A. Stotz All Weather Strategy – June 2021

The All Weather Strategy slightly underperformed a traditional 60/40 portfolio in June 2021. Western economies continue to reopen, and we tilt our 65% target equity allocation to US and Developed Europe. Expect strong commodities demand from Western and Chinese recovery; target allocation at 25%.

The A. Stotz All Weather Strategy is Global, Long-term, and Diversified:

- Global – Invests globally, not only Thailand

- Long-term – Gains from long-term equity return, while trying to reduce a portion of losses during equity market downturns

- Diversified – Diversified globally across four asset classes

The All Weather Strategy is available in Thailand through FINNOMENA. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

Review

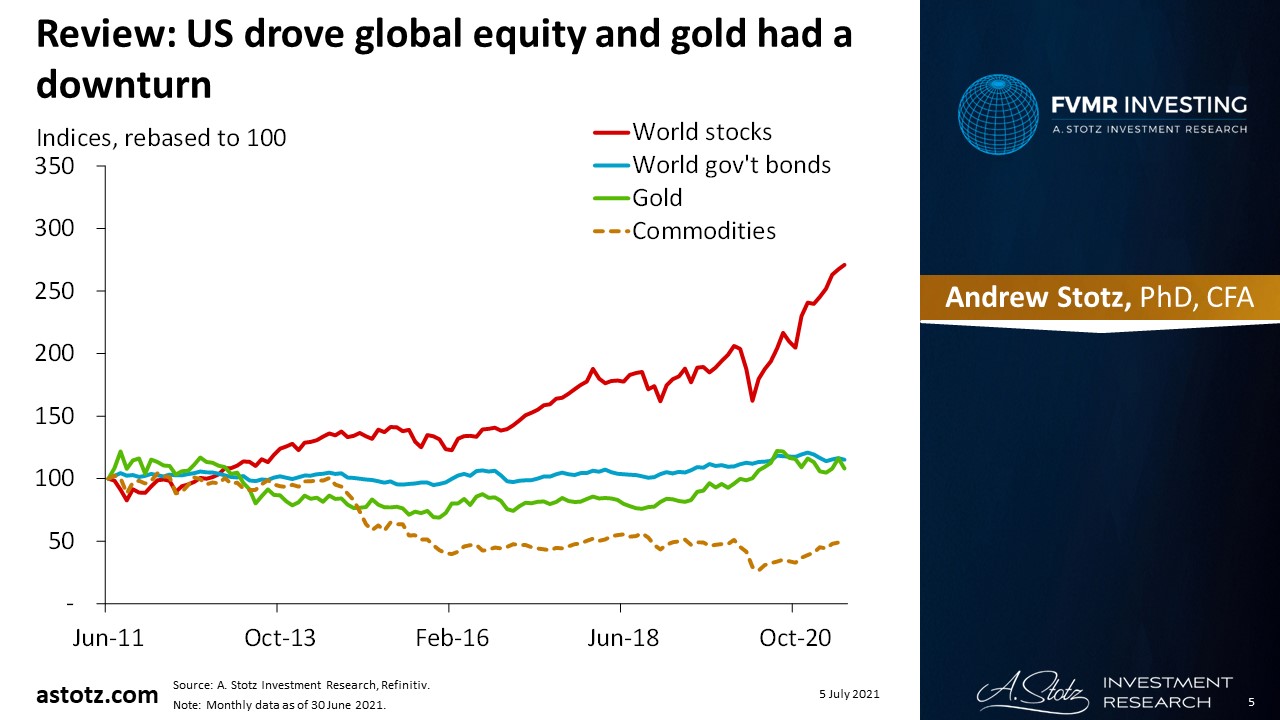

US drove global equity and gold had a downturn

Right call to switch into US equity

- In our latest revision, we switched our 25% equity allocations to the US and Developed Europe from Emerging markets and Asia Pacific ex Japan

- US was the best performer in June 2021, and we benefitted from this

- The US was driven by continued recovery expectations as vaccine rollouts have been rapid and the pandemic restrictions are eased

Developed Europe was flattish in June

- While Europe has faster vaccine rollouts than most Emerging and Asian markets, equities were slightly down in June

- Market worries about rising rates to stifle inflation and a stronger US dollar led to the relatively weak performance

- Our 25% target allocation didn’t help the return, but it didn’t harm it much either

Low bond target allocation at 5%

- We have a bond target allocation of 5% as they appeared less attractive relative to equity

- The strategy is to hold only Thai government bonds, rather than a mix of global government and corporate bonds

