A. Stotz All Weather Strategy – January 2020

The All Weather Strategy has slightly underperformed World equity in terms of return but at a much lower risk. Equity has some near-term support, and we have a 65% target allocation; Japan is overweight. Continued geopolitical tensions and coronavirus outbreak make us continue to like gold.

The A. Stotz All Weather Strategy is Global, Long-term, and Diversified:

- Global – Invests globally, not only Thailand

- Long-term – Gains from long-term equity return, while trying to reduce a portion of losses during equity market downturns

- Diversified – Diversified globally across four asset classes

The All Weather Strategy is available in Thailand through FINNOMENA. Please note that this post is not investment advice and should not be seen as recommendations. Also, remember that backtested or past performance is not a reliable indicator of future performance.

Review

Coronavirus has been a drag on equity markets

- Equity remains at high valuations, and fundamentals appear to have peaked

- Since our December 2019 revision, we have 25% target allocations to gold, US equity, and Japan equity

- In January, the coronavirus led to falling equity markets almost across the board as it spurred worries about a global growth slowdown

- US and Japan performed the best though

Increased uncertainty pushed up gold

- Commodities January performance reflected the virus outbreak in the world’s second-largest economy as well; oil and industrial metals fell as growth outlook worsened

- Increased uncertainty led investors to “safe-haven assets,” and gold performed well

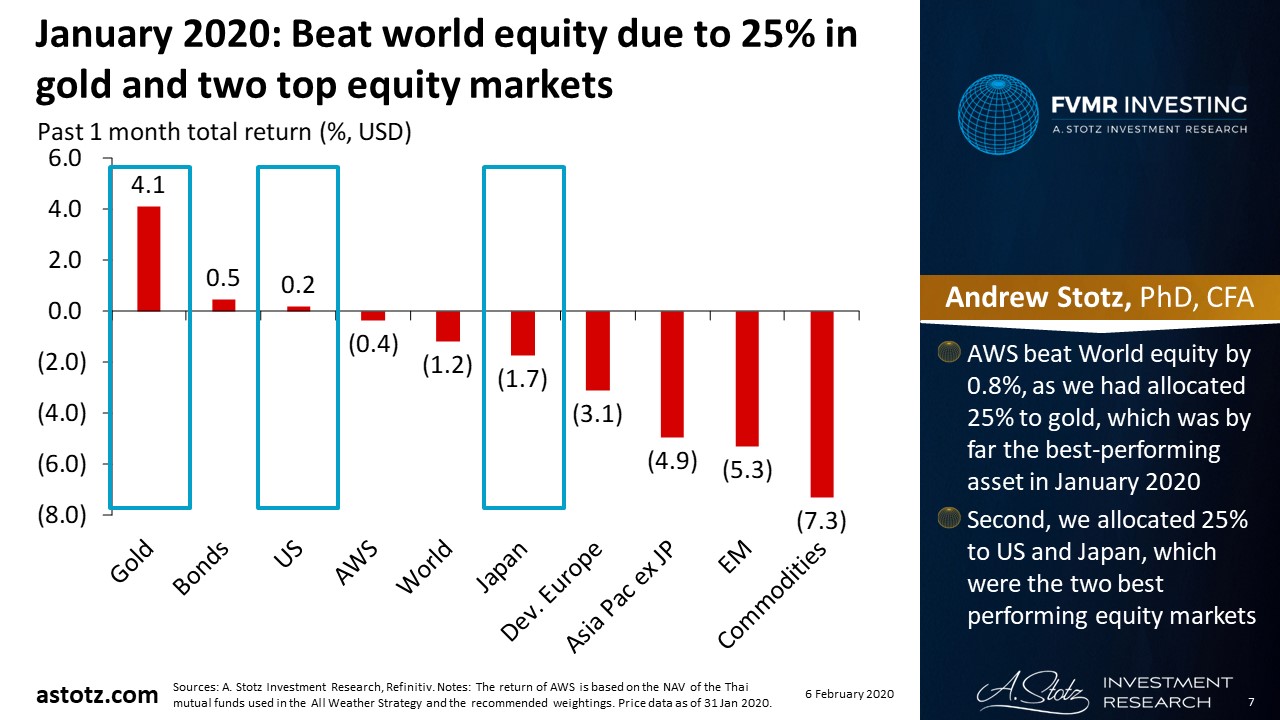

January 2020: Beat world equity due to 25% in gold and two top equity markets

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- The A. Stotz All Weather Strategy beat World equity by 0.8%, as we had allocated 25% to gold, which was by far the best-performing asset in January 2020

- Second, we allocated 25% to US and Japan, which were the two best performing equity markets

