2030) March 16, 2023

The Swiss gov’t had to quickly broker a deal for UBS to take over Credit Suisse

It just doesn’t seem fair that the Swiss didn’t have adequate time to prepare for a crisis at Credit Suisse. Things happen so fast these days… pic.twitter.com/8fNC4y9JHp

— Michael Green (@profplum99) March 15, 2023

- Note, Michael Green is sarcastic in his tweet

- The chart shows the stock’s steady decline since 2010

Fed hiked 0.25% and said there is more to come

Posturing towards further HIKES if no mayhem happens

“The Committee anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.”

— Alf (@MacroAlf) March 22, 2023

ECB hiked 0.5%

50bp from the ECB, but it could well be the final hike, if we listen to their communication

“The elevated level of uncertainty reinforces the importance of a data-dependent approach to the Governing Council’s policy rate decision”

— AndreasStenoLarsen (@AndreasSteno) March 16, 2023

US house prices hit by rate hikes

The median price of an existing home sold in the US is down on a YoY basis for the first time since 2012. pic.twitter.com/8HwtNBxd0b

— Charlie Bilello (@charliebilello) March 21, 2023

New buddies, Xi and Putin, met and concluded big changes are to come

“Right now there are changes, the likes of which we haven’t seen for 100 years, and we are the ones driving these changes together.”

“I agree.”

“Please take care, dear friend.”

Our current foreign policy drove China and Russia together. Brilliant move.pic.twitter.com/EDcuOj9wne

— Stephen Geiger (@Stephen_Geiger) March 22, 2023

China challenges the petrodollar system

China’s first yuan-settled liquefied natural gas (LNG) trade was completed on Tuesday through the Shanghai Petroleum and Natural Gas Exchange, with about 65,000 tonnes of LNG imported from the UAE changing hands in the trade. (file pic) pic.twitter.com/7J9KYipvmB