- Besides US and Emerging markets, other equities and commodities were down, hence, the flattish return of bonds was attractive

Commodities contracted in June

- Most energy commodities, led by natural gas and oil, performed strongly in June

- WTI crude oil closed June at US$73/bbl

- Industrial and precious metals were weak

- Agricultural commodities were mixed, cattle were up while wheat and soybeans were down, and corn price was flattish

- The US dollar strengthened in June; a stronger dollar typically means lower commodity prices

Gold price was hit hard in June

- We have a minimum 5% allocation to gold

- It was a correct call as gold price suffered a significant 8% loss and closed the month at US$1,770/oz t

- Though, we were also slightly hit by it through our 25% commodities allocation

- As with general commodities, a stronger US dollar was negative for the gold price

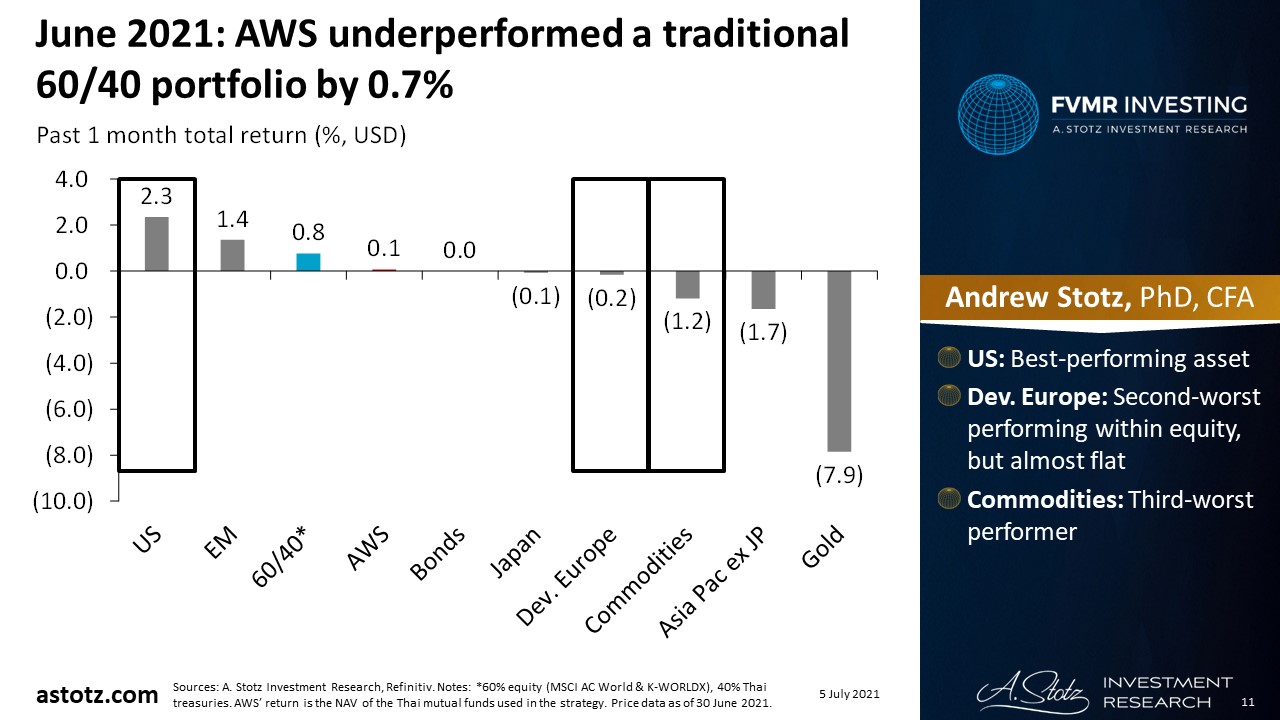

June 2021: The All Weather Strategy underperformed a traditional 60/40 portfolio by 0.7%

