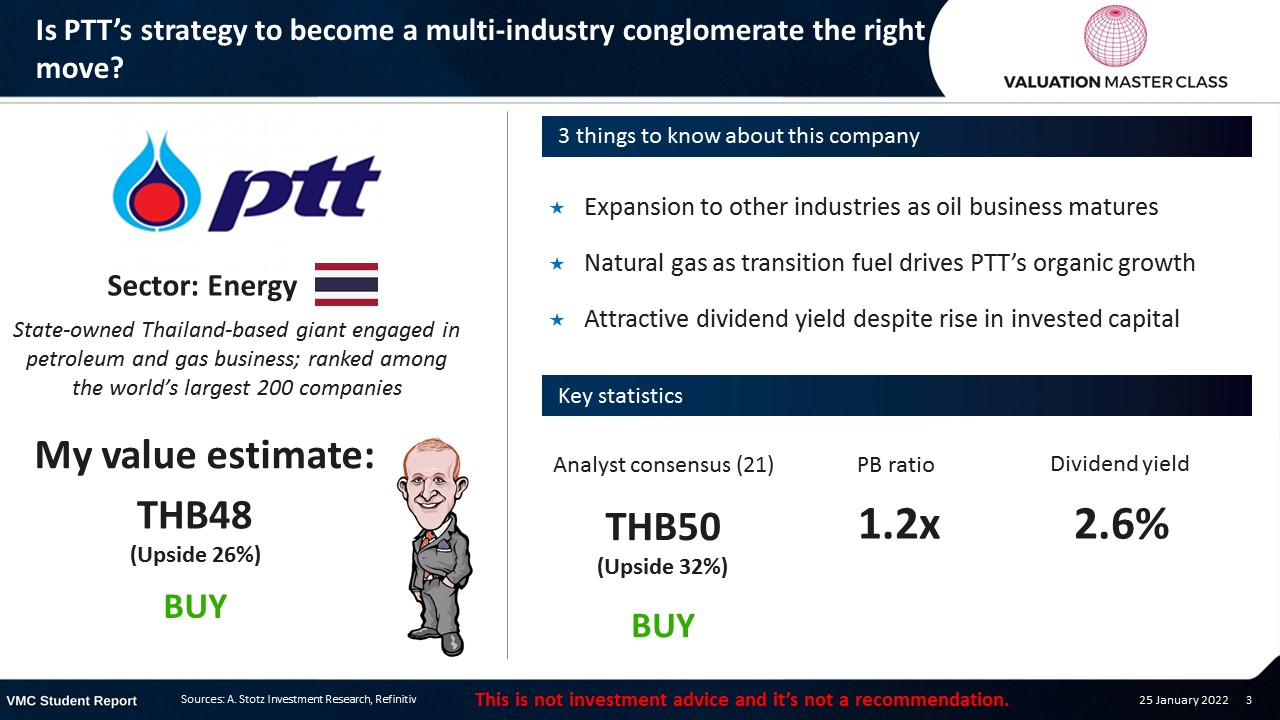

Is PTT’s Strategy to Become a Multi-Industry Conglomerate the Right Move?

The post was originally published here.

Highlights:

- Expansion to other industries as oil business matures

- Natural gas as transition fuel drives PTT’s organic growth

- Attractive dividend yield despite rise in invested capital

Download the full report as a PDF

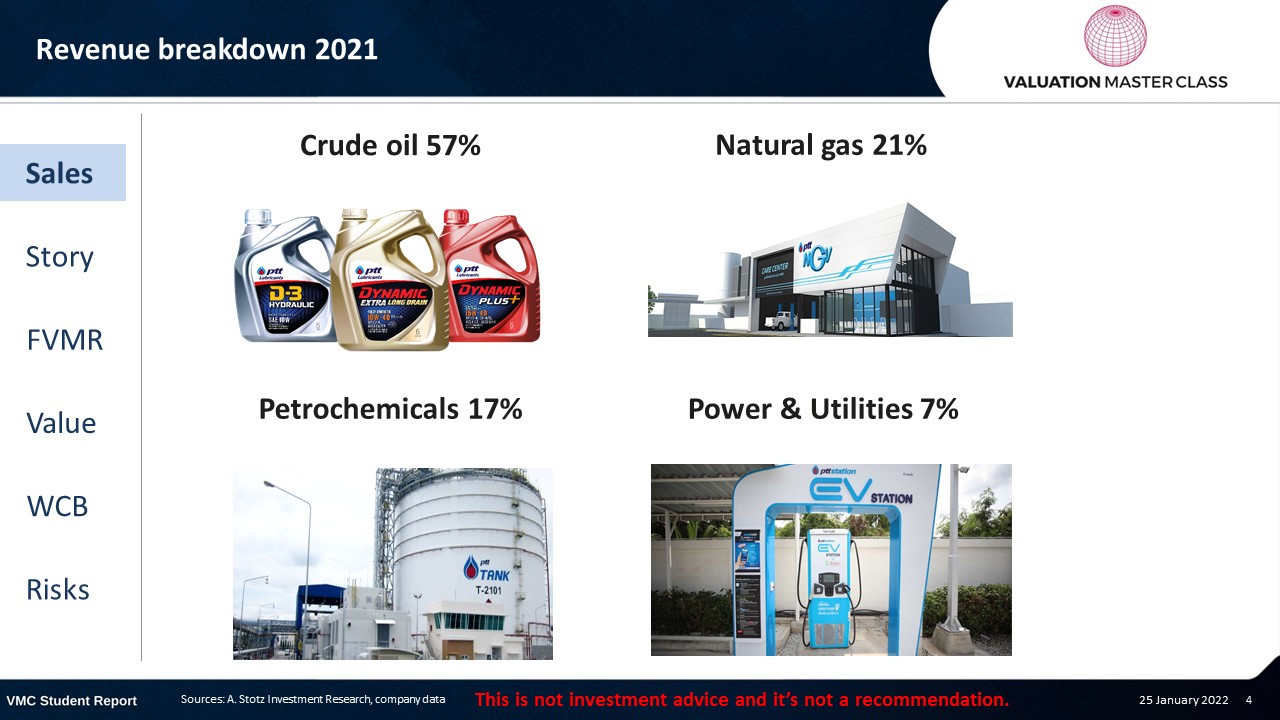

PTT’s revenue breakdown 2021

Volatile price, but volume could help to turnaround

- Over the past year, the stock price has been highly volatile

- Most recently, the 50 DMA stayed below the 200 DMA, which is a bearish signal

- However, both lines moved close together since early this year

- The Volume RSI has stayed slightly above the 50%-line, which is a positive sign

