Can FedEx Hit $300 Again?

The post was originally published here.

What’s interesting about FedEx is that its margin is half of its main competitor UPS

3 things to know about this company:

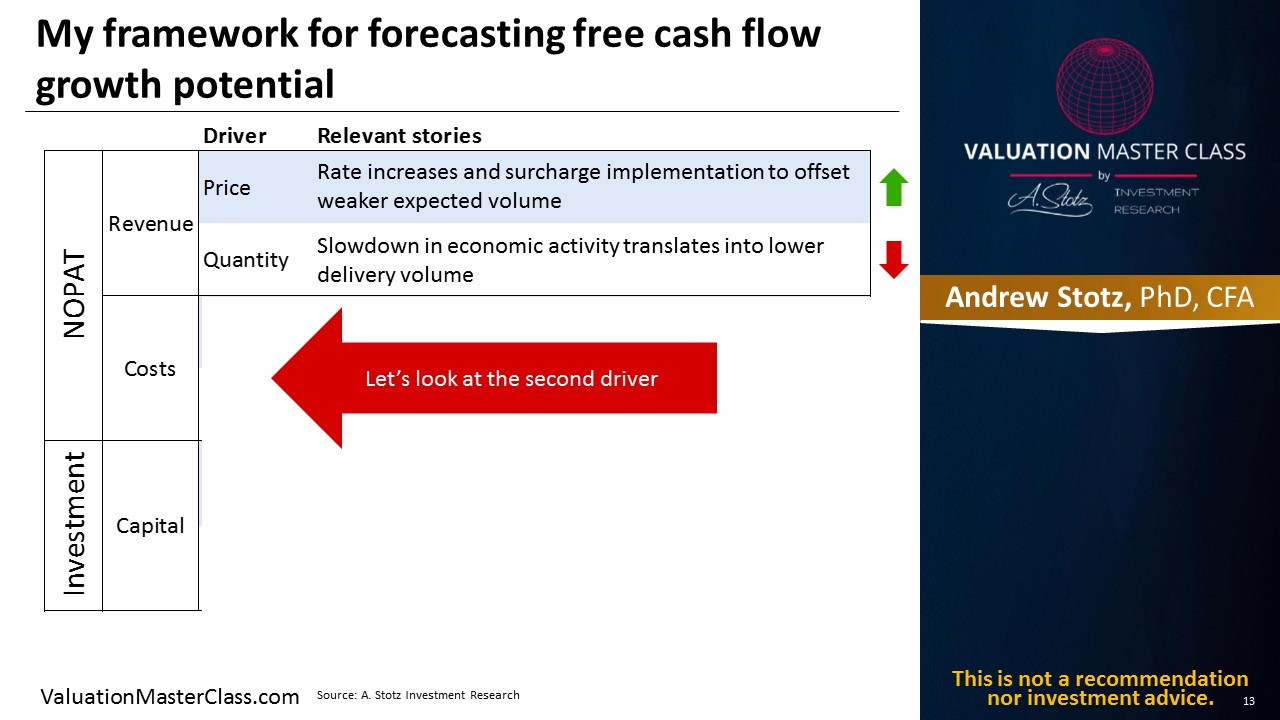

- Weak demand squeezes volume requiring price increases to keep revenue on track

- Accelerating cost-cutting program makes margin expansion key catalyst

- Reducing capital spend could help to improve shareholder returns

Download the full report as a PDF

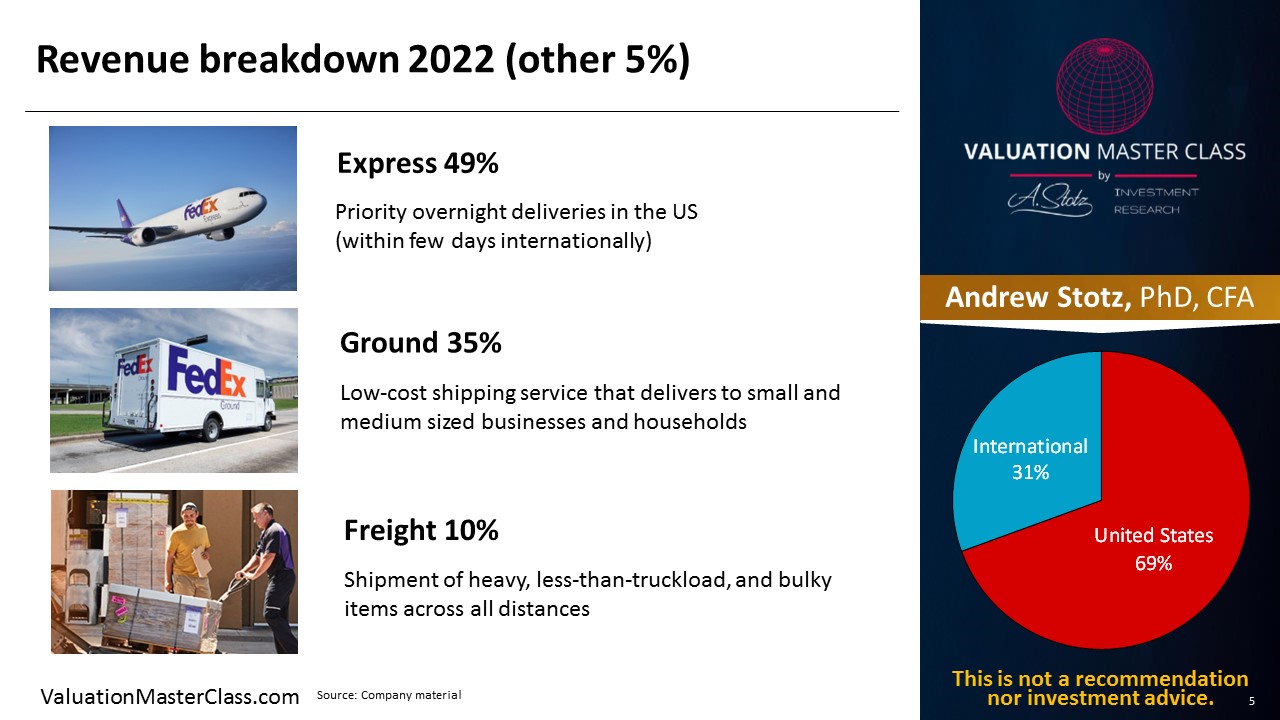

Revenue breakdown 2022 (other 5%)

