Will Pressure on Kohl’s Management Drive Share Price?

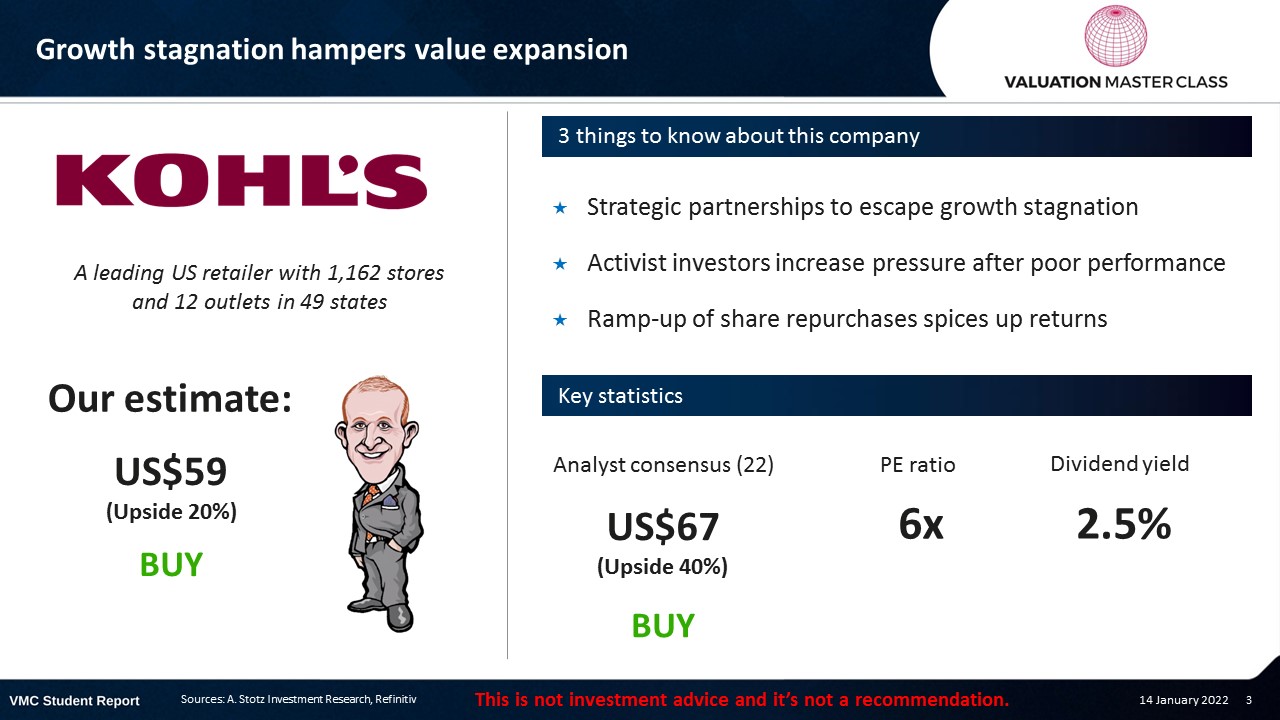

Growth stagnation hampers value expansion

The post was originally published here.

Highlights:

- Strategic partnerships to escape growth stagnation

- Activist investors increase pressure after poor performance

- Ramp-up of share repurchases spices up returns

Download the full report as a PDF

Price signal unclear, volume is bearish

- Share price has been flat for years

- Recently, the 50 DMA has fallen below the 200 DMA

- Both lines converged leaving an unclear signal

- The RSI-Volume stayed below the 50%-line which suggest a bearish signal

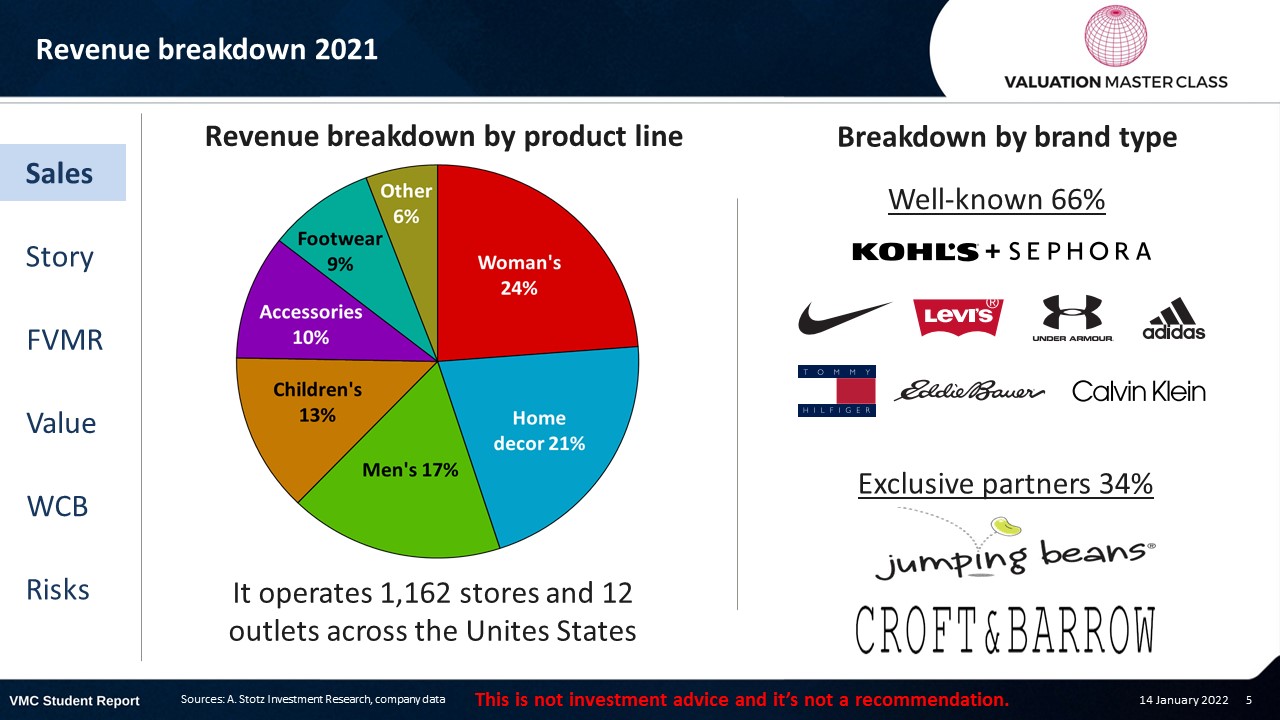

Kohl’s revenue breakdown 2021

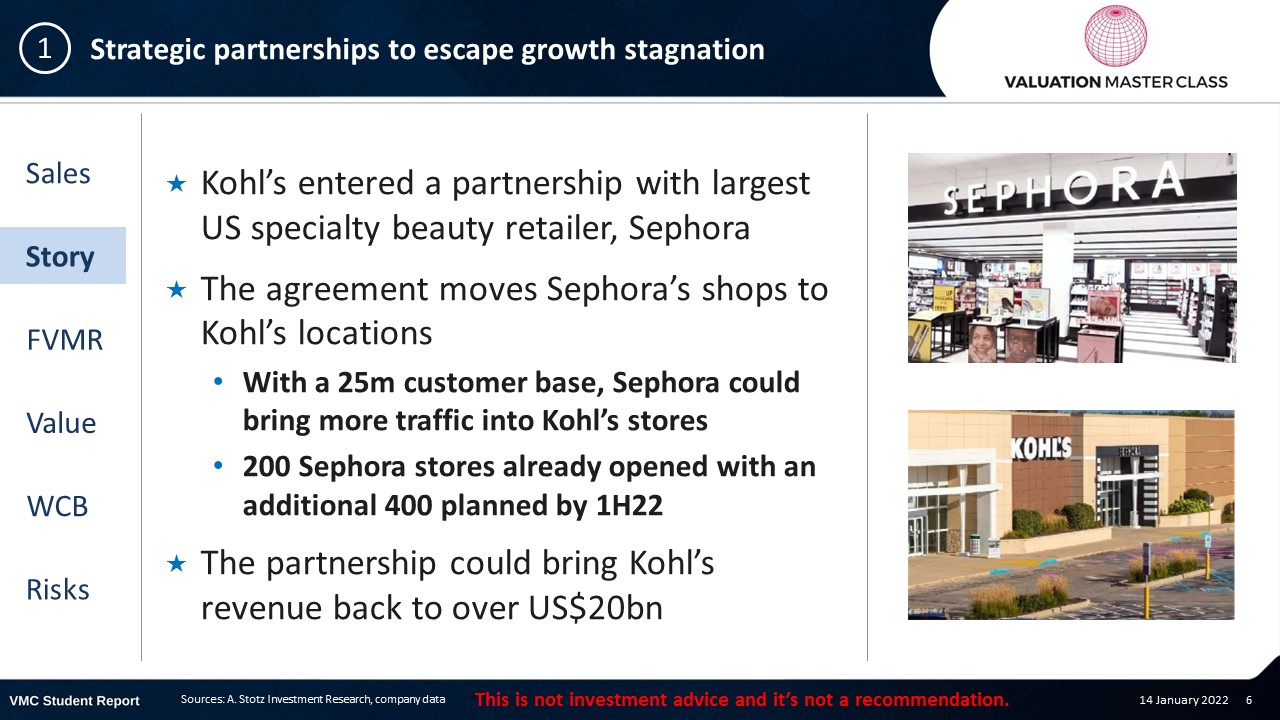

Strategic partnerships to escape growth stagnation

- Kohl’s entered a partnership with largest US specialty beauty retailer, Sephora

- The agreement moves Sephora’s shops to Kohl’s locations

