China Equity FVMR Snapshot: ‘China in Your Hand—Every Week’

Watch the video with Andrew Stotz or read about how to use the China Equity FMVR Snapshot below.

China in Your Hand—Every Week

We’re excited to debut our new weekly research tool, the China Equity FVMR Snapshot. It uses the same format we first reviewed in our post about the Global Equity FVMR Snapshot.

With this Snapshot, you will always be up to date; just one page covers Fundamentals, Valuation, Momentum, and Risk—what we call “FVMR.”

This is the same information used by elite institutional investors and fund managers around the world.

And the best part? You do nothing.

Once you’ve signed up, you will receive a one-page PDF every Monday. Print it out. Put it on your desk. Use it in your analysis of what’s going on in China.

First: An important distinction. Commonly, when people talk about Chinese stocks, they’re talking about China H-shares. These are the shares that are traded in Hong Kong.

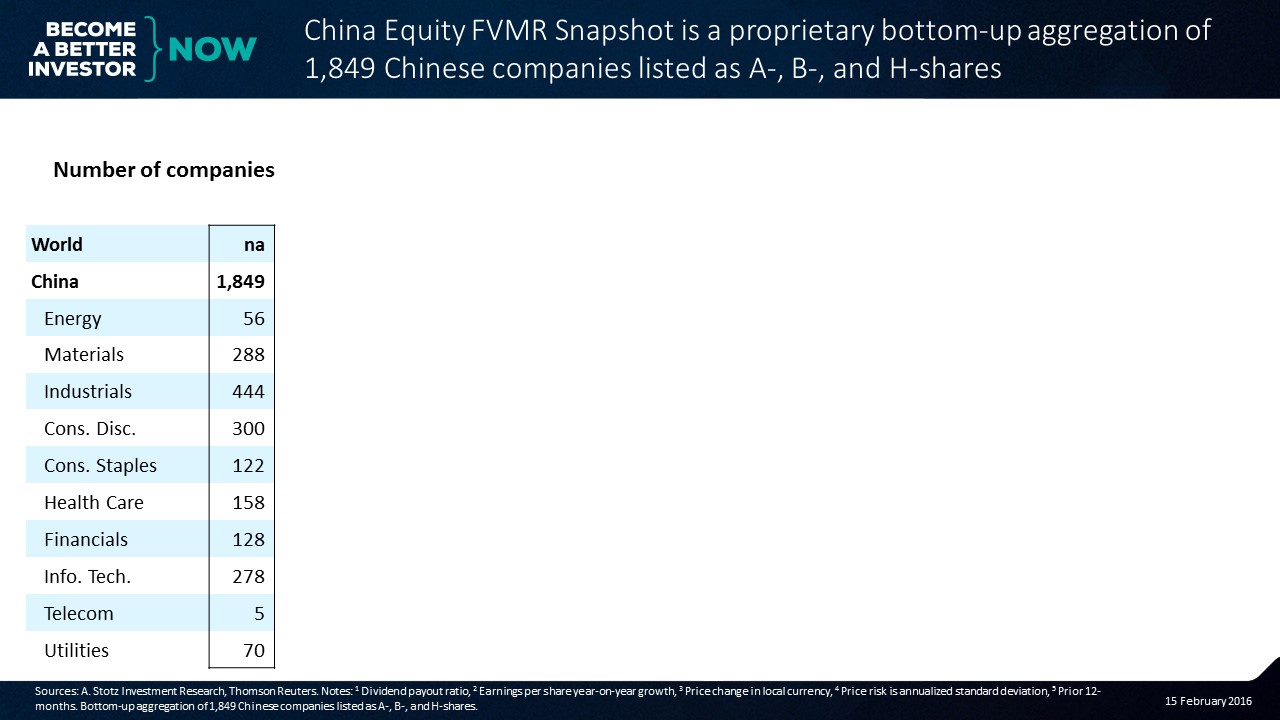

But this FVMR Snapshot is a proprietary bottom-up aggregation of 1,849 Chinese companies that are listed as A-, B-, and/or H-shares, giving you a wide breadth of market coverage.

