Learning Valuation: PTT Global Chemical

Disclaimer:

This example was created on January 24, 2016. This is NOT a valuation, forecast, rating, or recommendation; rather, it is a teaching example. What follows is NOT investment advice; rather, it is a teaching example. It is intended only as academic information to those who want to learn about valuation. It should not be construed as the basis for any valuation or investment. The information in this presentation came from various sources which we believe are reliable, though we do not guarantee the accuracy, adequacy or completeness of such information. We hope you enjoy learning about valuation as much as we do!

Background

PTT Global Chemical Public Company Limited is a 49%-owned subsidiary of PTT PCL (PTT TB).

It is Thailand’s largest fully integrated petrochemical and chemical company operating in refinery, olefins and aromatics business accounting for 34%, 33% and 20% of the company’s revenue respectively.

PTTGC’s refinery business contributes 34% of revenue, and it is a leading petroleum refiner in Thailand, supplying refined petroleum products such as LPG.

Its olefins business contributes 33% of its revenue. The business manufactures and distributes olefin products using natural gas and naphtha as its feedstock.

Aromatics products are used to make automotive and electronic parts, clothing and food packaging, and they generate 20% of revenue.

Forecast

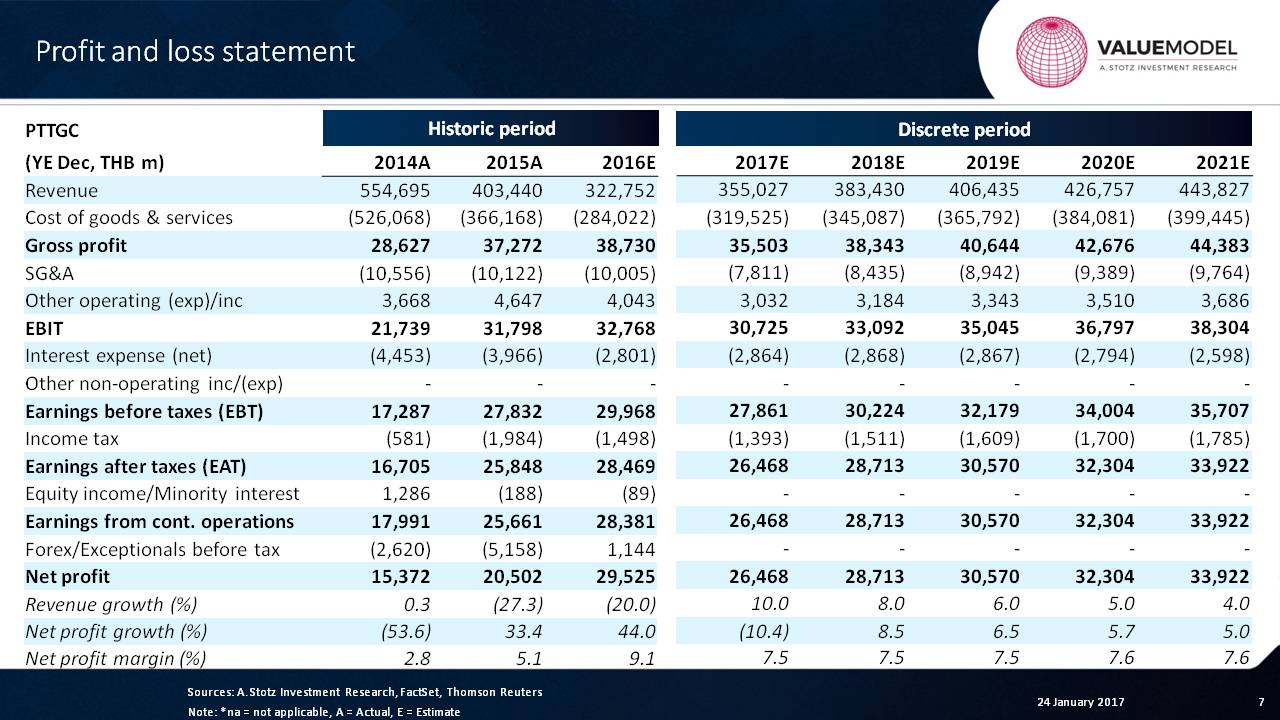

We have to first create a forecast if we want to value any company. So let’s take a look at the forecast that we have right here.

First of all, what we can see is that because this is an energy-related company, it can be very volatile. In fact, it sometimes has a falling revenue, as we can see revenue growth is negative.

Most companies are going to go up steadily in their revenue projections. But in this case, it’s a cyclical company, which means that the revenue can eventually come up as we see right here.

However, you’re going to face a problem with forecasting the revenue of a cyclical company.

If we say that the revenue of a cyclical company is going to go up, then down, then down again, and then up, should we continue this cycle as we forecast throughout the years or should we try to get some kind of average?

My answer is that you can never really predict these cycles. Therefore, it’s probably best to just go with an average knowing that this company over time could be above the average or below the average.

Assets

Now, we can see that the net profit margin recovers here and we’re going to hold it flat again because we’ve kept things flat in the overall company.

You’ve already learned something there about the cyclicality and what to do about it.