- With a 25m customer base, Sephora could bring more traffic into Kohl’s stores

- 200 Sephora stores already opened with an additional 400 planned by 1H22

- The partnership could bring Kohl’s revenue back to over US$20bn

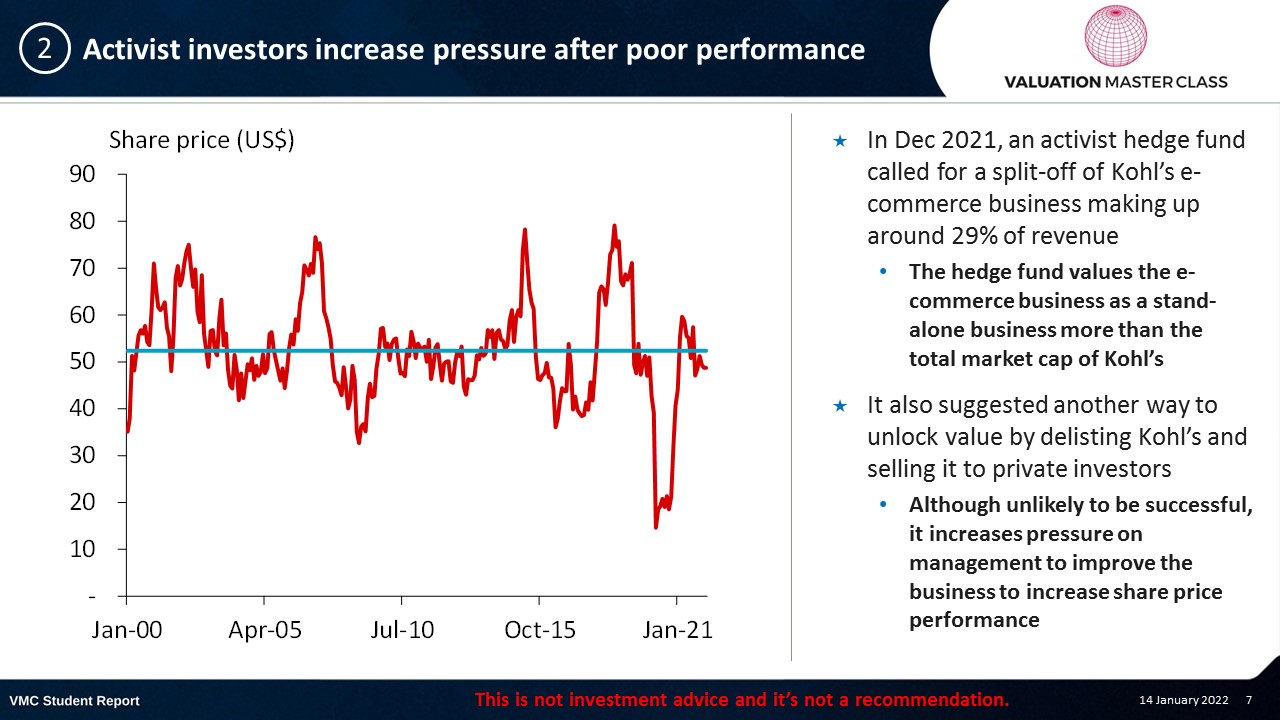

Activist investors increase pressure after poor performance

- In Dec 2021, an activist hedge fund called for a split-off of Kohl’s e-commerce business making up around 29% of revenue

- The hedge fund values the e-commerce business as a stand-alone business more than the total market cap of Kohl’s

- It also suggested another way to unlock value by delisting Kohl’s and selling it to private investors

- Although unlikely to be successful, it increases pressure on management to improve the business to increase share price performance

What is an activist investor?