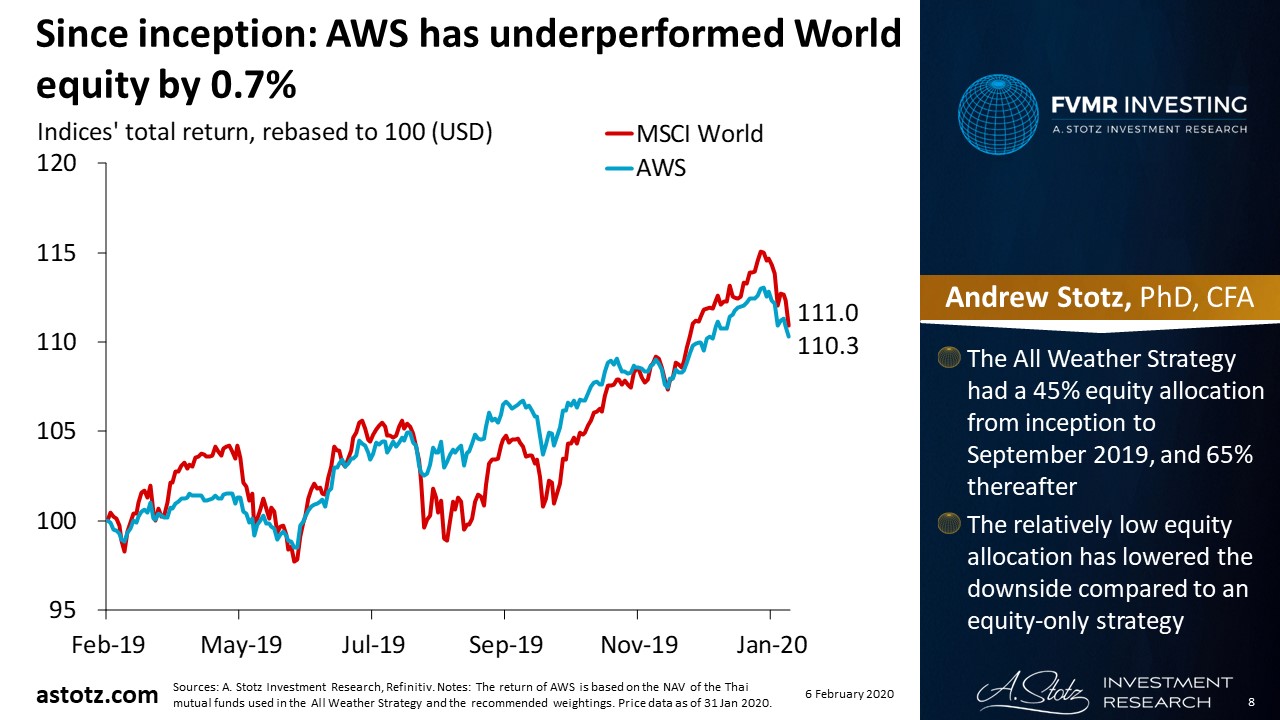

Since inception: The A. Stotz All Weather Strategy has underperformed World equity by 0.7%

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- The All Weather Strategy had a 45% equity allocation from inception to September 2019, and 65% thereafter

- The relatively low equity allocation has lowered the downside compared to an equity-only strategy