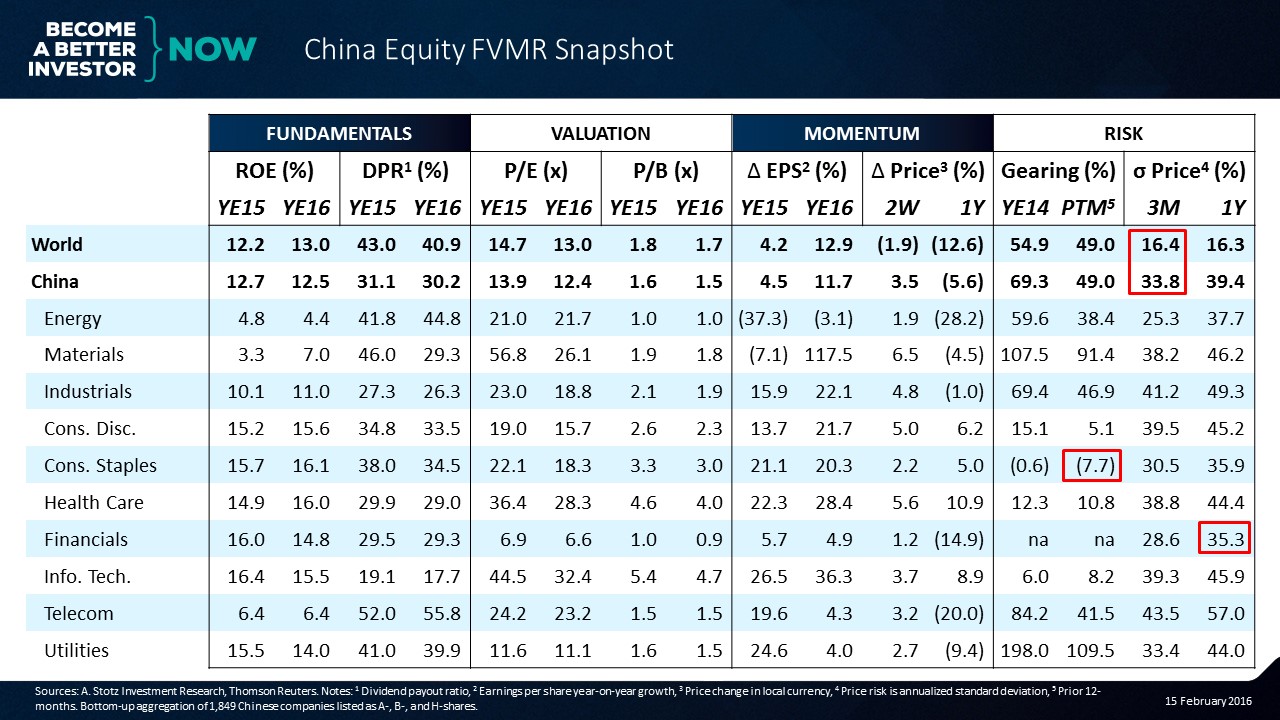

There are about 3,000 companies in China. These are the largest and the most liquid companies. What we can see above is that the largest sector by number of companies is industrials, while the smallest is telecom.

We know that telecom companies have a bit of a monopoly in most countries around the world. They’re given that monopoly through the government.

So let’s take a look at what we can see.