— People’s Daily, China (@PDChina) March 29, 2023

Key takeaways

- Silicon Valley Bank started banking turmoil

- Fed announced a 0.25% rate hike, and ECB hiked 0.5%

- US housing market got hit further

- China and Russia tighten their relationship to challenge the US

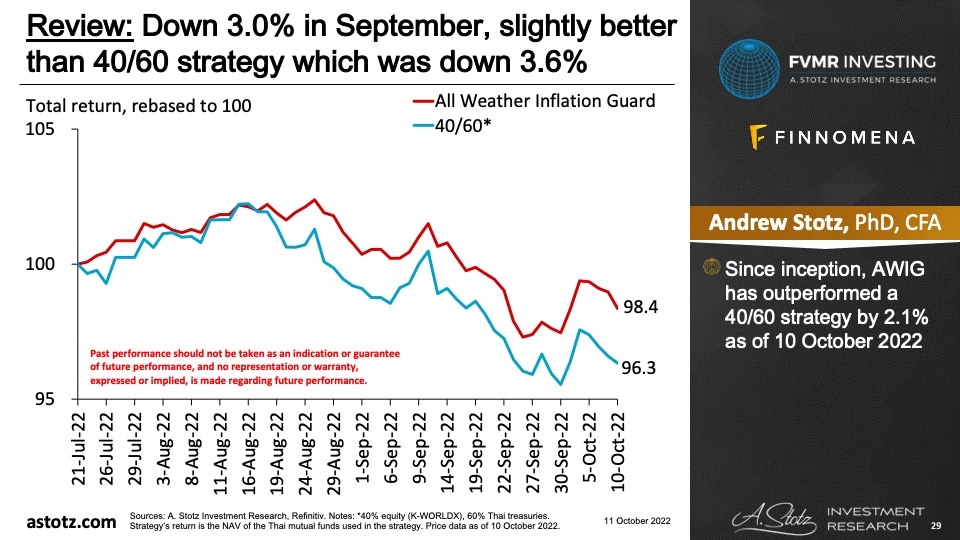

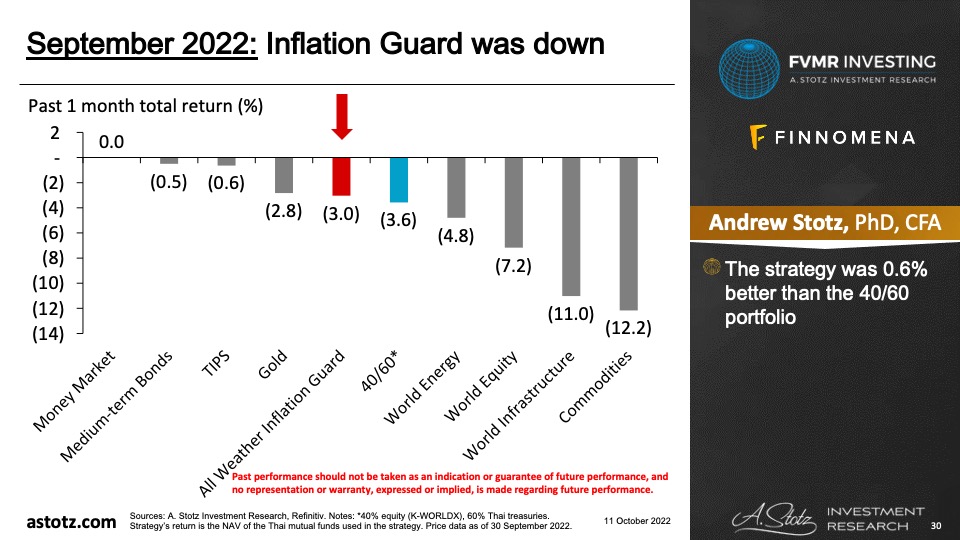

Performance review: All Weather Inflation Guard

All Weather Inflation Guard was up 0.1%

- The strategy has experienced less volatility though

The strategy was 1.0% below the 40/60 portfolio

- Except for TIPS, bonds held up well

- Our 10% gold allocation did well, while our 5% in World energy took a hit

- The world equity fund underperformed the MSCI AC World index

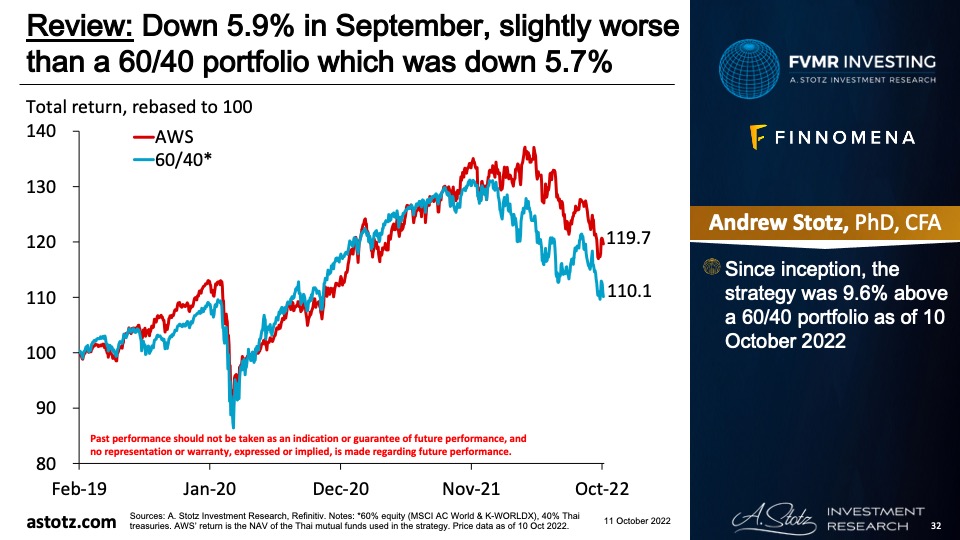

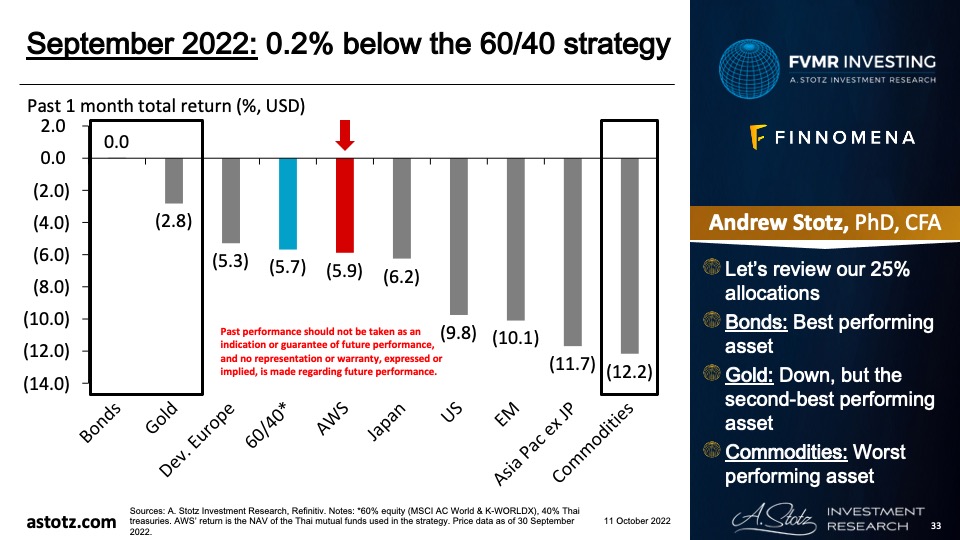

Performance review: All Weather Strategy

All Weather Strategy was up 2.2%

The strategy was 0.5% above the 60/40 portfolio

- Our 25% allocation to gold drove outperformance

- We had 25% in Dev. Europe and Japan, which were only beaten by the US within equity

