A. Stotz All Weather Strategy – March 2022

The All Weather Strategy significantly outperformed a traditional 60/40 portfolio by 2.1% in March 2022. Fed’s unwillingness to crash markets to support equities. War in Ukraine, recovery demand, and supply-chain bottlenecks to drive commodities and gold. Risks: Inflation quickly gets under control, global recession, Fed rate hikes crashing the US market.

The A. Stotz All Weather Strategy is Global, Long-term, and Diversified:

- Global – Invests globally, not only Thailand

- Long-term – Gains from long-term equity return, while trying to reduce a portion of losses during equity market downturns

- Diversified – Diversified globally across four asset classes

The All Weather Strategy is available in Thailand through FINNOMENA. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

Review

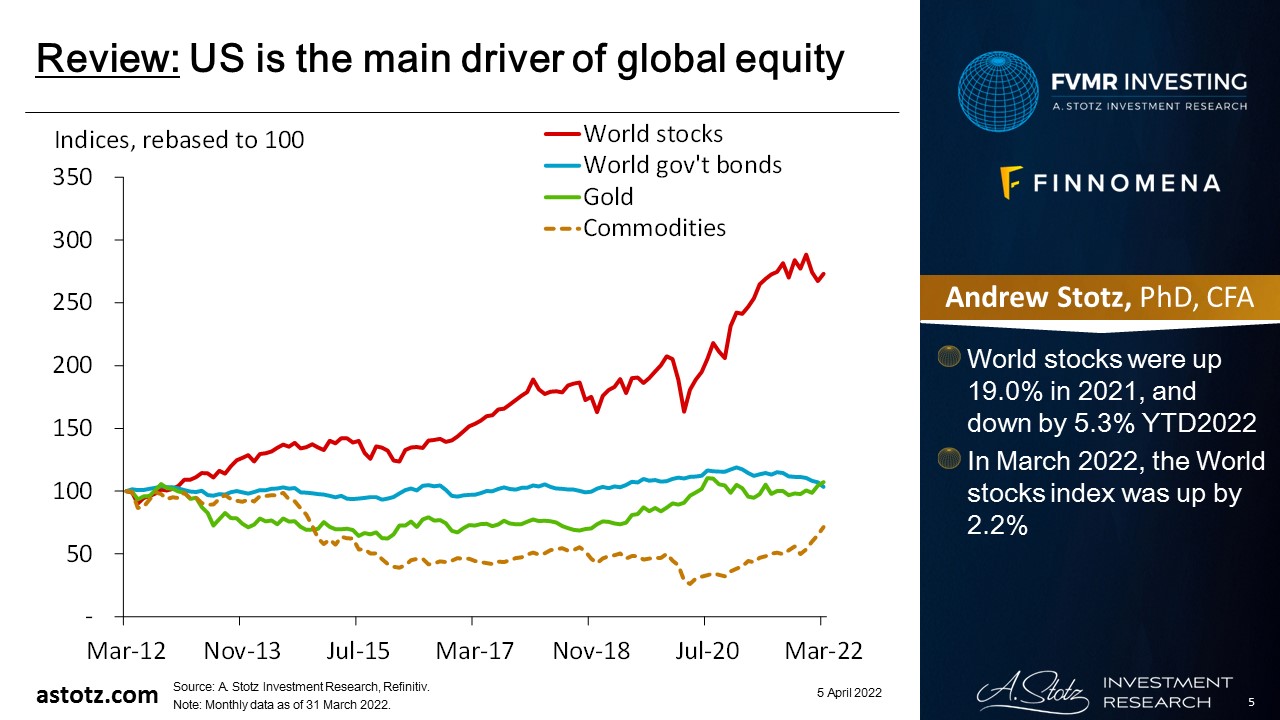

US is the main driver of global equity