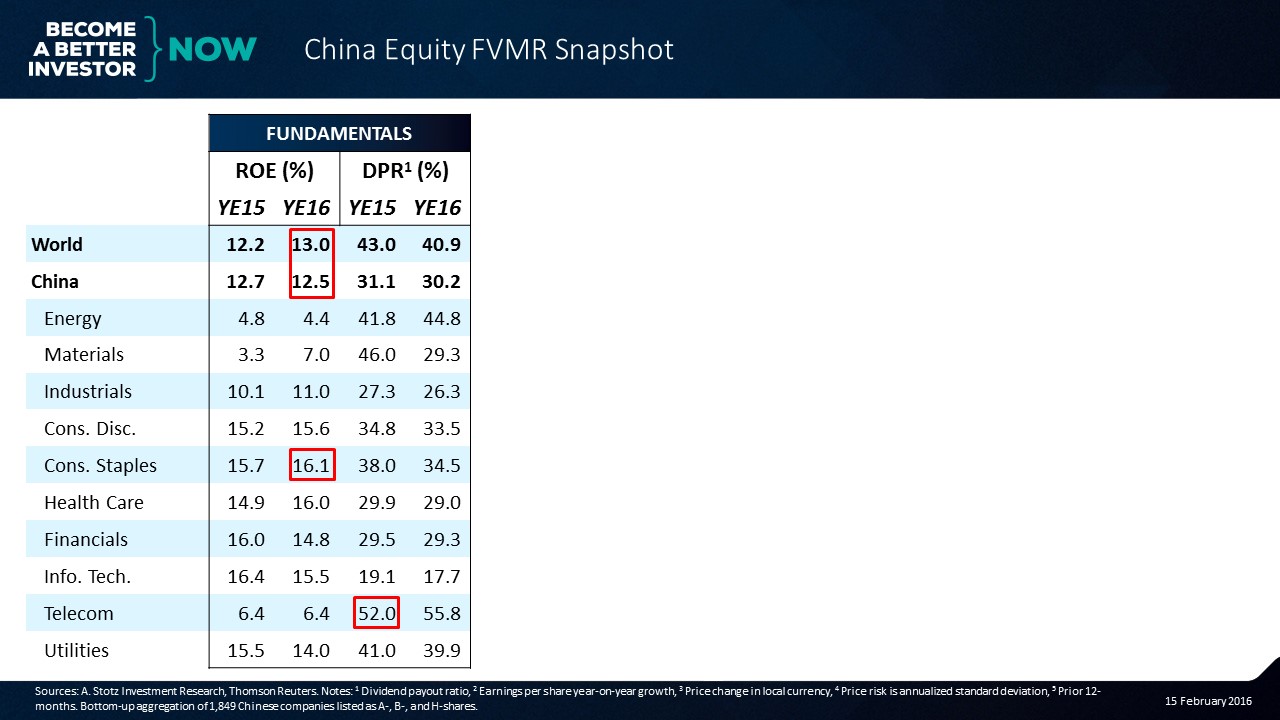

Fundamentals

In fundamentals, we look at the profitability through return on equity, and then look at the dividend payout ratio to understand what you, as an investor, get.

Let’s look at a few different highlights.

First, the expected consensus return equity for the world is about 13% in 2016, and China is a little bit less at 12.5%.

We can also see that the consumer staples sector is expected to post an increase in return on equity, rising from 15.7% in 2015 to 16.1% in 2016.

If we look at dividend payout ratio, we can see that telecoms tend to have very high dividend-payout ratios, which can make them attractive investments.

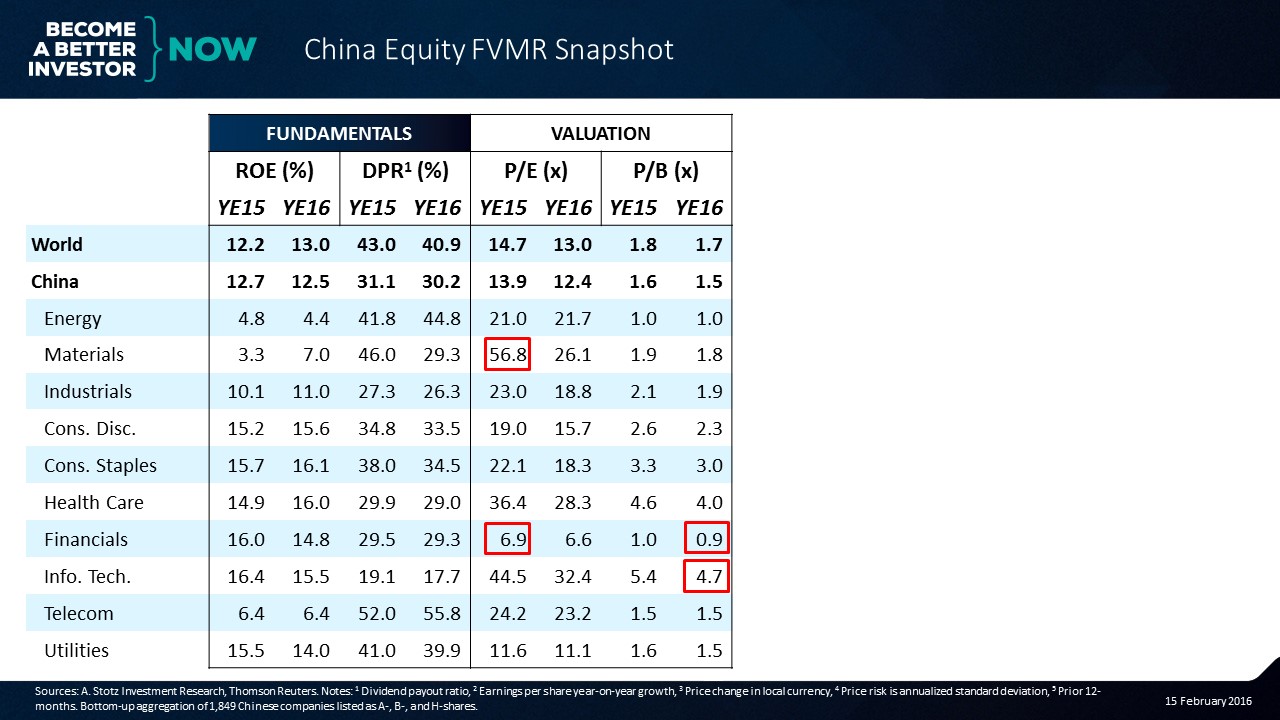

Valuation

If we look at the next area which is valuation, we can see price to earnings and price to book.