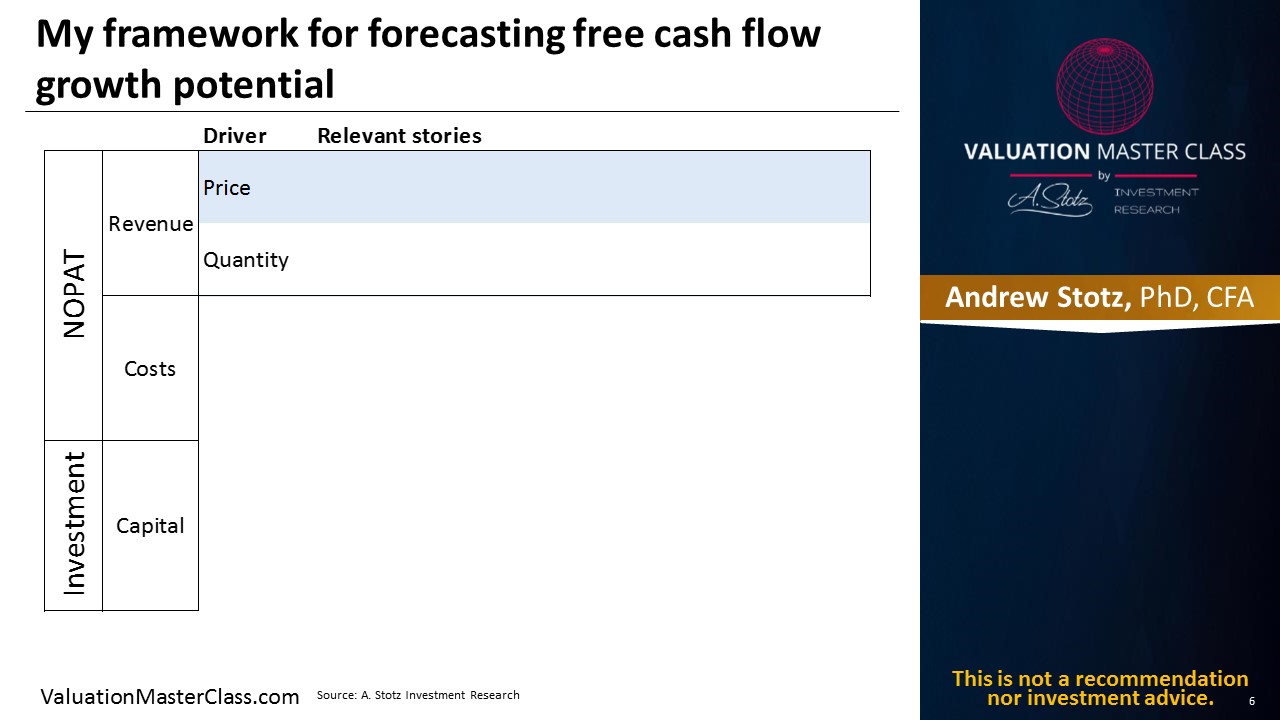

My framework for forecasting free cash flow growth potential

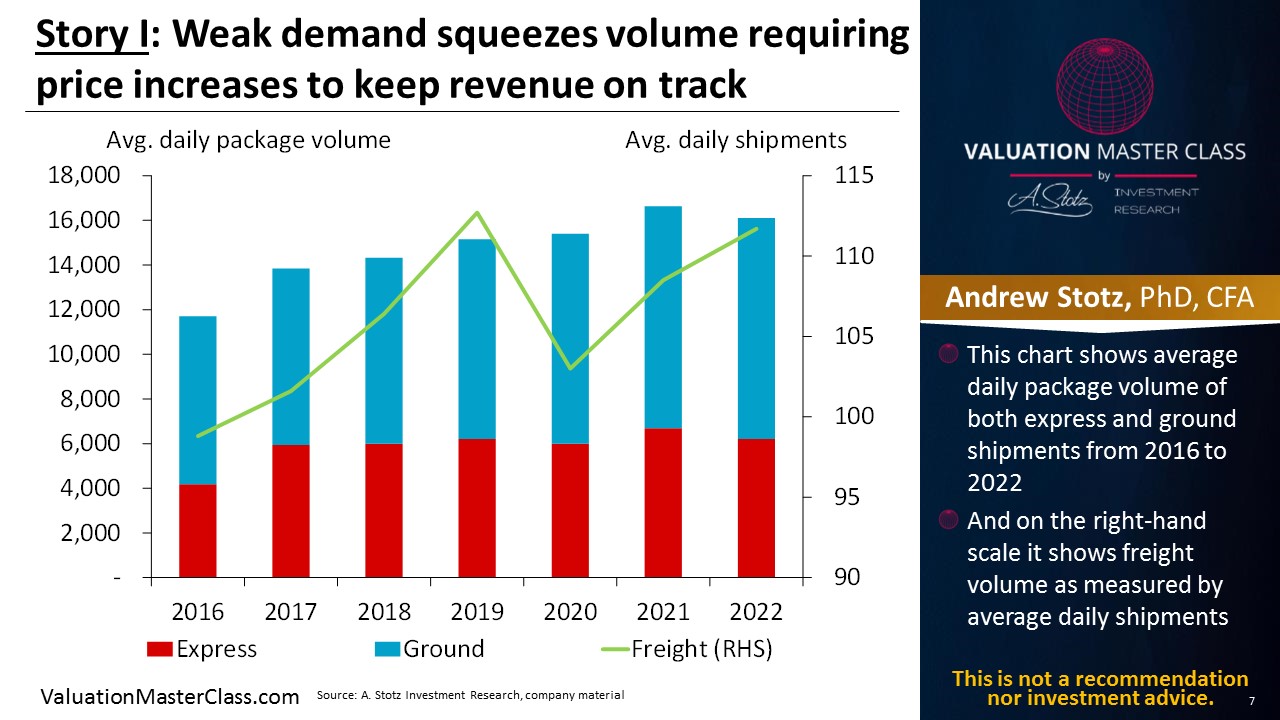

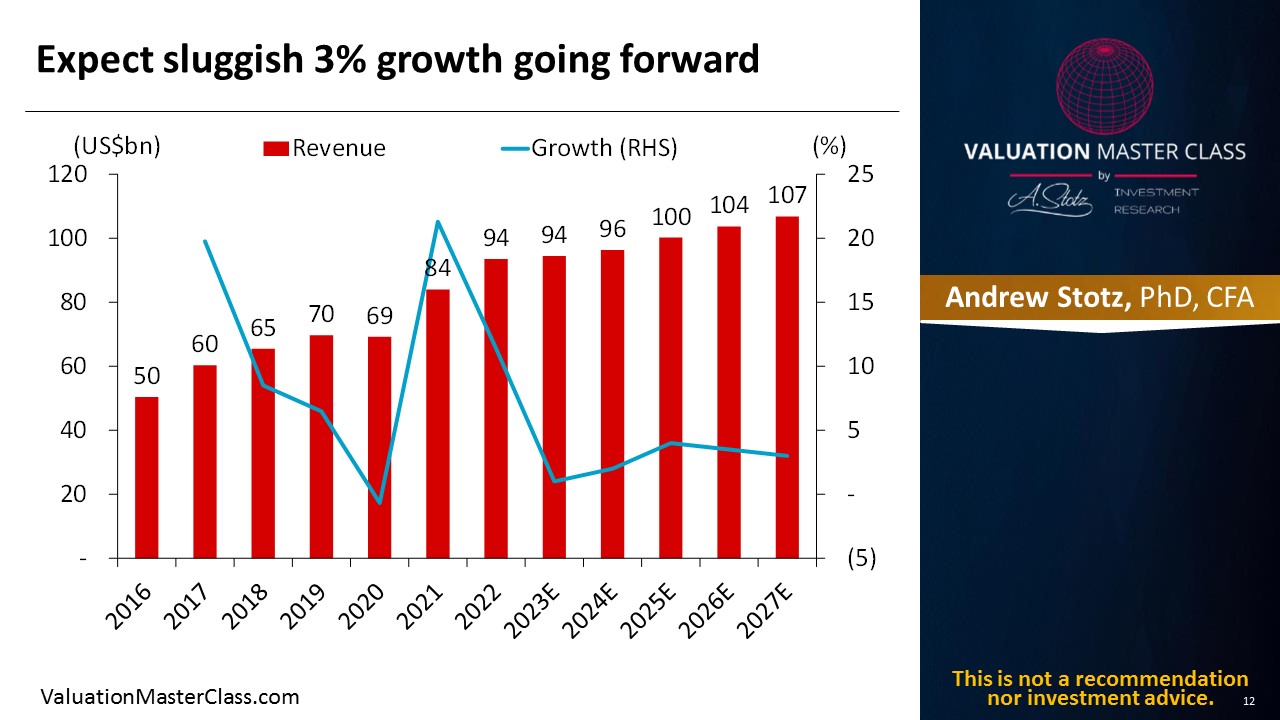

Story I: Weak demand squeezes volume requiring price increases to keep revenue on track

- This chart shows average daily package volume of both express and ground shipments from 2016 to 2022

- And on the right-hand scale it shows freight volume as measured by average daily shipments

- Over the past 6 years, FedEx was able to expand its avg. daily volume of Ground and Express services from 12,000 to 16,000 packages

- Its freight segment (green line) has recovered to pre-pandemic levels and stands at 112 daily shipments

- However, the YoY comparison of the recent months shows that volume started to decline