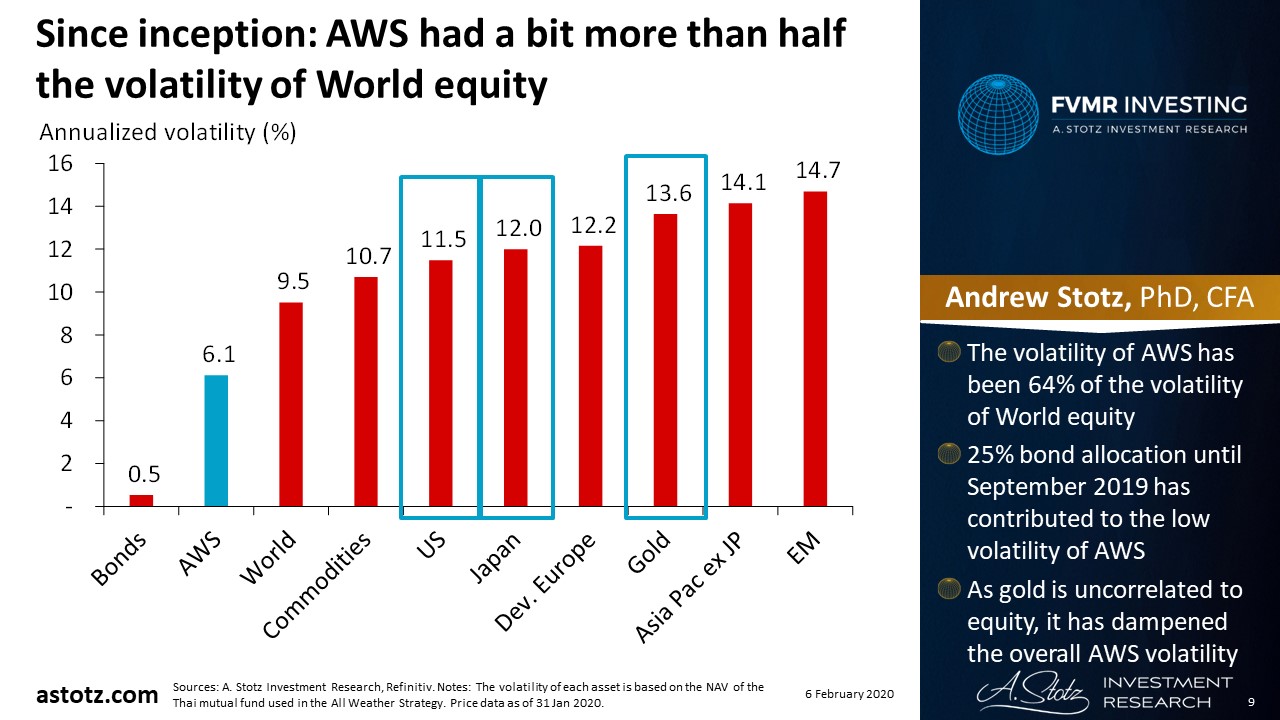

Since inception: All Weather Strategy had a bit more than half the volatility of World equity

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- The volatility of the All Weather Strategy has been 64% of the volatility of World equity

- 25% bond allocation until September 2019 has contributed to the low volatility

- As gold is uncorrelated to equity, it has dampened the overall volatility in the strategy

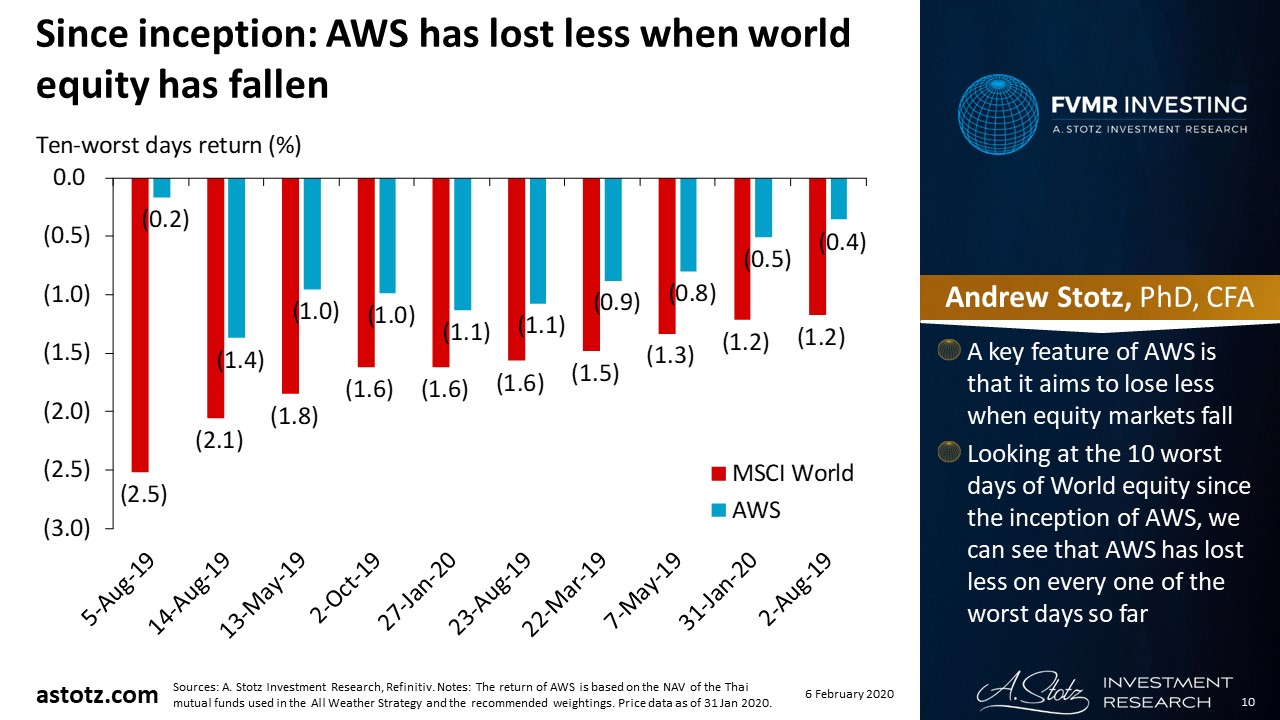

Since inception: The All Weather Strategy has lost less when world equity has fallen

Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

- A key feature of the All Weather Strategy is that it aims to lose less when equity markets fall

- Looking at the 10 worst days of World equity since the inception of the All Weather Strategy, we can see that the strategy has lost less on every one of the worst days so far

Outlook

US market gets closer to peak

- US gov’t debt and currency issues

- Positive for gold, risk for US market

- Further rate cuts in the US might not come, and if any, it’s expected by the end of 2020

- About 65% chance of a cut in September 2020

- Low bond yields and US presidential election to support higher-risk equities in 2020

- Looking at corporates, fundamentals appear to have peaked which could lead to limited upside in equity

US tensions with China and Iran remain but somewhat muted at the moment

- “Phase one” US-China trade deal should support strong equity performance in the near term

- Though, a “phase one” US-China trade deal doesn’t mean the trade war is over; and uncertainty will continue

- US killing of a top Iranian commander and Iran’s retaliation didn’t lead to an escalation in the conflict, but tensions remain

Coronavirus raises uncertainty about global growth; gold can protect the downside

- If China can’t contain the coronavirus and it spreads to other countries, the global growth outlook could rapidly worsen

- Already, it is disrupting global demand, supply chains, and tourism

- Geopolitical tensions and the coronavirus are negatives for the global growth outlook, and equity; likely that investors continue to switch to “safe-haven assets,” in the near term

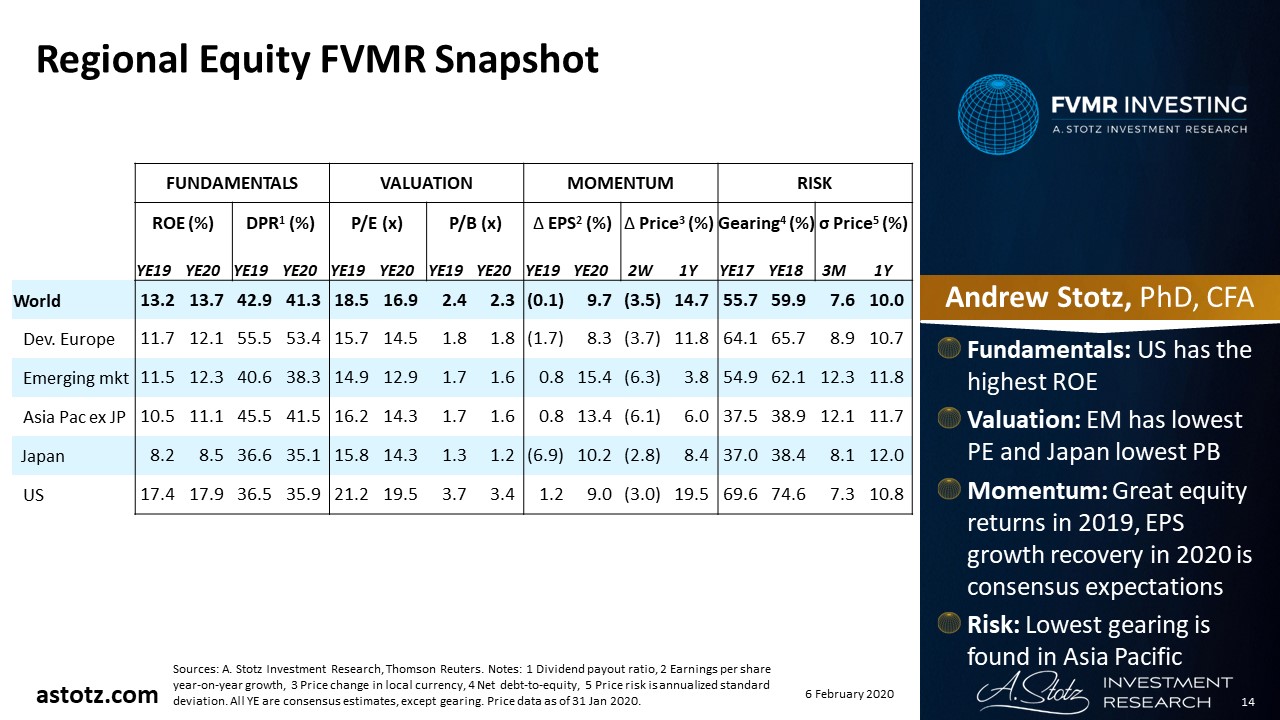

Regional Equity FVMR Snapshot

- Fundamentals: US has the highest ROE

- Valuation: EM has the lowest PE and Japan lowest PB

- Momentum: Great equity returns in 2019, EPS growth recovery in 2020 is consensus expectations

- Risk: Lowest gearing is found in the Asia Pacific

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.