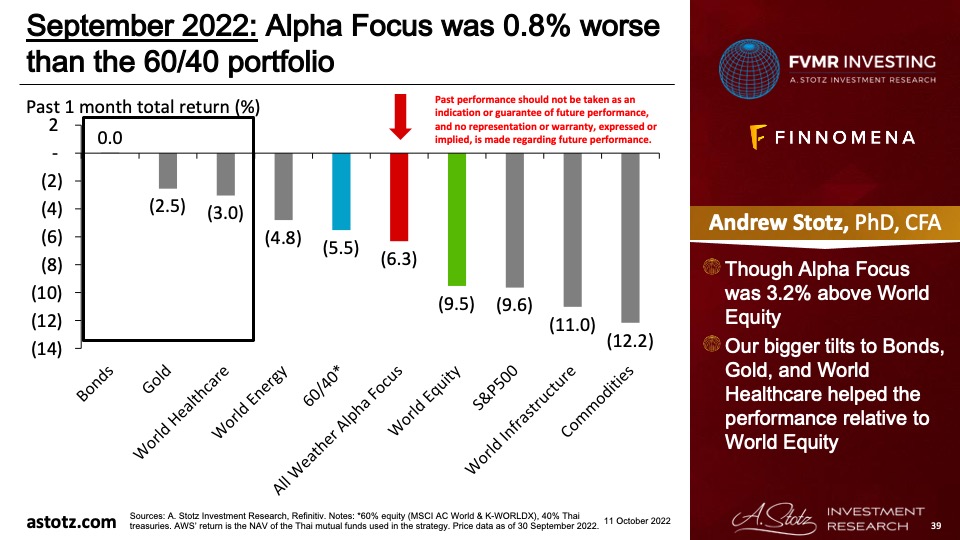

Performance review: All Weather Alpha Focus

All Weather Alpha Focus was up 0.8%

Since inception, the strategy was 4.2% above World equity as of 31 March 2023

The strategy was 0.8% below the 60/40 portfolio

- The strategy was 1.9% below World Equity

- Our 15% tilts to Europe Small Caps and World Energy and a relatively high bond allocation (after taking a hit in World Financials) led to underperformance

