Following Recognition of Bad Loans, India’s Banks are Struggling

With news of bad loans mucking up the Indian banking system throughout 2016, the Reserve Bank of India set a March 2017 deadline for banks to release all data on non-performing loans.

The data that has been released thus far, however, won’t steady the nerves of investors.

Backstory

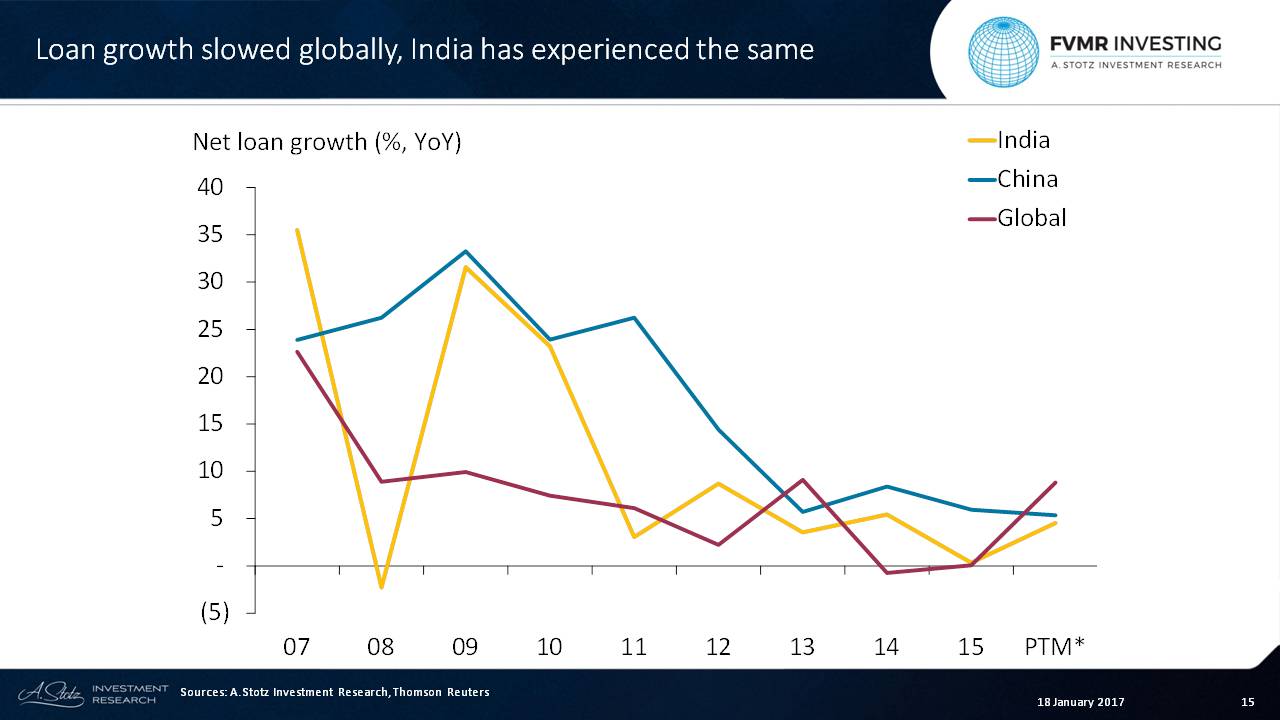

Since the global financial crisis of the 2007-2009 period, global net loan growth has trended downward toward zero with just a slight uptick over the last year.

China experienced slightly above average loan growth over that period, but recently both it and India have fallen below the global average.

Both Indian and global banks experienced a flat 2015. In fact, as you can see below, only the crisis year of 2008 was worse for India.

Banks in the largest emerging countries, India and China, have much higher net interest margins.

This core profitability, however, began to fall in China while rising in India in 2014. Since then the trend has only continued.

