India Equity FVMR Snapshot: ‘India in Your Hand—Every Week’

Watch the video with Andrew Stotz or read about how to use the India Equity FMVR Snapshot below.

India in Your Hand—Every Week

The India Equity FVMR Snapshot uses the same format we first introduced with our Global Equity FVMR Snapshot.

When you sign up, every week you will receive our India Equity FVMR Snapshot, you will always be up to date. You’re going to know all your numbers, as this one-page document covers Fundamentals, Valuation, Momentum, and Risk—our FVMR framework.

You’re going to be professional as this is the same information used by institutional investors and fund managers.

And here’s the best part: You do nothing because after signing up, you’re going to receive a one-page PDF every Monday with updated numbers.

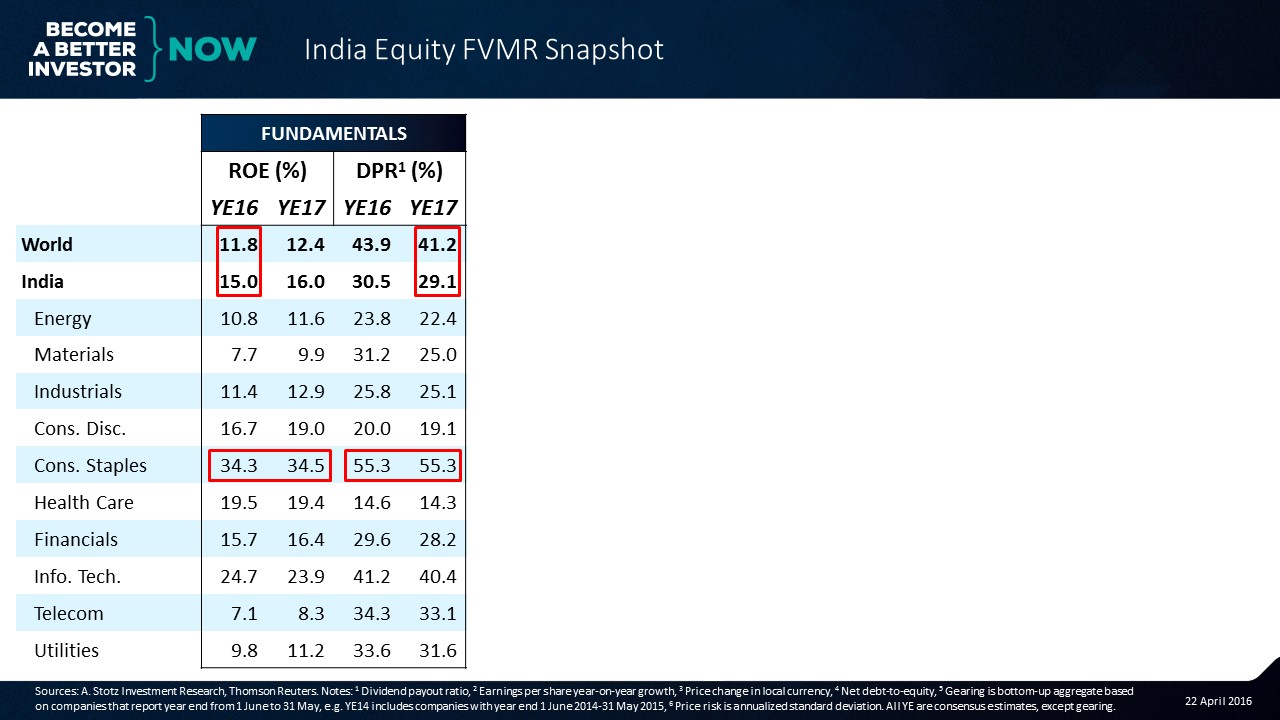

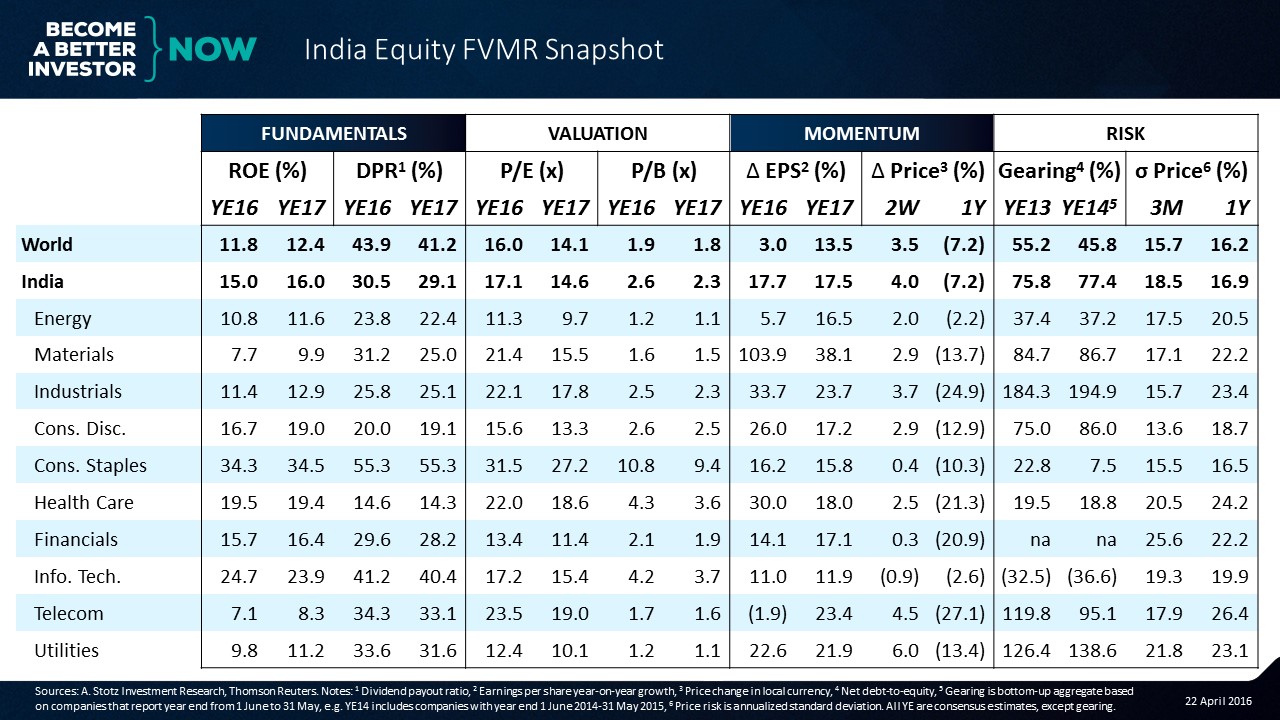

Fundamentals

If we look at the fundamentals of India, we can see that the ROE of the country is at 15% compared to about 12% for the world—a good healthy return premium.

If we look at some of the sectors, we can see that the consumer staples sector is the highest returning sector of all.

The dividend payout ratio is much lower than the rest of the world and that’s mainly because it’s a fast growing and a highly profitable economy. So it probably makes little sense for these companies to pay out their dividends. To put the proceeds into a bank doesn’t make sense either.

We can see that some sectors such as consumer staples which is making much money also has a pretty massive 55% dividend payout ratio.