- World stocks were up 19.0% in 2021 and down by 5.3% YTD2022

- In March 2022, the World stocks index was up by 2.2%

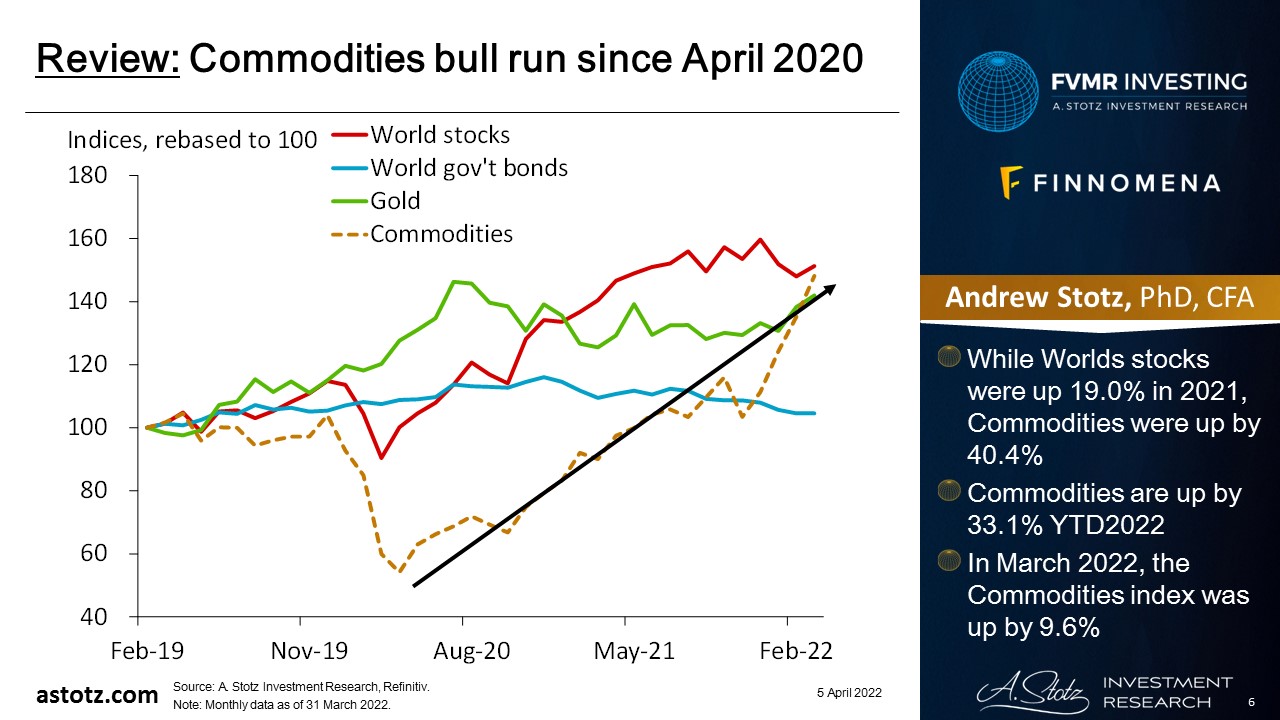

Commodities bull run since April 2020

- While Worlds stocks were up 19.0% in 2021, Commodities were up by 40.4%

- Commodities are up by 33.1% YTD2022

- In March 2022, the Commodities index was up by 9.6%

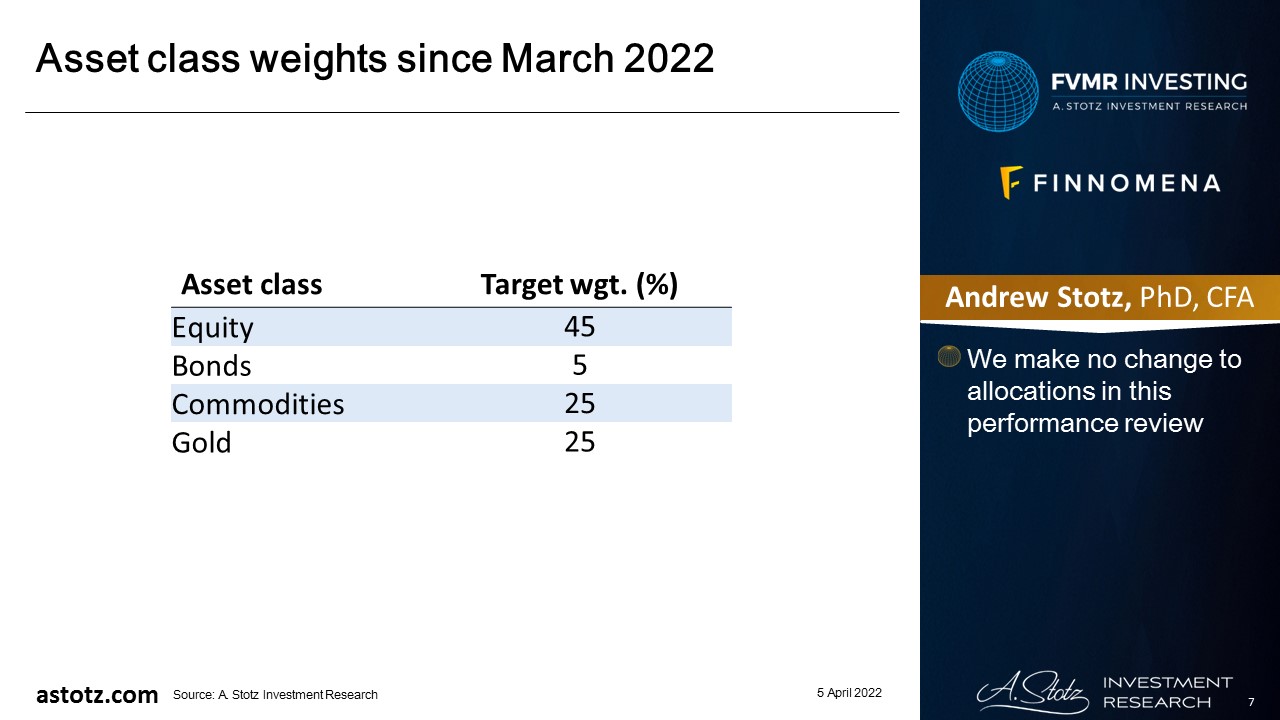

Asset class weights since March 2022

- We make no change to allocations in this performance review

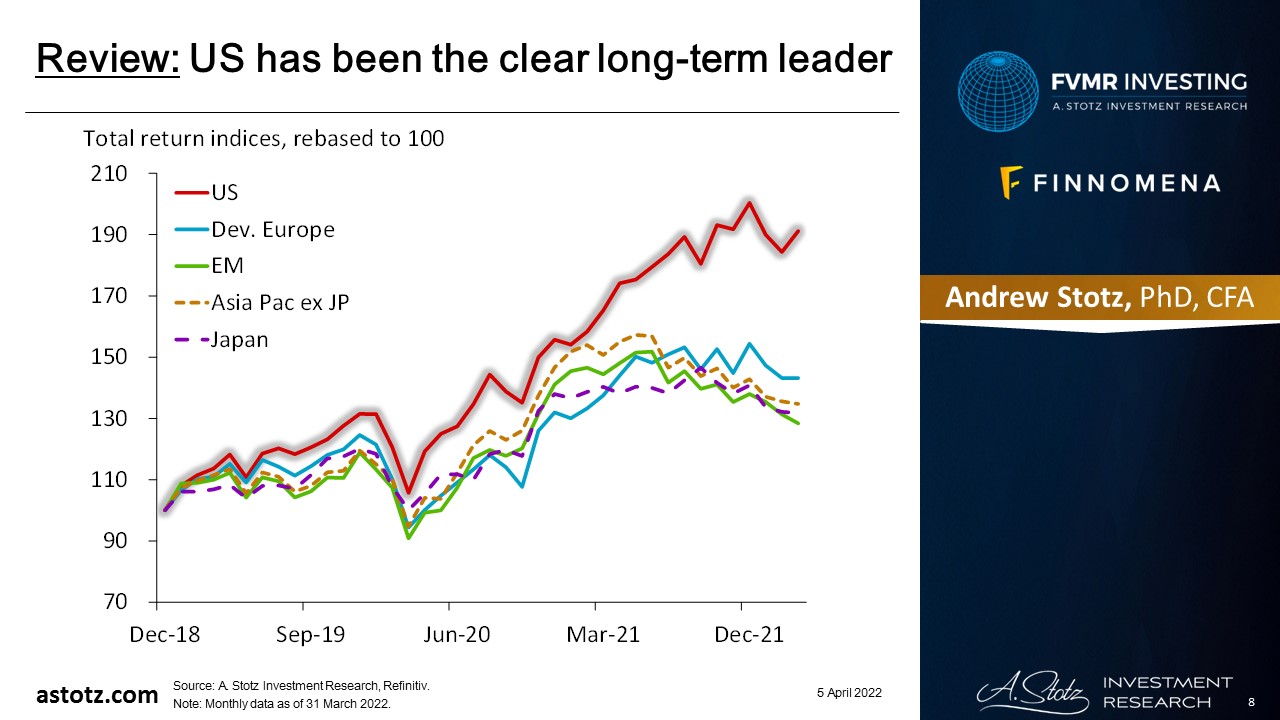

US has been the clear long-term leader

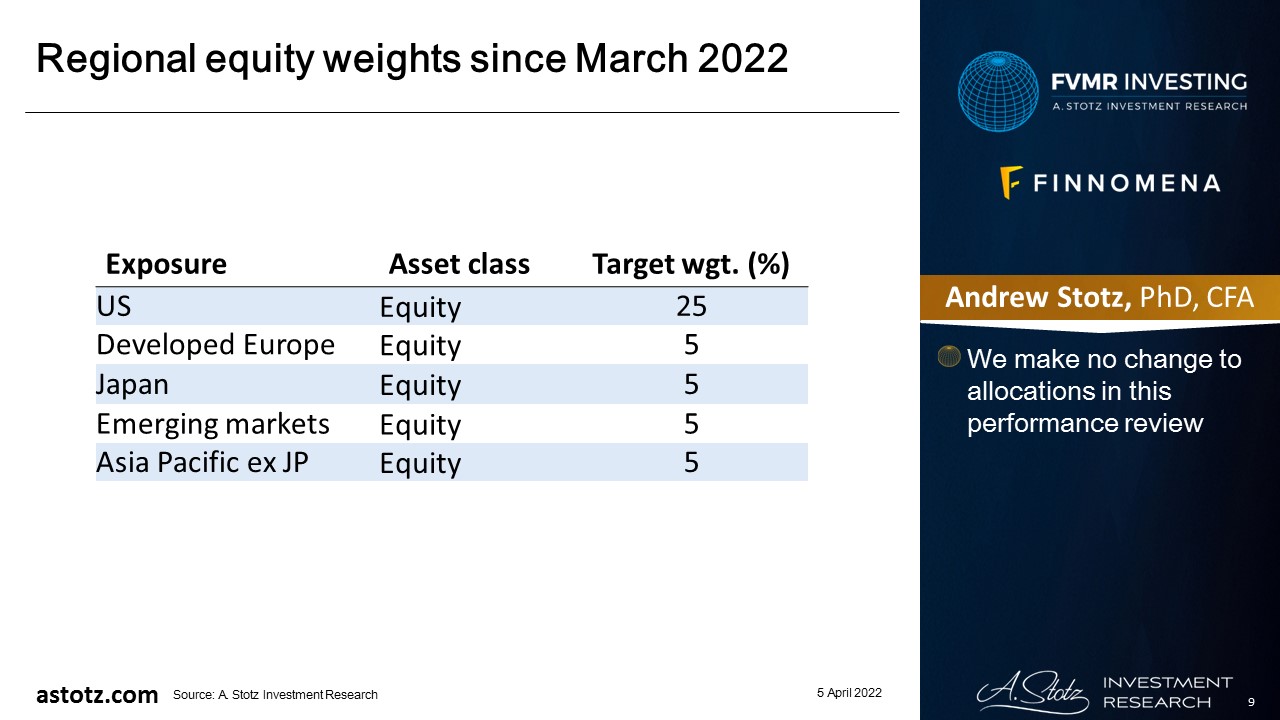

Regional equity weights since March 2022

- We make no change to allocations in this performance review

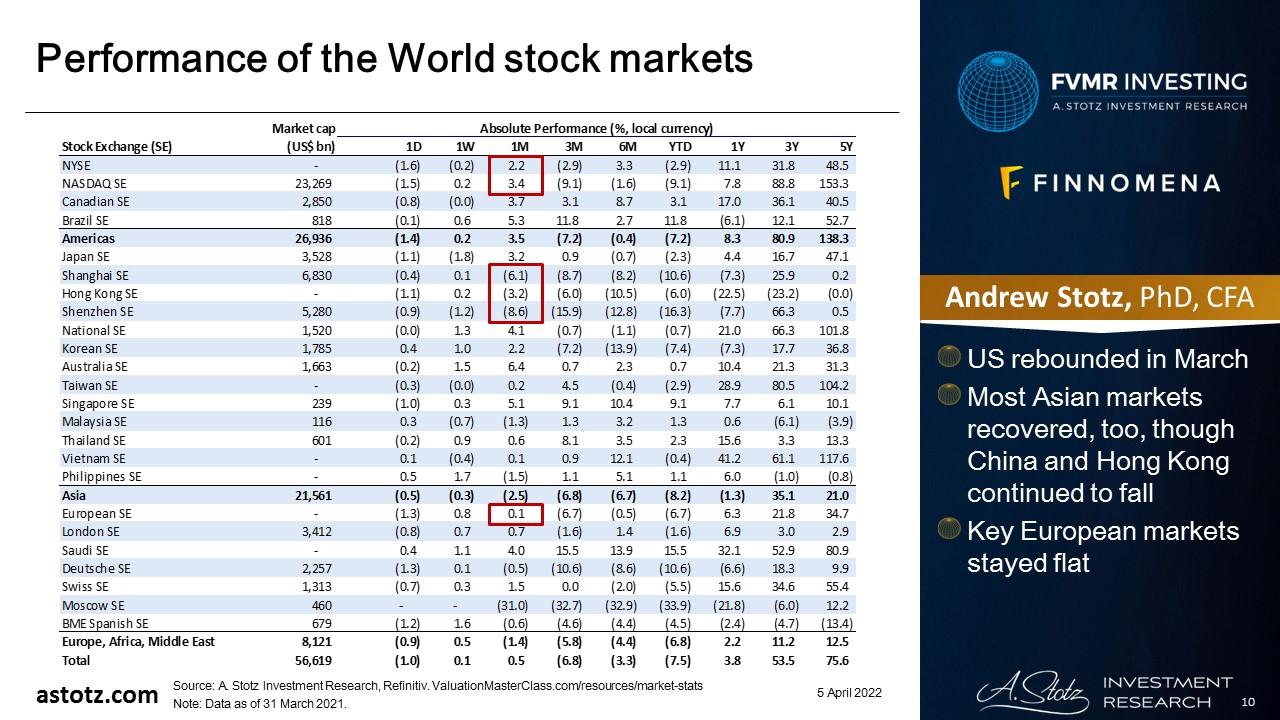

Performance of the World stock markets

- US rebounded in March

- Most Asian markets recovered, too, though China and Hong Kong continued to fall