Global outlook that guides our asset allocation

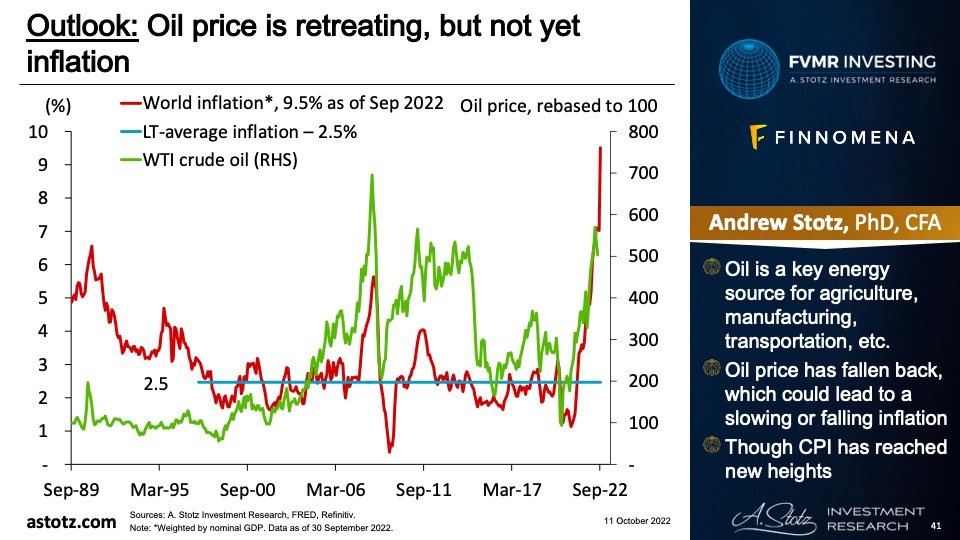

Without a crisis or oil shock, by YE23 US CPI could be down at 3-4%

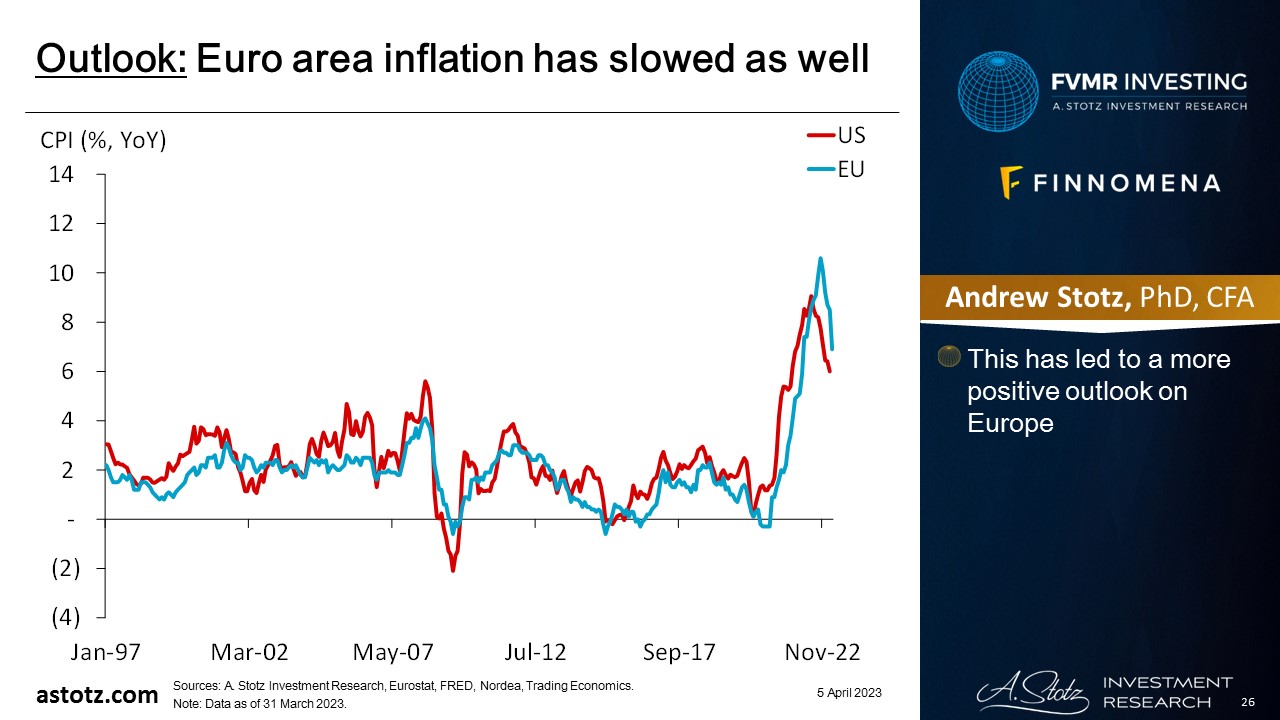

Euro area inflation has slowed as well

- This has led to a more positive outlook on Europe

The battle against inflation isn’t over

- High inflation will likely persist for a while

- In the long run, equity is the best hedge against inflation, as companies have to adapt to survive

A May Fed hike is priced in

- The market is pricing in a 58% probability for another 0.25% rate hike at the next FOMC meeting

The expected rate curve has shifted down significantly since a month ago

- Recent events in the US bank sector have led to a shift in expectations

- The peak is now expected at 5% in June versus 5.5% in July

- The market thinks the Fed will pivot rather than keep the rate high for some time

Fed has kept the peak target rate for 6 months on average since the 1980s

- During the dotcom bust, Fed kept the peak rate for 8 months, and during the GFC, for a record 15 months