- Activist investors are an individual or group of investors with a significant stake in a company, who aim to influence or make material changes to how the business is run. Changes like:

- Board composition

- Share repurchases and dividends

- Advancing ESG issues

- Privatization of the business

- Spin-off of business segments

- Divestitures of inefficient segments

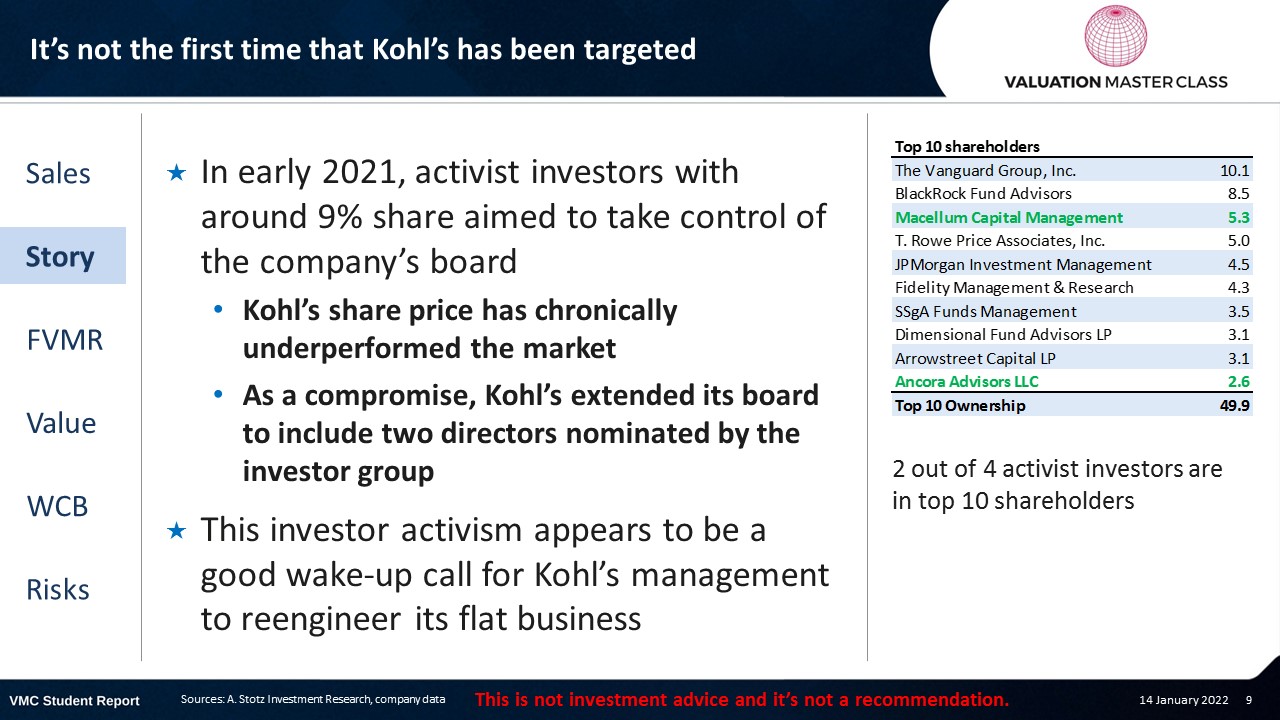

It’s not the first time that Kohl’s has been targeted

- In early 2021, activist investors with around 9% share aimed to take control of the company’s board

- Kohl’s share price has chronically underperformed the market

- As a compromise, Kohl’s extended its board to include two directors nominated by the investor group

- This investor activism appears to be a good wake-up call for Kohl’s management to reengineer its flat business