- Key European markets stayed flat

25% weight to the best equity performer

- In our March 2022 revision, we reduced our equity allocation to 45%

- We have a 25% target allocation to US equity and a minimum 5% target allocation to the other regions

- US was the best-performing equity this month and was up by 5.9%

Developed markets outperformed

- There were hopes for nearing a resolution between Russia and Ukraine, which led to a recovery in Developed markets equity

- Emerging markets and Asia underperformed as the US$ strengthened and China fell

- A stronger US$ is typically negative for Emerging markets

Worst quarter ever for US Treasuries

- We have a small 3% target allocation to the Thai money market, which was flat

- The main purpose of our money market allocation is downside protection

- Since the inception of the “Bloomberg U.S. Treasury Total Return Index” in 1973, 1Q22 was the worst on record, down by 5.6%

- Other asset classes did well in March; hence, it was good with to have a small allocation

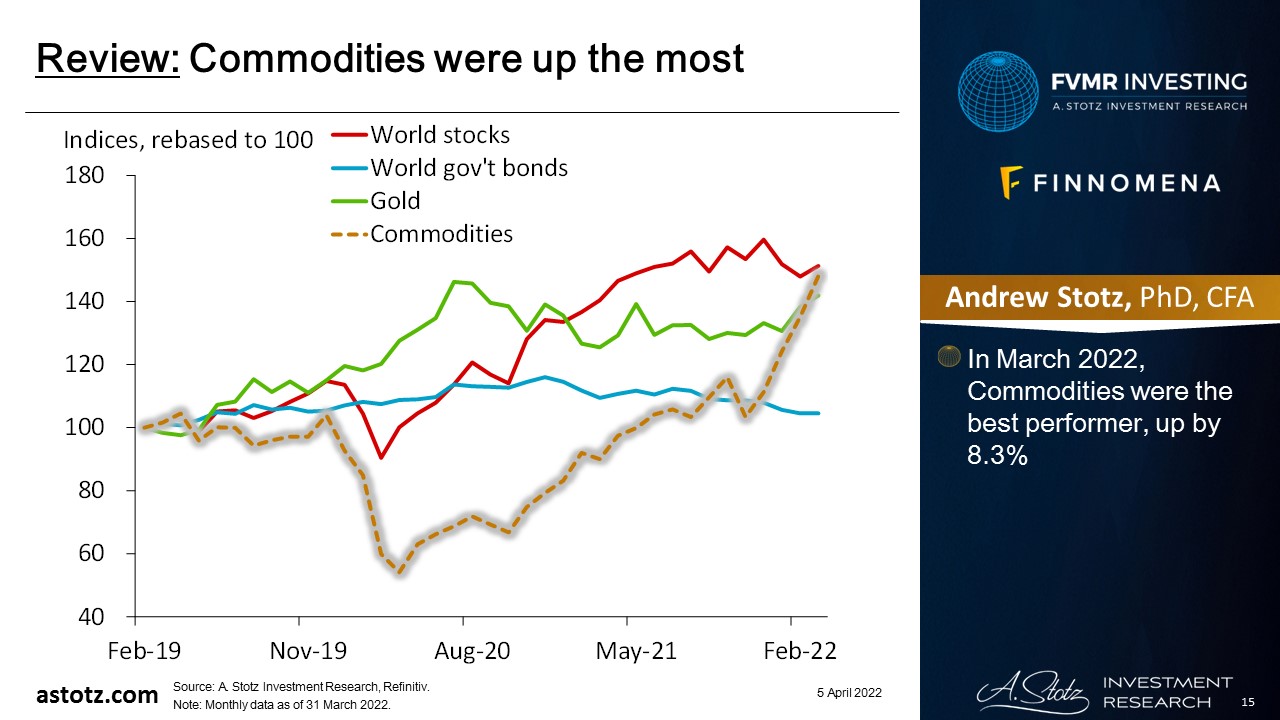

Commodities were up the most

- In March 2022, Commodities were the best performer, up by 8.3%

Energy continued to drive commodities

- Commodity groups where Russia and Ukraine are big exporters were the strongest performers