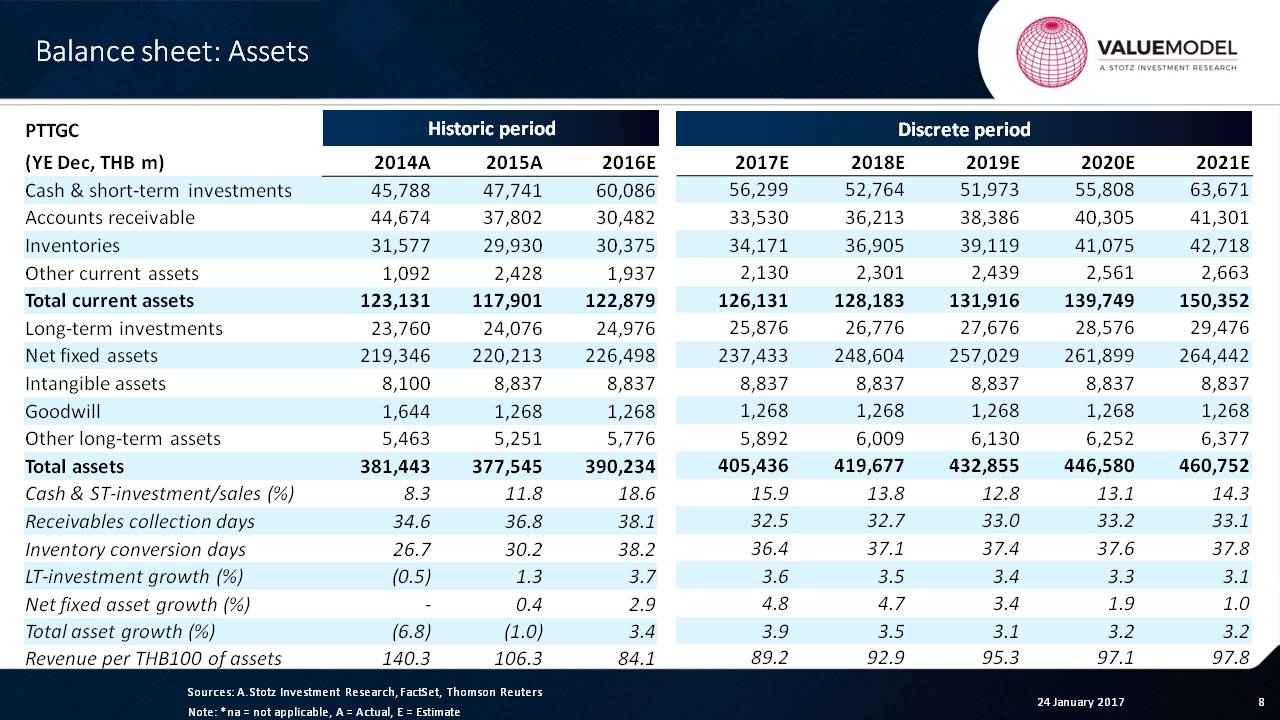

What we can see here is that our growth assumptions are pretty low on the asset side and we’re not expecting major changes in the asset turnover which you can see going from 89 to 98 or so.