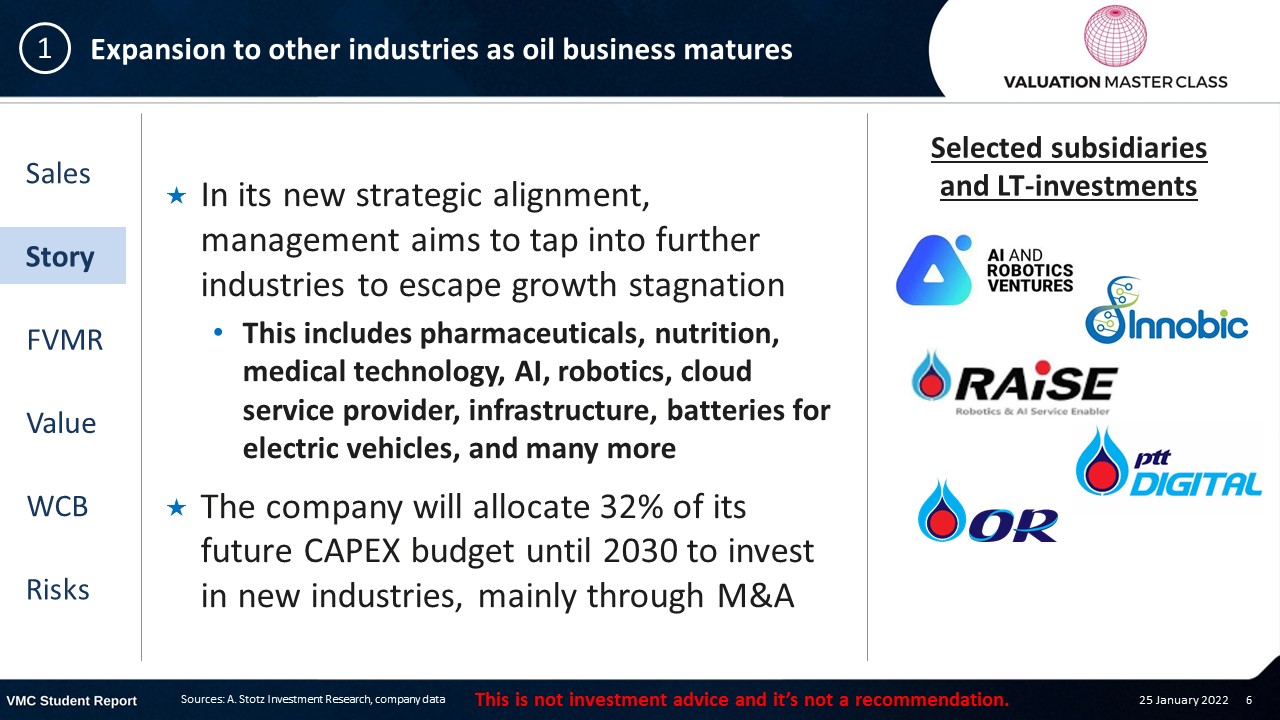

Expansion to other industries as oil business matures

- In its new strategic alignment, management aims to tap into further industries to escape growth stagnation

- This includes pharmaceuticals, nutrition, medical technology, AI, robotics, cloud service provider, infrastructure, batteries for electric vehicles, and many more

- The company will allocate 32% of its future CAPEX budget until 2030 to invest in new industries, mainly through M&A

Diversifying business lines sounds great, but is there any downside?

- The advantage of focusing on one single segment is that a company allocates all resources to maximize the return out of that business

- In case of multiple business lines, investors are exposed to industries in which they might not want to invest

- Investors can diversify themselves by simply adding stocks of other companies to their portfolio

- This is why conglomerates usually trade at a discount

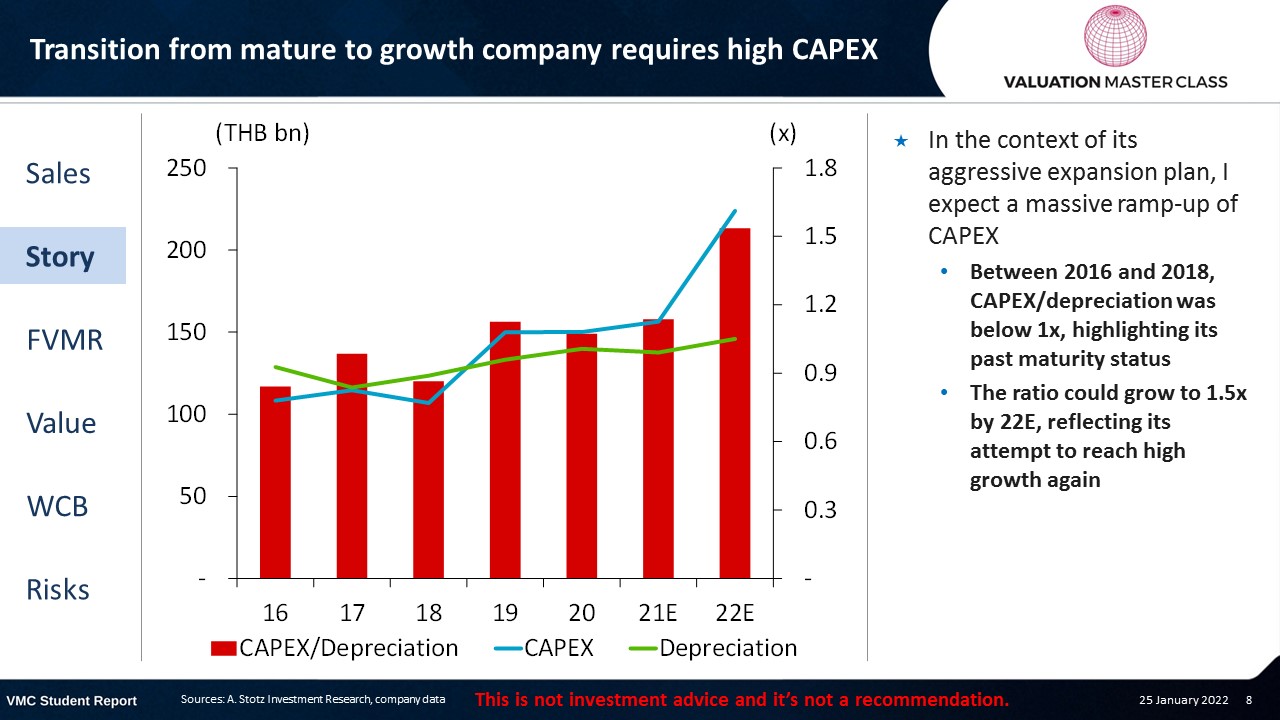

Transition from mature to growth company requires high CAPEX

- In the context of its aggressive expansion plan, I expect a massive ramp-up of CAPEX