The Verdict

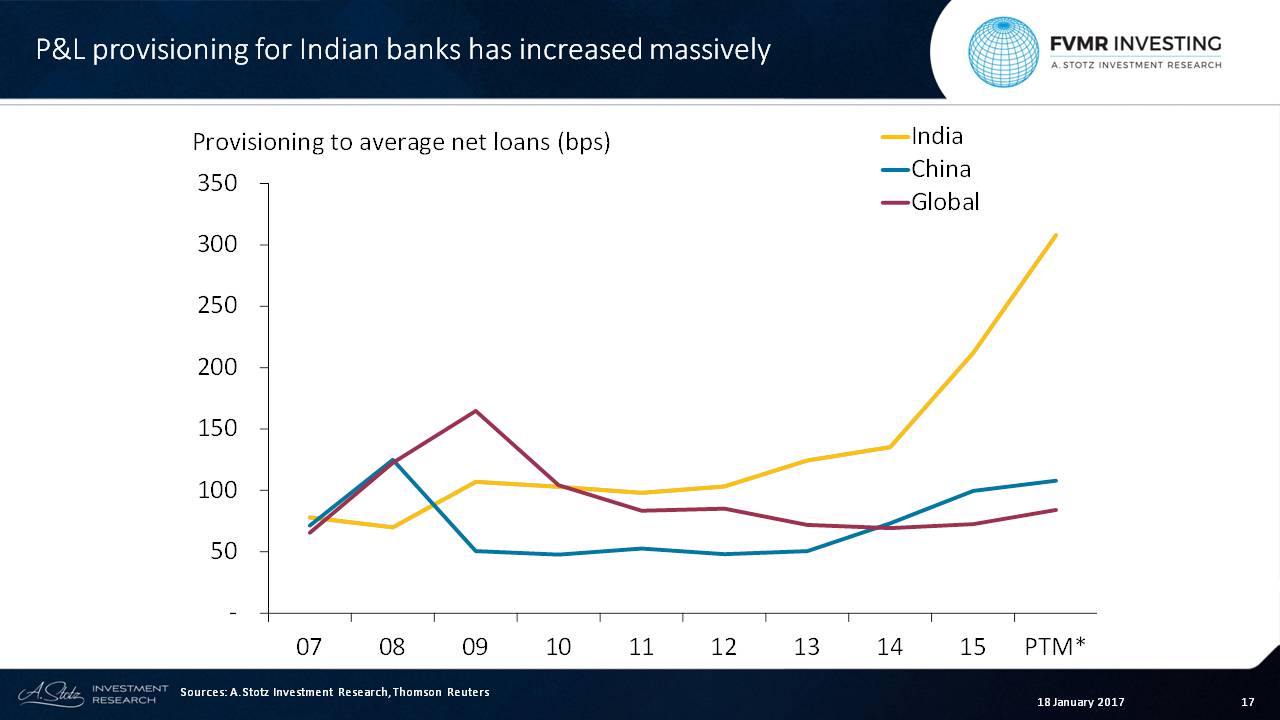

The news would appear to be positive for Indian banks, except that provisioning has grown enormously in recent years, giving the impression that bank executives are worried about the quality of their loan books.

The worries only increase when one notices that provisioning has been flat globally since 2013 while increasing in India ever since.

Provisioning began to increase massively in India in 2015, following government’s attempt to deal with legacy issues in the banking industry.

The Reserve Bank of India has forced Indian banks to recognize more of its non-performing loans.