- The market expects Fed to keep the peak rate for only 2 months this time

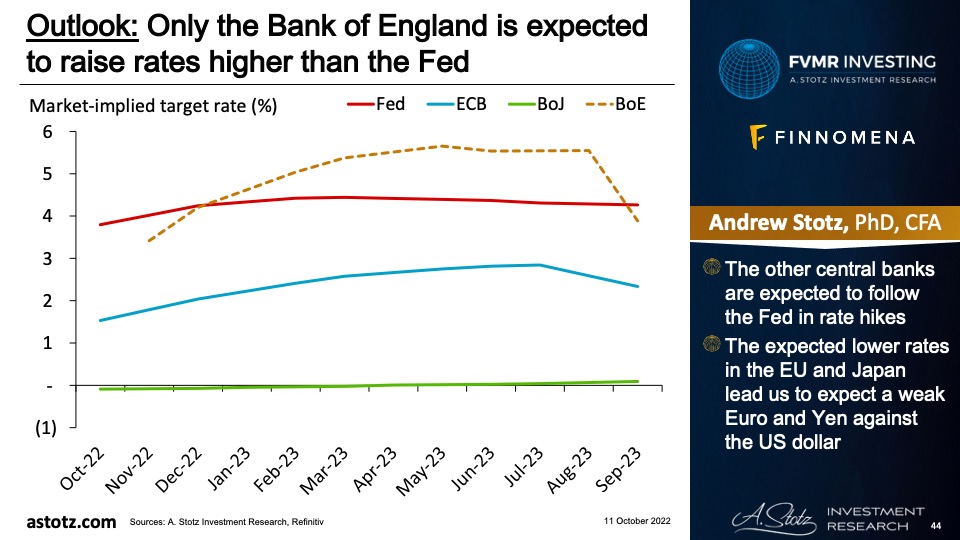

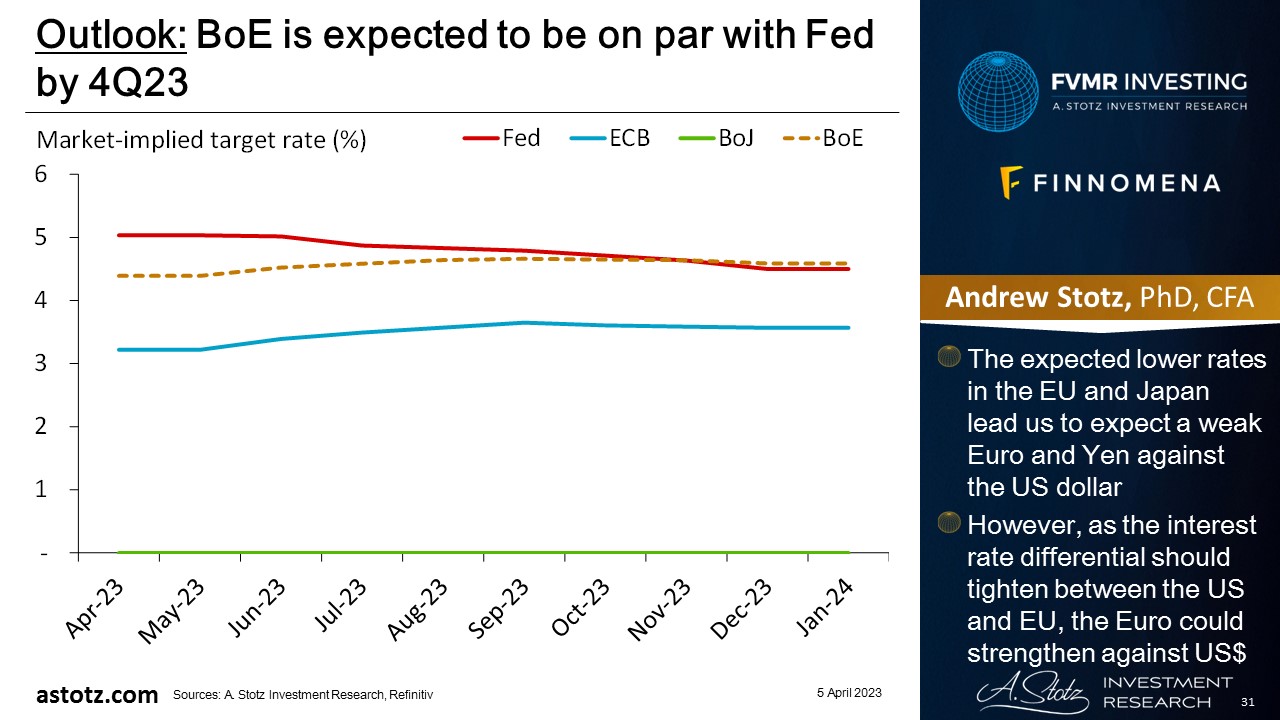

BoE is expected to be on par with Fed by 4Q23

- The expected lower rates in the EU and Japan lead us to expect a weak Euro and Yen against the US dollar

- However, as the interest rate differential should tighten between the US and EU, the Euro could strengthen against US$