- Between 2016 and 2018, CAPEX/depreciation was below 1x, highlighting its past maturity status

- The ratio could grow to 1.5x by 22E, reflecting its attempt to reach high growth again

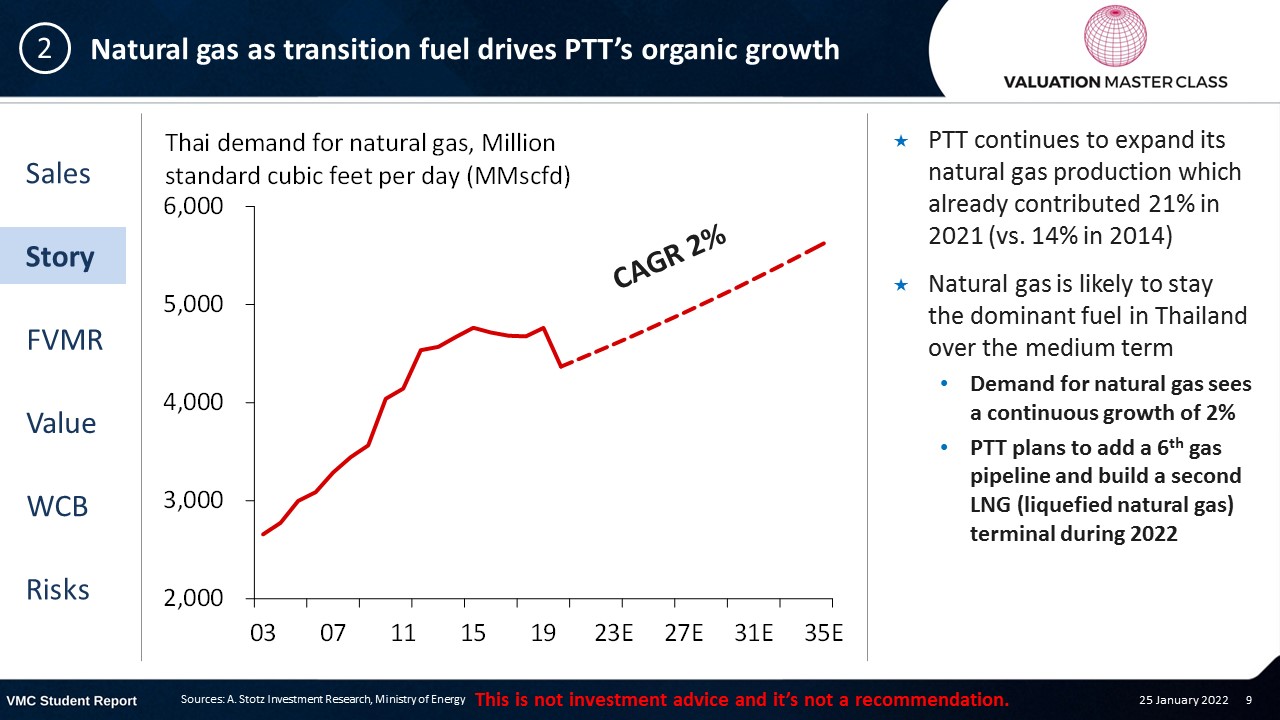

Natural gas as transition fuel drives PTT’s organic growth

- PTT continues to expand its natural gas production which already contributed 21% in 2021 (vs. 14% in 2014)

- Natural gas is likely to stay the dominant fuel in Thailand over the medium term

- Demand for natural gas sees a continuous growth of 2%

- PTT plans to add a 6th gas pipeline and build a second LNG (liquefied natural gas) terminal during 2022

PTT also aims to become a dominant player in renewable energy

- In 2021, PTT entered the renewable energy market with a capacity of 200MW

- This equals around 1.3% of Thailand’s total renewable energy capacity (15,000 MW)

- The company plans to allocate 15% of its CAPEX budget to expand its existing capacity to 12,000MW by 2030