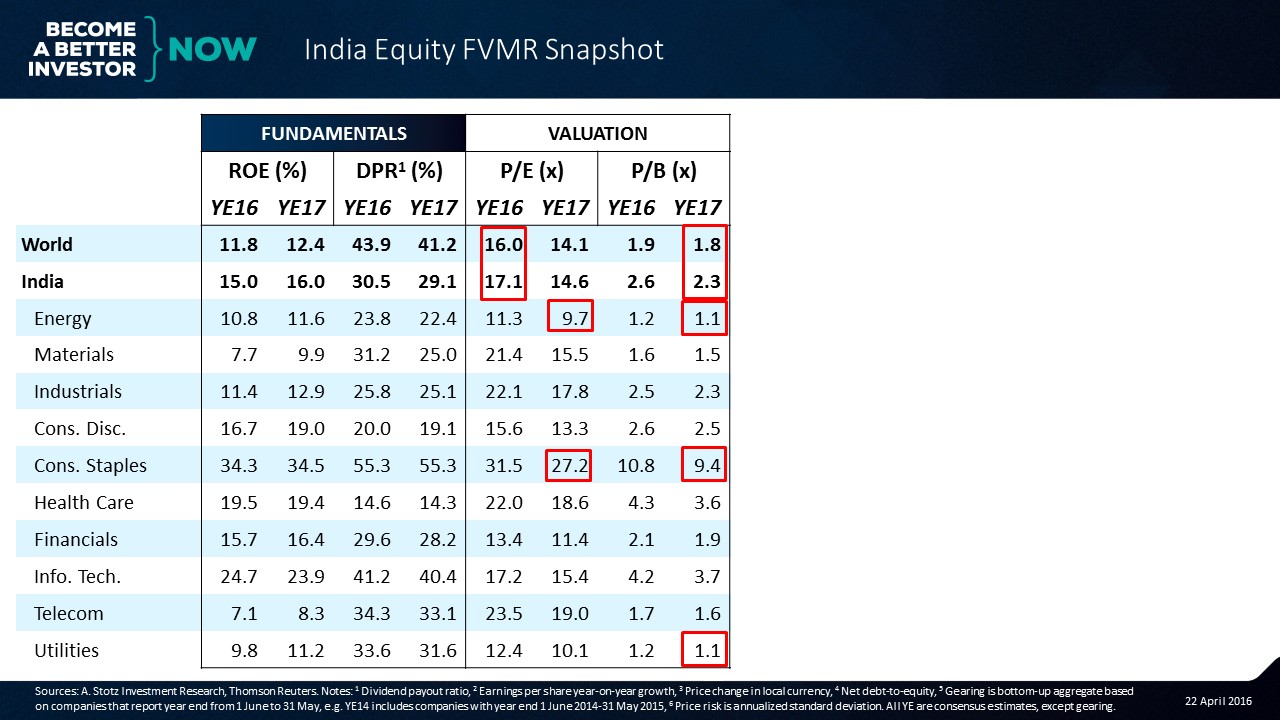

Valuation

Now, let’s look at valuation.

Next, we can see that the P/E of India is only slightly higher than the rest of the world, so you get a good fundamental premium and a tiny P/E premium.

We can see that some sectors are very cheap such as the energy sector but, of course, we know that energy tends to be very cyclical. The consumer staples which we’ve talked about as a very profitable sector is an expensive sector, too, at 27x; but that’s expensive across the world at this point.

Now, the price-to-book of India is also at a slight premium at 2.3x versus 1.8x for the world; and we can see that some sectors such as energy are very cheap. Another sector that looks very cheap is the utility sector. Furthermore, we can see that the consumer staple sector is trading at almost 10x price-to-book; that’s a very pricey price-to-book. But if the returns are there, it could be sustained.