Looking at the material sector, and we see 56.8x P/E. This is a result of the tiny profits that have been earned in the wake of the collapse in oil and other commodity prices.

Financials are trading at about 7x P/E. Financials often trade with low P/Es; China financials in particular are going through a difficult stretch right now as the overall market has declined and the economic growth is falling.

Now, for price to book, we can see for financials that it’s slightly below one. Still, that’s not necessarily cheap when you think about the major headwinds China is facing as their economy slows.

As far as information technology companies (such as Alibaba) go, we can see that the price to book is almost 5x and P/Es are at 30x-40x. While those multiples may seem high, they’re not unusual for tech companies these days.

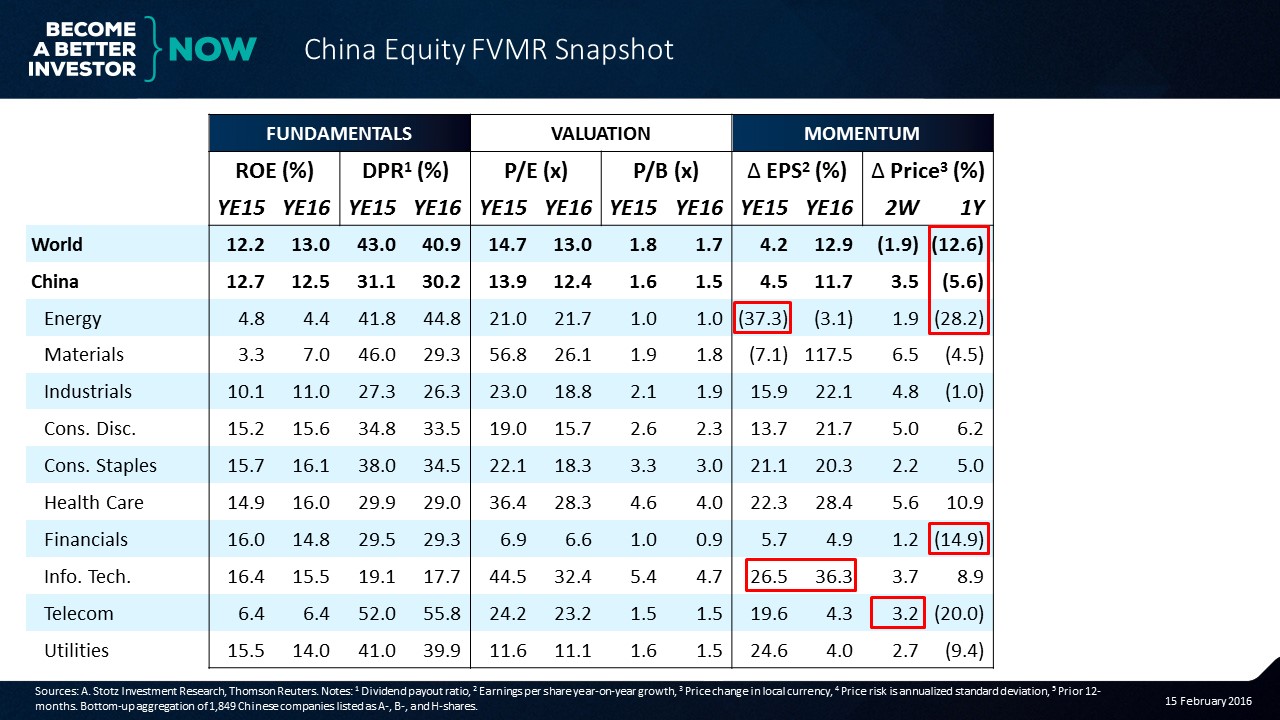

Momentum

Let’s move on to momentum. We look at earnings momentum and price momentum.

We can see a collapse in the earnings of energy companies, thanks to the fall in oil prices.

We can also see that the EPS of the information technology stocks are very, very high as they continue to grow very strongly.

We can see that they earned 26.5 in 2015 and that analysts are expecting 36.3 in 2016.

Now, let’s look at price as far as momentum is concerned and take a look at telecoms as an example: Their two-week price momentum is at 3.2%.

Let’s look at one-year price momentum. The world market is down by 12.6%. China is down 5.6%.

We can also see that energy sector is down 28.2%.

It’s interesting to see that China is only down 5.6%. Remember, we’re looking at almost 2,000 companies that are listed across China, not just the largest-cap stocks which are listed in Hong Kong.