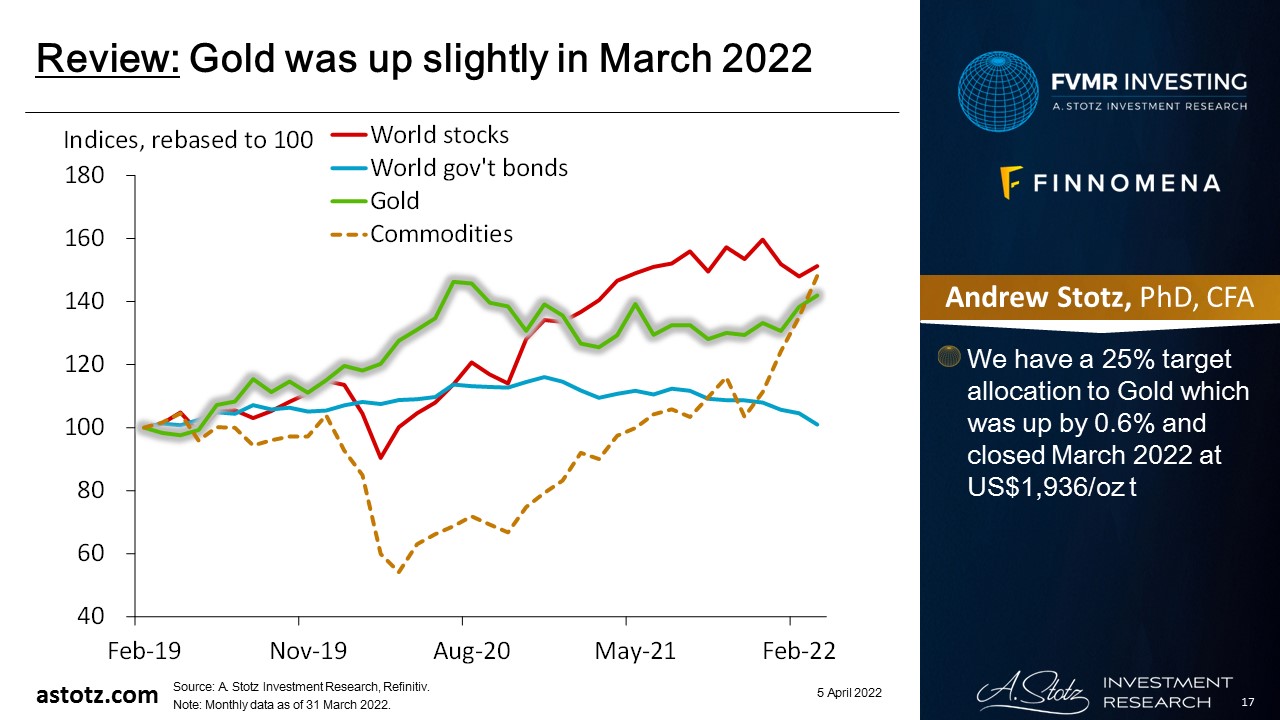

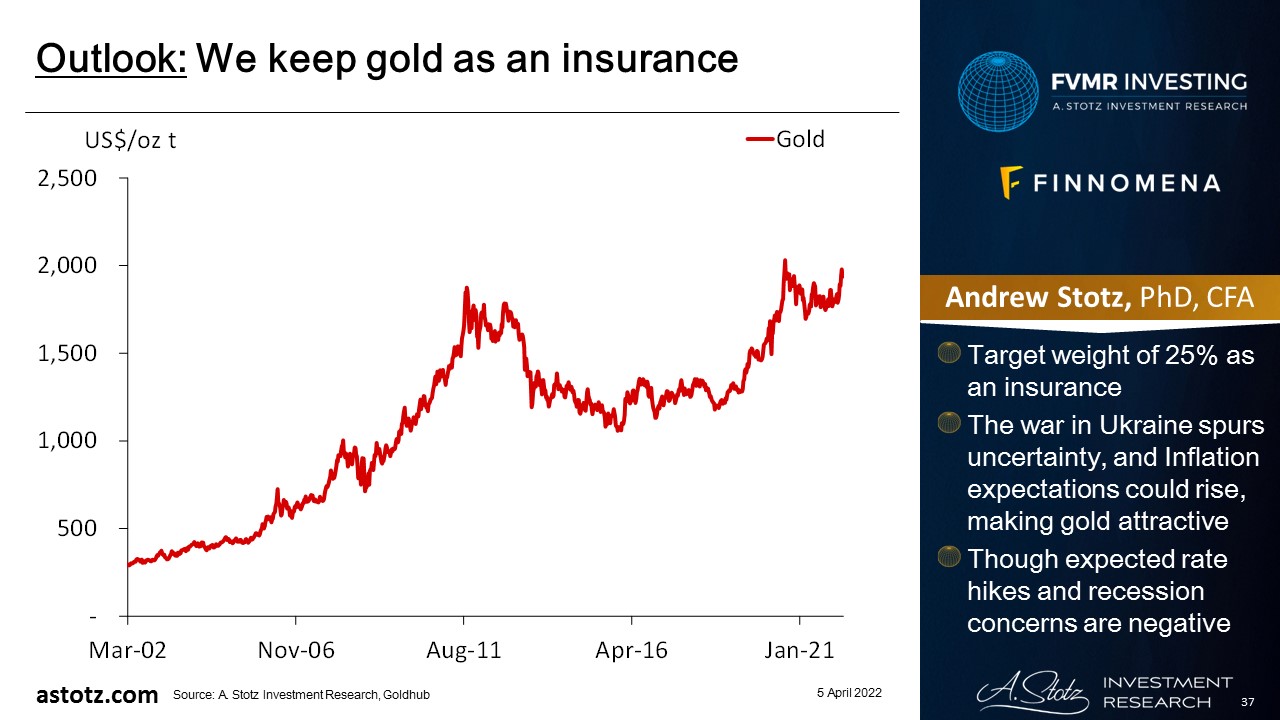

Gold was up slightly in March 2022

- We have a 25% target allocation to Gold which was up by 0.6% and closed March 2022 at US$1,936/oz t

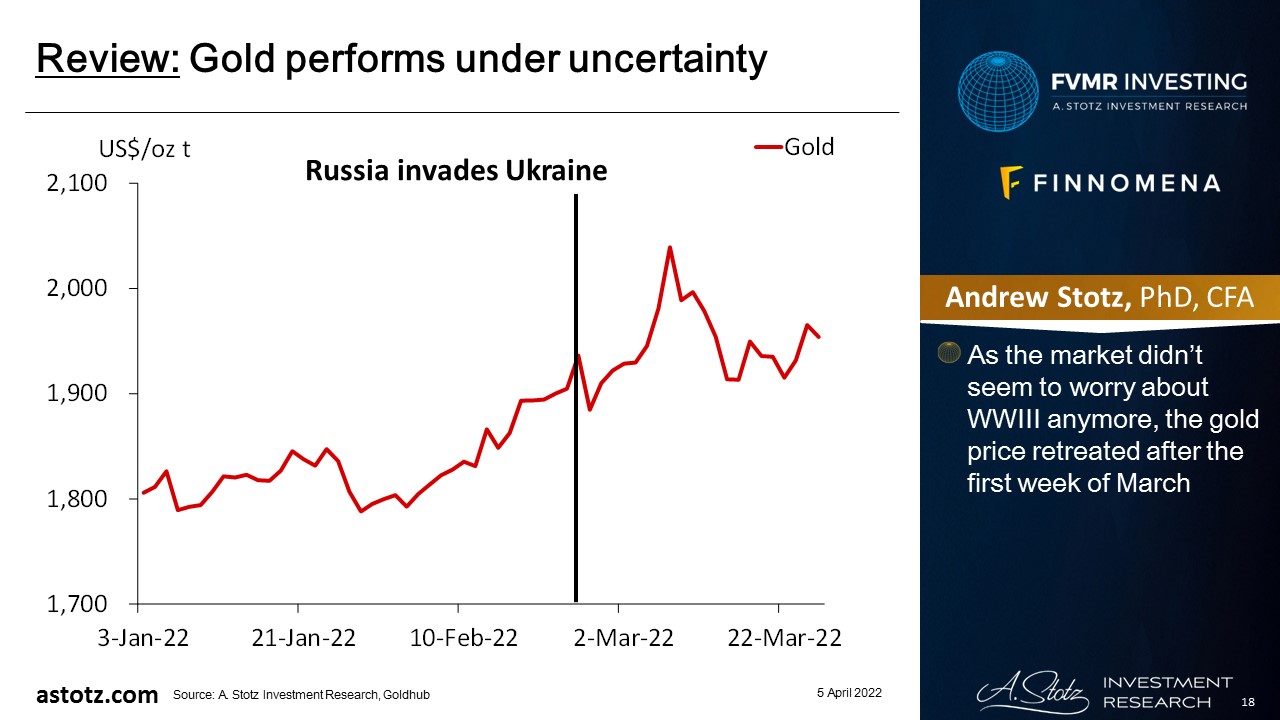

Gold performs under uncertainty

- As the market didn’t seem to worry about WWIII anymore, the gold price retreated after the first week of March

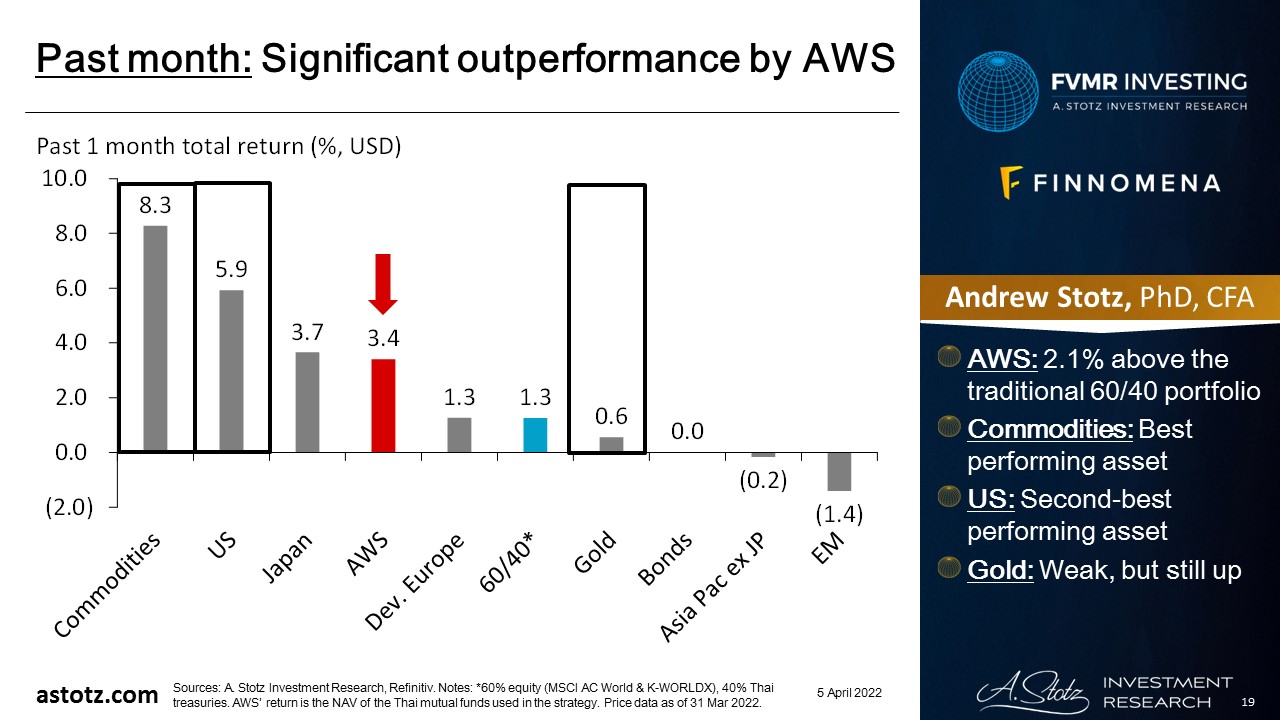

March 2022: Significant outperformance by AWS

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- AWS: 2.1% above the traditional 60/40 portfolio