- For example, domestic Express packages volume was down 16% in Nov’22

- The management expects weak demand throughout 2023 as well

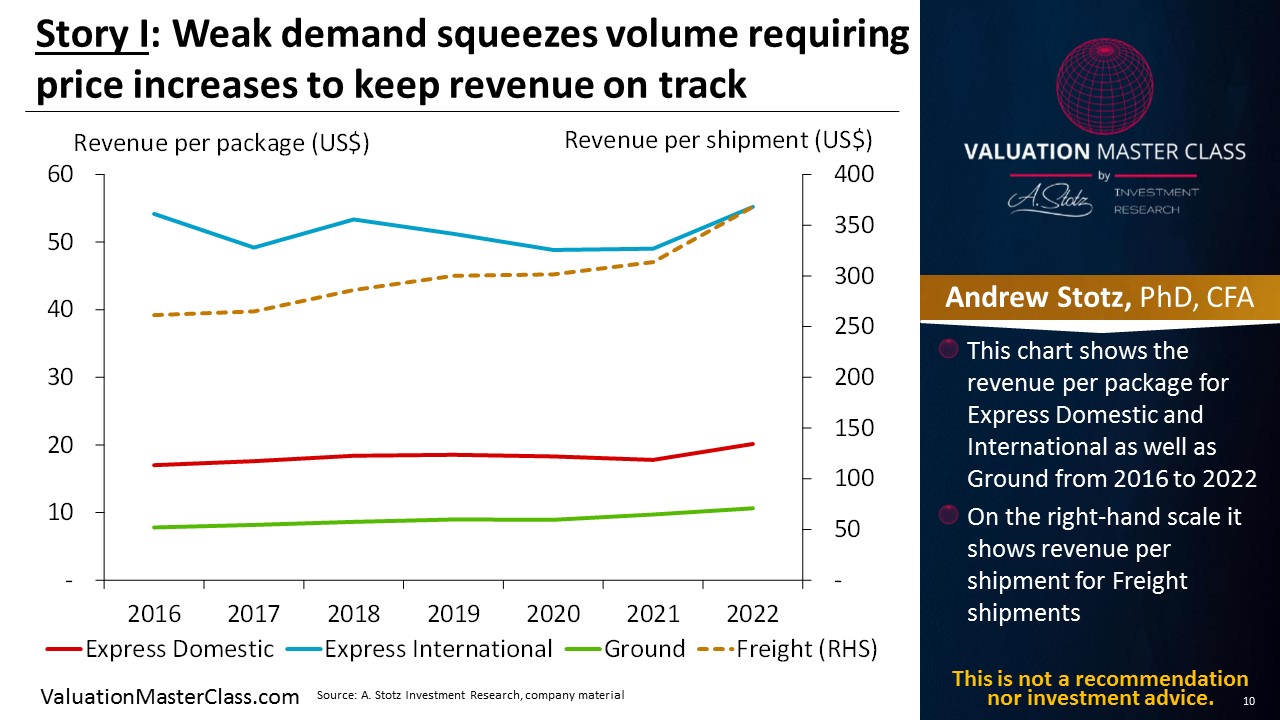

- This chart shows the revenue per package for Express Domestic and International as well as Ground from 2016 to 2022

- On the right-hand scale it shows revenue per shipment for Freight shipments

- The avg. revenue per package has been mostly stable and flat among all transportation methods

- Only freight rates saw good consistent hikes

- Though, in 2022, FedEx raised the prices of ground and express services to offset inflation effects