This proprietary insight allows us to see the forest for the trees: there’s not as big of a share-price collapse in China as one might think if they only looked at the most mainstream, H-share data.

Risk

The next thing is risk where we look at gearing or net debt to equity and price risk.

Looking at this, we can see that consumer staples, much like they are around Asia, are in very good position as far as gearing goes. In fact, they have net cash.

If we look at the price, we can see that the price volatility of China is about 33.8% compared to the world index at 16.4%.

We want to be careful about comparing the world against an individual country, because the aggregation of so many different countries will always make the overall volatility fall.

But if we were to compare China’s price volatility to the U.S., the U.S. would be close to 20% and China would be at 33.8%.

Finally, we can see that the financial sector has a one-year price volatility level of about 35%.

China in Your Hand

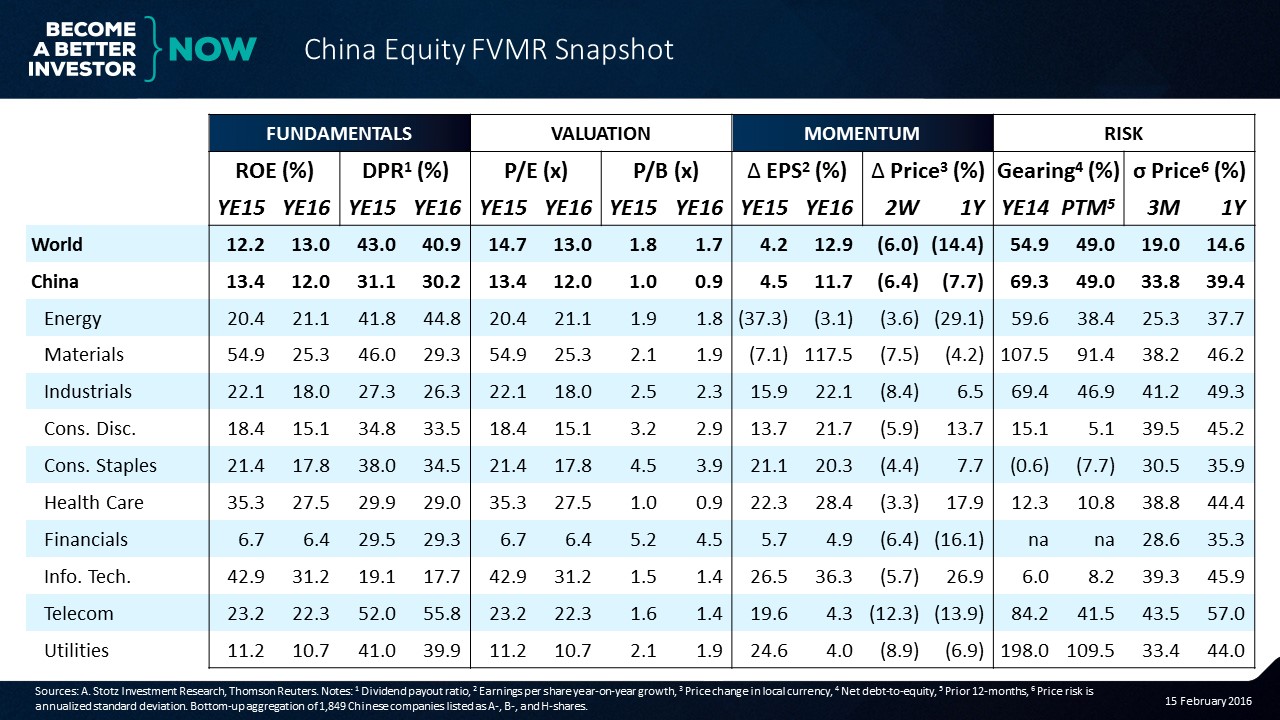

With our China Equity FVMR Snapshot, you’ll get a weekly update like the one below covering Chinese stocks.

You’re going to understand fundamentals, valuation, momentum, and risk, and the way we look at them.

After signing up, YOU will:

-

Always be up to date: Every week you will receive the updated China Equity FVMR Snapshot

-

Know all the numbers: One page covers Fundamentals, Valuation, Momentum, and Risk (FVMR)

-

Be professional: Use the same information as institutional investors and fund managers

-

Not have to do anything else to stay informed: After signing up you will receive a one-page PDF every Monday

The China Equity FVMR Snapshot is free for everyone signing up within a limited time period. Sign up now to not miss out on getting it for free.

NOTE: You’ll have to fill in the form below to receive the China Equity FVMR Snapshot even if you’re already subscribing to the Global or Korea Equity FVMR Snapshot and/or a founding member that get our newsletter.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.