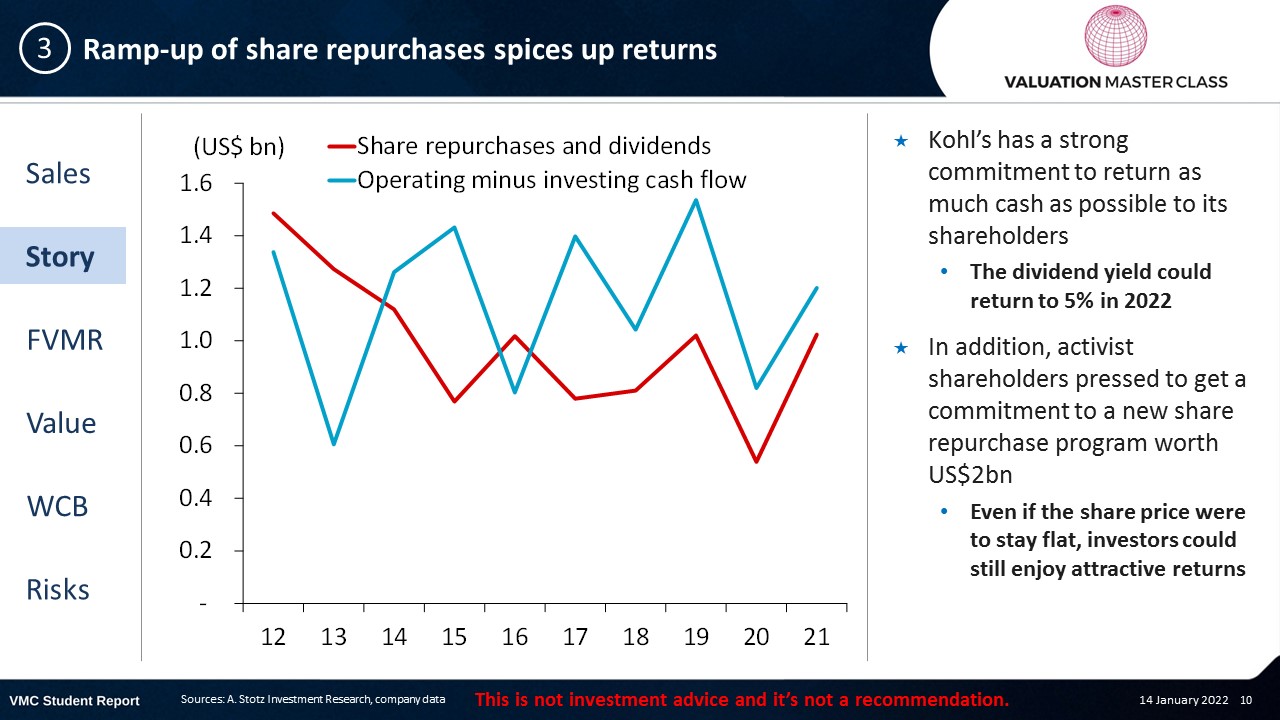

Ramp-up of share repurchases spices up returns

- Kohl’s has a strong commitment to return as much cash as possible to its shareholders

- The dividend yield could return to 5% in 2022

- In addition, activist shareholders pressed to get a commitment to a new share repurchase program worth US$2bn

- Even if the share price were to stay flat, investors could still enjoy attractive returns