Expect sluggish 3% growth going forward

My framework for forecasting free cash flow growth potential

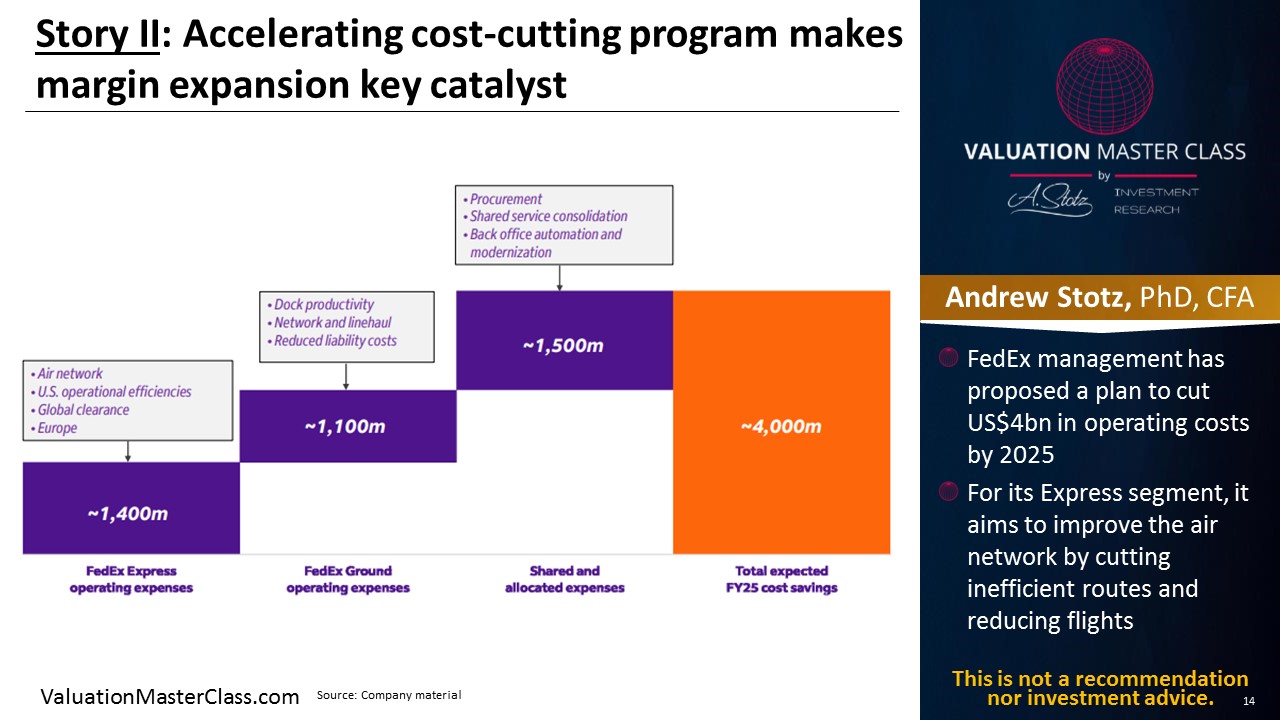

Story II: Accelerating cost-cutting program makes margin expansion key catalyst

- FedEx management has proposed a plan to cut US$4bn in operating costs by 2025