- Commodities: Best performing asset

- US: Second-best performing asset

- Gold: Weak, but still up

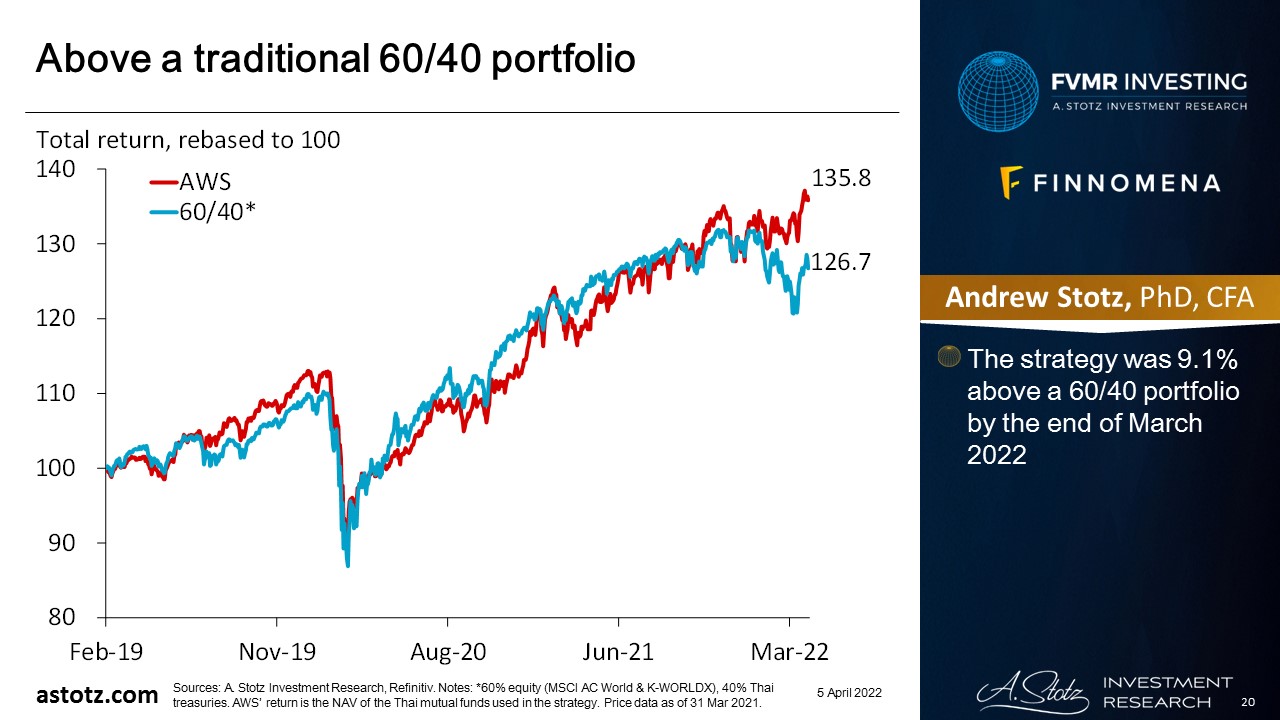

Above a traditional 60/40 portfolio

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- The strategy was 9.1% above a 60/40 portfolio by the end of March 2022

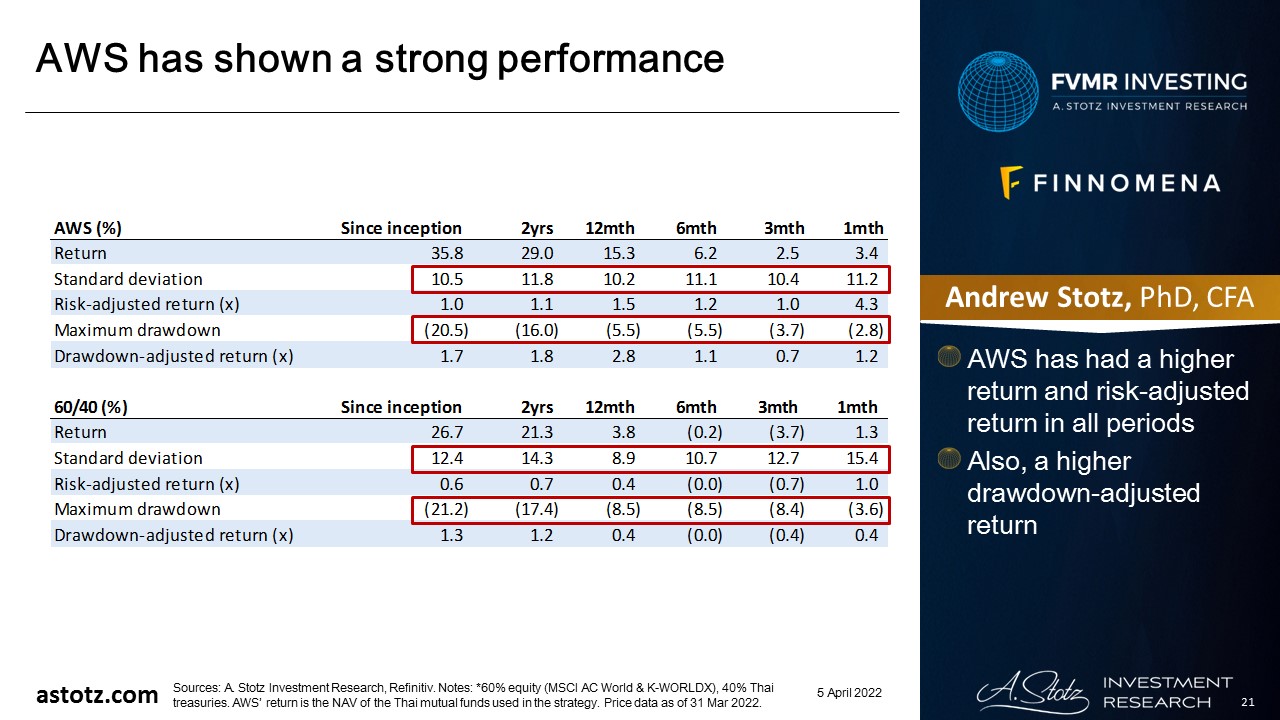

AWS has shown a strong performance

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- AWS has had a higher return and risk-adjusted return in all periods

- Also, a higher drawdown-adjusted return

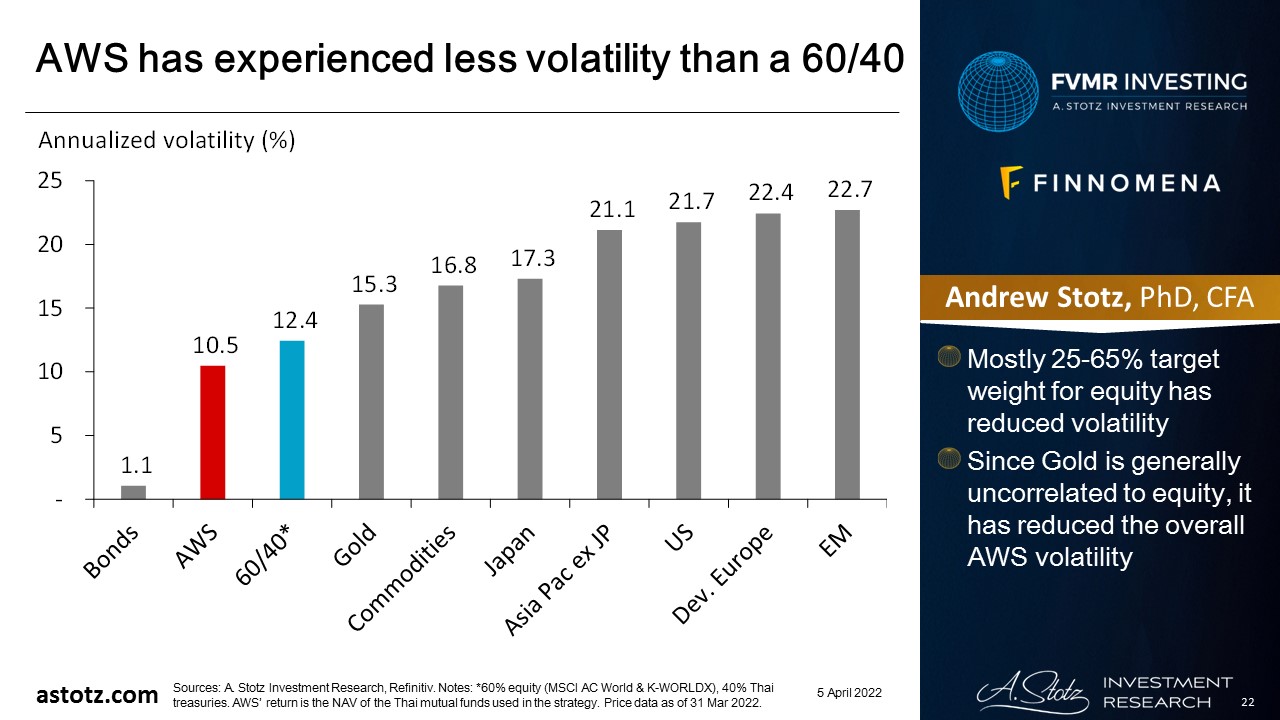

AWS has experienced less volatility than a 60/40

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- Mostly 25-65% target weight for equity has reduced volatility

- Since Gold is generally uncorrelated to equity, it has reduced the overall AWS volatility