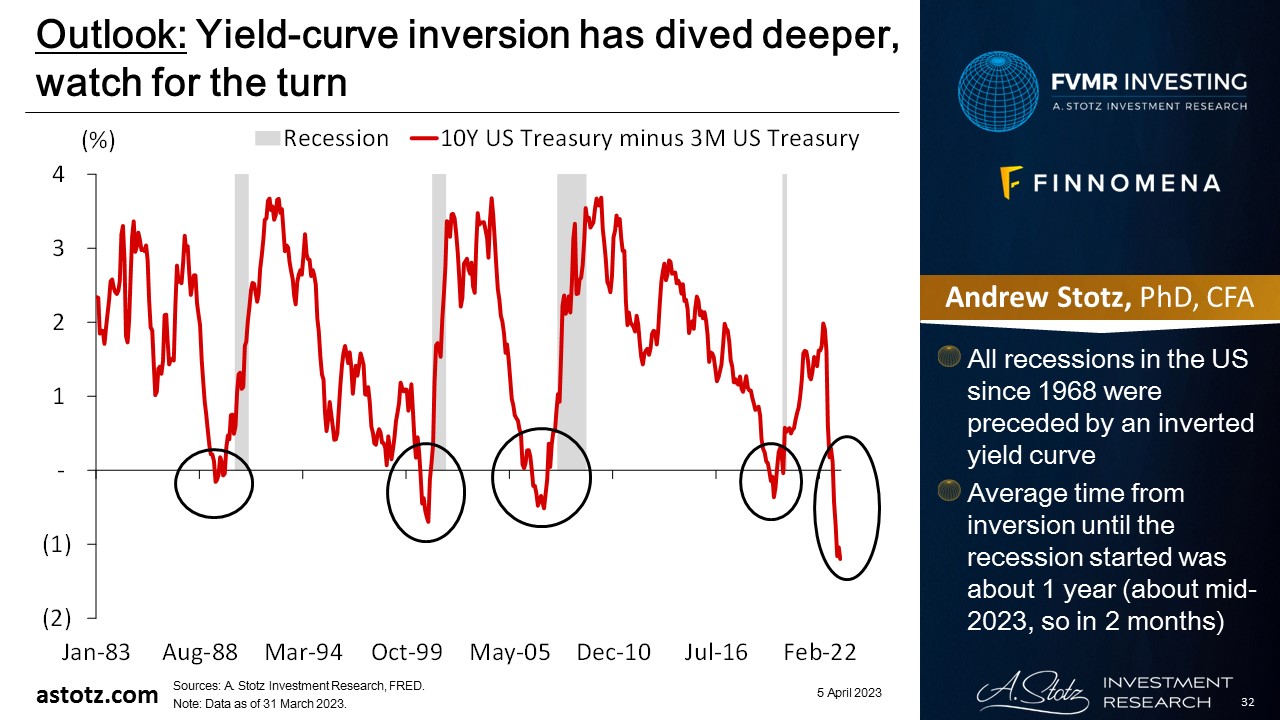

Yield-curve inversion has dived deeper, watch for the turn

- All recessions in the US since 1968 were preceded by an inverted yield curve

- Average time from inversion until the recession started was about 1 year (about mid-2023, so in 2 months)

There hasn’t been much QT in the US

- Mainly, central banks have let bonds mature, which has led to little change in their balance sheets; ECB has dropped recently

- BoJ’s balance sheet began to grow in Oct ‘22, and Fed’s has grown in the recent bank crisis

For the past year, we’ve said that we think the course will eventually be reversed

- We still think central bankers and politicians will change course and return to accommodative policies as soon as something “breaks”

- And we do think central bankers are going to break things

- The recent actions related to US banks support our thesis

Bonds are typically a safe place to be, even though 2022 was exceptionally bad

- In recessions, safer assets like government bonds typically have performed well

- Though with high inflation, low yields could still lead to negative real returns

- We generally don’t allocate to bonds to speculate on the upside but rather use it to protect capital over time