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- US: Best-performing asset

- Developed Europe: Second-worst performing within equity, but almost flat

- Commodities: Third-worst performer

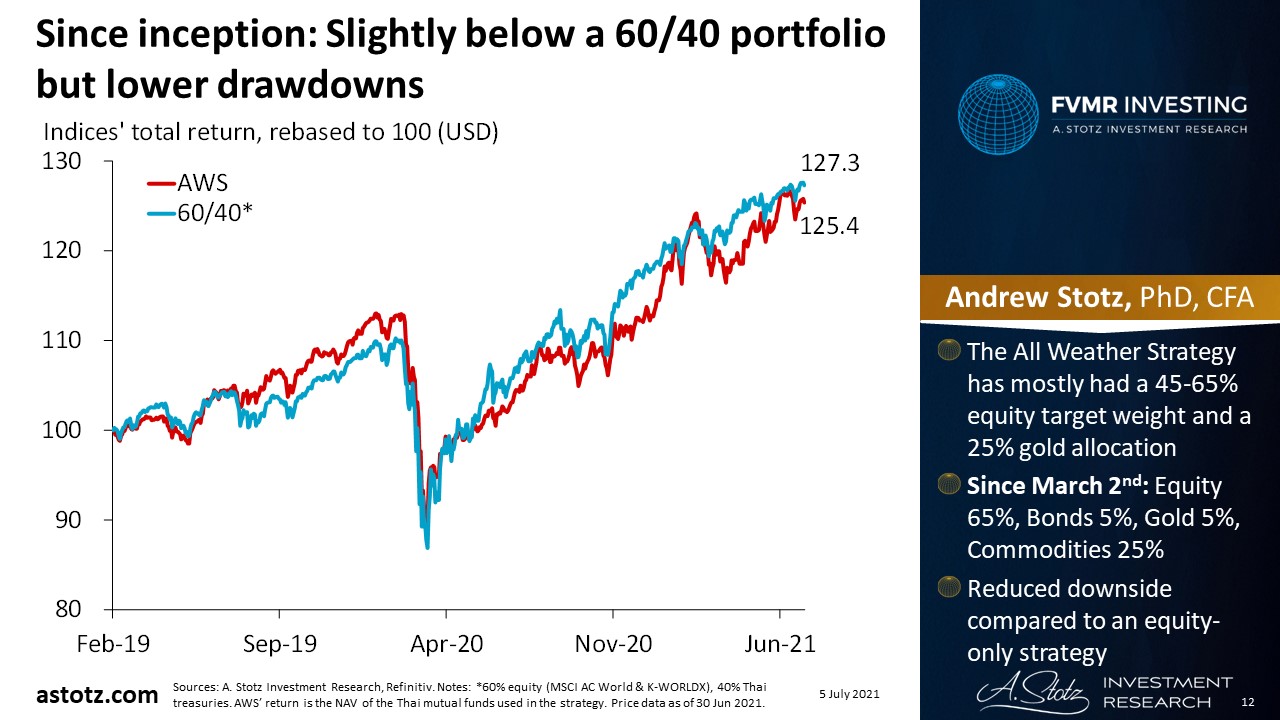

Since inception: Slightly below a 60/40 portfolio but lower drawdowns

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- The All Weather Strategy has mostly had a 45-65% equity target weight and a 25% gold allocation