Liabilities and Equity

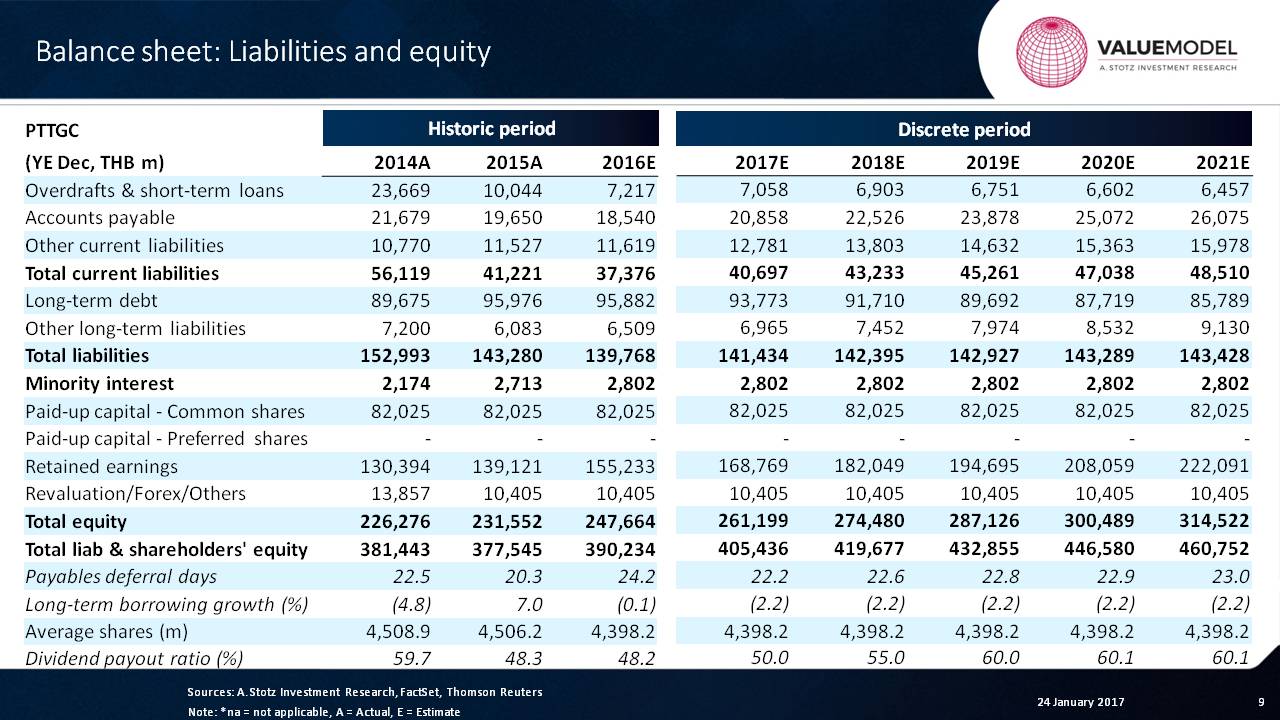

From a borrowing perspective, the company has borrowed less and less. This is short-term borrowing. We’re going to keep that relatively stable.

The long-term borrowing of the company has been maintained pretty steadily, and then we’re going to have it actually fall slightly over time.

The dividend payout ratio of the company hovers between 60% and 50% for the data we have here, and we’re going to keep that for the future.

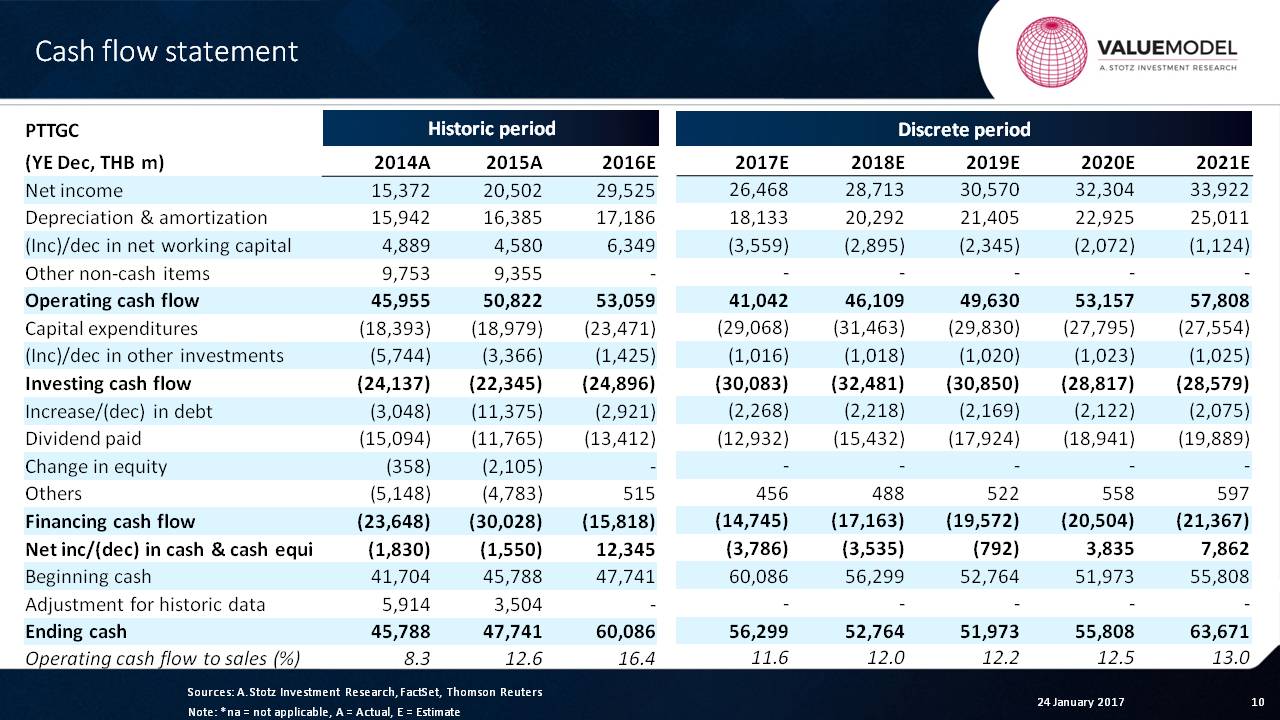

Cash Flow

Next, let’s take a look at the cash flow statement. We can see a massive amount of operating cash flow.

Why is that?

It’s because it’s a heavy fixed-asset business, which means depreciation that gets added back can be very massive.

In this case, they’ve also had gains on net working capital. And so, the result is that the amount of investing cash flow that they’ve had is half of what they’re producing as far as operating cash flow, which leaves a lot of money left to be paid as dividends.

If we go forward, we can see our forecast. And it’s going to maintain its steady growth, and our CAPEX and investment will be strong and flat, but that will always leave enough money to pay a pretty darn good dividend.

We can see operating cash flow as a percent of sales rising here, as recovery in net income happens. Then it’ll reach about 12% or so.