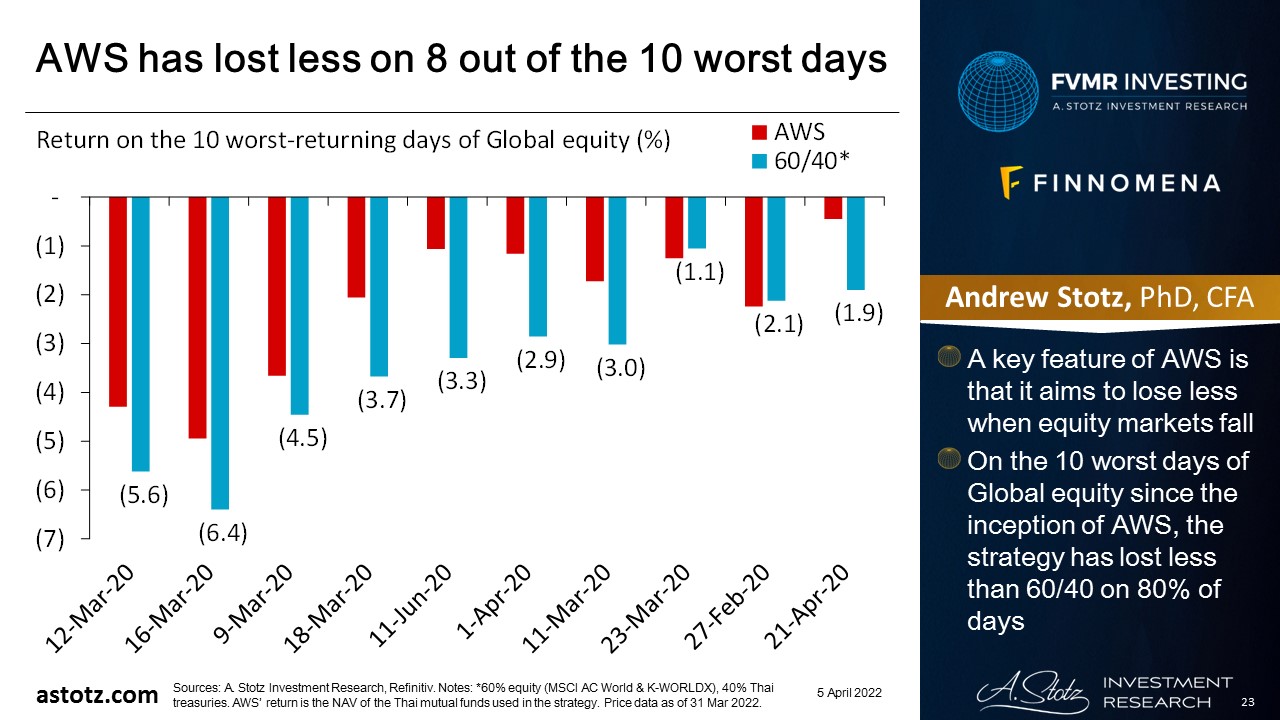

AWS has lost less on 8 out of the 10 worst days

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- A key feature of AWS is that it aims to lose less when equity markets fall

- On the 10 worst days of Global equity since the inception of AWS, the strategy has lost less than 60/40 on 80% of days

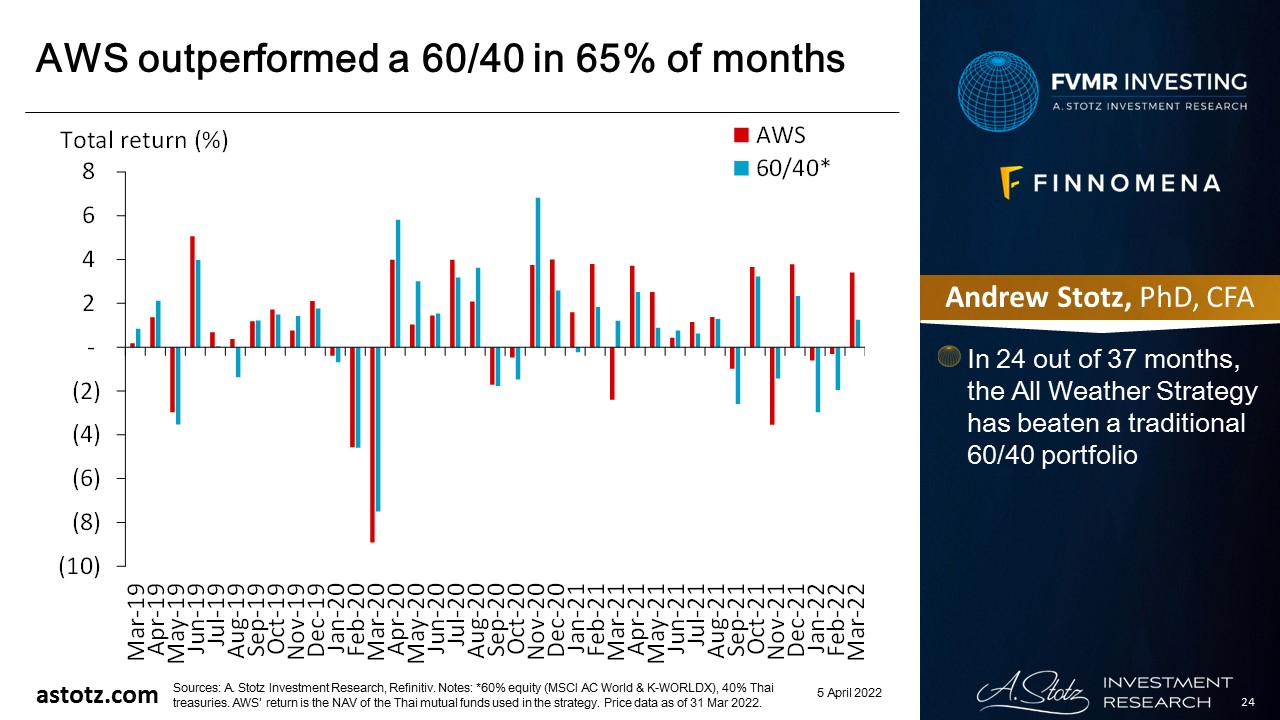

AWS outperformed a 60/40 in 65% of months

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- In 24 out of 37 months, the All Weather Strategy has beaten a traditional 60/40 portfolio

Outlook

Expect continued high volatility

- In the near term, we expect continued equity volatility due to the war in Ukraine

- In our revision in March 2022, we reduced the equity allocation to 45% from 65% and raised gold to 25% from 5%

Expect Fed to support the US market

- American companies are doing well and have global pricing power

- US economy to remain strong thanks to Gov’t spending

- Biden and the Democrats need Powell to prop up markets ahead of the November mid-terms