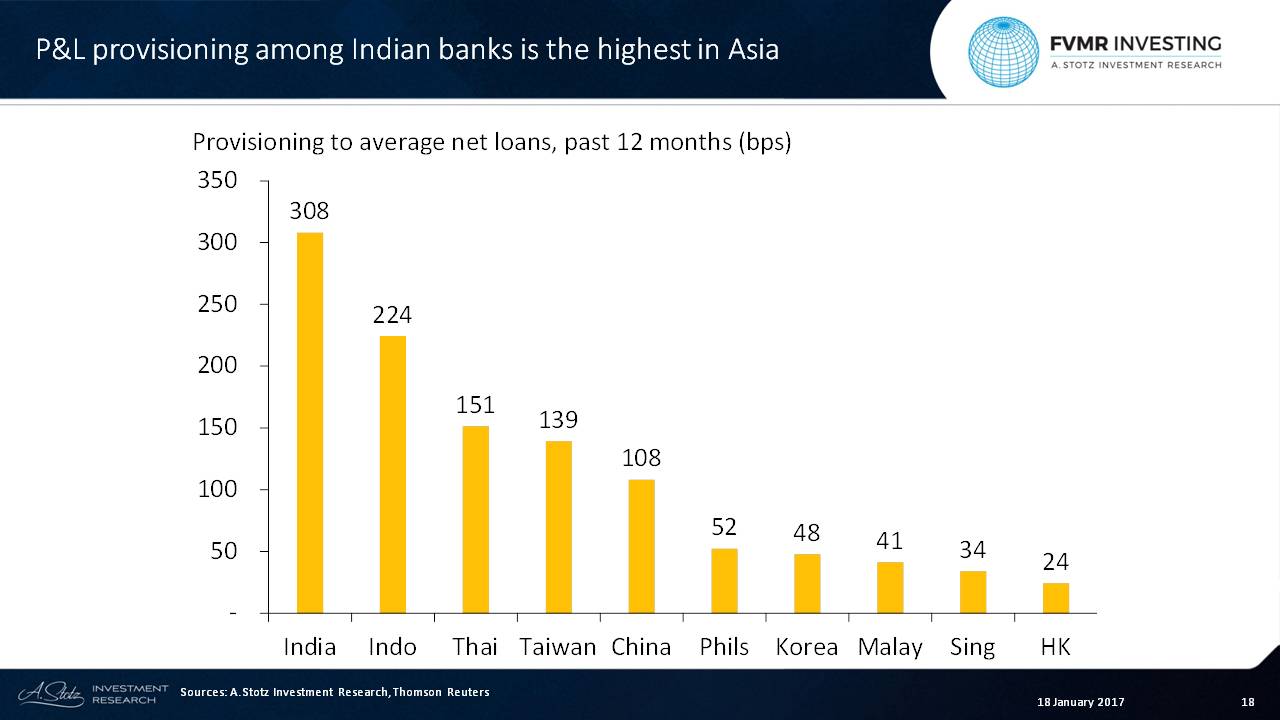

The issue is so large that provisioning in India now sits more than twice as high than all other countries in Asia besides Indonesia.

A challenge for the government is that state banks sit on almost 90% of the system’s bad loans, as of the first half of 2016.

Indian GDP slowed in the third quarter of 2016 and could continue to slow as the government is likely to take most of the hit.