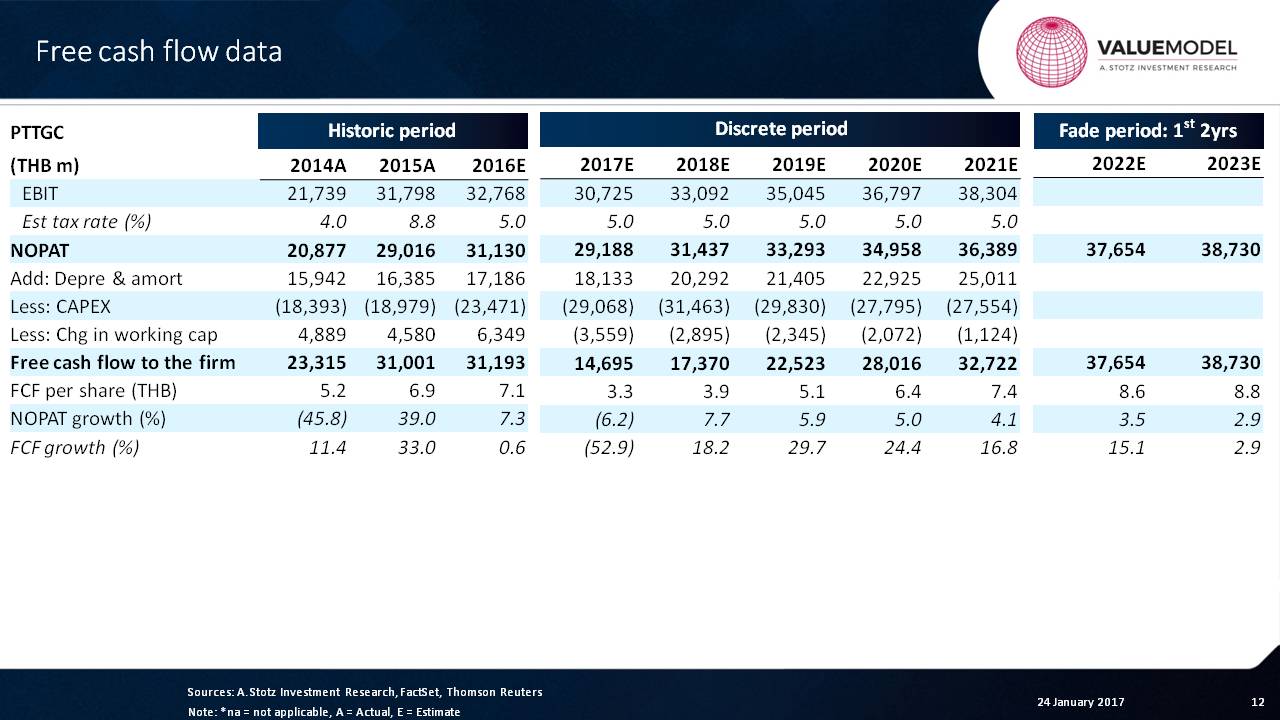

Free Cash Flow

Next, let’s talk about the valuation section of this company.

What we can see is that the NOPAT is always positive. We have this large amount of CAPEX, and we are forecasting change in working capital to be negative over time. So there’s an investment amount that’s pretty significant.

But the end result is that the free cash flow to the firm is relatively strong and rising quite a bit. And so, we see some very strong growth in free cash flow to the firm.