- The target might be a bit ambitious

- Also, I expect the margin from this business to be lower than gas and oil

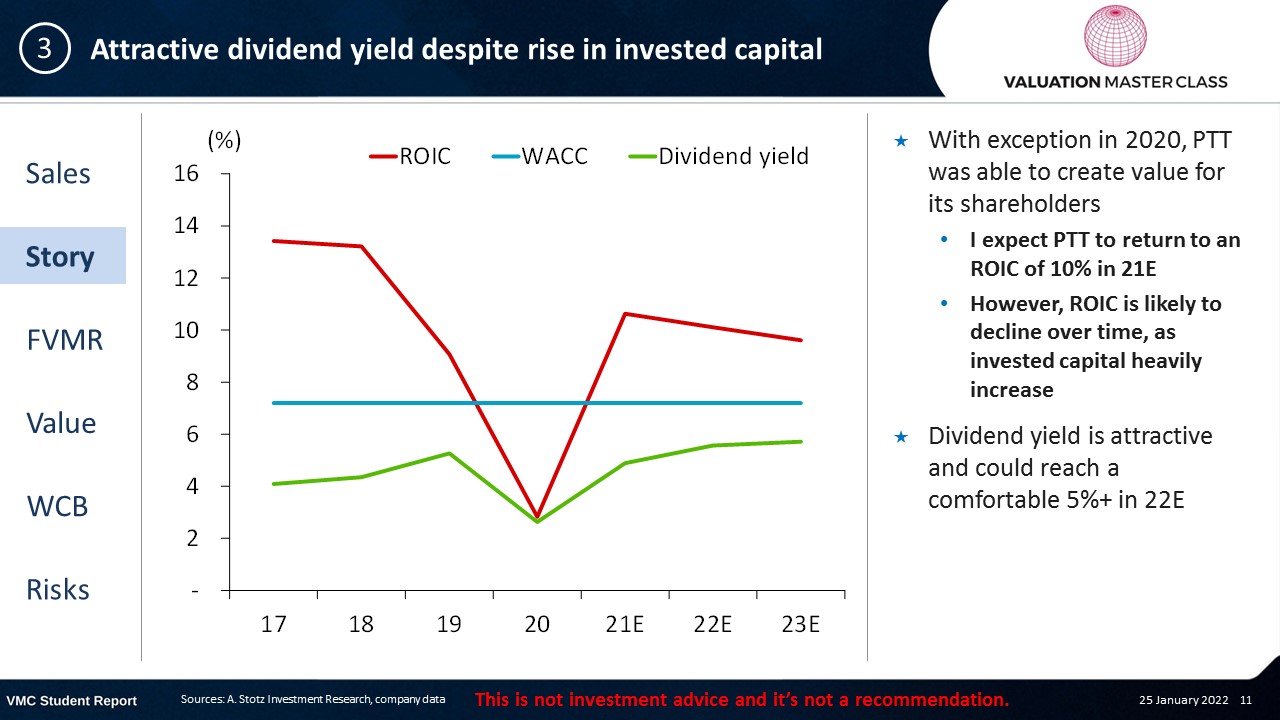

Attractive dividend yield despite rise in invested capital

- With exception in 2020, PTT was able to create value for its shareholders

- I expect PTT to return to an ROIC of 10% in 21E

- However, ROIC is likely to decline over time, as invested capital heavily increase