- For its Express segment, it aims to improve the air network by cutting inefficient routes and reducing flights

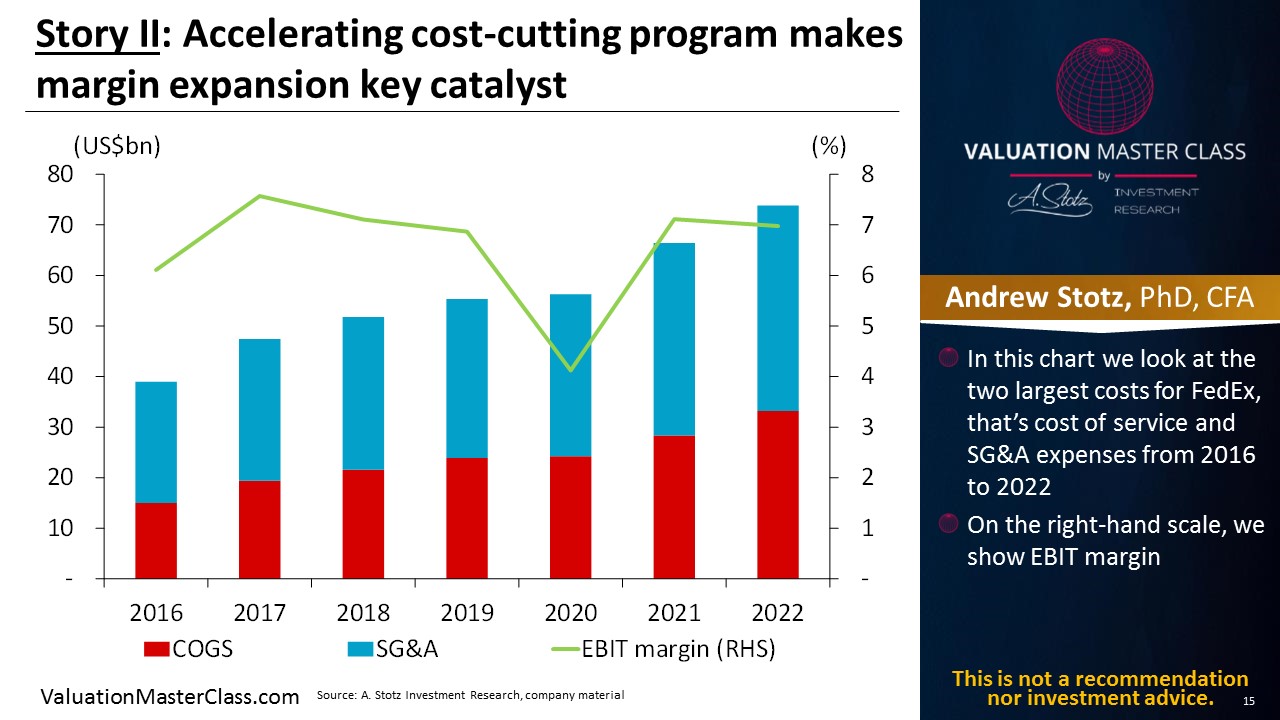

- In this chart we look at the two largest costs for FedEx, that’s cost of service and SG&A expenses from 2016 to 2022