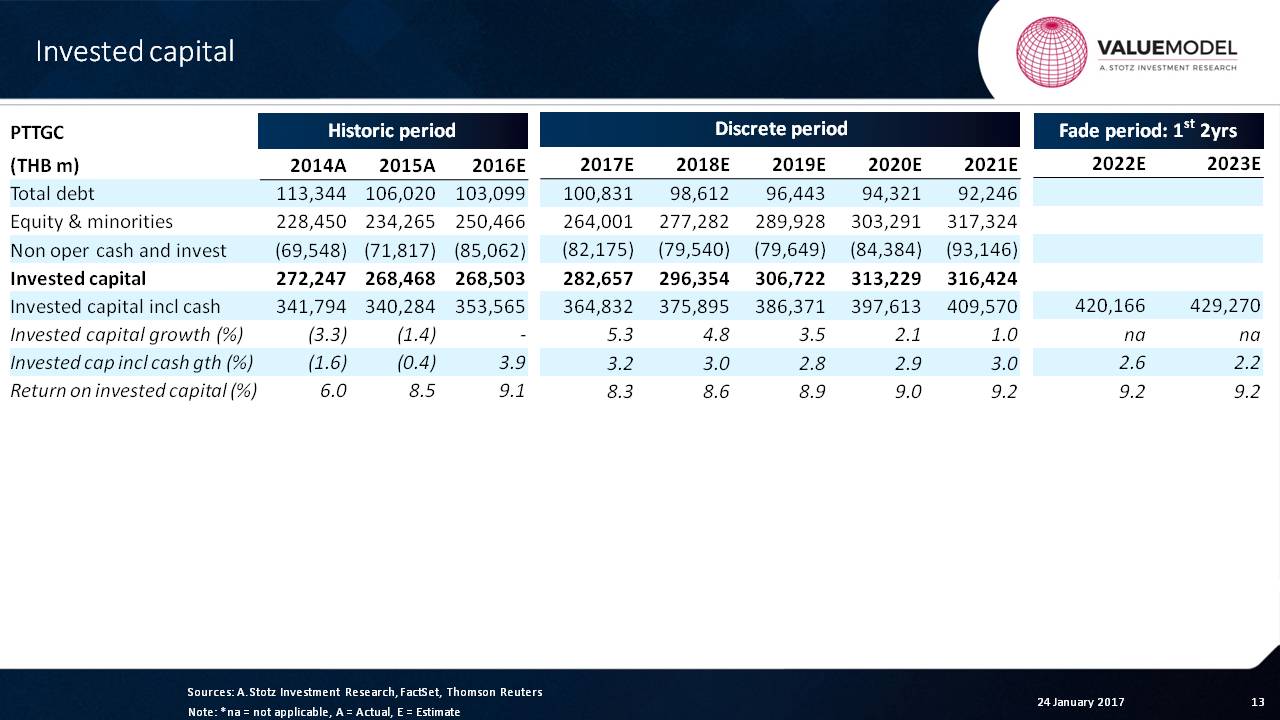

Invested Capital

Continuing on, we can see the invested capital in the business. That’s the debt plus the equity minus the non-operating cash and investments.

So we can see that there’s a pretty steady amount of invested capital in the business. In fact, if we look at the growth rate of invested capital, including or excluding cash, it’s pretty low. And we can see that will continue going forward, based upon our estimates.

As for the return on invested capital, 9% is the peak. It comes down a bit from there and then comes back up. So there’s a reasonable return on invested capital.

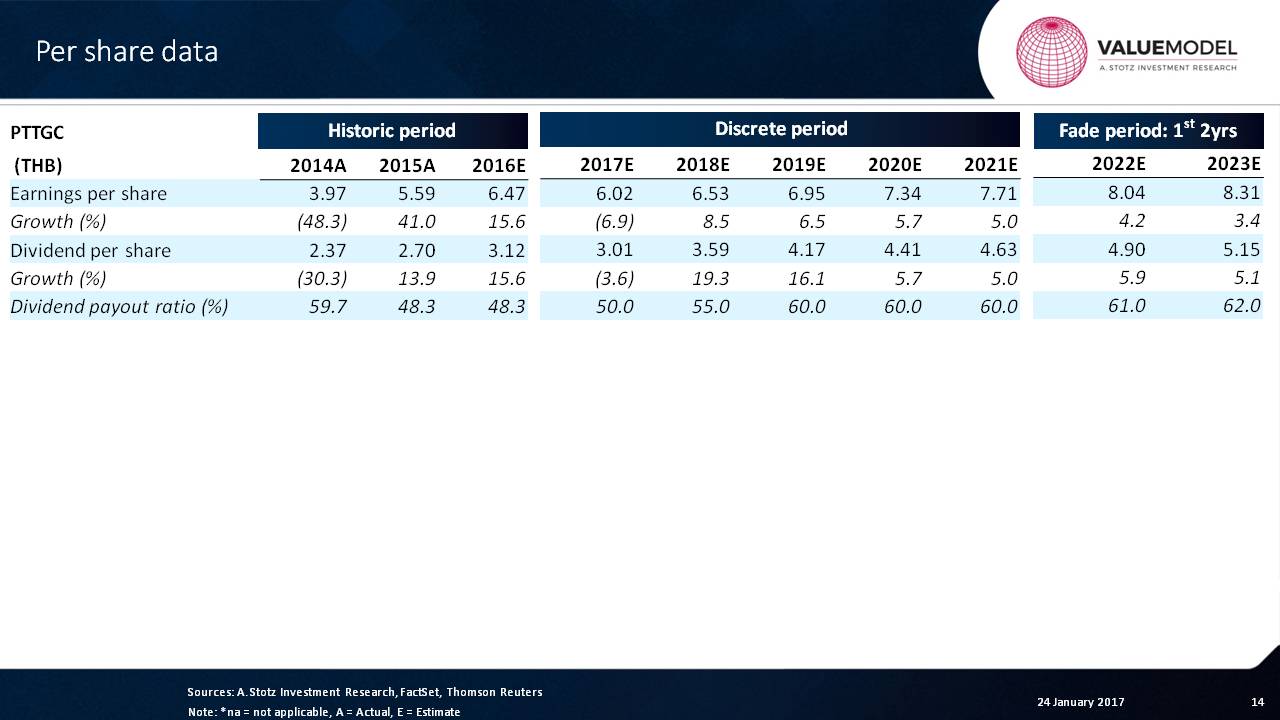

Per Share Data

Now, let’s move on to the next section, the EPS growth. We can see that it’s had a pretty significant recovery, maybe a small fall, and then it’s starting to rise and grow again.

In this case, the dividend payout ratio will be rising and then rising some more.

And so, we will see that the dividend per share will rise by 19% and 16%, which is faster than the EPS growth because of the payout ratio.

If we look at this company, we have our assumptions for Thailand right here: 4% for the risk-free rate and 8% for market premium gives us a market return of 12%.

The company is relatively volatile, so we’re going to give it a 1.25 beta, which is what we put on a company when we think that it is high risk ─ meaning, it’s volatile in its revenue and its earnings. This corresponds to a 14% cost of equity.