- Dividend yield is attractive and could reach a comfortable 5%+ in 22E

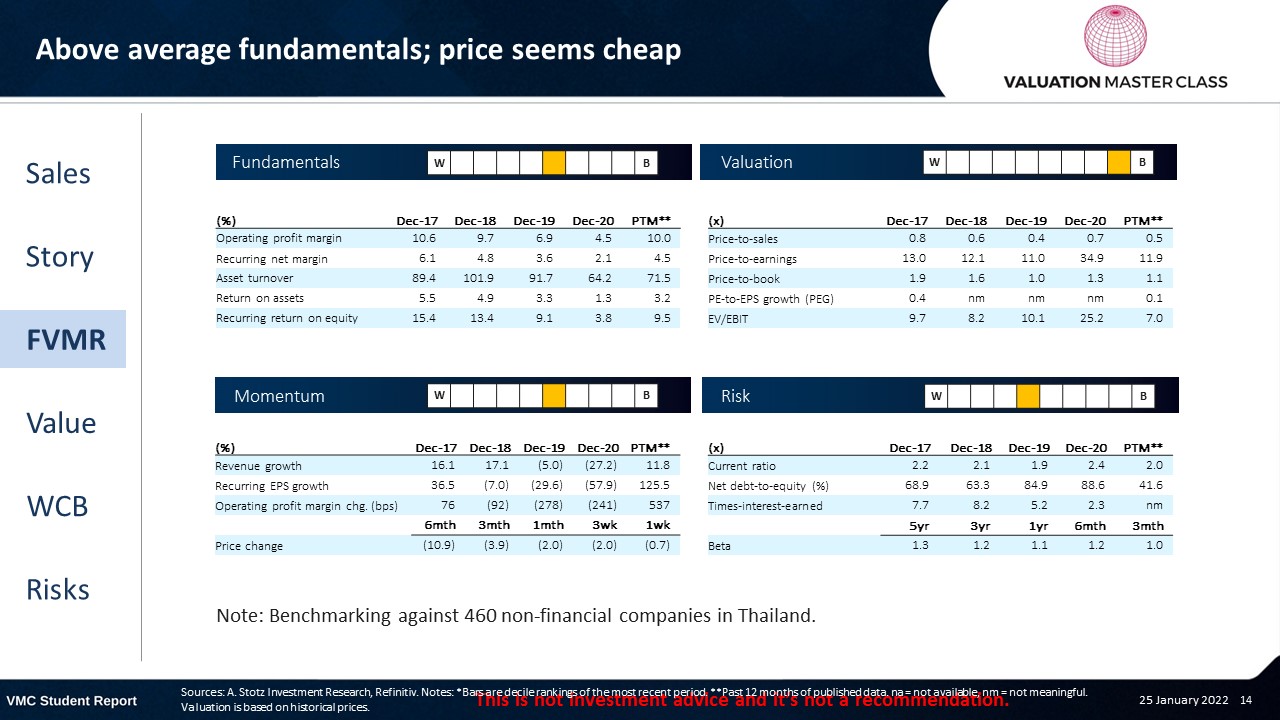

FVMR Scorecard – PTT

- A stock’s attractiveness relative to stocks in that country or region

- Attractiveness is based on four elements

- Fundamentals, Valuation, Momentum, and Risk (FVMR)

- Scale from 1 (Best) to 10 (Worst)

Analysts are pessimistic about the company’s outlook

- Analysts’ consensus is bullish with 90% of analysts issuing a BUY recommendation

- Currently there is only 1 BUY recommendation

- 7 analysts recommend to HOLD, with another 8 recommending to SELL

- Consensus expects strong revenue prospects over the next 3 years

- Also, operating margin should return to pre-pandemic levels

Get financial statements and assumptions in the full report

P&L – PTT

- Strong bottom-line mainly driven by heightened demand

Balance sheet – PTT

- PTT is a capital-intensive business, with more than 57% of total assets being net fixed assets

- The global average is around 33%

- Its aggressive expansion plan requires the issuance of further capital, likely debt

- Being state-owned, I don’t expect PTT to struggle raising capital

Ratios – PTT

- Given its capital-intensive nature, efficiency is likely to stay below 100%

- Gross margin in 21E and 22E on a record level, but it might be difficult to maintain a gross margin above 15% over time