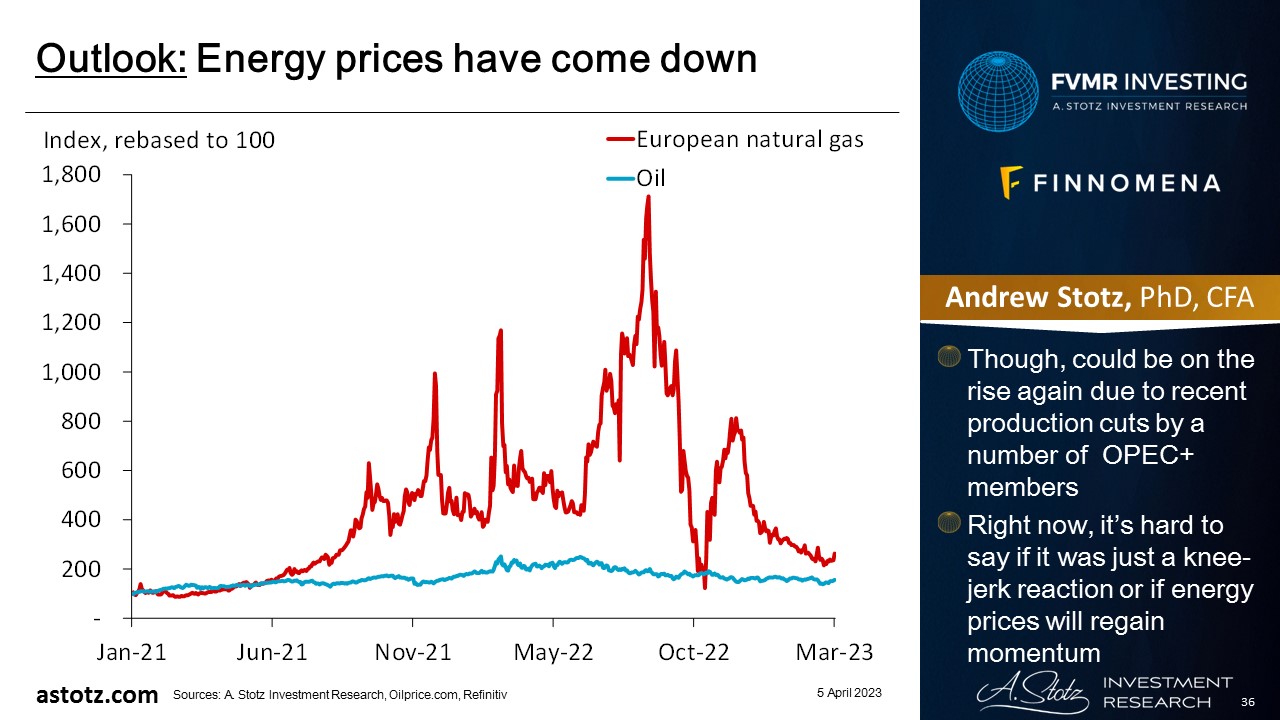

Energy prices have come down

- Though, could be on the rise again due to recent production cuts by a number of OPEC+ members

- Right now, it’s hard to say if it was just a knee-jerk reaction or if energy prices will regain momentum

Food prices have softened

- If the trend continues, it would help to lower the pace of inflation

Commodities have lost momentum as energy prices eased due to a mild winter

- We currently don’t see a clear catalyst for energy prices to go significantly higher, but we think they can remain high, which supports profits for energy companies

- The main upside in commodities would come from a supply shock, adverse weather conditions, or significantly higher demand from, for example, the China reopening