In the company’s capital structure, about 77% is coming from equity. So we can see that the company can get a very good cost of debt of 4.4% recently and then, let’s say, up to 5% later on. But they’re always going to get very close to the government rate, because they are partially owned by the government.

And so, the result is that the cost of equity is higher than the weighted average cost of equity right here due to the amount of debt that they have, which is a small amount.

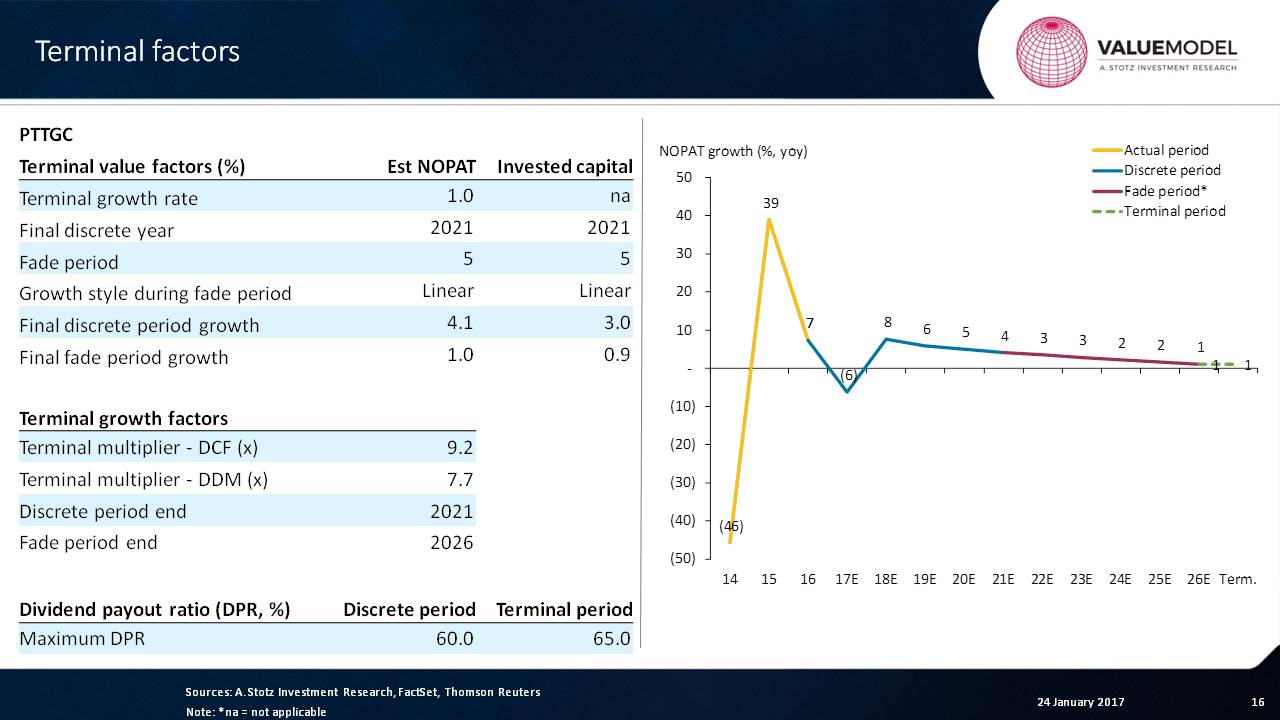

Terminal Factors

If we continue on, we make an assumption of 1% on the terminal growth rate, and we have a 5-year fade period. The fade period, remember, is the red line.

And then, from this, we can see that a final multiple that we use at that point for the terminal value is about, let’s say 8x or 9x ─ a reasonable multiple.