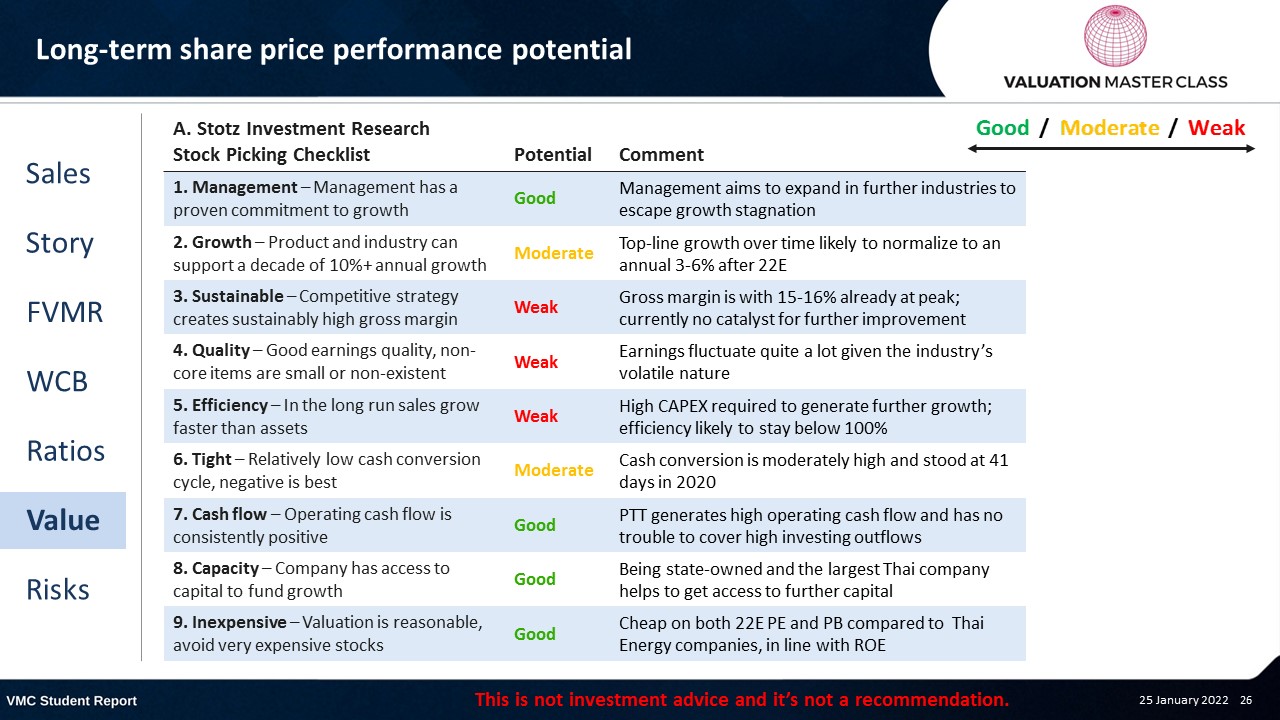

Long-term share price performance potential

Free cash flow – PTT

- I expect rising CAPEX in line with its strategy to realize further growth by investing in other industries

