India: High Funding for Future Growth

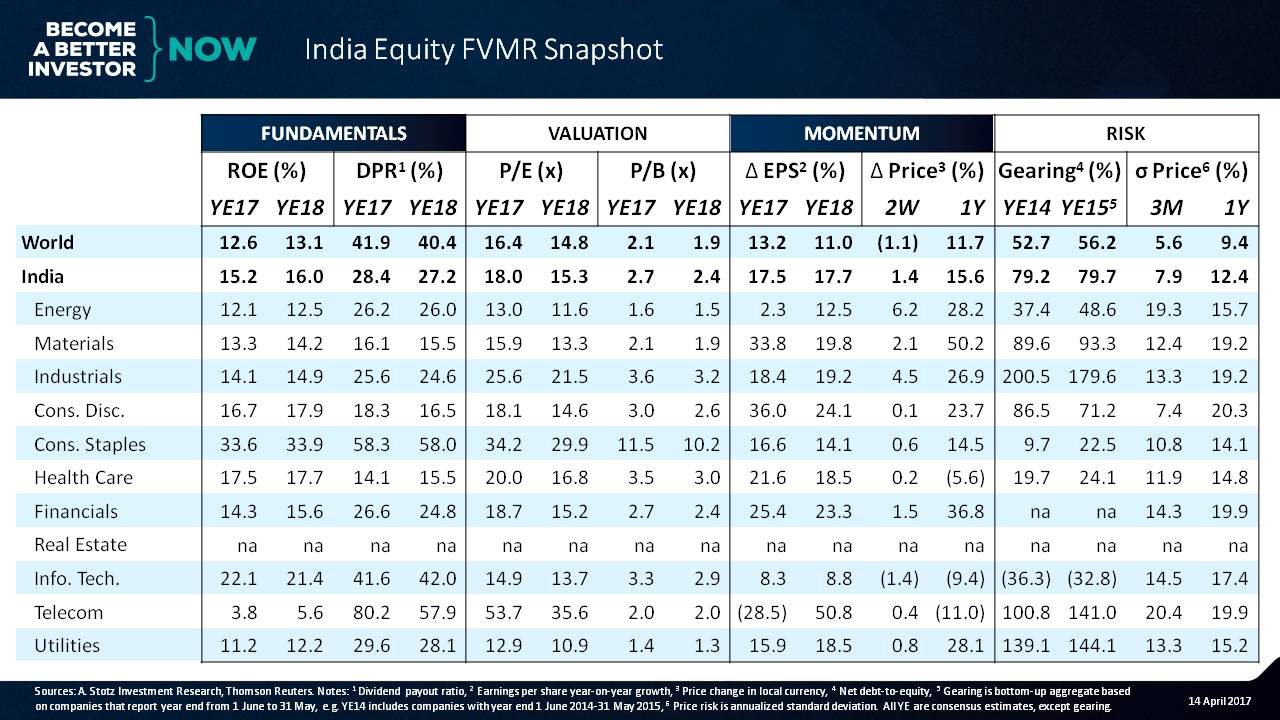

India Equity FVMR Snapshot

Fundamentals: Hi, ROE!

What we can see is that India’s ROE is at a premium to the world ─ nice work, India!

And we can see that the dividend payout ratio is lower than the world. That makes sense for two reasons.

The first reason is if you’re a developing market, and you’ve got a lot of investment opportunities, so it’s better to not pay out as much and use that money to fund your growth.

The second reason is because if you have a high ROE such as 15% to 16%, in this case, why not keep investing that money at that high ROE?

Valuation: A little bit expensive

What we can see next is that the PE of the Indian market is about 15x to 18x, and price-to-book is a little bit expensive compared to the world.

But this is a product of earnings growth experiencing high momentum right now! It’s much higher in both the current year and analysts’ expectations for the next year.

Momentum: Earnings translating to large share price gains

We can also see that this is being rewarded. Share prices over the past year have been doing very well relative to the rest of the world.

While companies have a little bit more gearing than the rest of the world, that makes sense because companies can borrow as much as they want when they’re highly profitable.

India’s ROE of 15% is probably high due to this level of gearing.

We could look at ROA to try to see the difference.

Volatility: Above world average

The volatility of the Indian market is about 12% versus the global at about 9%. It’s not a perfect comparison because global has got every company in the world, but we can use it to look across the country.

India by sector

We can see that consumer staples have quite a high ROE, and the lowest ROE that we can find here is in the utilities sector, which is not unusual. Being a regulated industry, it’s hard for utilities to gouge customers.

And if we follow PE levels sector-by-sector, we see that high ROEs correlate with high PE and price-to-book levels. So consumer staples look awfully expensive, but EPS looks pretty steady.

Now, let’s look at some of the other sectors.

We can see that telecom is an expensive sector, but that’s on an earnings basis that is largely a product of a fallout in earnings followed by a recovery.

If we look at price to book, it’s not bad ─ about 2x price-to-book.

However, the problem that the telecoms sector is facing is that the ROE is disastrous. Recently, there’s been a new entrant who’s been slashing prices, which is causing the crash in performance.

Where is there a recovery in EPS?

We can see pretty good recovery right there in the materials and consumer discretionary sectors. The materials sector, in particular, is up 50%, and consumer discretionary is up about 24%.

Sector Volatility

Finally, let’s take a look at the volatility of the sectors, and what we can see is that the lowest volatility sector is consumer staples followed by healthcare.

The highest volatility sectors, as we’ve mentioned, are consumer discretionary and telecoms.

This gives you a general picture of what’s happening in India ─ relatively high return on equity, though that may be partially because gearing is a bit high. You’re paying slightly higher than the world average PE and price-to-book, but you’re getting steady earnings growth in return.

Right now, analysts are forecasting between 17% and 18% earnings growth.

So it’s not a bad story in India right now.

If you want to see the FVMR snapshot for your country, just let me know in the comments below.

Have a great day!

Get our Equity FVMR Snapshots for free to your inbox every Monday!

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.