- So, we have a 25% target allocation to US equity

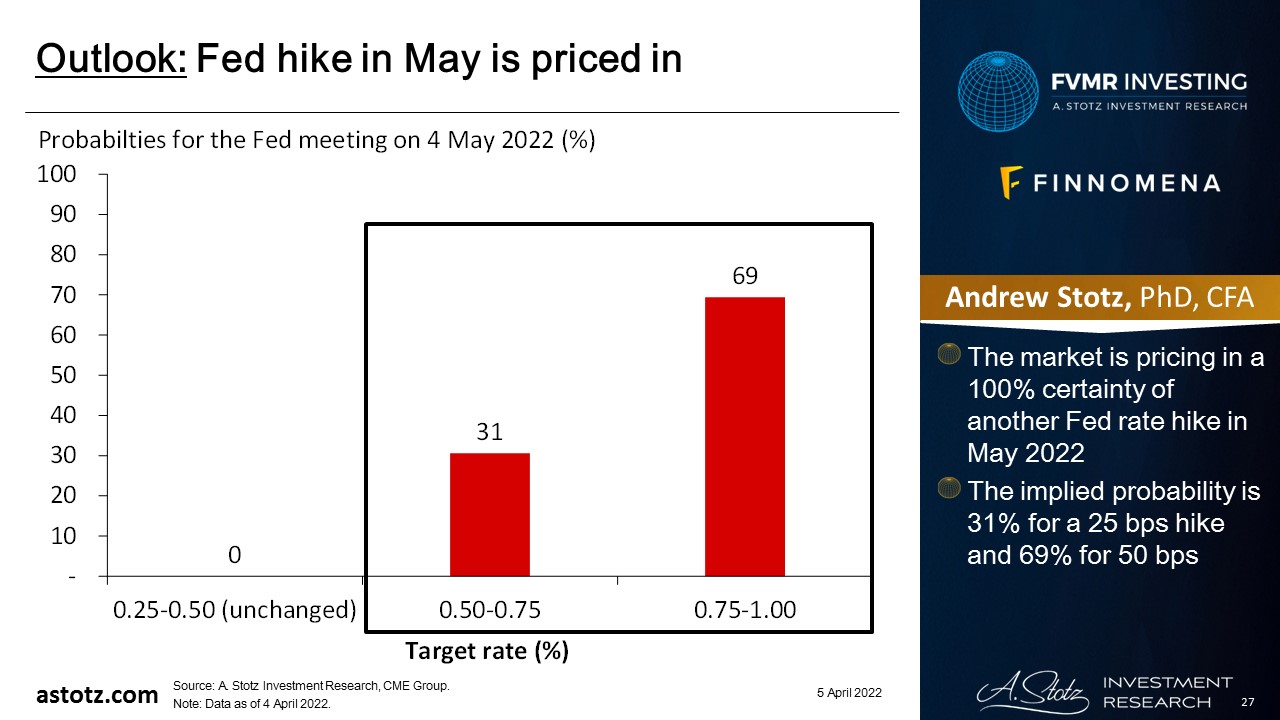

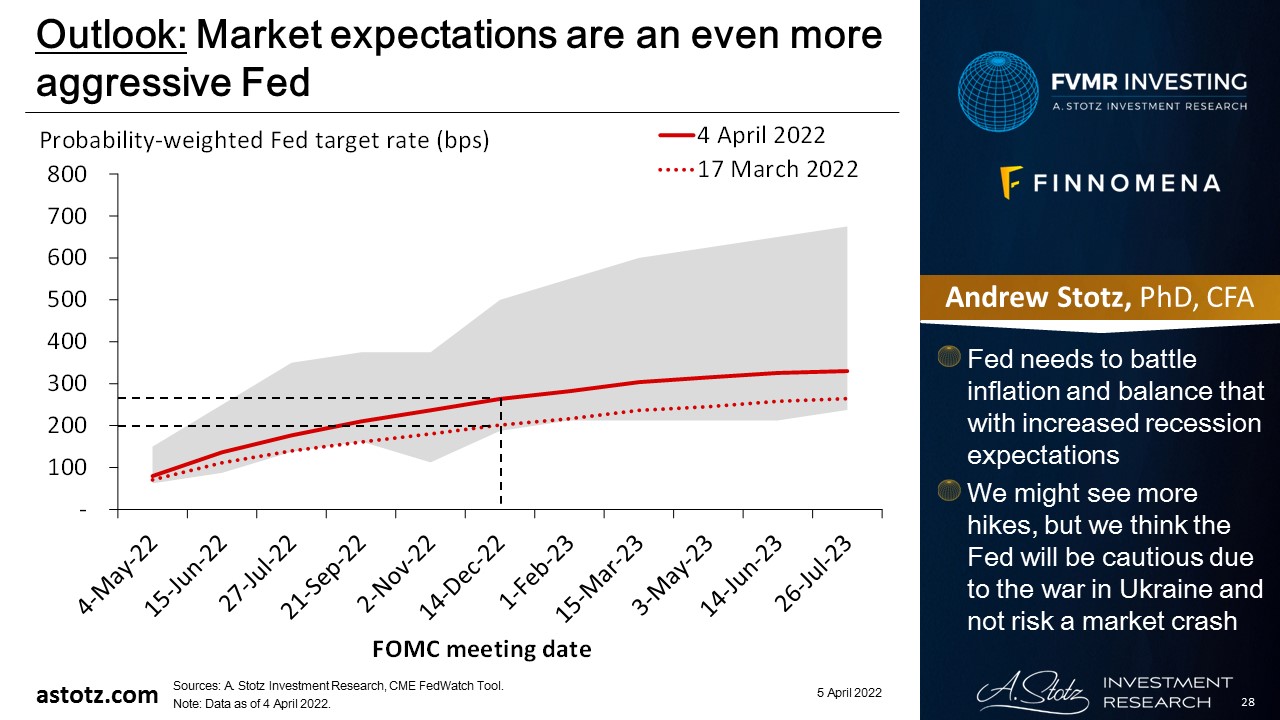

Fed hike in May is priced in

- The market is pricing in a 100% certainty of another Fed rate hike in May 2022

- The implied probability is 31% for a 25 bps hike and 69% for 50 bps

Market expectations are an even more aggressive Fed

- Fed needs to battle inflation and balance that with increased recession expectations

- We might see more hikes, but we think the Fed will be cautious due to the war in Ukraine and not risk a market crash

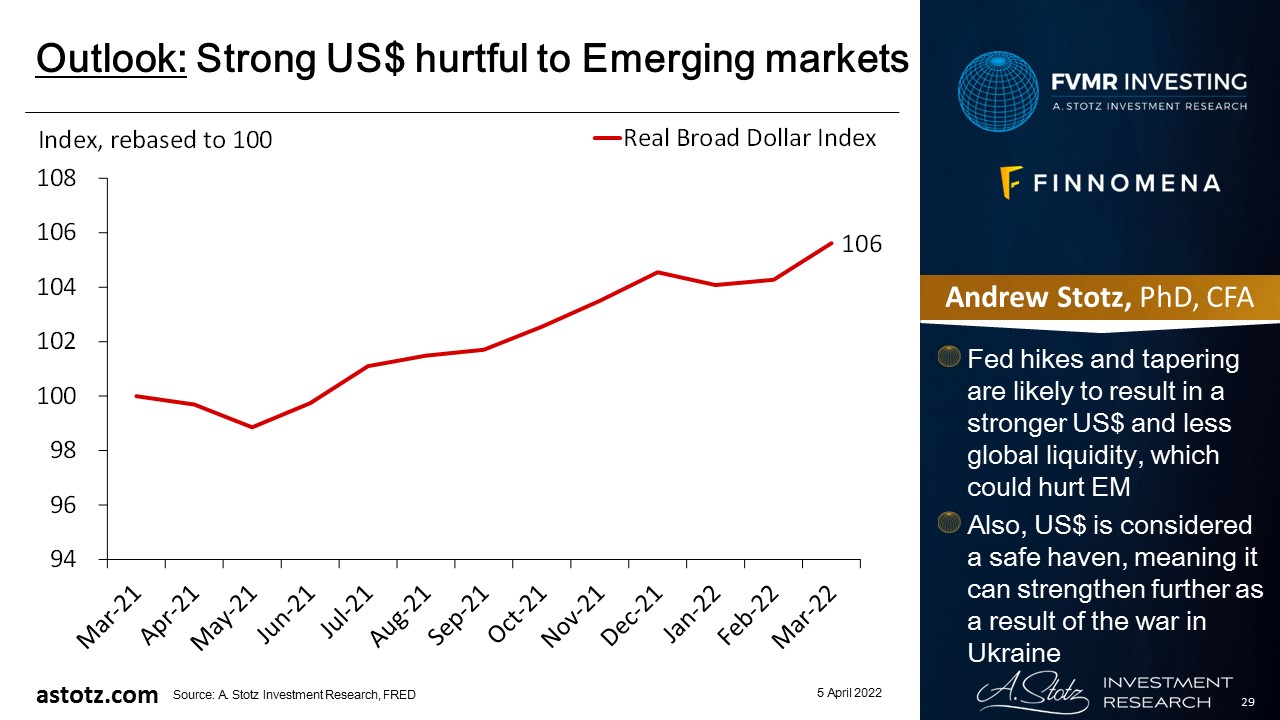

Strong US$ hurtful to Emerging markets

- Fed hikes and tapering are likely to result in a stronger US$ and less global liquidity, which could hurt EM

- Also, US$ is considered a safe haven, meaning it can strengthen further as a result of the war in Ukraine

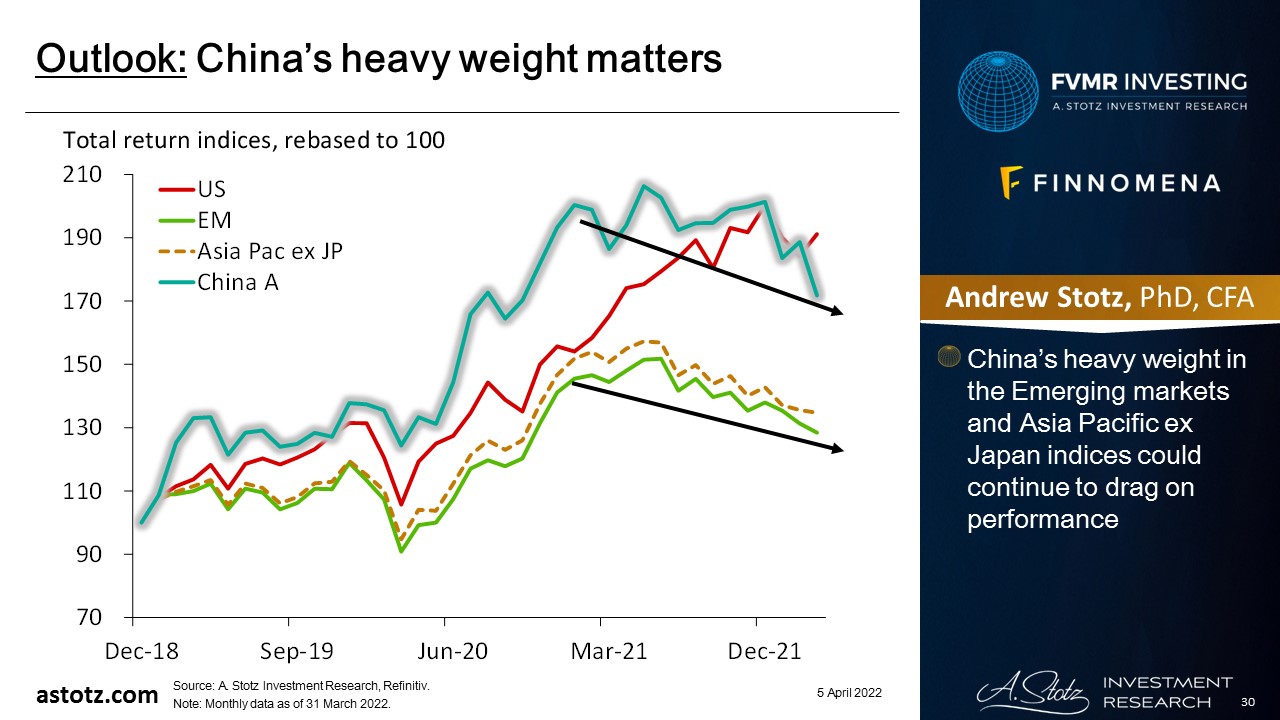

China’s heavy weight matters

- China’s heavy weight in the Emerging markets and Asia Pacific ex Japan indices could continue to drag on performance