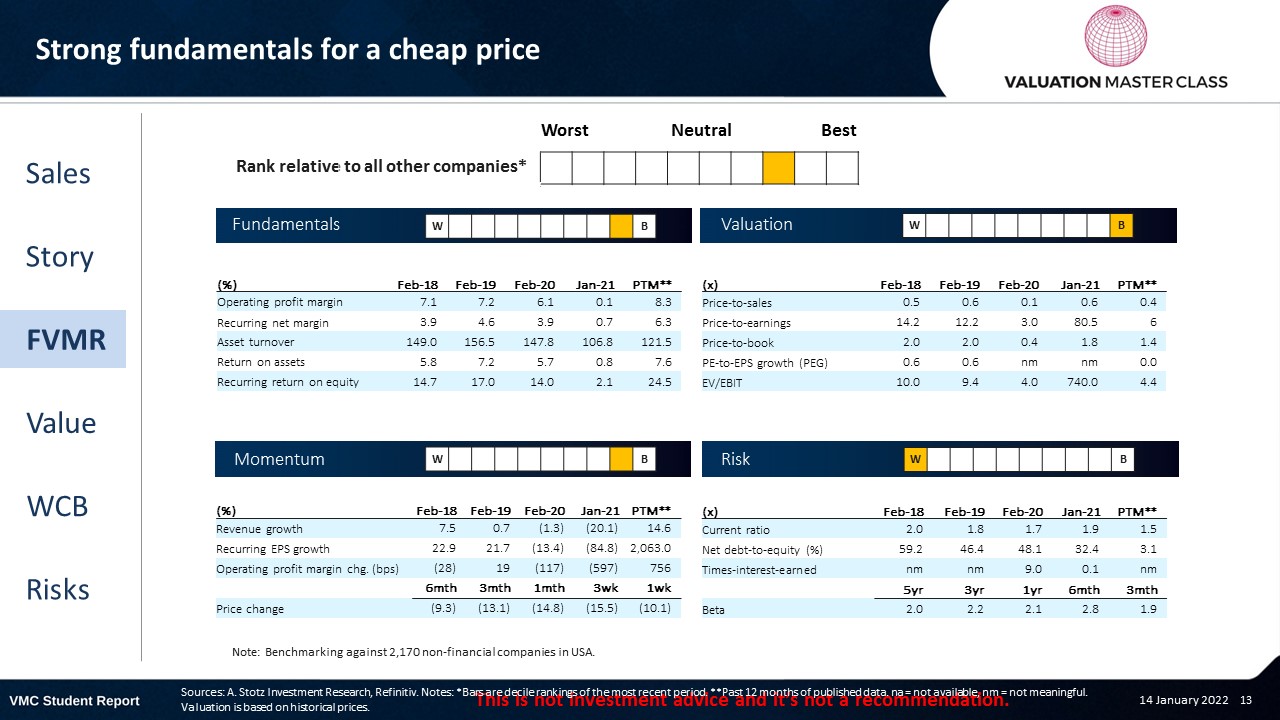

FVMR Scorecard – Kohl’s

- A stock’s attractiveness relative to stocks in that country or region

- Attractiveness is based on four elements

- Fundamentals, Valuation, Momentum, and Risk (FVMR)

- Scale from 1 (Best) to 10 (Worst)

Consensus remains cautious but sees upside

- Most analysts still have HOLD recommendations

- The poor share price performance over the past two decades has made analysts skeptical

- They forecast that the increased profit margin is likely to fade over the next two years

Get financial statements and assumptions in the full report

P&L – Kohl’s

- Net profit has a strong rebound and exceeds its pre-pandemic level

- The strong bottom-line is mainly driven by the margin expansion

Balance sheet – Kohl’s

- As of 2021, the company holds a record US$2bn in cash which it will distribute to its shareholders over time

- The company continues its massive share repurchase program which is the main driver of increasing EPS over time

Cash flow statement – Kohl’s

- Strong operating cash flow allows the company to pay out dividends which are in line with its pre-pandemic policy

- We expect that the dividend yield over the near-term to range between 5-6% like in 2019 and 2020