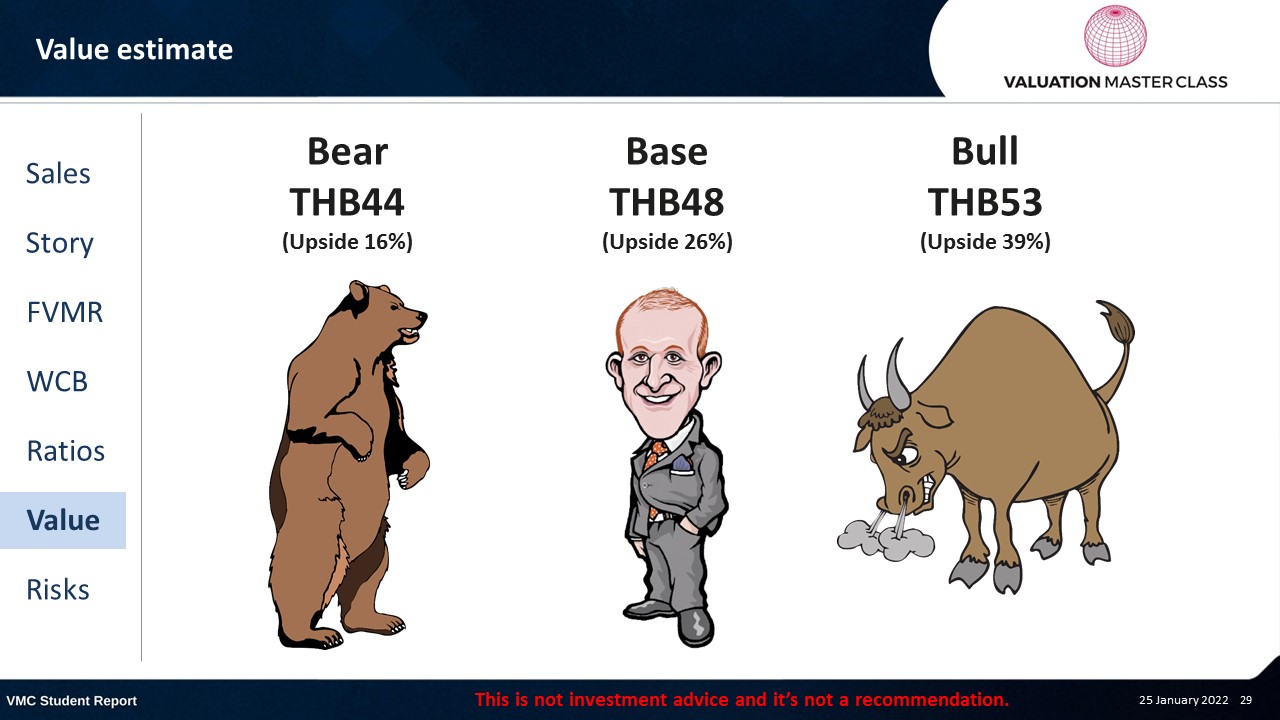

Value estimate – PTT

- My revenue and margin forecast is roughly in line with analyst’s consensus

- Engaging in new industry lines and M&A could justify a terminal growth rate of 4%

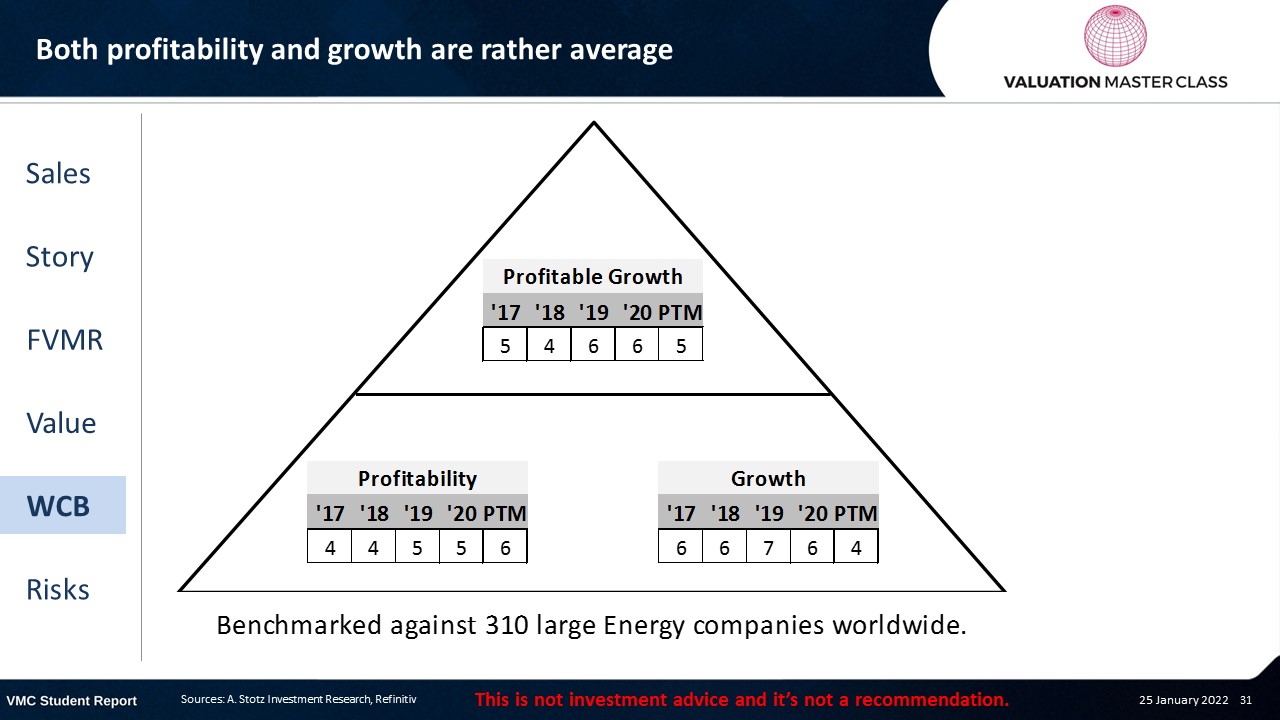

World Class Benchmarking Scorecard – PTT

- Identifies a company’s competitive position relative to global peers

- Combined, composite rank of profitability and growth, called “Profitable Growth”

- Scale from 1 (Best) to 10 (Worst)

Key risk is fluctuations in oil price

- Depleting gas reserves in questions longevity of its gas business

- Engaging in new industries might be a risky move (e.g. overpaying acquisitions; inefficiency in integration)

- Volatile commodity prices could pressure margin

Conclusions

- Growing gas business and renewables drive organic growth

- PTT’s expansion to other industries could be still value accretive

- Attractive dividend yields despite growing CAPEX requirements

Download the full report as a PDF

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.