- Since March 2nd: Equity 65%, Bonds 5%, Gold 5%, Commodities 25%

- Reduced downside compared to an equity-only strategy

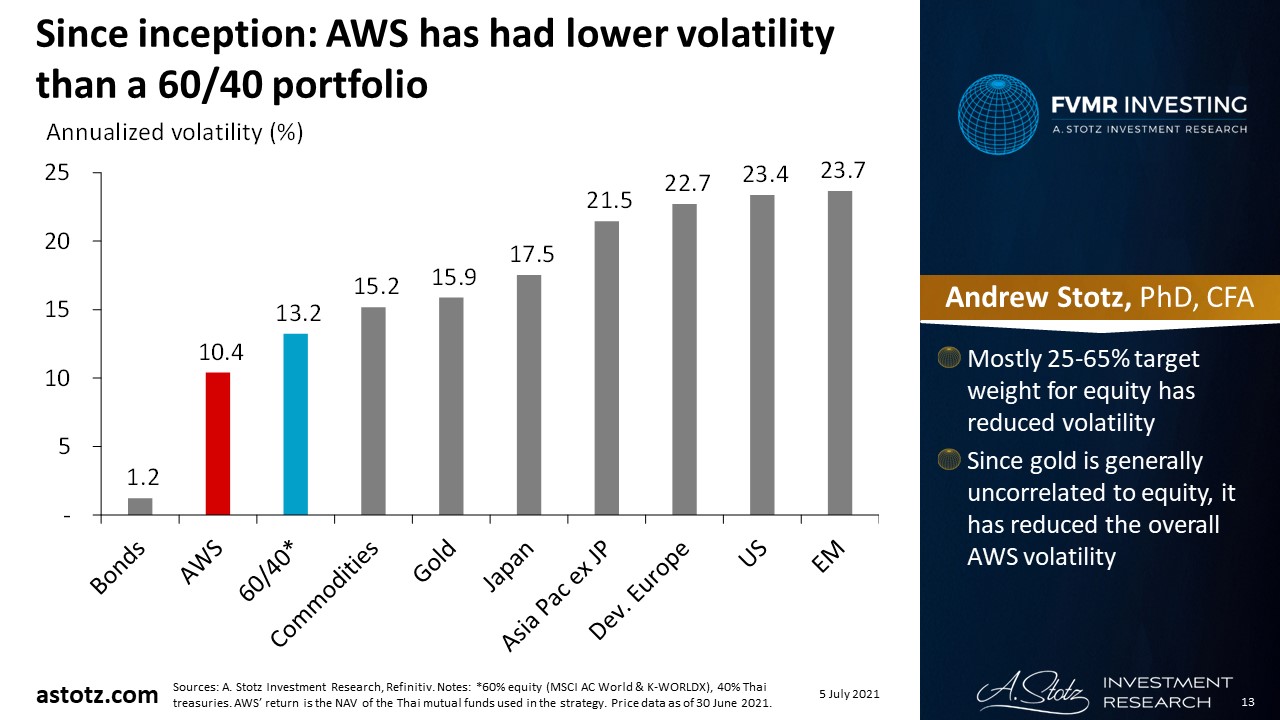

Since inception: The All Weather Strategy has had lower volatility than a 60/40 portfolio

- Mostly 25-65% target weight for equity has reduced volatility

- Since gold is generally uncorrelated to equity, it has reduced the overall strategy’s volatility

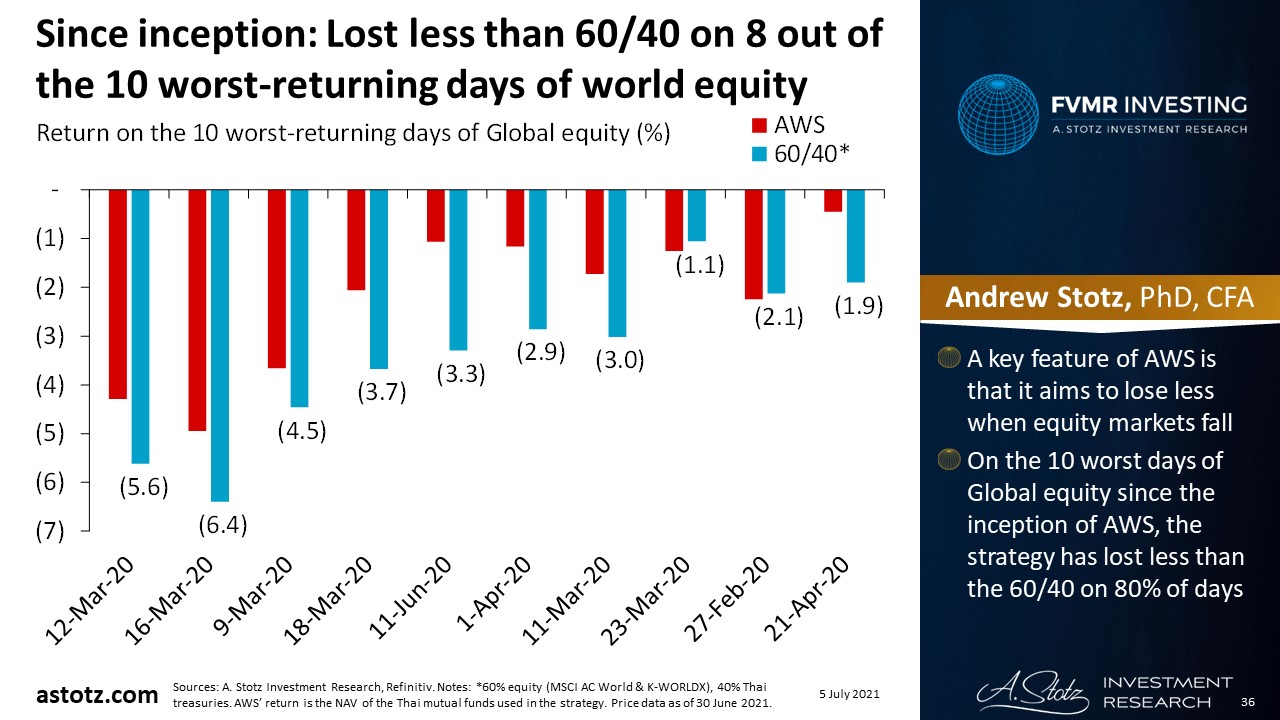

Since inception: The All Weather Strategy has lost less than a 60/40 portfolio on 8 out of the 10 worst-returning days of world equity