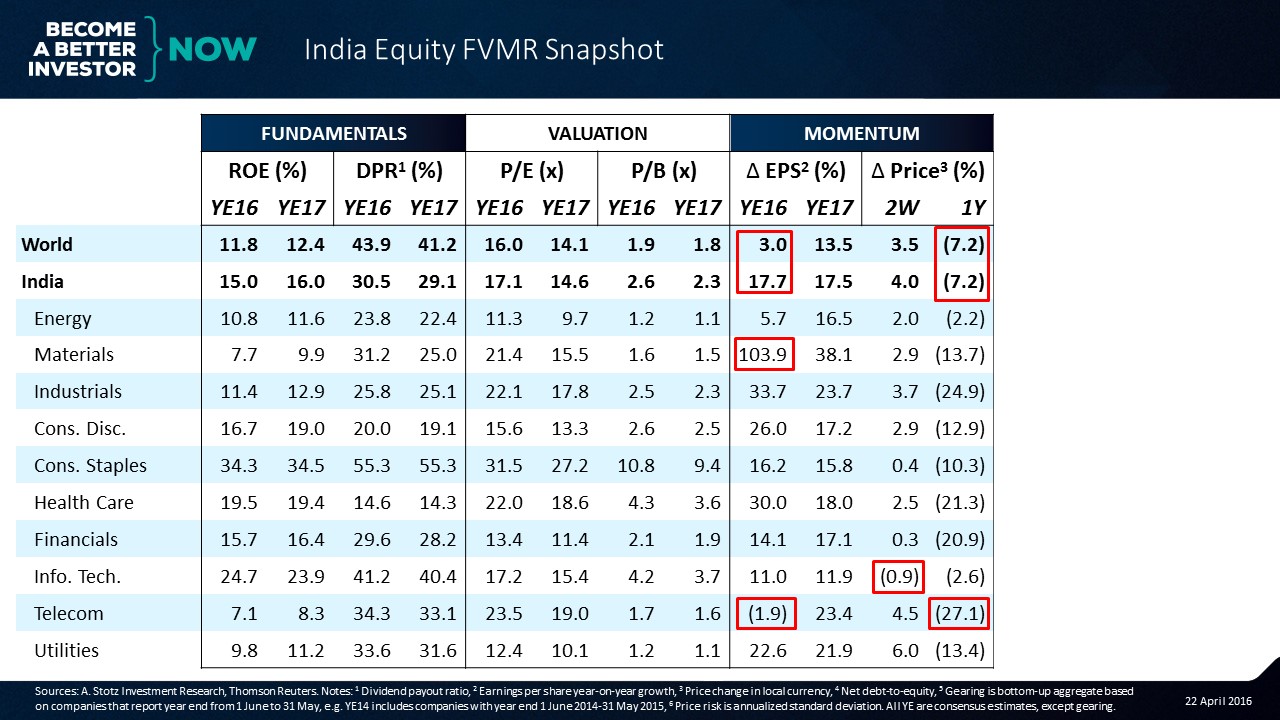

Momentum

Now, let’s look at momentum in both earnings and price.

The momentum in earnings is very strong in India relative to the rest of the world, and we can see some sectors where it’s strong such as materials and some sectors where it’s weak such as telecoms.

Price movement has been about in line with the rest of the world over the last year. And so, what we can see is that the decline in price has made India a little bit cheaper; and since fundamentals are strong, there’s a good opportunity there.

We can also see that price momentum in some of the sectors such as info tech has over the last two weeks been coming down, and the telecom sector over the last year has had a massive price fall of 27%.