- On the right-hand scale, we show EBIT margin

- The EBIT margin has been stable, ranging between 6-8%, except for 2020 when it got cut nearly in half

- Its main competitor, UPS enjoys a 13% operating margin

- Hence, there is room for FedEx to improve

My framework for forecasting free cash flow growth potential

Story III: Reducing capital spend could help to improve shareholder returns

- This chart shows total capital expenditures from 2014 to 2022

- And on the right-hand scale, we show CAPEX as a percent of revenue

- Over the past 9 years, FedEx’s CAPEX/revenue averaged 8.2%

- However, it started to show a declining trend in line with the company’s mission to employ capital more efficiently

- The goal is to bring it down to 6.5% by 2025

My framework for forecasting free cash flow growth potential

Simplified valuation

- Finally, we divide this by the number of shares to arrive at our value estimate per share

Get financial statements and assumptions in the full report

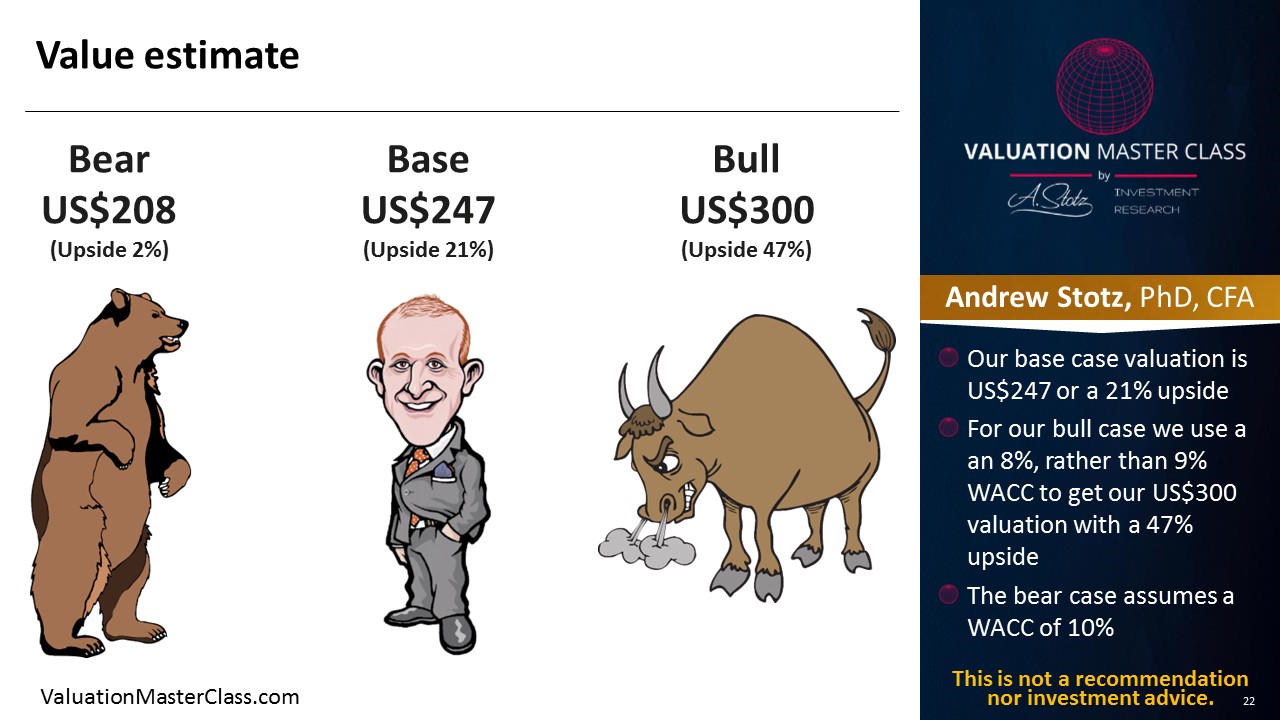

Value estimate

- Our base case valuation is US$247 or a 21% upside

- For our bull case we use a an 8%, rather than 9% WACC to get our US$300 valuation with a 47% upside

- The bear case assumes a WACC of 10%

Download the full report as a PDF

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.