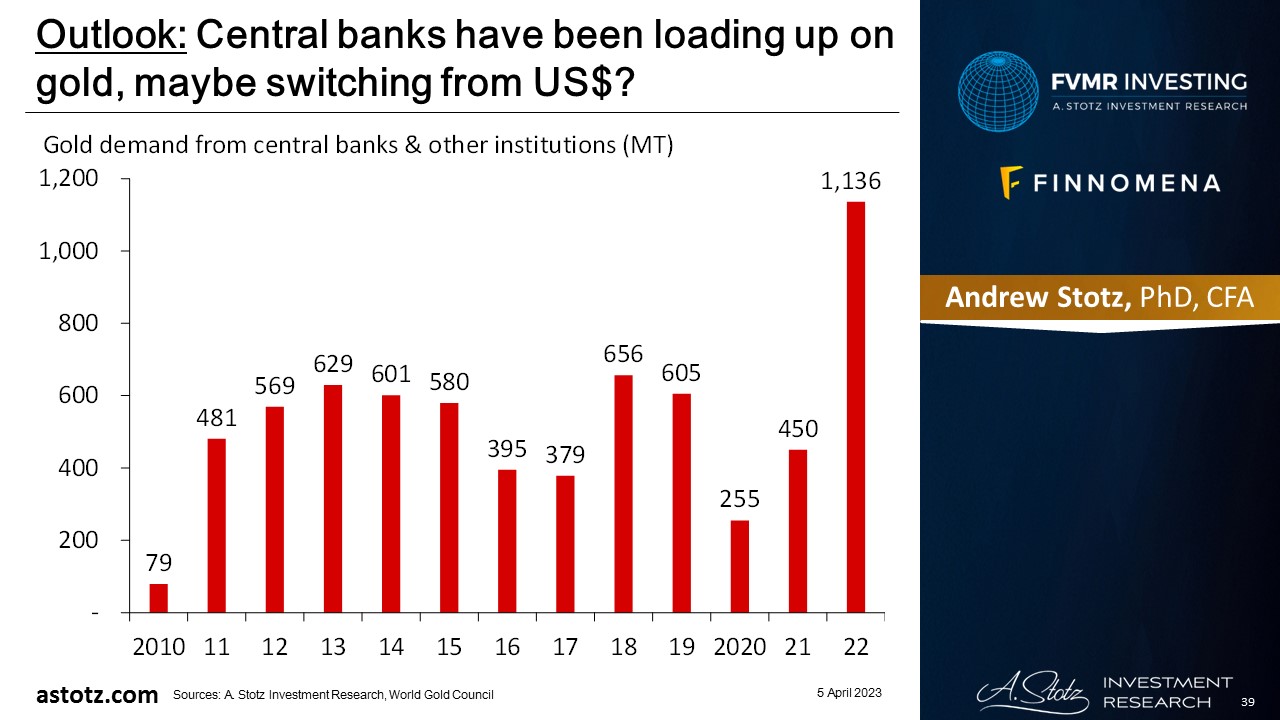

Central banks have been loading up on gold, maybe switching from US$?

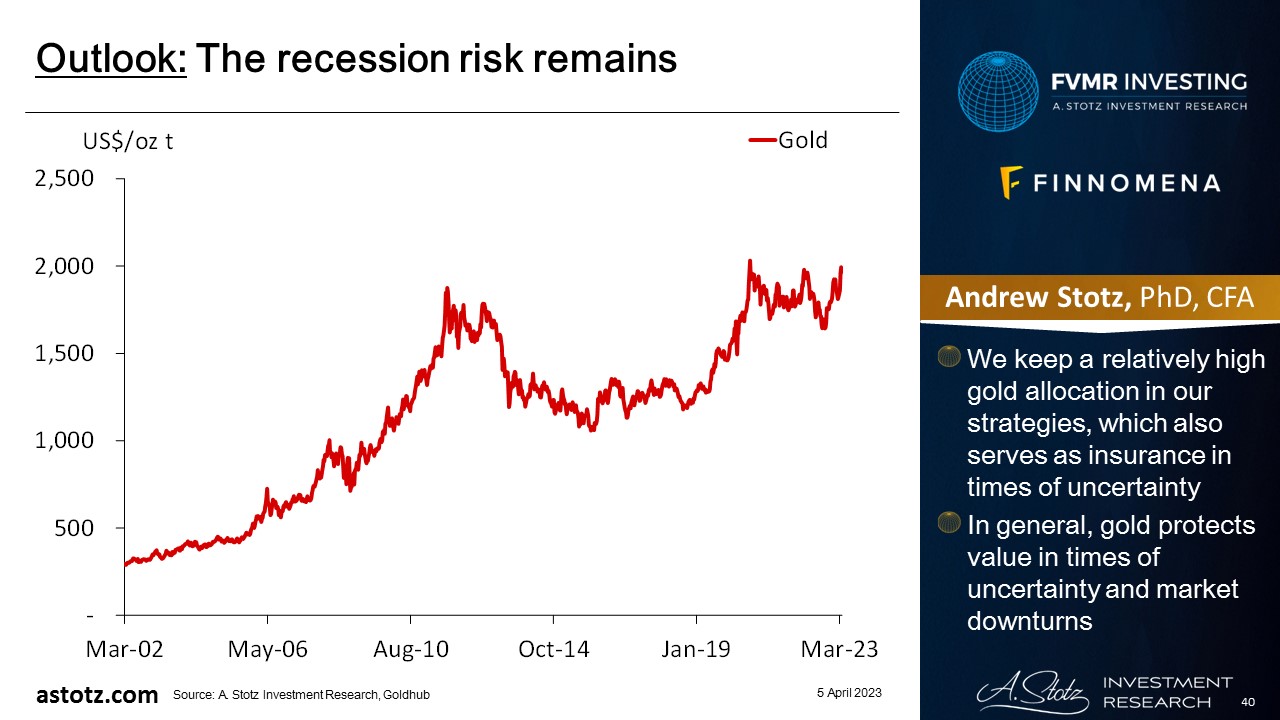

The recession risk remains

- We keep a relatively high gold allocation in our strategies, which also serves as insurance in times of uncertainty

- In general, gold protects value in times of uncertainty and market downturns

Risk: Inflation reaccelerates

- Central banks’ aggressive rate hikes and QT crash the stock markets

- Collapsing energy prices would be damaging to our tilts to World energy

- If inflation reaccelerates, we could miss out on rising commodities prices

- Our high gold allocation could get hit by higher rates or improved market sentiment

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.