Bonds to remain flat

- In the near term, we think bonds will underperform equity

- This is reflected in our 5% target allocation

- Our allocation is to the Thai money market, so a Fed rate hike should have little to no impact

- In addition, if we were to see rate hikes in Thailand, short-term paper is typically less negatively impacted due to shorter duration

Commodities set to go higher

- We have a 25% target allocation to Commodities

- Recovery demand, inflation, and supply-chain disruptions related and unrelated to the war in Ukraine are going to drive the asset class higher

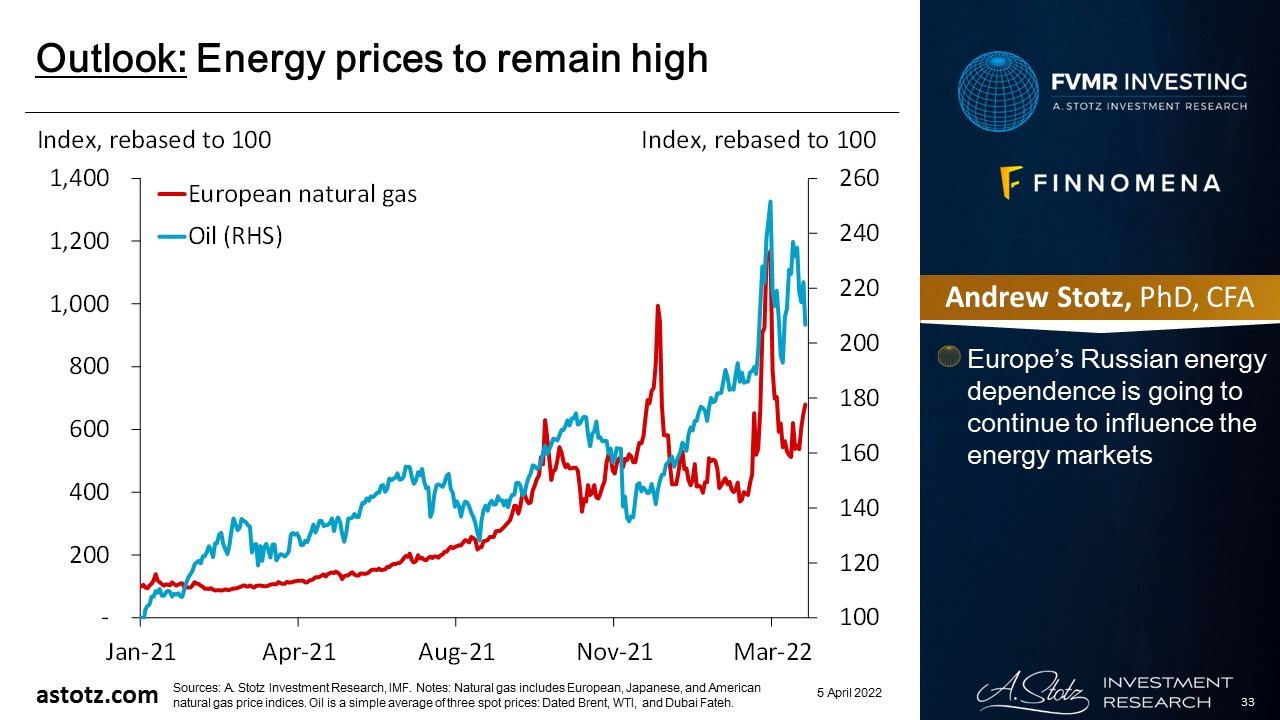

Energy prices to remain high

- Europe’s Russian energy dependence is going to continue to influence the energy markets

Ukraine war disrupts supply

- Besides energy, Russia is an exporter of many industrial metals, and Russia and Ukraine are both important exporters of soft commodities

- Putin’s move to avoid settlement in, for example, US$ or EUR is likely to be another disruption in the commodities markets

Metals prices are on the rise too

- Russia supplies almost 20% of global high-quality nickel used in EV batteries

- The precious metal palladium is mainly used in catalytic converters for cars, and the EU gets more than 40% of its supply from Russia

And food is getting more expensive

- Natural gas is used in fertilizer, and higher fertilizer costs lead to higher grain prices

- Also, Russia and Ukraine account for 15-20% of global supply of corn and wheat

- Corn is a primary input for feed grain of livestock and poultry, driving up meat prices

- Wheat is an important ingredient for bread, pasta, snack food, and cereals; Egypt and Turkey get more than 70% of total wheat imports from Russia and Ukraine

We keep gold as an insurance

- Target weight of 25% as an insurance

- The war in Ukraine spurs uncertainty, and Inflation expectations could rise, making gold attractive

- Though expected rate hikes and recession concerns are negative

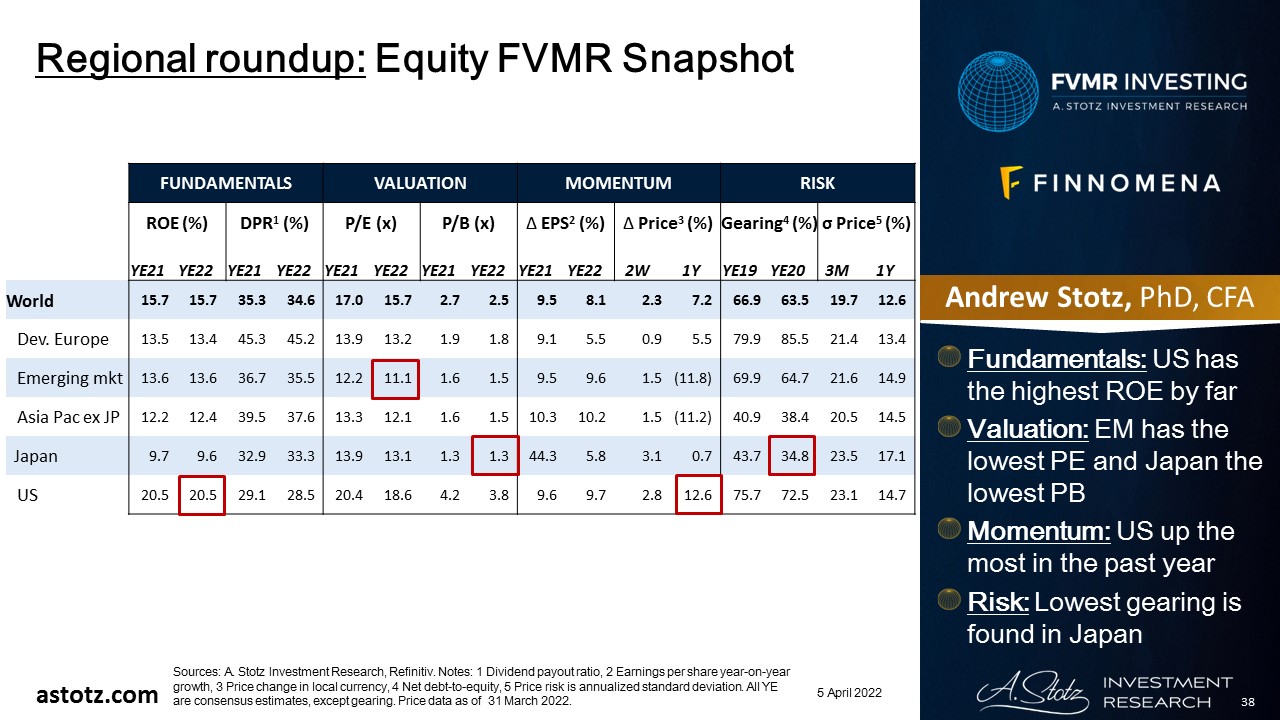

Regional Equity FVMR Snapshot

- Fundamentals: US has the highest ROE by far

- Valuation: EM has the lowest PE and Japan the lowest PB

- Momentum: US up the most in the past year

- Risk: Lowest gearing is found in Japan

Risks

Inflation quickly gets under control

- The strategy is still positioned to benefit from rising inflation at the beginning of 2022

- There’s a risk that inflation is transitory and falls faster than we expect, which could hurt our performance

- A quick resolution of the war in Ukraine would also likely lead to lower commodities and gold prices

Global recession pushing down stocks

- New Covid mutations could arise, leading to new shutdowns globally or in specific countries, which would be negative for the related equity markets

- We have started to see yield curve inversion, which has historically been an accurate predictor of recessions

- Since 1970 in the US, the average time from inversion until the recession started was about 12 months

Fed rate hikes crashing the US market

- If the Fed would surprise and not be cautious about rate hikes, it could impact the US stock market negatively

- The US stock market usually has a global impact; hence, it would hurt other equity markets too

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.