Ratios – Kohl’s

- After the revenue rebound in 22E, we assume revenue growth to normalize

- Going forward, we see poor revenue growth potential between 2-3%

- EBIT margin expansion in 22E probably only short-lived

- Going forward, we see the EBIT margin to range between 7-8%

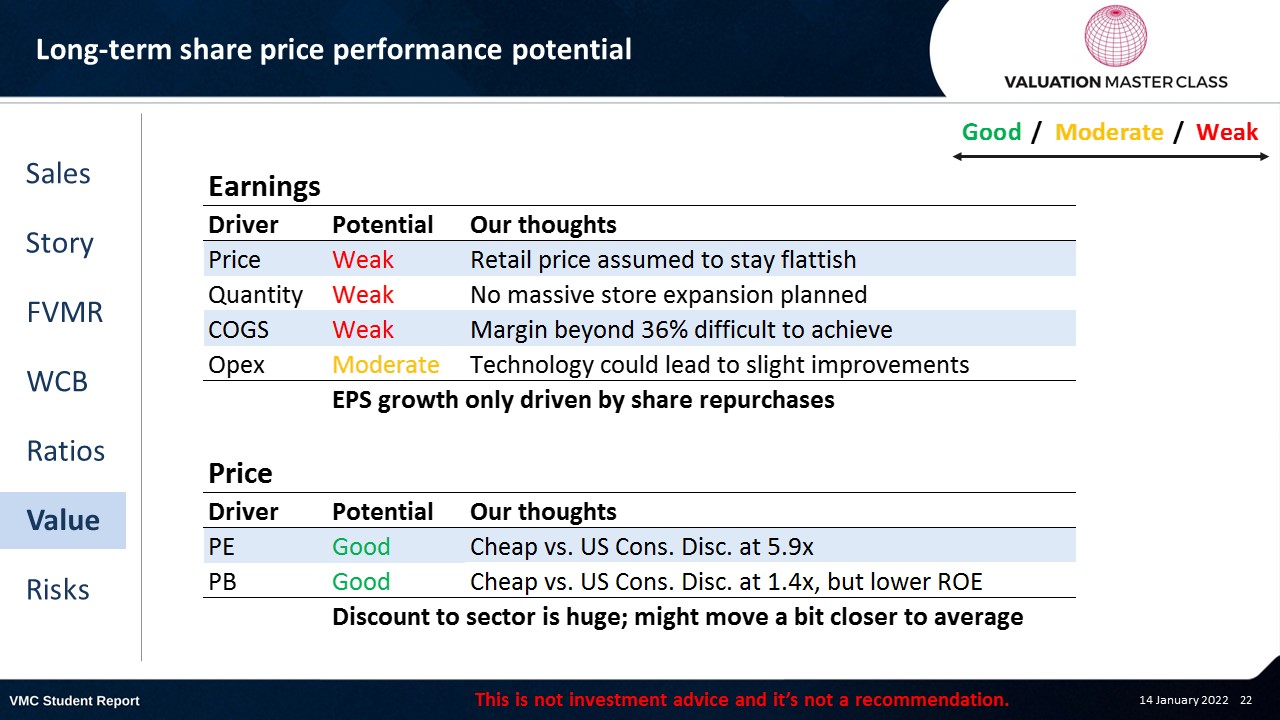

Long-term share price performance potential

Free cash flow – Kohl’s

- Strong cash flow generation is crucial for returning cash to shareholders

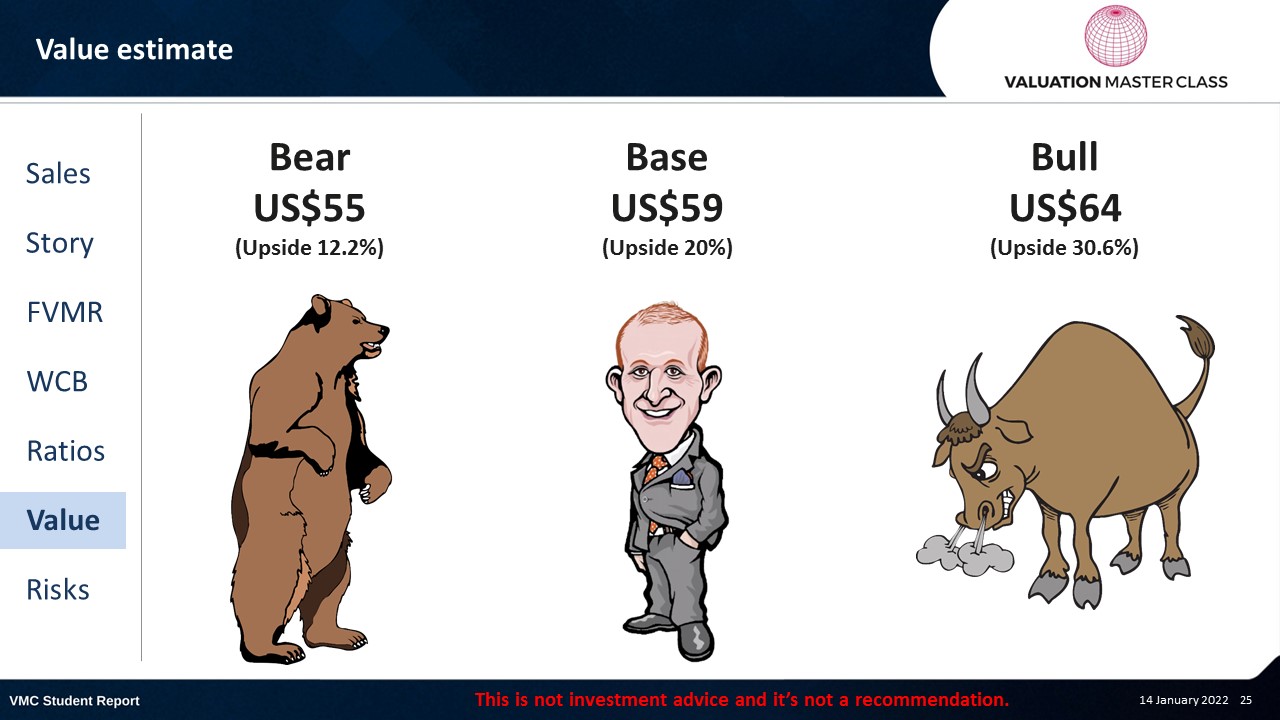

Value estimate – Kohl’s

- Like consensus, we expect a slightly stronger margin compared to the past

- The revenue growth CAGR is distorted by growth rebound in 2022

- Expect lower growth 23E onward

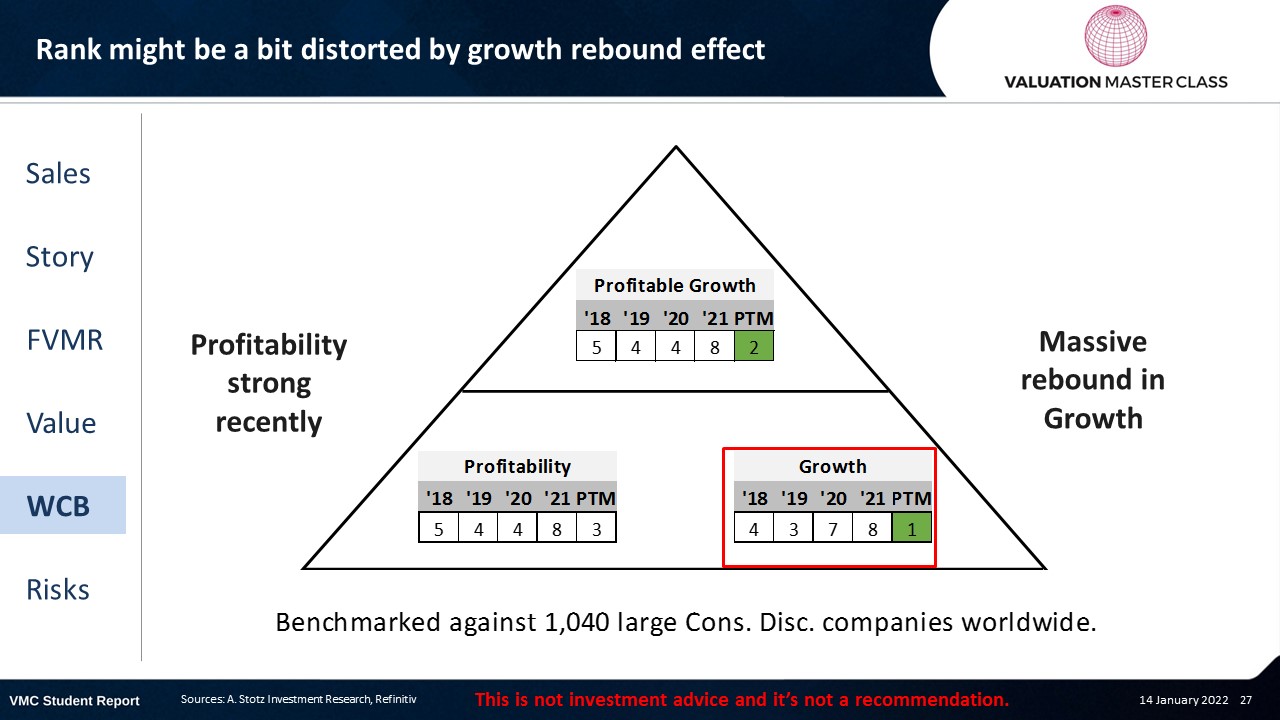

World Class Benchmarking Scorecard – Kohl’s

- Identifies a company’s competitive position relative to global peers

- Combined, composite rank of profitability and growth, called “Profitable Growth”

- Scale from 1 (Best) to 10 (Worst)

Key risk is falling behind in online sales

- Activist investors might not decide in favor of the long-term future

- Increased transportation costs and worsening of inventory management

- Failure to keep up with e-commerce could lead to lost of market share

Conclusions

- Don’t expect high growth, but price discount offers upside

- Intervention of activist investors could be accretive

- Attractive dividend yield and share repurchase program can be satisfying enough

Download the full report as a PDF

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.