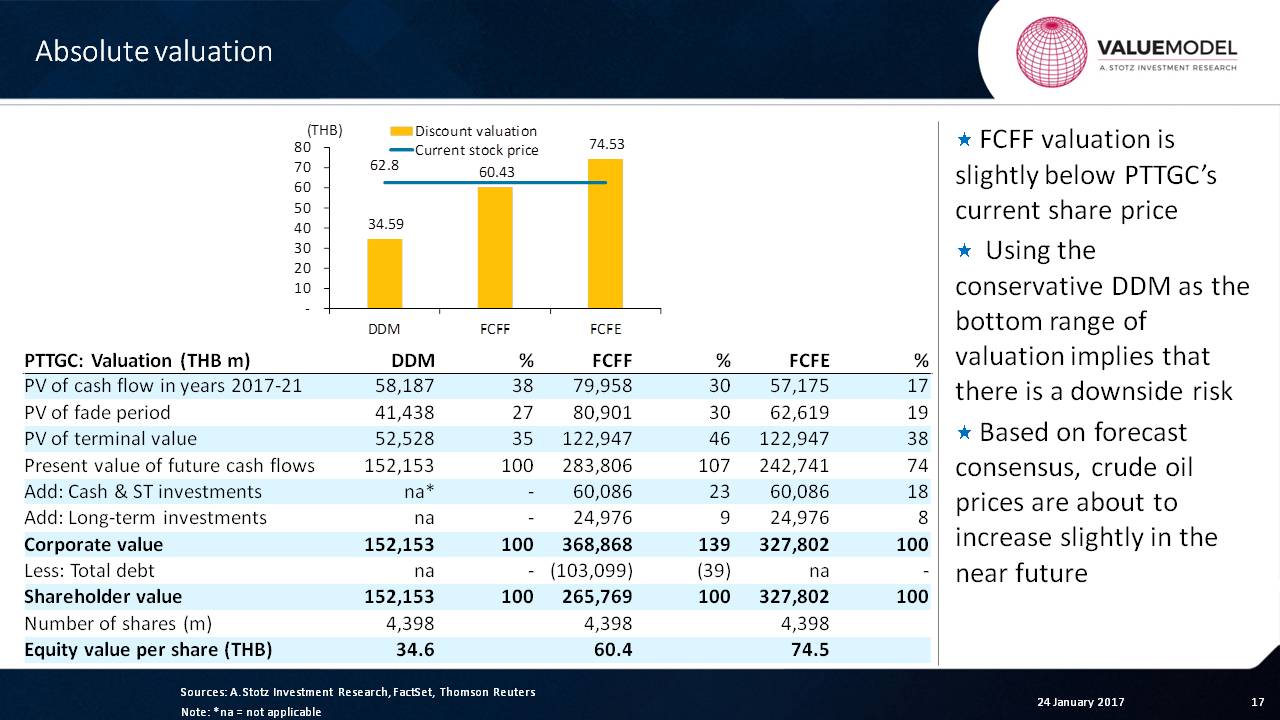

Absolute Valuation

Now, let’s look at what that comes up with from a DDM free cash flow basis and free cash flow to equity basis. These are all absolute valuation measures.

Let’s see what we get.

The first thing I always like to look at is what percent of each of these is coming from that discrete period. And we can see that in the case of the free cash flow to equity, the least amount is coming from this discrete period, and dividend discount is the most that’s coming from that discrete period.

What we can see from this is that we get a range of values from 35 to 75 ─ almost double.

The result is that the price is sort of in the middle of the two. As we almost always see, the dividend discount model output tends to be lower than the share price ─ it’s a conservative measure ─ and the free cash flow to equity, in this case, appears to be the highest.

So is it cheap? Is it expensive?

I’d say it’s kind of “middle of the road.”

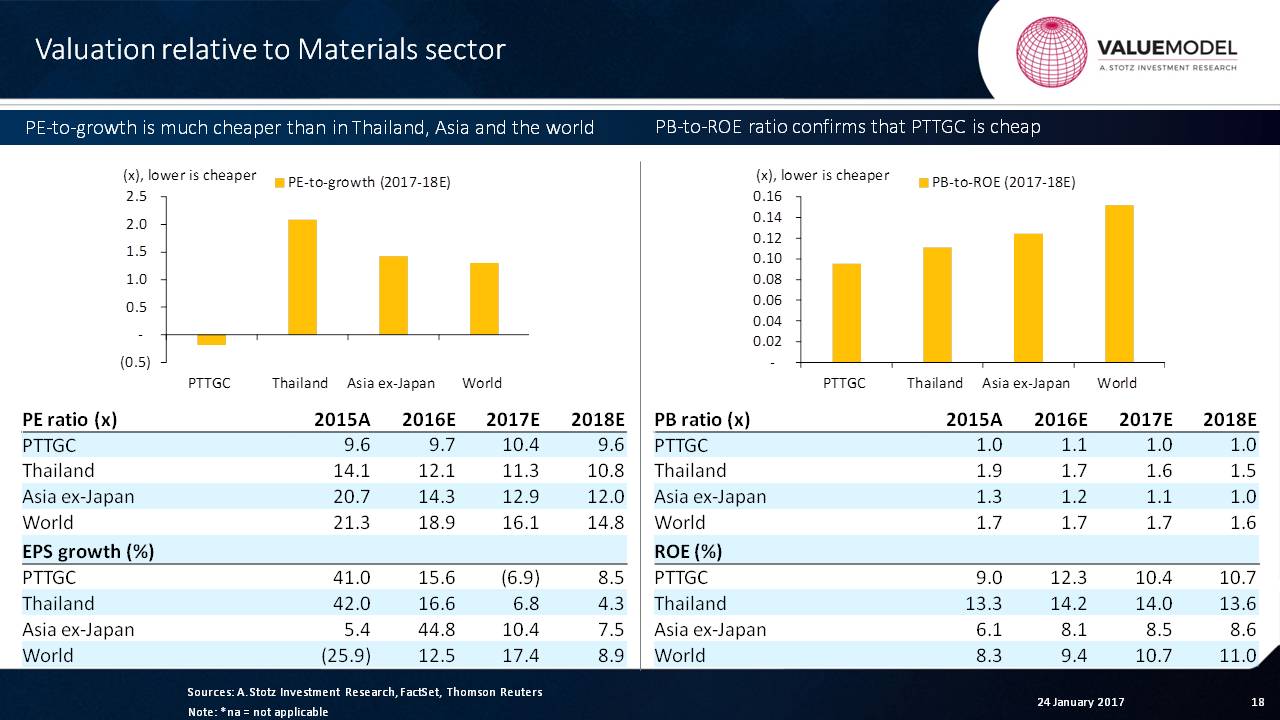

Relative Valuation

Let’s move on to multiples and understand this company relative to its global peers.