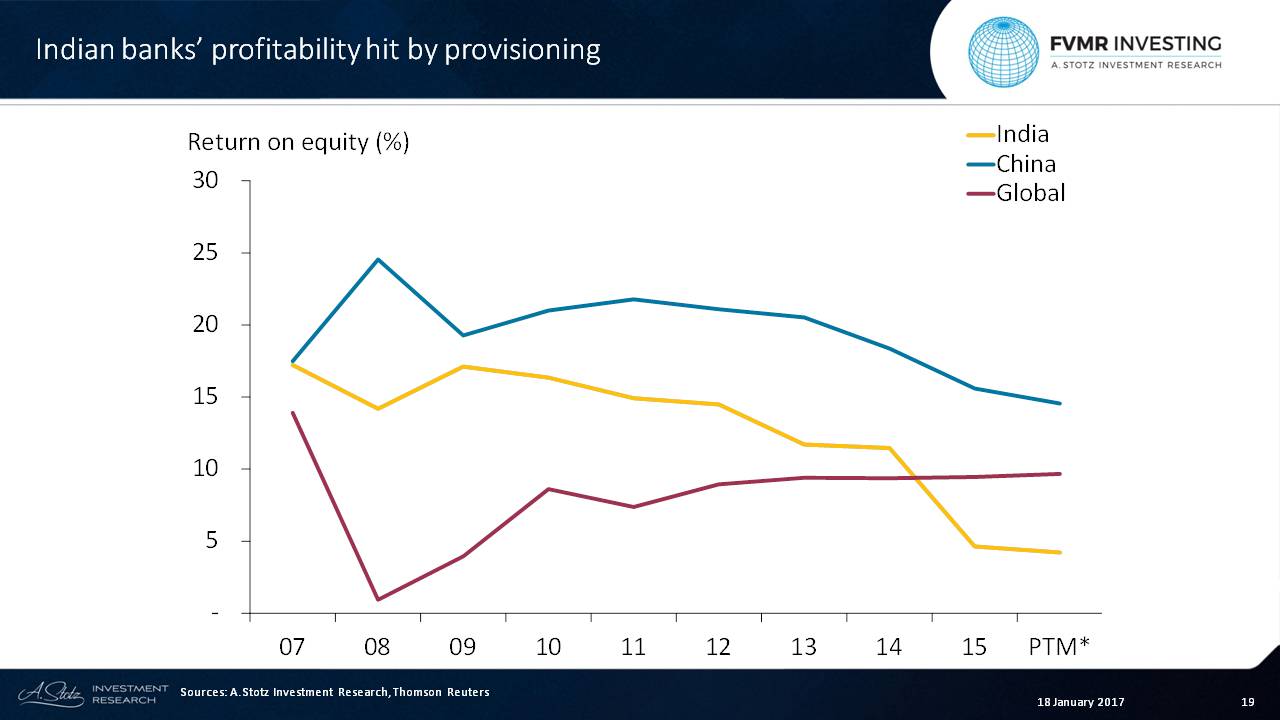

Looking at return on equity, the ROE of global banks has been stable since the recovery following the global financial crisis.

Chinese bank profitability has fallen since 2011 but is still significantly higher than the world at large. Indian banks suffered by the need for provisioning, which caused ROE to fall below 10% for the first time during this period.

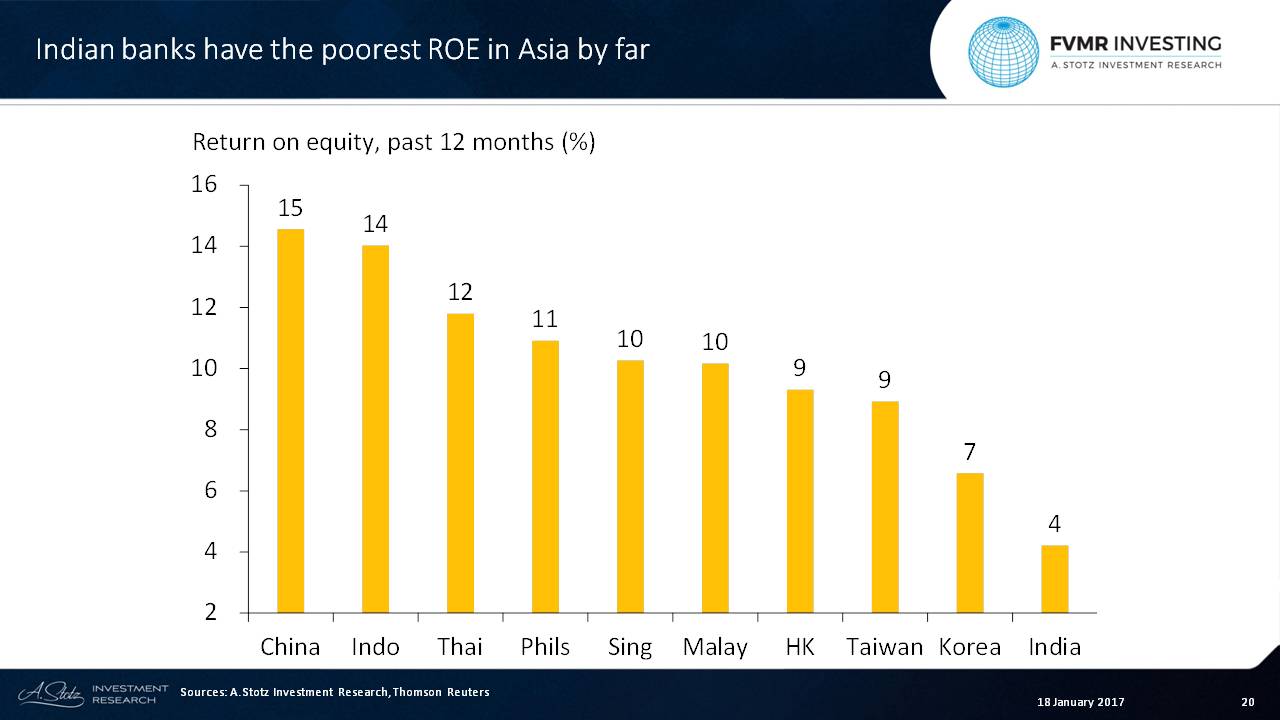

While the Indian stock market as a whole beat Asia and the World in terms of ROE in the past 12 months, the story for Indian banks differ.

First, return on equity among Indian banks is almost half that of the second lowest country Korea, at only 4%. Chinese banks, on the other hand, are still delivering a strong ROE of 15%. The ROA of Indian banks was above Chinese banks in 2009 but has fallen ever since.