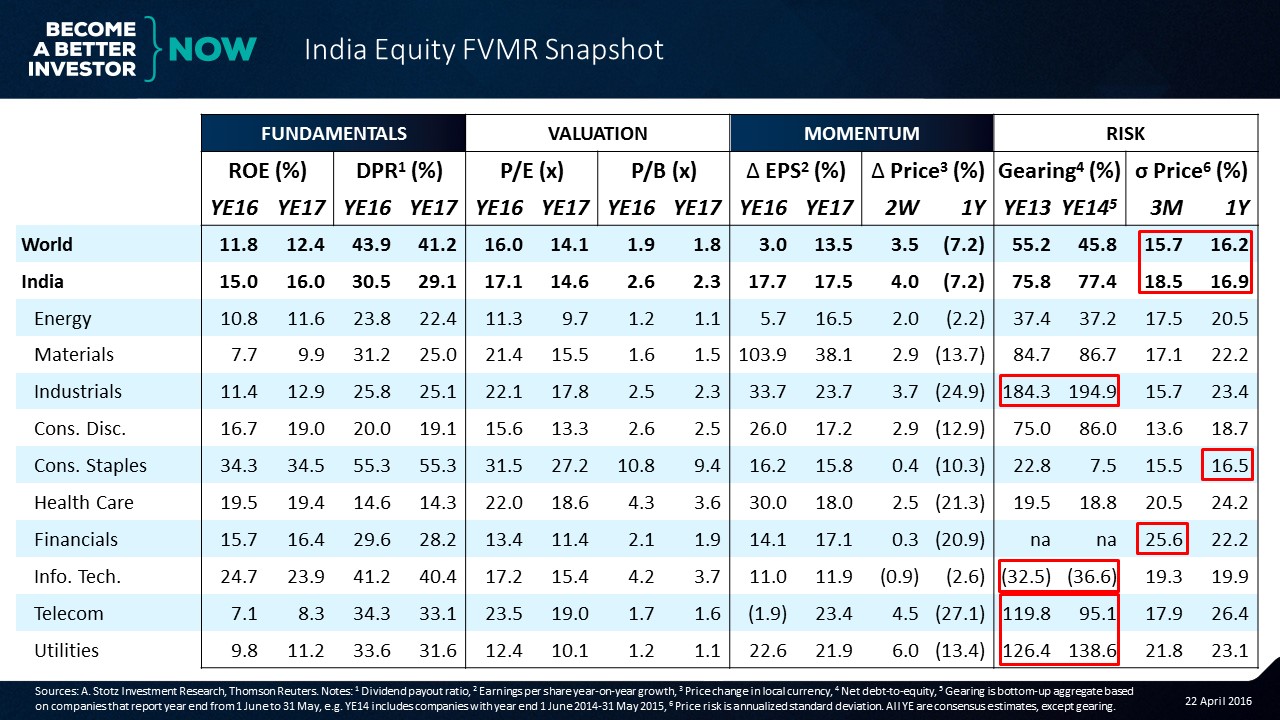

Risk

Let’s continue on to risk to understand the balance sheet and price risk of the companies. What we can see is that the gearing in India is quite high at about 75% relative to about 55% or 45% in the world.

Some sectors such as industrials are massively geared. Usually, this is because there is some distress in the industry. We’ve got some companies such as info tech companies that tend to not have a lot of assets; therefore, they have a lot of cash on their balance sheet and they have little or no debt. Resulting in a negative number for gearing (net debt-to-equity).

Telecoms and utilities tend to be highly leveraged in India. That’s much different than the rest of the world where they have a lot less leverage.

If we look at price volatility, we can see that India’s price volatility is about in line with the world’s volatility. Comparing a country’s volatility to the world is a little bit distorting because a country has fewer constituents in it. So I would say that the volatility of India looks very good. There are some volatile sectors such as the financial sector and there are some low volatility sectors such as consumer staples.

India in Your Hand

With our India Equity FVMR Snapshot, you’ll get a weekly update like the one below covering the Indian stock market.

You’re going to understand fundamentals, valuation, momentum, and risk, and the way we look at them.

After signing up, YOU will:

-

Always be up to date: Every week you will receive the updated India Equity FVMR Snapshot

-

Know all the numbers: One page covers Fundamentals, Valuation, Momentum, and Risk (FVMR)

-

Be professional: Use the same information as institutional investors and fund managers

-

Not have to do anything else to stay informed: After signing up you will receive a one-page PDF every Monday

The India Equity FVMR Snapshot is free for everyone signing up within a limited time period. Sign up now to not miss out on getting it for free.

NOTE: You’ll have to fill in the form below to receive the India Equity FVMR Snapshot even if you’re already subscribing to other Equity FVMR Snapshots and/or is a founding member that get our newsletter.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.