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- A key feature of the All Weather Strategy is that it aims to lose less when equity markets fall

- On the 10 worst days of Global equity since the inception of the All Weather Strategy, the strategy has lost less than the 60/40 portfolio on 80% of days

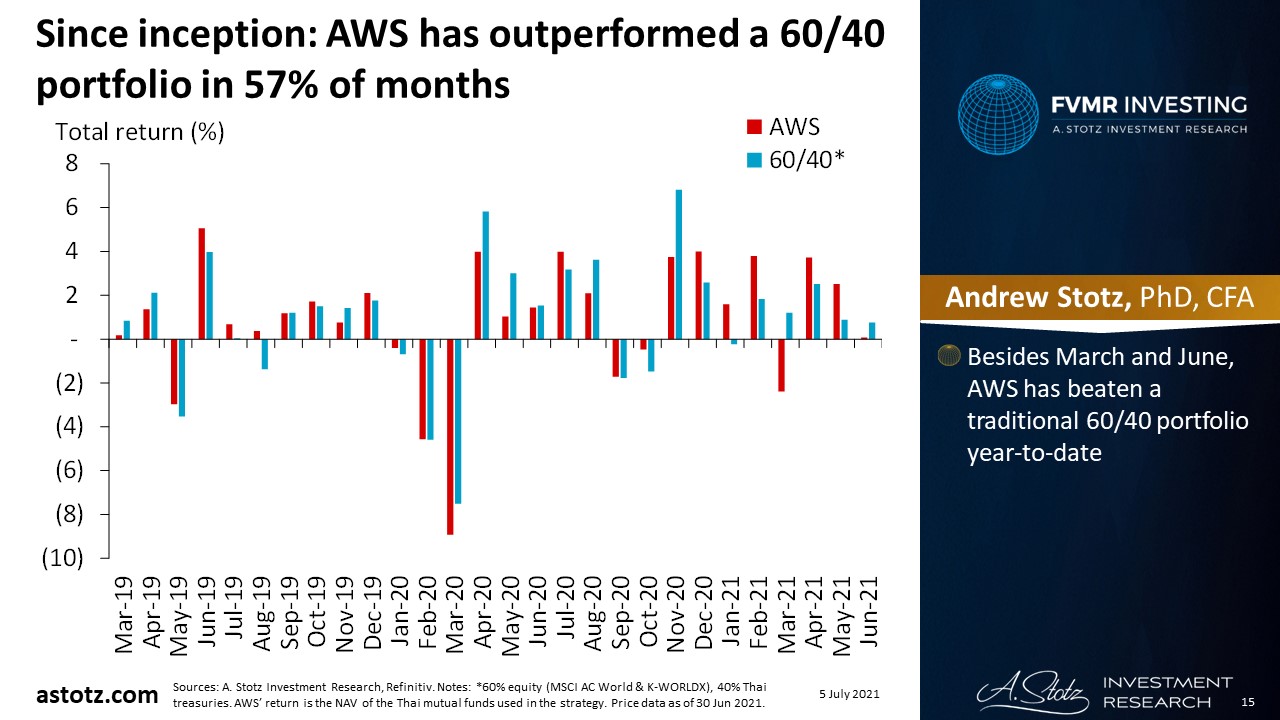

Since inception: The All Weather Strategy has outperformed a 60/40 portfolio in 57% of months

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- Besides March and June, the All Weather Strategy has shown a solid year-to-date performance relative to the traditional 60/40 portfolio

Outlook

Strong recovery in the West

- Western economies continue to reopen, while Emerging and Eastern markets are still behind on vaccine rollouts

- Company earnings in the US have surprised on the upside, supporting the recovery theme

European markets to benefit from the value factor

- Developed Europe has lagged a bit in terms of recovery

- Value and cyclical stocks are constituting more of the stock markets in Europe vs. the US

- Within equity value stocks can be more attractive in times of rising inflation

Central banks to let economies run hot

- The Fed and ECB are willing to overshoot their inflation targets due to undershooting for a long time

- This should allow stocks to run further

Delayed recovery in Asia ex China

- Besides China, Asia is still seeing rising cases in many countries and slow vaccine rollouts