When Indian banks were forced to recognize more non-performing loans, the provisioning led to a much worse return on assets ratio than the global average for the first time in recent years.

The global tier one capital ratio increased after the financial crisis, following the Basel III regulatory agreement, where minimum tier one capital was set at 6%. Indian and Chinese banks are above the minimum requirements but still below the global average. This stands in contrast to other Asian countries’ banks that have a tier one capital ratio in line with or above the global average.

Still, tier one capital improved in 2015, in contrast to other ratios among Indian banks. India and China are exceptions, together with Taiwan and Korea.

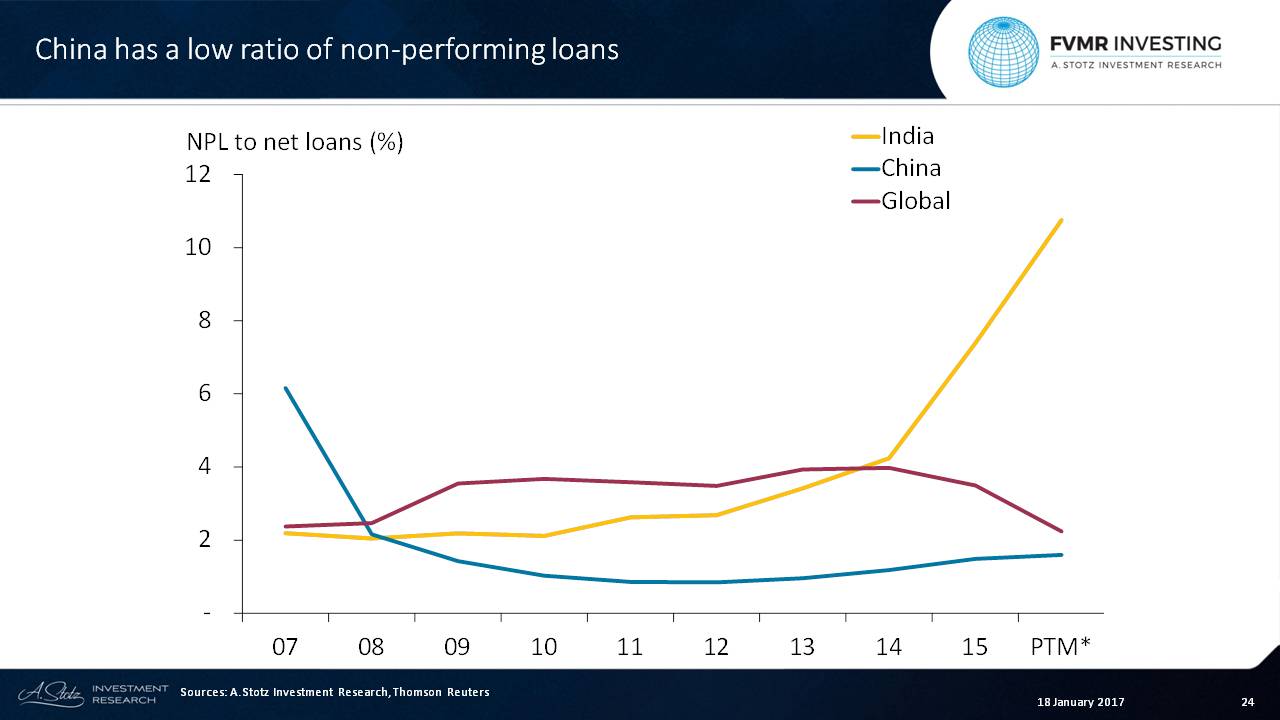

China had a low ratio of non-performing loans (NPL) until recently when NPLs decreased globally but increased in China.

India has seen a low NPL-to-net-loans ratio of about 2% prior to the recent recognition of bad loans, but now it’s above 10%.

India’s high NPL-to-net-loans ratio isn’t seen in the rest of Asia. Most Asian banks’ ratio sits around 2% or less, though Thailand and Indonesia are a bit higher.

DISCLAIMER: This content is for information purposes only. It is not intended to be investment advice. Readers should not consider statements made by the author(s) as formal recommendations and should consult their financial advisor before making any investment decisions. While the information provided is believed to be accurate, it may include errors or inaccuracies. The author(s) cannot be held liable for any actions taken as a result of reading this article.