The first thing we can see is that the multiple is about 10x, and when we compare that to Thailand, it’s about 11x: so it’s a little bit cheap. Compared to Asia, it’s a little bit cheap and definitely cheaper than most of the world’s materials sector.

We can also see that it had negative earnings growth when Thailand had positive and Asia had positive and the world had positive.

The end result is that this company appears to be attractive, but the truth is that it probably is not that attractive.

On a PEG ratio, it appears to be super attractive, but the fact is that the amount of EPS ─ if you average these two, which we’re doing ─ is pretty low.

So maybe it may make sense, in this case, for an analyst to say, “Well, I’m only going to look at this information for 2018, rather than 2017, because that negative just throws it off.”

That’s up to the analyst, of course.

Now, here we can look on the price-to-book side, and we can see that it’s cheap relative to Thailand but not relative to Asia ex-Japan. In other words, maybe Thailand’s material companies are too expensive. But when we look at it from the world, it’s cheap relative to the world.

And the ROE is slightly lower than Thailand, so that makes sense that it’s cheaper.

But how much cheaper?

That’s where this helps us to see. This is the price-to-book. So how much ROE do we pay for with price-to-book?

We can see from this case that the company is slightly cheap compared to the others.

I’d say that the end result of the valuation is that PTT is moderately attractive.

Now, of course, that’s assuming that our forecasters are correct. They could be wrong in any of our numbers. They could be wrong, and then we’re completely wrong.

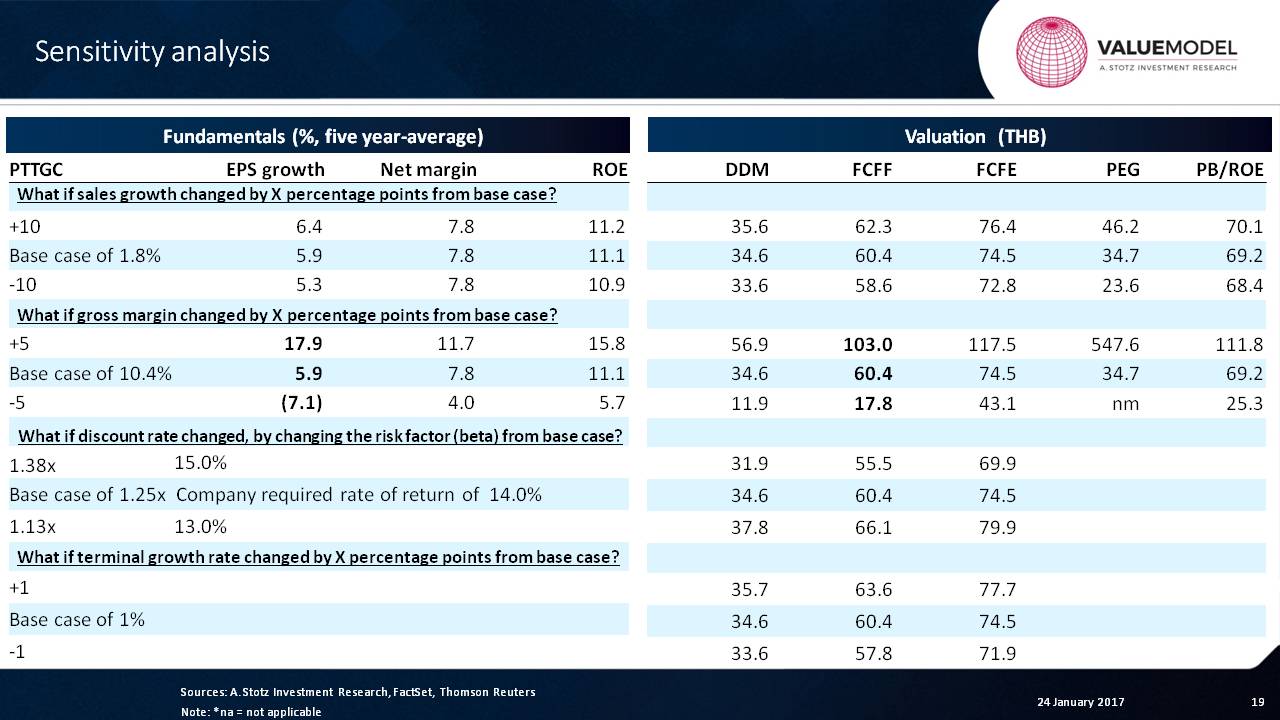

Sensitivity Analysis

This company operates on a really thin gross margin. So if we were to increase gross margin to 15% or to 5%, in this case, we’re going to see a pretty significant fall or rise in the EPS growth.

So there’s a lot of volatility there.

And then, the second thing is that the free cash flow to the firm valuation can vary quite a bit based upon that change.

Remember that we look at: sales growth, margin change, discount rate and terminal growth rate.

There you have it for this company. You can think about it yourself.

Is it cheap? Is it expensive? What do you think?

Let’s keep learning.

Check out the World Class Benchmarking of PTTGC

If you have any questions or comments or experiences with it, leave them below… we want to talk to YOU.