- There is also a risk that the new Delta variant of the virus could scare governments to shut down further

We still expect a continued recovery in the Chinese economy

- Chinese gov’t intervention in the Tech industry and concerns about tighter monetary policy has weighed on the Emerging markets index

- Together with the recovery in the West, the Chinese recovery should support commodities demand

Bonds to remain weak

- As we’re expecting rising inflation, we expect bonds to underperform

- This is reflected in our 5% target allocation

Energy and industrial metals should perform well

- If the outcome of the OPEC+ meeting leads to a production increase below market expectations, oil price could run further

- Industrial metals should benefit from the post-shutdown recovery in the West and China

Short-term gold outlook remains weak

- In the longer term, as the inflation narrative spreads, it could lead to expectations of negative real rates

- Which should support the gold price

- However, in the shorter run, economic recovery leads to “risk on” and makes gold less attractive

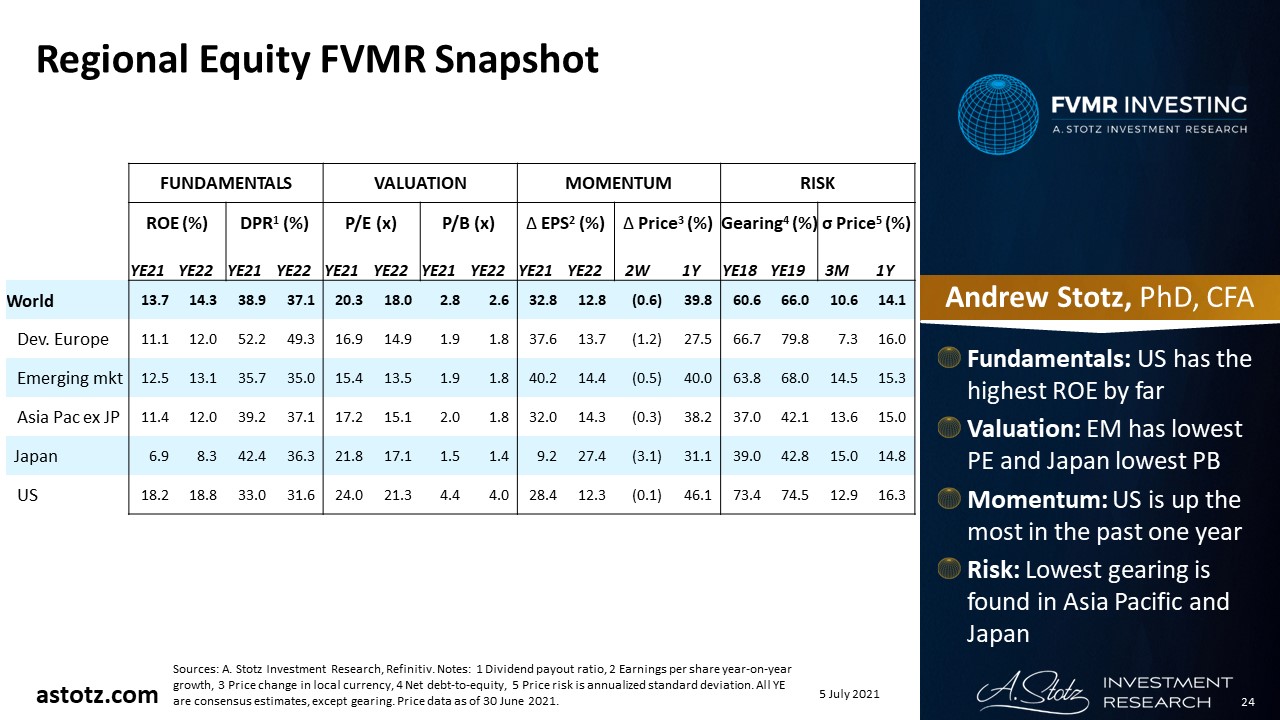

Regional Equity FVMR Snapshot

- Fundamentals: US has the highest ROE by far

- Valuation: Emerging markets have the lowest PE and Japan lowest PB

- Momentum: US is up the most in the past one year

- Risk: Lowest gearing is found in Asia Pacific and Japan

Risks

Inflation turns out transitory

- The All Weather Strategy is positioned to benefit from rising inflation

- There’s a risk that inflation is transitory, which could hurt our performance

- Besides, return expectations in inflationary environments are based upon corresponding rising interest rates

- But the Fed and ECB are expected to keep rates low at least until late 2022

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.